If you’ve ever paid your credit card on time and still seen interest charges on your next statement, you’re not alone. It feels unfair, and it’s confusing. Most people think paying something each month is enough to keep purchases free of interest, but the grace period credit card rule is stricter than that. One small slip can quietly switch off the interest-free window without any warning.

The fix is simple once you understand it: pay the full statement balance by the due date, every cycle, on every card.

In this guide, we’ll walk through how the grace period works, what kills it, how to bring it back, and how to keep it locked in for good.

Key Takeaways

This guide covers what a grace period on a credit card is. It explains how the interest-free window works, what makes it end, how to get it back, and the payment habits that help avoid interest charges.

Core Facts:

- A credit card grace period is the time between the statement closing date and payment due date, typically lasting 21 to 25 days.

- Keeping a grace period active requires paying the full statement balance by the due date every billing cycle.

- Making just the minimum payment or carrying even $1 into the next cycle can end the grace period and start interest charges right away.

- Cash advances, most balance transfers, cryptocurrency purchases, money orders, casino chips, and some peer-to-peer payments do not qualify for a credit card grace period.

- Most issuers require two consecutive billing cycles of full on-time payments, including any trailing interest, to restore a lost grace period.

- Interest charges are calculated using the daily periodic rate, which equals the card’s APR divided by 365 and applies daily when the grace period is inactive.

Best for:

- People who want to understand what a grace period on a credit card is and how to avoid paying purchase interest.

- Cardholders who paid on time but still received interest charges need to identify what caused the grace period to disappear.

- Anyone comparing statement balances, current balances, cash advances, balance transfers, and other transactions that affect interest-free borrowing.

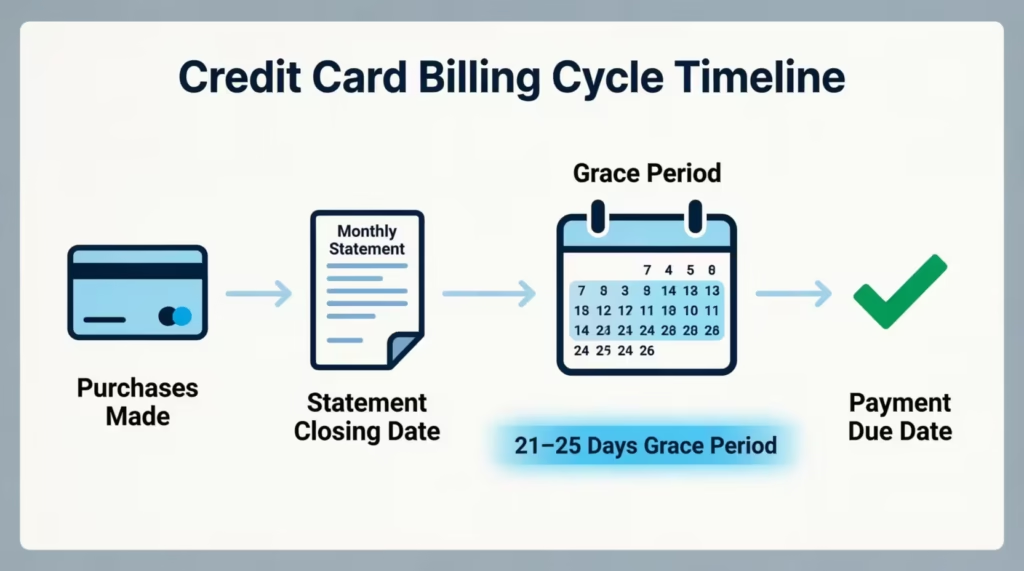

How a Credit Card Grace Period Works

A grace period is the gap between your statement closing date and your payment due date. During this stretch of days, the card issuer doesn’t charge interest on new purchases, as long as you pay your full statement balance by the due date. Think of it as a short, interest-free loan the bank gives you on every purchase you make during the billing cycle.

Here’s how the timeline plays out in real life. Say your billing cycle ends on the 5th of each month. That date is your statement closing date. The bank then prints your statement and gives you at least 21 days to pay. So your due date might be around the 30th.

Any purchase you made between the 6th of the previous month and the 5th of this month is covered by the credit card’s interest-free period, as long as you pay the full statement amount by the 30th.

If you do that, the bank charges zero interest on those purchases. If you don’t, interest starts piling up using a method called the daily periodic rate, which we’ll cover in a later section.

How Long Is a Credit Card Grace Period

Most credit cards offer a grace period that runs between 21 and 25 days. The federal law sets the floor, so banks can’t give you less than 21 days. Some premium cards stretch it to 25 days or a bit more, but going below 21 is not allowed for cards that offer a grace period at all.

To find your exact length, look at your monthly statement. It shows both the closing date and the due date. The days between those two dates equal your grace period. You can also check the cardholder agreement, often inside a section titled “How to Avoid Paying Interest on Purchases.”

The Law Behind the Grace Period (Credit CARD Act of 2009)

The Credit CARD Act of 2009 changed how grace periods work in the United States. Before this law, banks could shorten the window or change due dates without much notice.

Now, federal rules force issuers to mail or deliver your statement at least 21 days before the payment is due. This protects you from getting a statement on Monday and being told it’s due Wednesday.

The law also blocks banks from picking random new due dates each month. Your due date must stay roughly the same from one cycle to the next. According to the Consumer Financial Protection Bureau, payments must be considered on time as long as they arrive by 5 p.m. on the due date.

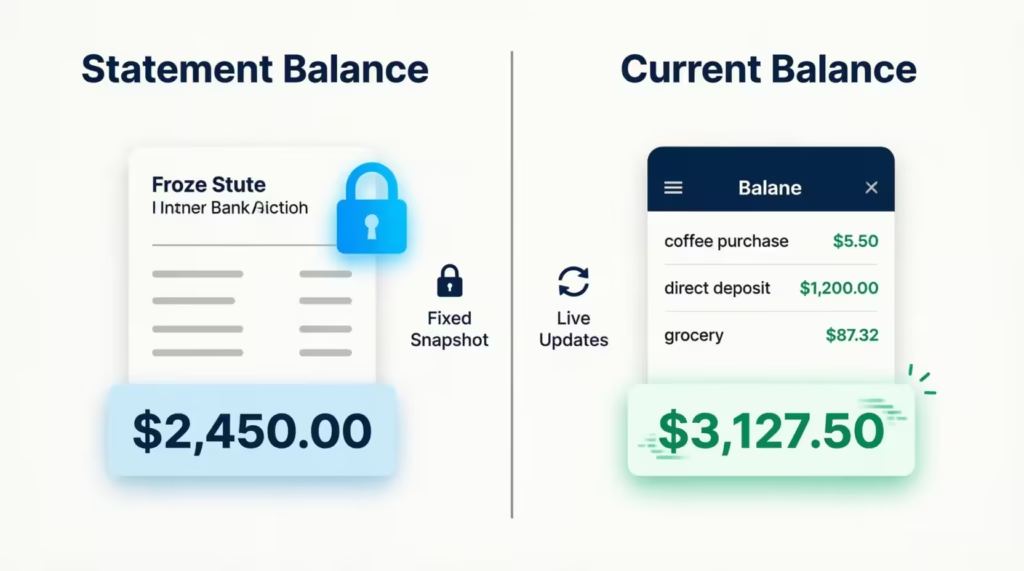

What “Paying in Full” Actually Means: Statement Balance vs. Current Balance

This is where most people slip up. Your card shows two numbers, and they’re not the same thing. The statement balance is the amount you owed at the moment the bank closed your last billing cycle. It’s frozen. It doesn’t move, no matter how much you spend after that date.

The current balance is the live, running total. It changes every time you swipe your card or get a refund. So if your statement closed at $800 and you spent another $200 the next day, your current balance now shows $1,000, but your statement balance is still $800.

To keep your grace period, you must pay in full the statement balance, not the current balance. Paying the statement amount is what tells the bank you cleared the prior cycle. Paying the current balance is fine too (it just means you pay more now), but paying less than the statement balance breaks the rule.

Here’s a concrete example. Sarah, a 29-year-old marketing coordinator, sees a current balance of $1,400 on her app. Her statement balance is $900. She pays $900 by the due date. The bank counts this as paid in full. Her grace period stays active, and the new $500 in purchases will appear on next month’s statement, still interest-free, as long as she repeats the pattern.

If Sarah had paid only the minimum payment of $35, the bank would consider her grace period broken, even though her payment was on time.

💡 Pro Tip: Always set up your bank app to display the statement balance on the home screen. Looking at the current balance trains your brain to pay the wrong number.

How Interest Accrues When the Grace Period Is Active and When It Isn’t

When the grace period is active, the math is easy. Purchase interest is zero. The bank treats every new swipe as an interest-free short-term loan.

When the grace period is inactive, the math flips. The bank charges interest starting on the transaction date, not the statement date. So a coffee you bought on the 2nd of the month starts collecting interest that same day. This is called a finance charge, and it builds up using the daily periodic rate.

The daily periodic rate is your APR divided by 365. If your card has a 22% APR, your daily rate is about 0.0603%. The bank applies this rate to your average daily balance every day until you fully clear the account.

Here’s a side-by-side cost comparison. Say you spend $2,000 on a card with a 22% APR.

| Situation | Interest Charged for 30 Days |

|---|---|

| Grace period active, paid in full | $0 |

| Grace period lost, balance carried | About $36.20 |

| Grace period lost, balance held 90 days | About $108.60 |

That gap shows why protecting the interest-free window matters so much. A single missed full payment can cost more than the rewards you earn for an entire year.

Which Transactions Are Excluded From the Grace Period

Not every transaction gets the same treatment. Some types of charges skip the interest-free window completely.

Cash advances are the biggest ones. The moment you pull cash from an ATM using your credit card, interest starts adding up. There is no cash advance grace period. On top of that, the cash advance APR is almost always higher than the purchase APR, often by 5 to 10 percentage points. Most cards also tack on a fee of 3% to 5% of the amount you withdraw.

Balance transfers work the same way. Unless you took the card up on a promotional offer, transferred balances start charging interest from the day they post. Promotional balance transfer offers usually waive interest for 6 to 21 months, but standard transfers do not.

Other excluded transactions include:

- Wire transfers funded by your credit card

- Buying cryptocurrency, money orders, or casino chips

- Some peer-to-peer payments (depending on how the bank codes them)

Fees tied to these transactions also start accruing interest right away. If you pay a $30 cash advance fee, that $30 begins building interest the same day.

⚠️ Mistake to Avoid: Many people use credit cards in the ATM thinking it’s the same as a debit withdrawal. It’s not. A $300 cash advance can easily cost an extra $25 to $40 over a few weeks, even if you pay it back fast.

What Causes a Credit Card Grace Period to Disappear

The grace period is fragile. It vanishes for a few clear reasons, and once it’s gone, every new purchase starts collecting interest the same day you make it.

The most common cause is carrying a balance from one cycle to the next. Even one dollar left unpaid breaks the rule. The bank doesn’t care if it was $1 or $1,000. The result is the same: you lose the interest-free window on next month’s purchases too.

Other triggers include:

- A late payment, even by a single day

- Paying less than the full statement balance (a partial payment)

- An unpaid cash advance balance is dragging on into the next cycle

- An outstanding balance transfer from a previous month

People often think the grace period stays active as long as they make some payment on time. That’s a myth. The rule is binary. You either paid the full statement amount or you didn’t.

What Happens to New Purchases the Moment the Grace Period Is Lost

Once you lose the grace period, every new purchase starts collecting interest from the day it posts. This is called immediate accrual.

Here’s how it plays out. Michael, a 33-year-old IT support specialist, paid $400 of his $500 statement balance last month. He left $100 unpaid, thinking it was no big deal. The grace period switched off. The next day, he bought a $300 pair of running shoes.

That $300 started collecting interest right away, using the daily periodic rate. If his APR is 24%, the shoes alone added about $5.92 in interest before his next statement even closed.

This is the part that surprises most people. They expect the next statement to be clean since they paid on time. Instead, it shows interest charges on purchases they thought were covered. The interest follows every purchase made while the grace period is off, including ones made the same day the statement closes.

How to Get Your Grace Period Back After Losing It

The good news is that you can bring the grace period back. The bad news is that it takes more than one good month.

The rule most banks follow is the two-consecutive-payments rule. You must pay the full statement balance on time, two billing cycles in a row, before the grace period turns back on for new purchases.

Why two cycles instead of one? Because of trailing interest, sometimes called residual interest. Even after you pay off the statement balance in cycle one, the bank still charges interest for the days between the statement closing date and the day your payment is posted.

That small amount shows up on cycle two. You then have to pay that off as well. Once cycle two closes at zero, the restore grace period clock kicks in, and cycle three is once again interest-free.

While you’re waiting, try to avoid using the card at all. Every swipe during the recovery window adds more interest. If you must use it, keep purchases small and pay them down right away.

| Cycle | What to Do | Grace Period Status |

|---|---|---|

| Cycle 1 | Pay full statement balance | Still off |

| Cycle 2 | Pay full statement balance, including trailing interest | Resets at end |

| Cycle 3 | New purchases | Back on |

How to Find Out If Your Credit Card Has a Grace Period

Not every card offers one. Before you assume yours does, you’ll want to verify grace period rules in writing.

Start with the Schumer box. This is the federally required summary table found in your credit card agreement, named after Senator Chuck Schumer, who pushed for plain disclosures. It lists your APR, fees, and grace period terms in a clean grid. Look for a row labeled “Grace Period” or “How to Avoid Paying Interest on Purchases.”

That sentence will say something like: “Your due date is at least 25 days after the close of each billing cycle. We will not charge you interest on purchases if you pay your entire balance by the due date each month.”

If that wording is missing, the card may not offer a grace period at all. This is more common with:

- Some store credit cards

- Subprime or credit-builder cards

- Certain secured cards

- A few small-bank or fintech cards

You can find the Schumer box in the welcome packet that came with your card, inside your online account under “Disclosures” or “Terms,” or by calling the number on the back of the card and asking the rep to confirm.

📌 Did You Know: Federal law does not require credit cards to offer a grace period. It only regulates how grace periods must work if a card chooses to offer one. That’s why checking the Schumer box matters before you commit to a card.

Does Every Credit Card Have a Grace Period?

No. There’s a key difference between something being regulated and something being required. The Credit CARD Act of 2009 sets the rules for grace periods, but it doesn’t force banks to offer them.

Cards most likely to skip the grace period include certain store-only cards, deep subprime cards aimed at people rebuilding credit, and a handful of niche fintech products.

If your card uses average daily balance billing with no interest-free window mentioned in the Schumer box, you’re probably paying interest on purchases from day one. That’s a strong reason to either pay off purchases instantly or switch to a card that includes the feature.

Grace Period vs. 0% Intro APR vs. Deferred Interest: What’s the Difference

These three terms get mixed up all the time, but they work in very different ways. Getting them confused can cost you hundreds of dollars.

| Feature | Grace Period | 0% Intro APR | Deferred Interest |

|---|---|---|---|

| Permanent? | Yes, ongoing | No, 6 to 21 months | No, set promo window |

| Interest if balance carried? | Charged on new purchases | Charged only after promo ends | Backdated to day one |

| Where you’ll see it | Standard credit cards | New card offers | Store financing deals |

Grace Period vs. 0% Intro APR

A grace period is a standard, ongoing feature. It resets every month as long as you pay in full. A 0% intro APR is a temporary offer, usually for new cardholders, that waives interest on purchases or balance transfers for a set number of months.

The big difference shows up when you carry a balance. With a grace period, carrying any balance shuts the window off. With a promotional APR, you can carry a balance during the promo months and pay zero interest. But the moment the promo ends, any unpaid amount starts collecting interest at the regular APR going forward.

Grace Period vs. Deferred Interest

This is the most dangerous one. Deferred interest is common in store financing, like “No interest if paid in full within 12 months.” It sounds like a 0% APR offer, but it isn’t.

With deferred interest, the bank tracks interest the whole time at the regular APR. If you pay off the full balance before the promo ends, the bank waives that tracked interest. But if you have even one dollar left when the promo ends, the bank charges you every penny of the tracked interest, going all the way back to the original purchase date. This is called the backdating trap.

Here’s how it plays out. Jennifer, a 38-year-old dental hygienist, financed a $2,400 sofa with 12-month deferred interest at 28.99% APR. She paid it down to $50 by month 11, missed the final payoff by two weeks, and got hit with $360 in retroactive interest on her next statement. A real 0% intro APR would have charged her interest only on that $50 going forward.

How to Protect Your Grace Period Going Forward

Once you understand the rules, keeping the interest-free window open is mostly about good habits and a few smart settings.

Set autopay to the statement balance, not the minimum, and not a fixed dollar amount. This single change wipes out the most common cause of lost grace periods. Autopay set to the statement balance pays exactly what’s needed, on time, every cycle, with no work from you.

Make large purchases right after your statement closes. That way, you get the longest possible interest-free window before the next due date. A $1,500 laptop bought the day after the statement closes can ride free for over 50 days.

Use a separate card for balance transfers and cash advances. These transactions don’t share the same grace-period rules as regular purchases, and keeping them on your main card keeps them from polluting your interest-free window.

Track your restoration timeline if you ever lose the grace period. Mark the next two statement closing dates on your calendar so you know exactly when the window comes back. Cards don’t usually send a notification when this happens.

A few extra credit card grace period tips worth following:

- Check your statement balance the day after each cycle closes

- Keep your due date the same every month if your bank lets you set it

- Pay a few days before the actual due date to avoid posting delays

- Watch out for foreign holidays or weekends that can delay processing

According to the Federal Reserve, the average credit card APR sits well above 20% in 2026, which means losing a grace period now costs more than ever. Protecting the grace period is one of the highest-value financial habits available, and it costs nothing.

Frequently Asked Questions (FAQs)

Is there a 3-day grace period for a credit card?

No. The minimum grace period allowed by federal law is 21 days, not 3. Most credit cards offer between 21 and 25 days from your statement closing date to your payment due date.

Do all credit cards have a 30-day grace period?

No, and 30 days is not the standard. Federal law sets the minimum at 21 days, most cards offer 21 to 25 days, and some cards, including certain store and secured cards, offer no grace period at all.

What happens if I’m 1 day late on my credit card?

One day late breaks your grace period entirely. Your next statement will include interest charges on new purchases starting from the day each transaction is posted, even purchases you made before the late payment.

What happens if I pay my credit card 2 days late?

Paying 2 days late has the same result as paying 1 day late: your grace period is gone. Every new purchase from that point forward starts collecting interest immediately using your card’s daily periodic rate, which is your APR divided by 365.

What happens if you pay during the grace period?

If you pay the full statement balance by the due date, the bank charges zero interest on all purchases from that billing cycle. Paying only the minimum or a partial amount breaks the grace period even if the payment arrives on time.

Can I get my grace period back on my credit card?

Yes, but it takes two billing cycles. You must pay the full statement balance on time two months in a row, including any trailing interest that appears on the second statement, before new purchases become interest-free again.

What are the downsides of a grace period?

The grace period is simple: miss one full payment, and it ends. Then, any new purchase starts collecting interest right away. Rebuilding it requires two consecutive full payments, so even a single partial payment can cost you weeks of interest-free purchasing.

What is the difference between a grace period and deferred interest?

A grace period is an ongoing monthly feature that keeps purchases interest-free as long as you pay your full balance each cycle. Deferred interest, common in store financing deals, silently tracks interest the entire time and charges all of it retroactively if any balance remains when the promotional period ends.

Does a grace period apply to cash advances?

No. Cash advances start collecting interest the day they post, with no grace period at all. The cash advance APR is also typically 5 to 10 percentage points higher than your regular purchase APR, and most cards add a fee of 3% to 5% on top.

What is the difference between my statement balance and current balance?

Your statement balance is the frozen total from when your last billing cycle closed, and paying that amount in full is what preserves your grace period. Your current balance is a live running total that includes new charges added after the cycle closed, which are not yet due.

Bottom Line

We’ve walked through the full life of a grace period, from how it works to what kills it, to how to bring it back, and how to lock it in for good. The key point is that paying your statement balance in full and on time each cycle keeps your cards interest-free.

Based on the math shown earlier, setting autopay to the statement balance is the most effective approach. It removes human error from the equation and protects the value.

If you know someone who pays their card monthly but still sees interest charges, share this guide with them. It could save them hundreds of dollars a year and clear up the confusion their bank never bothered to explain.