An unexpected bill hits, the plumber only takes cash, or your debit card is stuck at home. In moments like these, many Citi cardholders wonder if their credit card can help. You may know the card can pull cash from an ATM, but the exact process, PIN setup, and true price tag stay unclear. If that sounds familiar, this quick walkthrough on how to get a cash advance on a Citi credit card will clear things up.

To get a cash advance on a Citi credit card, request a PIN, then withdraw funds at any ATM, visit a bank teller, or use a Citi convenience check.

Keep reading for step-by-step actions, real dollar-cost examples, limits, fees, and expert-level tips to keep your cost as low as possible.

At a Glance

This guide explains how to get a cash advance on a Citi credit card through ATMs, bank tellers, direct transfers, and convenience checks, including PIN setup, fees, APR, and cheaper alternatives.

Core Facts:

- Citi cash advances can be completed three ways: ATM withdrawal with a PIN, an in-person bank teller transaction, or a direct transfer to a linked bank account through the Citi Mobile App or website.

- A cash advance PIN must be requested separately from Citi and typically takes 7 to 10 business days to arrive by mail before it can be used at an ATM.

- Citi charges a cash advance fee of $10 or 5% of the amount, whichever is greater, and this fee posts to the account the same day as the withdrawal.

- The cash advance APR runs around 29.74% variable, and unlike purchases, interest starts accruing immediately with no grace period.

- ATM daily withdrawal caps usually range from $300 to $1,000 per machine per day, which is separate from the account’s overall cash advance limit set by Citi.

- A Citi Flex Loan offers a fixed APR typically between 8% and 18% with no transaction fee on most offers, making it a cheaper alternative to a standard cash advance for cardholders who qualify.

Best for:

- Citi cardholders who need emergency cash and want to understand the exact steps, PIN requirements, and fees before using an ATM or bank teller.

- Readers comparing the cost of a traditional cash advance against a Citi Flex Loan before borrowing against their credit line.

- Cardholders who received a Citi convenience check or balance transfer check and need to understand which one applies lower fees and interest.

Ways to Get a Cash Advance on Your Citi Credit Card

Citi gives cardholders more than one way to turn available credit into cash. The right method depends on how fast you need the money, whether you have a PIN, and how much cash you plan to take out. Below are the three main paths most Citi users choose.

Getting or Resetting Your Cash Advance PIN

Before you can use an ATM, your Citi card needs a cash advance PIN. Most new cards do not come with a PIN already set. You must ask for one, and it can take 7 to 10 business days to arrive by mail.

To set up or reset your PIN, you have three options:

- Log in to your account at citi.com and go to the “Services” tab. Look for the option to request or change your PIN.

- Open the Citi Mobile App (available on the Apple App Store and Google Play) and follow the same path under card services.

- Call the number on the back of your card, or dial 1-800-347-4934, and follow the automated prompts.

If you already had a PIN but forgot it, the reset process is the same. Citi does not display your existing PIN online for security reasons. You will get a new one by mail.

💡 Pro Tip: If you need cash today and you don’t have a PIN, skip the mail wait and head straight to a bank branch. A teller cash advance does not need a PIN, just a valid photo ID and your card.

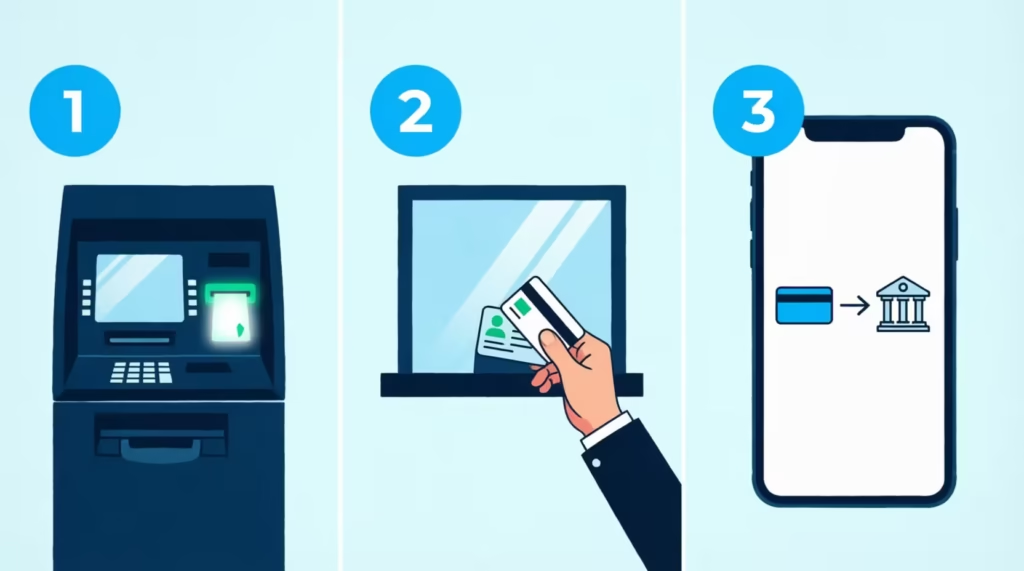

Bank Teller Cash Advance

A teller cash advance works when you can’t wait for a PIN. Walk into any Citibank branch or any bank that displays the Visa or Mastercard logo (matching your card’s network). Hand the teller your Citi credit card and a government-issued photo ID.

Tell the teller you’d like a cash advance for a specific amount. They will run the transaction and hand you cash on the spot. Fees still apply, and the amount comes off your cash advance limit, not your full credit line.

One benefit to note is that tellers often allow you to withdraw more cash than an ATM in one go. However, your account’s cash advance limit still applies.

Cash Advance via App or Online Transfer

Some Citi cards let you move cash straight from your credit line to a linked checking account. This is known as a direct deposit cash advance, and it works through the Citi Mobile App or your online account.

Log in, choose your card, then look for “Cash Advance” or “Direct Deposit” under card services. Pick the linked bank account, enter the amount, and confirm. Funds usually land within one to three business days.

This method still counts as a cash advance. Fees and the higher cash advance APR apply just like an ATM pull. If speed isn’t urgent, this route saves you a trip and any ATM surcharge.

Step-by-Step: Withdrawing Cash at an ATM

Once your PIN is active, an ATM withdrawal is quick. Follow these steps to avoid errors and extra fees:

- Find a fee-friendly ATM. Citibank ATMs and machines in the MoneyPass or Allpoint network usually skip surcharges. A non-network machine will add its own fee on top of Citi’s charge.

- Insert your Citi credit card, chip side up (or tap if the ATM supports it).

- Enter your 4-digit cash advance PIN when prompted.

- Select “Cash Advance” or “Credit” from the account menu. Do not pick “Checking” or “Savings,” since your credit card is not linked to a deposit account.

- Enter the amount you want in cash. If the ATM shows a daily cap that’s lower than your need, you may have to visit the next day again or use a teller instead.

- Review any on-screen fee disclosure. Federal rules require the ATM to show its own surcharge before you agree. If the fee feels high, cancel and find another machine.

- Take your cash, card, and receipt. Keep the receipt until the transaction posts to your account.

Once posted, the amount, plus the Citi cash advance fee, hits your card balance right away. Interest starts building from that same day.

How to Check and Understand Your Citi Cash Advance Limit

Your cash advance limit is not the same as your total credit limit. It’s a smaller slice of your credit line that Citi sets aside for cash transactions. On most cards, it runs somewhere between 20% and 40% of your overall limit, though the exact number varies by card and cardholder profile.

To find your current cash advance limit:

- Log in to your Citi online account and open your card details page. The limit shows under “Available Cash.”

- Open the Citi Mobile App, tap your card, and scroll to “Credit Available for Cash.”

- Check your latest paper or PDF statement, where cash advance details sit near your credit line summary.

- Call customer service and ask directly.

Knowing this number before you try to withdraw saves an embarrassing decline at the ATM.

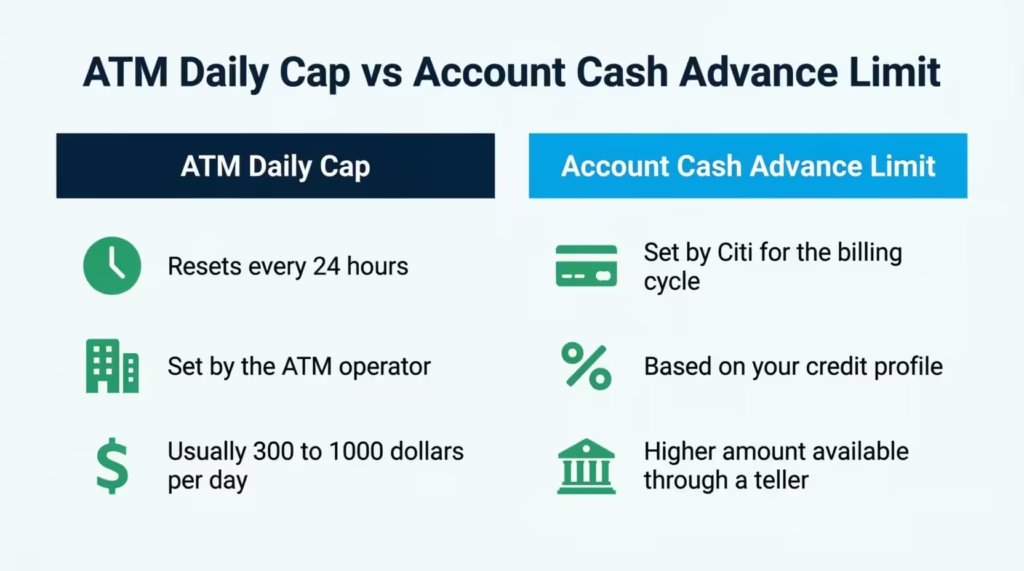

ATM Daily Cap vs. Account Cash Advance Limit

These two limits often get mixed up, but they work in very different ways.

The ATM daily cap is a limit the ATM or its network sets for a single day. It usually falls between $300 and $1,000 per machine, per 24 hours. This cap is not set by Citi. It’s a safety rule from the ATM operator.

The account cash advance limit is your total borrowing cap for cash across a billing cycle. It’s set by Citi based on your credit profile and card type. Even if you have $2,000 available for cash, an ATM might only give you $500 in one trip due to its own cap.

If you need more than the ATM allows, a teller inside a bank can usually process the full amount your card supports, up to your account cash advance limit.

Requesting a Cash Advance Limit Increase

If your cash advance limit is too low, you can ask Citi to raise it. Log in to your account, go to “Services,” and select “Request a Credit Line Increase.” You can also call the number on the back of your card.

Be ready to share your current income, monthly housing cost, and reason for the increase. Citi may run a soft credit check, which does not hurt your score, or a hard inquiry, which can lower it by a few points.

A higher cash advance limit does not mean lower fees or interest. It only means you can borrow more cash if needed. If your goal is a lower-cost option, a Citi Flex Loan (covered below) is often a smarter route.

Using Citi Convenience Checks

Citi sometimes mails paper checks tied to your credit card account. These are called convenience checks, and they let you pay someone (or yourself) using your credit line. Write the check like any personal check, and the amount posts to your card as a cash advance.

Convenience checks are useful when:

- A vendor accepts checks but not credit cards.

- You need to pay rent, taxes, or another bill that blocks card payments.

- You want to deposit funds into your own checking account without an ATM trip.

Once cashed or deposited, the check clears in one to three business days. The FDIC notes that these checks come with the same high fees and instant interest as any other cash advance, so treat them with care.

Convenience Check vs. Balance Transfer Check: Don’t Mix Them Up

Both come in the same envelope. They look almost the same. But they cost very different amounts.

A convenience check works like a cash advance. It comes with a cash advance fee (usually 5% or $10, whichever is greater) and the full cash advance APR, which starts building interest right away.

A balance transfer check is meant to move debt from another credit card. It often carries a lower balance transfer fee (around 3% to 5%) and, if you’re in a promo period, a much lower APR, sometimes 0% for a set number of months.

Before you write any check Citi sent you, read the letter that came with it. The fee, APR, and any promo terms will be listed on the top or bottom of the check itself. Cashing the wrong one could cost you hundreds in extra interest.

⚠️ Mistake to Avoid: Using a balance transfer check to pay a vendor or deposit into your own account. This is against the terms and can trigger the higher cash advance APR right away, wiping out the promo benefit.

Citi Cash Advance Fees Explained

Every Citi cash advance comes with a transaction fee on top of interest. According to Citi’s current pricing terms, the standard fee is either $10 or 5% of the amount, whichever is greater.

So if you take out $100, you pay $10 (the minimum). If you take out $500, you pay $25 (5% of the total). The fee posts to your account on the same day as the advance, and it counts toward your card balance right away.

On top of Citi’s fee, you may also pay:

- An ATM surcharge, typically $2 to $5, if the machine is out of Citi’s network.

- A foreign transaction fee, usually 3%, if you use the card overseas. This applies to most Citi cards, though a few premium cards waive it.

- A cash equivalent fee, which is the same 5% or $10 rule, on transactions like money orders, wire transfers, casino chips, cryptocurrency buys, and lottery tickets.

The Consumer Financial Protection Bureau reports that cash advance fees have risen sharply in recent years, especially around gambling-related transactions. Always check the ATM fee disclosure before you confirm the withdrawal.

Citi Cash Advance APR and Interest Accrual

Here is where cash advances get expensive. The cash advance APR on most Citi cards sits around 29.74% variable, based on the current Prime Rate. That’s several points higher than the purchase APR on the same card.

Worse, there is no grace period. On regular purchases, you get about 21 to 25 days to pay before interest kicks in. On a cash advance, interest starts the moment the transaction posts. Citi’s cardmember agreement confirms this rule clearly.

The interest also compounds daily. Each day’s unpaid balance earns its own tiny piece of interest, which then earns interest the next day. Over a few weeks, this stacks up faster than most people expect.

Real Cost Example: What a $300 Cash Advance Actually Costs

Let’s break down the true price of a $300 cash advance at a 29.74% APR. This assumes a 5% fee (rounded to $15) and daily compounding, using the daily rate of about 0.0815%.

| Time Held | Fee | Interest Charged | Total Cost |

|---|---|---|---|

| 7 days | $15.00 | $1.72 | $16.72 |

| 30 days | $15.00 | $7.42 | $22.42 |

| 60 days | $15.00 | $15.02 | $30.02 |

| 90 days | $15.00 | $22.79 | $37.79 |

Even after just one week, you’ve paid nearly $17 to borrow $300. Held for three months, the same advance costs almost 13% of the original amount. If you also paid a $3 out-of-network ATM fee, add that to every row.

The takeaway: pay the advance back as soon as you can. Every day matters.

Citi Flex Loan vs. Cash Advance: Which Costs Less?

A Citi Flex Loan is a cheaper way to borrow from your credit card if you qualify. It pulls from your existing credit line, but the interest rate is usually much lower than the cash advance APR. There’s no application, no credit check, and no origination fee for most offers.

Here’s how the two stack up:

| Feature | Citi Flex Loan | Citi Cash Advance |

|---|---|---|

| APR | Fixed, often 8% to 18% | Variable, around 29.74% |

| Transaction fee | None on most offers | 5% or $10 minimum |

| Grace period | Fixed monthly payments | None, interest starts day one |

| Speed | 1 to 3 business days | Instant at ATM |

| Where funds go | Bank account (direct deposit) | Cash, check, or transfer |

To check if you have a Flex Loan offer, log in to your Citi account and look under “Services” or “Offers.” Not every cardholder qualifies, and offer amounts vary based on your credit profile.

If you can wait a day or two and the offer is available, the Flex Loan almost always wins on cost. The NerdWallet analysis of card issuer credit line products confirms that structured loan offers like this are far cheaper than traditional cash advances.

📌 Did You Know: A Citi Flex Loan does not create a new account or a new hard inquiry, but the balance still counts toward your credit utilization. That matters if you’re trying to keep your utilization low for a mortgage or auto loan.

Does a Citi Cash Advance Hurt Your Credit Score?

A cash advance itself does not show up as a separate item on your credit report. Credit bureaus don’t get a note that says “this was a cash withdrawal.” But the balance you add can still hurt your score in an indirect way.

Here’s how the impact works:

- Credit utilization goes up. Your card’s balance grows by the advance plus fees. If your utilization ratio (balance divided by credit limit) climbs above 30%, your score can dip. Above 50%, the drop gets sharper.

- Statement closing date matters most. Citi reports your balance to the credit bureaus on the day your statement closes, not your due date. Even if you plan to pay it off in a few days, if the advance sits on your account when the statement closes, that higher balance is what gets reported.

- Missed payments cause the biggest damage. If the higher balance and fast-growing interest push you toward a late payment, that late mark can knock 60 to 100 points off your score.

The advance itself is invisible to lenders. The higher balance and any missed payment are what they see. To protect your score, try to pay the advance down before your statement closing date.

How to Minimize the Cost of a Citi Cash Advance

If a cash advance is your only option, a few smart moves can keep the damage small.

- Take out only what you truly need. Every dollar carries a 5% fee floor and near-30% interest. Don’t round up “just in case.”

- Pay it back within days, not weeks. Since interest builds daily, a fast payment saves real money. Use the Citi Mobile App to make a same-day payment from your bank account.

- Use a surcharge-free ATM. Stick to Citibank ATMs, MoneyPass, or Allpoint machines to skip the extra $2 to $5 charge. The Allpoint ATM locator makes it easy to find one nearby.

- Check for a Flex Loan offer first. Log in and look under “Offers” before you head to the ATM. A lower-rate loan can save you a lot if you qualify.

- Pay before the statement closes. This keeps your reported utilization lower and protects your credit score.

- Avoid stacking cash equivalents. Money orders, casino chips, and crypto buys all count as cash advances and rack up the same fees.

- Ask about hardship options. If the advance is for an emergency and you’re worried about repayment, call Citi and ask about hardship or Flex Plan options. Some cardholders qualify for reduced-rate repayment plans.

Small choices add up. Pulling $500 from a surcharge-free ATM and paying it back in 5 days costs about $26. The same $500 held for two months at an out-of-network ATM can cost close to $60. That’s more than double, for the exact same borrowed amount.

Frequently Asked Questions (FAQs)

How do I get a PIN for a Citi cash advance?

Request one through your Citi online account under “Services,” through the Citi Mobile App, or by calling 1-800-347-4934. It takes 7 to 10 business days to arrive by mail.

Do I need a PIN for a cash advance?

You need a PIN to use an ATM, but not for a bank teller cash advance. A teller only requires your Citi card and a government-issued photo ID.

Can I withdraw $2,000 from my credit card?

It depends on your account’s cash advance limit and the ATM’s daily cap, which usually runs $300 to $1,000 per machine per day. A bank teller can typically process a larger amount, up to your full cash advance limit.

Can I transfer money from my Citi credit card to a bank account?

Yes, through the Citi Mobile App or online account using the “Cash Advance” or “Direct Deposit” option. Funds usually arrive in your linked checking account within one to three business days.

What is a cash advance PIN on a credit card?

It’s a 4-digit code that lets you withdraw cash from your credit line at an ATM. It’s separate from any online account password and must be requested from Citi before first use.

What happens if I withdraw cash from my credit card?

Citi charges a fee of $10 or 5% of the amount, whichever is greater, and interest starts accruing the same day at around 29.74% APR. Unlike purchases, there’s no grace period before interest begins.

Does a Citi cash advance hurt your credit score?

The advance itself doesn’t appear as a separate item on your credit report. However, it raises your card balance and credit utilization, which can lower your score if it pushes utilization above 30%.

Is a Citi Flex Loan cheaper than a cash advance?

Yes, a Flex Loan typically carries a fixed rate of 8% to 18% with no transaction fee, compared to a cash advance’s roughly 29.74% variable APR and 5% fee. Check for a Flex Loan offer under “Services” or “Offers” before using an ATM.

Can I use my Citibank credit card to withdraw cash at any ATM?

Yes, but Citibank ATMs and machines in the MoneyPass or Allpoint network skip extra surcharges. A non-network ATM will add its own fee of $2 to $5 on top of Citi’s cash advance charge.

What’s the difference between a convenience check and a balance transfer check from Citi?

A convenience check works like a cash advance, with a 5% fee (or $10 minimum) and interest starting immediately. A balance transfer check carries a lower 3% to 5% fee and sometimes a 0% promotional APR for moving debt from another card.

Wrapping Up

Getting cash from a Citi credit card is quick, but it’s rarely cheap. Between the 5% fee, an APR near 29.74%, and no grace period, even a small withdrawal can grow fast. The methods ATM, bank teller, direct deposit, or convenience check all lead to the same cost structure, so the smartest move is knowing your limit, your PIN status, and your cheaper options before you act.

For most readers, checking for a Citi Flex Loan first will deliver the best results because it cuts both the fee and the interest rate in half or better.

If this guide helped, share it with a friend who’s ever stared at an ATM screen wishing they’d read the fine print first.