I’ve spent years helping friends and family make sense of their credit card statements, and one question keeps coming up: why does paying feel so confusing when the rules sound simple? If you’ve ever paid your bill “on time” and still seen interest, or watched your score drop after paying in full, you’re not alone. Learning how a credit card billing cycle works is the missing piece most people skip.

Your billing cycle has three dates that control interest charges and your credit score, and timing your payment around them changes everything.

In this guide, I’ll walk you through each date, the math behind interest, and the smartest day to pay your bill.

Key Takeaways

This guide explains how a credit card billing cycle works, covering the three key dates that control interest charges and credit scores, how interest is calculated using the average daily balance method, and the two-payment strategy that eliminates interest while keeping reported utilization low.

Core Facts:

- A billing cycle runs 28 to 31 days and contains three critical dates: the cycle start date, the statement closing date, and the payment due date, which by law must fall at least 21 days after closing.

- The statement closing date, not the payment due date, is when issuers report your balance to Equifax, Experian, and TransUnion, making it the date that directly affects your credit utilization ratio.

- Credit card interest is calculated using the average daily balance method: multiply the average daily balance by the daily periodic rate (APR divided by 365), then multiply by the number of days in the cycle.

- Paying only the minimum payment ends the grace period immediately, causing new purchases to accrue interest from day one of the next cycle.

- To avoid interest entirely, pay the full statement balance by the due date; to protect your credit score, pay down the balance 3 to 5 days before the statement closing date.

- Most major issuers allow cardholders to change their payment due date through the app or by phone, with changes taking 1 to 2 billing cycles to take effect.

Best for:

- Cardholders who have paid on time but still seen interest charges or unexpected credit score drops.

- People looking to lower their credit utilization ratio without reducing their actual spending.

- Anyone who wants to understand the exact timing strategy for when to pay their credit card bill each month.

What a Credit Card Billing Cycle Actually Is

A credit card billing cycle is the recurring period your card issuer uses to track your spending, fees, and payments. It usually lasts between 28 and 31 days. At the end of each cycle, the issuer takes a snapshot of the account and creates a statement.

Think of it like a monthly report card. Every purchase, refund, fee, and payment in this window lands on one statement. The next cycle then starts fresh the very next day.

A common mistake is to assume the cycle matches the calendar month. It often does not. A cycle might run from the 6th of one month to the 5th of the next. The dates depend on when the account was opened, not on the first or last day of the month.

Under federal rules summarized by the Consumer Financial Protection Bureau, issuers must keep billing periods roughly equal in length so cardholders can plan around them.

How Long a Billing Cycle Lasts and Why It Varies

Most statement cycles run for about 30 days, but the exact length can shift. Some cycles are 28 days. Others stretch to 31. The reason is simple. Months have different lengths, weekends fall in different spots, and holidays can push dates by a day or two.

Card issuers set the cycle length when the account opens. From there, the pattern stays steady. The exact dates appear at the top of each statement and inside the card’s app.

Here’s a quick example. Say the cycle runs from April 6 to May 5. Every purchase made in that window shows up on the May statement. A purchase on May 6 belongs to the next cycle, not this one. Knowing these start and end dates makes it easier to plan big buys.

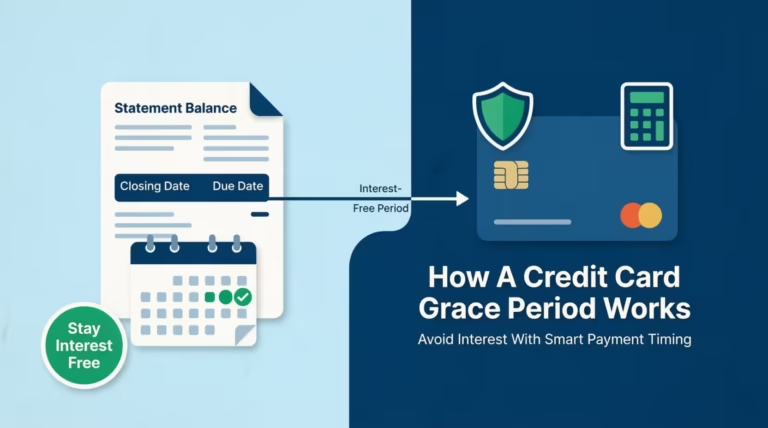

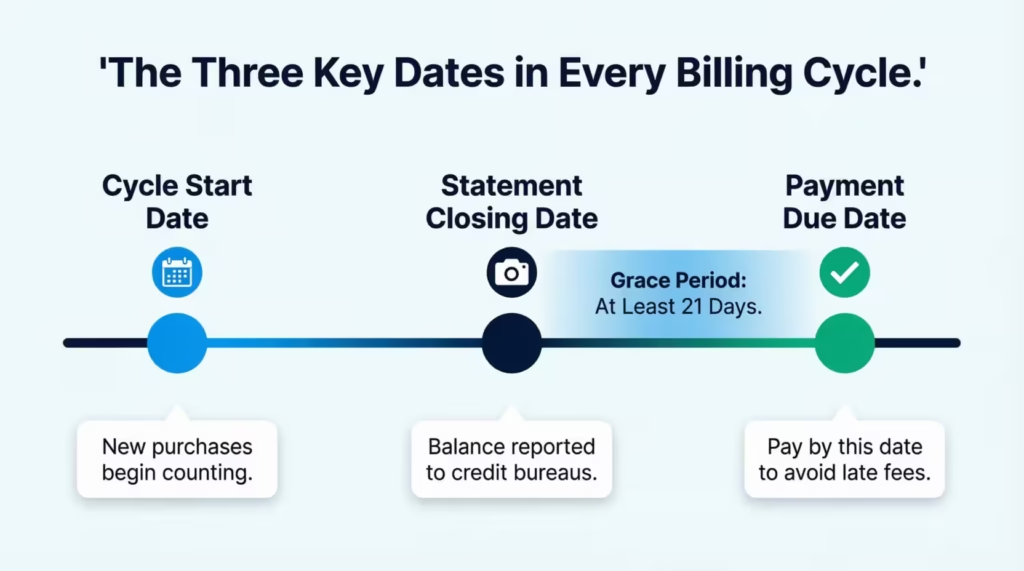

The Three Key Dates Inside Every Billing Cycle

Every billing period has three dates that matter most. Mixing them up is the top reason people get charged interest or hurt their credit score.

The cycle start date is the day the period begins. The statement closing date is the day it ends. The payment due date is when at least the minimum must be paid to stay current. By law, the due date must fall at least 21 days after the closing date, a rule set by the CARD Act of 2009 as detailed by the Federal Reserve.

Here’s how they line up in real life:

| Date | What It Means | Why It Matters |

|---|---|---|

| Cycle Start | First day of the period | New purchases start counting toward this cycle |

| Statement Closing | Last day of the period | The issuer snaps a photo of the balance |

| Payment Due | At least 21 days after closing | Pay by this day to avoid late fees |

Once all three dates are clear, the rest of the system gets much easier to follow.

What Happens on the Statement Closing Date

The statement closing date is the most powerful day in the cycle. The issuer freezes the balance, totals up purchases, fees, and payments, then creates the official bill. This number is called the statement balance.

This same day usually triggers something else. The issuer sends the balance to the credit bureaus. So whatever is owed at closing is what shows up on the credit report for the next month.

📌 Did You Know: The statement closing date, not the due date, is what gets reported to Equifax, Experian, and TransUnion. That’s why two people with the same habits can have very different scores.

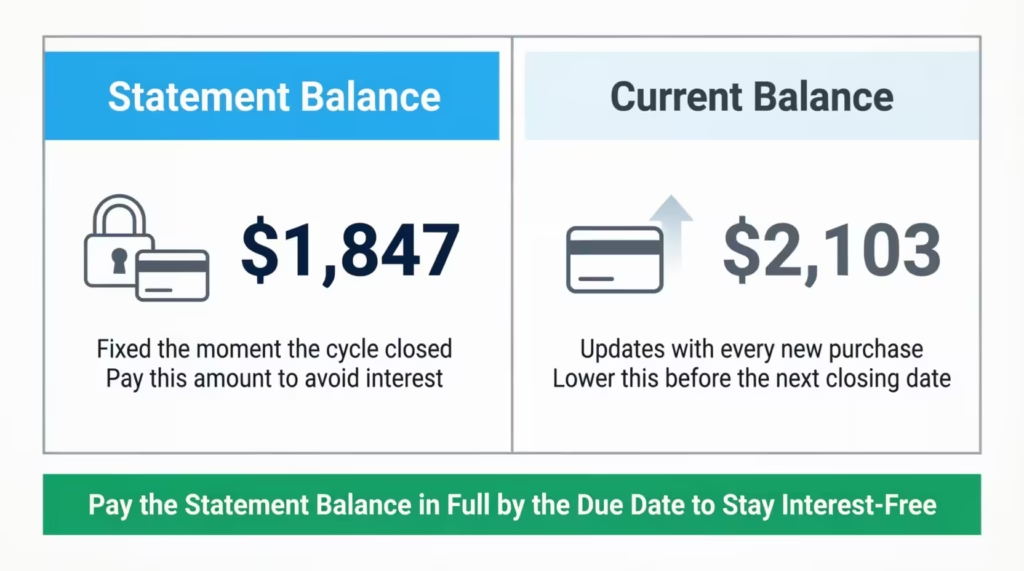

Statement Balance vs. Current Balance

These two balances trip up almost every new cardholder. The statement balance is locked. It is the amount owed at the second the cycle closed. Paying this full amount by the due date avoids interest.

The current balance is live. It updates every time a purchase, refund, or payment posts. So if groceries were bought this morning, the current balance went up, but the statement balance did not change.

A simple rule helps. To dodge interest, pay the statement balance by the due date. To lower reported utilization, pay down the current balance before the next closing date.

How the Grace Period Works

The grace period is the stretch of time between the statement closing date and the payment due date. During this window, no interest builds on new purchases, but only under one condition. The previous statement balance must be paid in full.

Most cards offer a grace period of at least 21 days. Some give 25 or more. Paying in full each month keeps this benefit going. It works like a short, interest-free loan from the issuer.

Lose the grace period, and the rules change fast. Carrying a balance from one month to the next means new purchases can start earning interest right away. Paying the balance back to zero, then paying the next full statement on time, resets the grace period.

When Interest Starts Accruing

Interest does not start the moment a card is swiped. It usually starts after the grace period ends, but only when the balance is not paid in full.

Cash advances are the big exception. Taking cash out at an ATM starts accruing interest the same day. There is no grace period on cash advances, ever. The same rule often applies to balance transfers, depending on the offer.

⚠️ Mistake to Avoid: Paying only the minimum keeps the account in good standing but ends the grace period. The next month, even brand new purchases start earning interest from day one.

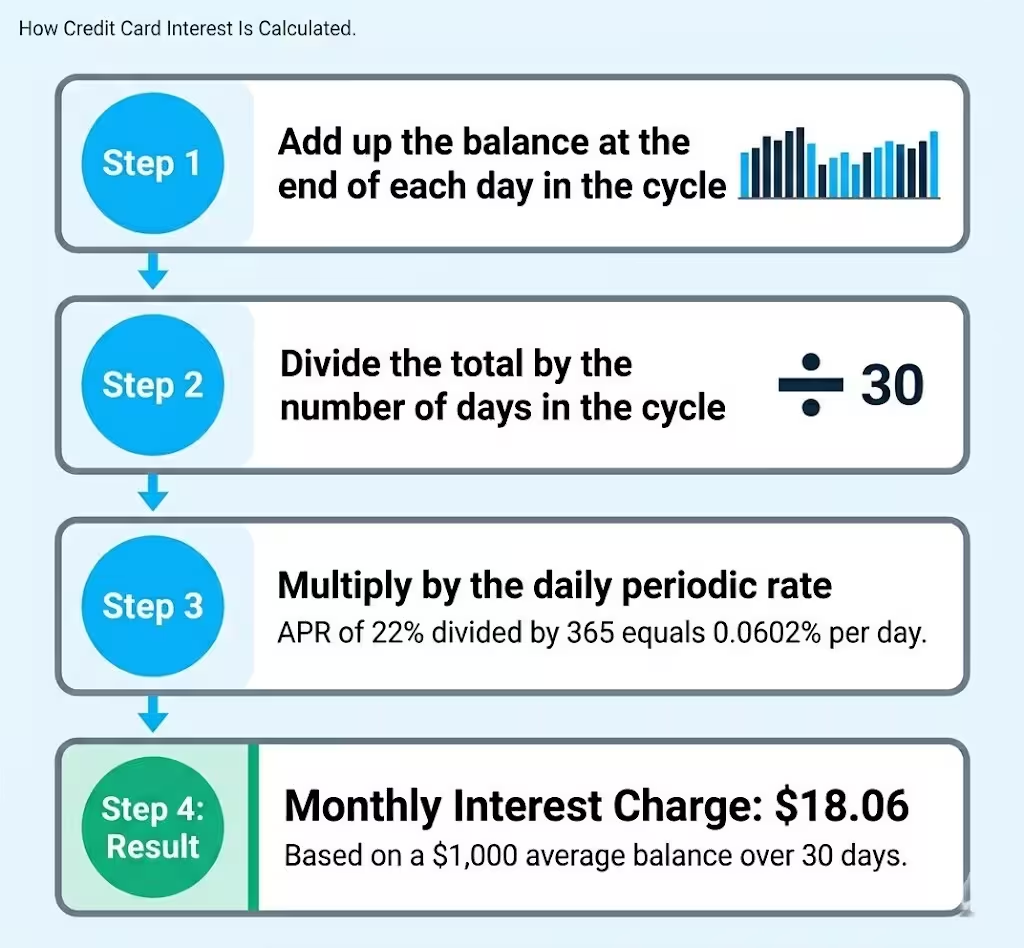

How Credit Card Interest Is Calculated Across the Billing Cycle

Most issuers use the average daily balance method. It sounds complex, but the steps are clear once you see them.

First, the issuer adds up the balance at the end of each day in the cycle. Next, it divides that total by the number of days in the cycle. That gives the average daily balance. Then it multiplies by the daily periodic rate, which is the APR divided by 365.

Here’s a worked example. Say the APR is 22%. The daily rate is 0.0602% (22% divided by 365). If the average daily balance is $1,000 over a 30-day cycle, the interest for that month is:

$1,000 x 0.000602 x 30 = $18.06

That $18.06 lands on the next statement as a finance charge. The higher the daily balance, the bigger the charge. This is why paying down a balance mid-cycle, not just on the due date, lowers what you owe. As research from the Federal Reserve shows, the average APR on credit card accounts assessed interest now sits well above 20%, which makes small daily balance reductions matter even more.

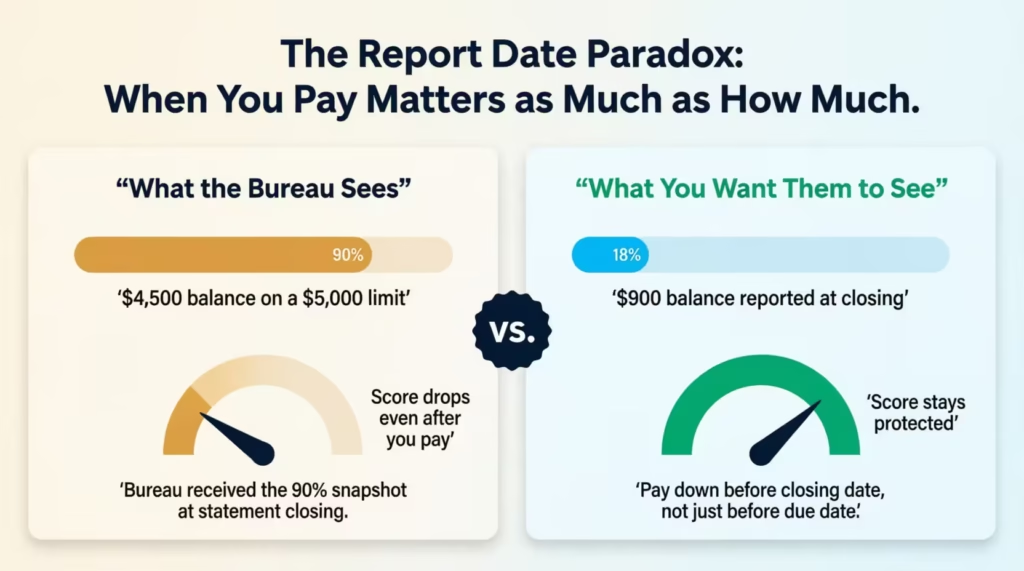

When Credit Card Issuers Report Your Balance to the Credit Bureaus

Card issuers report to the credit bureaus once per month. The most common reporting day is the statement closing date, give or take a day or two. They send the statement balance, the credit limit, and the payment status to Equifax, Experian, and TransUnion.

This snapshot is what lenders see. A $4,000 balance on a card with a $5,000 limit will show 80% utilization on the report, even if the bill was paid in full a week later.

This is the report date paradox. Every penny can be paid on time, and the borrower can still look heavy on paper. The fix is to pay down the card before the closing date, not just before the due date.

How Your Billing Cycle Affects Credit Utilization and Your Score

Credit utilization is the share of the credit limit being used. It is one of the biggest factors in the FICO score, second only to payment history.

Here’s the trap. The utilization ratio is based on the balance reported at statement closing. So even if the bill is paid in full a few days later, the bureaus already saw the high number. The score reacts to that number.

Take Sarah, a marketing coordinator at a small tech startup. She charged $4,500 on her $5,000 limit card to book a work trip, then paid it off two weeks later. Her score still dropped 40 points that month because her statement closed before her payment was posted. She fixed it the next cycle by paying $3,500 a few days before closing, which kept reported utilization under 20%.

💡 Pro Tip: Try to keep less than 30% of the limit reported each month. Under 10% is even better for top-tier scores. A small payment 3 to 5 days before the closing date helps control the number that gets reported.

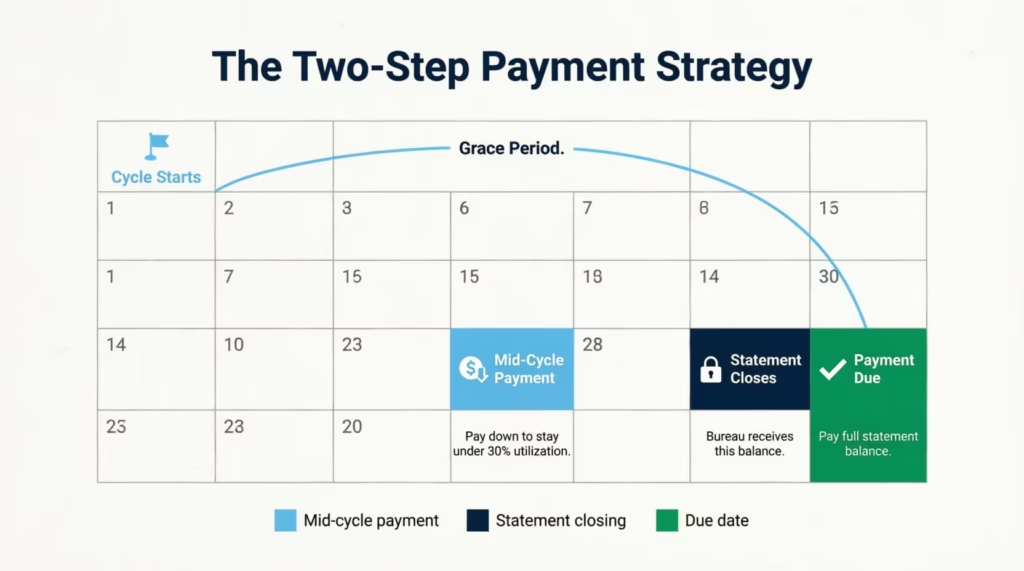

The Best Day to Pay Your Credit Card Bill

There is no single best day for everyone. The right day depends on the goal.

To avoid interest, pay the full statement balance by the due date. That is the bare minimum to keep the grace period and dodge finance charges. Paying a few days early adds a buffer in case of bank delays.

To boost the credit score, pay down most of the balance before the statement closing date. This lowers the number the bureaus see and shrinks reported utilization.

The smartest move is to do both. Make a mid-cycle payment to keep the reported balance low, then pay any remaining statement balance by the due date. This two-step habit protects the score and the wallet at the same time.

Pending vs. Posted Transactions — Which Cycle Do They Count In?

A pending transaction is one that the merchant has authorized, but the bank has not finished settling. A posted transaction is final. The money has moved, and the charge is locked into the account.

Most purchases post within 1 to 3 business days. Weekends and holidays can stretch this. A charge made on Friday night might not post until Tuesday.

Which cycle a charge belongs to depends on the post date, not the swipe date. A purchase made on the last day of a cycle but posted two days later lands on the next statement. This matters most near the closing date. A big pending charge on closing day may or may not show up on the bill, depending on when it posts.

When timing is tight, check the app’s pending list. Most major banks show pending and posted charges separately, so it is easy to see what is still in motion.

How to Change Your Credit Card Due Date

Most major issuers let cardholders change their due date. It is a small change that can fix big cash flow problems, especially when a bill lands a few days before payday.

There are usually three ways to ask. Log in to the issuer’s app and look under account settings. Call the number on the back of the card. Or send a secure message through the online account. The agent or the app will offer a list of possible new dates, often within a 10 to 14-day window.

The change usually takes 1 to 2 billing cycles to kick in. Until then, keep paying on the old schedule.

A good rule of thumb is to set the due date for 5 to 7 days after payday. This gives the deposit time to clear and leaves room for bills that hit first. David, an operations manager paid on the 15th of each month, moved his card due date from the 12th to the 22nd. He stopped missing payments and saved $35 in late fees in his first month.

Common Billing Cycle Mistakes and How to Avoid Them

A few simple errors cause most billing cycle problems. Watching for them saves money and protects credit scores.

Mixing up the closing date and the due date.

They are not the same. The closing date snaps the balance for the report. The due date is the payment deadline. Mark both on a calendar.

Paying only the minimum.

This keeps the account current, but the grace period ends. New purchases start earning interest from day one of the next cycle.

Making big purchases right before the closing date.

A large charge just before closing inflates reported utilization. Waiting one or two days until the new cycle starts often protects the score.

Trusting autopay alone.

Autopay is helpful, but it usually pulls the minimum or the statement balance on the due date. It does nothing for the utilization ratio. Pair autopay with a mid-cycle manual payment for the best results.

Ignoring pending charges near the cycle end.

A pending purchase can post into either cycle. Check the app before closing day if a charge is close to the line.

Frequently Asked Questions (FAQs)

What is the biggest killer of credit scores?

Payment history is the single largest factor in a FICO score, so missed payments cause the most damage. High credit utilization at statement closing is the second biggest drag and can drop a score even when every payment is made on time.

What happens if you miss a billing cycle?

Missing a payment triggers a late fee and ends the grace period, so new purchases begin accruing interest from the very first day of the next cycle. To restore normal interest-free status, pay the full balance back to zero, and then pay the next full statement on time.

Is it better to pay off a credit card immediately or wait for a statement?

Paying most of the balance before the statement closing date lowers the number reported to the credit bureaus and protects the credit score. Paying any remaining statement balance by the due date then keeps the grace period active and prevents interest charges entirely.

How do I know the billing cycle of my credit card?

The start and end dates of the billing cycle appear at the top of every monthly statement and inside the card issuer’s app or online account. Both the closing date and payment due date are listed there.

Is a billing cycle always 30 days?

Most billing cycles run close to 30 days, but the exact length can range from 28 to 31 days depending on the month and the issuer. The cycle dates are set when the account opens and stay consistent from there.

What happens if I pay after the billing cycle?

Paying after the statement closing date but before the payment due date is still on time and avoids any late fees. Paying after the due date triggers a late fee and can end the grace period, causing new purchases to accrue interest immediately in the next cycle.

What is the grace period for a billing cycle?

The grace period is the time between your statement closing date and payment due date, typically 21 to 25 days. If you pay your full statement balance during this period, you can usually avoid interest charges on new purchases.

What happens to the grace period if I only make the minimum payment?

Paying only the minimum keeps the account in good standing but ends the grace period immediately. Starting the next billing cycle, new purchases begin accruing interest from day one instead of getting the usual 21 or more days of interest-free.

How do pending transactions affect which billing cycle a purchase lands in?

Which billing cycle a charge belongs to depends on the posted date, not the date the card was swiped. A purchase made on the last day of a cycle that takes two days to post will land on the next statement, not the current one.

What is the grace period on a credit card billing cycle?

The grace period is the window between the statement closing date and the payment due date, which by law must be at least 21 days. During this stretch, no interest builds on purchases, but only if the previous statement balance was paid in full.

Bottom Line

A credit card billing cycle is built around three dates: the cycle start, the statement closing date, and the payment due date. Each one shapes a different part of financial life, from interest charges to credit scores.

Based on the math above, the most effective approach is to pay the statement balance in full by the due date to stay interest-free, and to make a smaller payment before the closing date to keep reported utilization low. That two-step habit turns the billing cycle from a source of stress into a tool you control.

If a friend just got their first credit card, share this guide. It could save them hundreds in interest and protect their score for years.