You just spotted the letters “(V)” or the words “variable APR” on your credit card statement. Maybe your rate went up last month, and you’re not sure why. It feels like the bank can raise your interest whenever it wants, and that’s a scary thought when you’re carrying a balance. The good news is that a variable APR on a credit card follows clear rules, not random moves by the bank.

A variable APR is a credit card interest rate that goes up or down over time because it’s tied to a public index, mainly the U.S. prime rate.

Below, you’ll find clear answers, a real dollar example, the exact rules banks must follow, and easy steps you can take today to lower your costs.

Key Takeaways

This guide explains how a variable APR on a credit card is calculated from the prime rate plus a personal margin, how often it changes, and specific ways to lower your rate.

Core Facts:

- A variable APR equals the prime rate (currently 6.75% as of December 11, 2025) plus a margin set by the bank based on credit risk at account opening.

- Your APR only changes when the Federal Reserve moves the federal funds rate, which pushes the prime rate up or down by the same amount within a day or two.

- Index-driven rate changes require no 45-day advance notice, while other rate increases like credit re-evaluation require 45 days’ written notice under Regulation Z.

- A penalty APR, often 29.99% or higher, is triggered by a payment 60 days past due and is not tied to the prime rate at all.

- On a $5,000 balance, a 0.50% APR increase costs about $2.10 more per month, or roughly $25 more per year.

- Paying your full statement balance each month eliminates interest charges entirely inside the grace period, regardless of whether the rate is variable or fixed.

Best for:

- Cardholders who noticed a “(V)” symbol or the word “Variable” on their statement and want to understand what it means.

- People carrying a credit card balance who want to calculate the real dollar cost of a rate change.

- Anyone deciding whether to call for a rate reduction, do a balance transfer, or focus on building credit to lower their margin.

What “Variable APR” Means on a Credit Card

A variable APR is the yearly interest rate on your credit card that can move up or down as time passes. It isn’t locked in. The word “variable” just means “it can change.”

Almost every major credit card in the U.S. today uses a variable rate. Not just some cards. Nearly all of them. So if you have a credit card in your wallet right now, there’s a very high chance it carries a variable rate.

You can spot it in two easy places on your own card:

On your monthly statement, look at the interest rate box. If you see a small “(V)” or the word “Variable” next to the APR number, that’s it. For example, “19.99% (V)” means your rate is 19.99%, and it can change.

In your cardholder agreement (the small booklet or PDF you got when you opened the account), look for a section called “Interest Rates and Interest Charges.” It will spell out the rate and note that it’s variable. It will also tell you what index the rate is tied to.

If your card shows a rate without the “(V)” mark or without the word “variable,” it might be a fixed-rate card. But those are rare now, and we’ll cover them later.

What a Variable APR Is Tied To

Your rate doesn’t just float on its own. It’s tied to a public number called an index rate. For credit cards, that index is almost always the U.S. prime rate.

The prime rate is a short-term rate that big banks use as a base rate for many loans. It’s published every day and easy to look up. The current U.S. prime rate is 6.75%, effective December 11, 2025, per the Federal Reserve’s H.15 release.

But the prime rate itself isn’t set out of thin air. It follows the federal funds rate, which is the rate the Federal Reserve controls. The Fed’s rate-setting group, called the FOMC (Federal Open Market Committee), meets about eight times a year. When the FOMC raises or lowers the federal funds rate, banks almost always move the prime rate by the same amount within a day or two.

The math is simple and steady. In the U.S., the prime rate has been set at the federal funds rate plus 3 percentage points for many years. So if the Fed raises rates by 0.25%, the prime rate goes up by 0.25% too. And soon after, your card’s variable APR moves up by the same 0.25%.

The numbers above are current as of this writing. Rates change often, so treat any single figure as a snapshot. To see today’s number, just check the Federal Reserve’s H.15 page or search on Google “current prime rate.”

How the Margin Is Set

Your card’s APR isn’t just the prime rate. There’s a second piece added on top called the margin. Think of it this way:

Your APR = Prime rate + Margin

The margin is the part your bank sets. It’s based on how the bank sees your credit risk when you open the account. A person with a high credit score might get a margin of 8%. Someone with a lower score might get a margin of 18% or more.

Here’s the key point: Once your margin is set at account opening, it usually stays the same, even when the prime rate moves. So if prime goes from 6.75% to 7.00%, your APR goes up by that same 0.25%. Your margin didn’t change. Only the index did.

That’s why two people can have the same card with very different APRs. They pay the same index, but they were given different margins based on their credit at the time.

How Often and How Fast a Variable APR Can Change

Your rate doesn’t change on a set schedule like “the first day of every month.” It only changes when the index changes. And the index only changes when the Fed moves the federal funds rate, which then pushes the prime rate up or down.

So in a year when the Fed doesn’t move rates at all, your APR stays flat. In a year when the Fed changes rates four times, your APR could move four times too.

There’s a short delay between a Fed move and your bill. Most card agreements say the new rate takes effect on the first day of the billing cycle that starts after the index change. So if the prime rate goes up on March 15, your new APR might not kick in until your April billing cycle begins.

The law does not cap how often a card’s variable rate can go up in a year. But that also doesn’t mean the bank can raise it whenever it wants. It can only move with the index. If the prime rate is flat, your rate is flat.

📌 Did You Know: The prime rate has moved as few as zero times in some calendar years and as many as seven times in others. Your APR follows the same pattern as the prime rate, so a quiet year at the Fed means a quiet year for your card rate.

Where to Find Rate-Change Information for Your Card

You don’t have to guess. Two places on paper (or on screen) will tell you the truth about your rate.

The first is your monthly statement. Every statement has an “Interest Charge Calculation” box near the bottom. It lists your current APR, whether it’s variable, and the daily rate used to charge interest. If your rate changed since last month, you’ll see it there.

The second is your cardholder agreement. This is the full contract. It will tell you:

- The exact index used (almost always “the U.S. Prime Rate as published in the Wall Street Journal”)

- Your margin

- When rate changes take effect (usually the first day of a billing cycle)

- What triggers a rate change

You can find your latest agreement inside your card’s online account or app, usually under “Documents” or “Statements & Documents.” If you can’t find it, call the number on the back of your card and ask them to email it to you.

When the Bank Must Notify You

This part causes a lot of confusion. The rules are clear, but they vary for different types of rate changes.

For a rate change that comes from an index move (like the prime rate going up), your bank does not have to send you 45 days of advance notice. The reasoning is simple: the index is public, and you agreed to a variable rate when you opened the card. The change will just show up on your next statement.

For other kinds of rate changes, the rules are much tougher. Under the CARD Act and Regulation Z, the Consumer Financial Protection Bureau requires 45 days of written advance notice before a bank can raise your rate for reasons like a new pricing tier or a re-evaluation of your credit. You also get the right to opt out and close the account in most of these cases.

You can read the exact rule at 12 CFR § 1026.9(c) if you want the legal wording. But the plain version is this: index-driven moves show up without a warning letter. Everything else requires 45 days’ notice.

How a Rate Change Actually Affects Your Bill

This is the part most people care about. A rate change on paper feels abstract. In dollars, it’s clearer.

Let’s walk through a real example.

Say you have a balance of $5,000 on your credit card. Your APR is 22.99%. You only pay the minimum each month, so the full balance rolls over.

To find your monthly interest, credit cards use a daily periodic rate. That’s your APR divided by 365. So:

- Daily rate = 22.99% ÷ 365 = 0.063%

- Daily interest on $5,000 = $5,000 × 0.00063 = about $3.15

- Monthly interest (30 days) = about $94.50

Now the Fed raises rates by 0.50%. Your APR goes from 22.99% to 23.49%. Same $5,000 balance. Let’s redo the math:

- New daily rate = 23.49% ÷ 365 = 0.0644%

- New daily interest = $5,000 × 0.000644 = about $3.22

- New monthly interest (30 days) = about $96.60

So the change costs you about $2.10 more per month, or about $25 more per year on that $5,000 balance. Not huge, but real. And if you carry the balance for years, that adds up with compound interest.

Now flip the numbers. If your balance is $500 instead of $5,000, the same 0.50% rate hike costs you about $0.21 more per month. Almost nothing.

Two lessons from the math:

The size of your balance is the real driver. A high rate on $500 is little money. A low rate on $10,000 is still big money.

How long you carry the balance also matters a lot. Paying it off in three months costs much less than dragging it out for three years, because interest keeps building each day the balance sits there.

💡 Pro Tip: The dollar cost of a rate change on your card is roughly your balance × the rate change ÷ 12. So a 0.25% rate hike on a $3,000 balance costs about $0.63 more per month ($3,000 × 0.0025 ÷ 12). Use this quick math to check if a rate move is worth worrying about.

Variable APR vs. Fixed APR on a Credit Card

A fixed APR is a rate that stays the same over time. It doesn’t move with the prime rate or any other index. If your card has a fixed APR of 17.99%, it stays at 17.99% until the bank sends you a written notice to change it.

That sounds nicer than a variable rate. But there’s a catch: fixed-rate credit cards are very rare now. Most big banks and card issuers moved to variable rates years ago. You’ll mostly find fixed rates on some credit union cards or on a few niche cards.

Even a “fixed” APR isn’t fully locked forever. The bank can still change it, but only after giving you 45 days of advance notice. With a variable rate, the change happens with the index, and no letter is sent.

In day-to-day life, the difference for most people is small. Both types charge interest the same way. Both use a daily periodic rate. The only real gap is who controls the change:

- Fixed APR: The bank chooses when to change it, and must warn you.

- Variable APR: The market (through the prime rate) drives the change, and no warning is required.

If you always pay your balance in full each month, this comparison barely matters. You’ll never pay interest anyway. If you carry a balance often, a lower rate is what matters most, not whether it’s fixed or variable.

Why Your APR Might Have Changed for a Different Reason

Not every rate jump is a variable-rate move. If your APR shot up by a big amount, like from 21% to 29%, that’s almost certainly not the prime rate moving. It’s something else.

Here’s how to tell the difference:

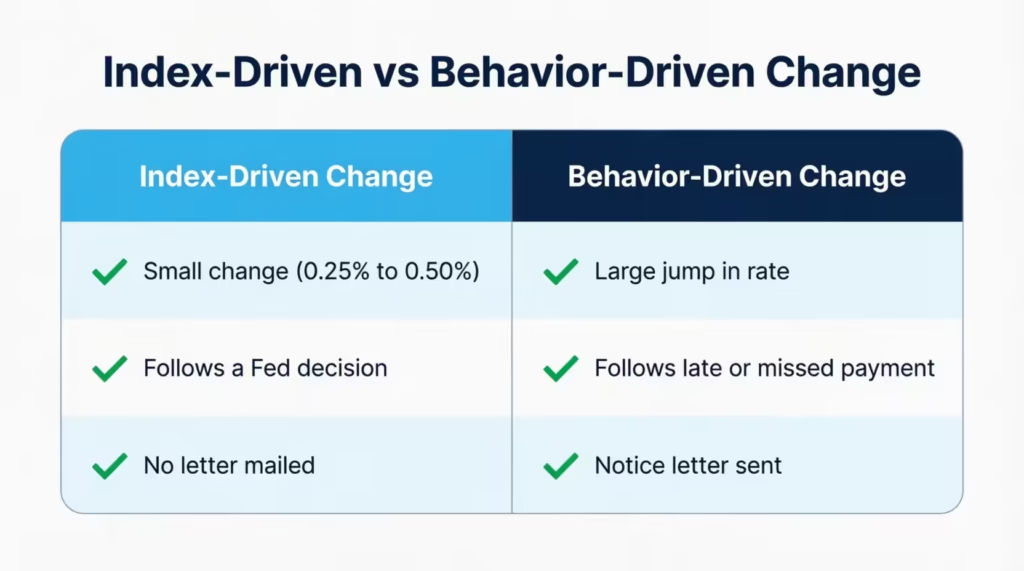

An index-driven move is small (usually 0.25% or 0.50%), lines up with a recent Fed decision, and shows up quietly on your statement with no letter mailed to you.

A behavior-driven change is much bigger, comes with a letter or email, and often follows a late payment, a missed payment, or a big drop in your credit score.

Look at the size of the jump. Look at whether you got a notice. Look at the timing. Those three clues tell you which kind of change hit your card.

Penalty APR

A penalty APR is a high rate your bank can charge if you break the rules of your card. The main trigger is a late or missed payment, usually 60 days past due.

A penalty APR is much higher than a normal rate. It often sits around 29.99% or higher, well above the current average credit card APR of 21.16% reported in the Federal Reserve’s Consumer Credit G.19 release for Q1 2026. That’s why a penalty APR can be double what you were paying before.

The important thing to know: a penalty APR is not tied to the prime rate at all. It’s a punishment rate set by the bank. It stays until you catch up on payments and, in most cases, make on-time payments for six months in a row.

To avoid it, pay on time every month. Even one very late payment can trigger it. Setting up autopay for at least the minimum payment is the easiest way to protect yourself.

Promotional or Introductory APR Ending

Some cards offer a low or 0% APR when you first open them. This is called a promotional APR or introductory APR. It might last 12, 15, 18, or even 21 months.

When that period ends, the rate jumps back to the card’s normal rate, which is usually the variable purchase APR shown in your cardholder agreement. This jump can look scary if you forgot about the end date. But it isn’t a “variable APR going crazy.” It’s a planned event, and the end date was set when you signed up.

You can find the exact end date in two places. The offer letter or email you got when you opened the card lists it. Your monthly statement also shows it, often in the interest charge box or in a “Promotional Rate” note.

⚠️ Mistake to Avoid: Many people carry a balance right up to the last day of a 0% intro APR, then get shocked when the next month’s bill has a big interest charge. Mark the end date on your calendar. If you can, pay off the balance before that date.

Is a Variable APR Bad?

Short answer: no, not by itself. Almost all cards have variable rates now, so “variable” isn’t the real story. The real story is two things:

The margin your bank added on top of the prime rate. This is the number you can shop for.

Your own balance-carrying habit. This is the number you can control.

If you pay your full balance every month before the due date, you fall inside the card’s grace period. That means you pay zero interest. Zero. It doesn’t matter if your APR is 15% variable or 25% variable. If you never carry a balance, the APR is just a number on paper. It never touches your money.

If you do carry a balance from month to month, then your APR matters a lot. And a lower margin will help you more than worrying about whether the rate is “variable” or “fixed.”

So the honest answer looks like this:

- Pay in full each month? A variable APR doesn’t hurt you at all.

- Carry a balance sometimes? A variable APR will cost you a bit more when rates rise, but not by huge amounts.

- Carry a large balance long-term? Focus on lowering the rate itself. That matters far more than the type of rate.

In other words, most people worry too much about the word “variable” and not enough about the size of their balance and margin.

What You Can Do About Your Variable APR

You’re not stuck. Even though you can’t control the prime rate, you can control several things that shape what you actually pay.

Pay the balance in full each month.

This is the strongest lever, and it’s free. Inside your grace period, you pay no interest at all. The APR could double tomorrow, and it still wouldn’t touch you. If you can shift to paying in full every month, do it. Nothing else beats it.

Ask the bank for a lower rate.

Call the number on the back of your card and ask for a rate reduction. This works better than most people think. If you’ve paid on time for a year or more and your credit score has improved, many issuers will lower your margin, often by 2 to 5 percentage points. The call takes 10 minutes. There’s no downside to asking.

Do a balance transfer to a lower-rate card.

If your current margin is high and you’re carrying a balance, look for a card offering 0% APR on balance transfers for 12 to 21 months. You’ll usually pay a transfer fee of 3% to 5% of the amount moved. But the interest you save often more than covers the fee, especially if you can pay off the balance during the promo window. Just don’t add new purchases to the new card while you’re paying off the transferred balance.

Focus on the balance, not the rate.

Every extra dollar of principal you pay saves you interest for as long as the balance would have sat there. If the APR is 22.99%, paying an extra $100 today saves you about $22.99 over the next 12 months. That’s a better return than most savings accounts.

How Your Credit Score Affects Your Margin

Your credit score doesn’t move the prime rate. But it does move your margin, which is the part of your APR the bank controls.

A higher score tells the bank you’re a lower risk. Lower risk means a smaller margin. On new cards, borrowers with scores above 750 often get margins that are 5 to 10 percentage points lower than borrowers with scores below 650. Same prime rate, very different APR.

Some issuers also review your account from time to time. If your score has gone up since you opened the card, they may offer you a lower margin without you asking, or approve a lower rate if you call in.

Keep in mind this is a slow-moving lever. Your credit score doesn’t jump overnight. But the basic steps are simple and steady: pay every bill on time, keep your credit card balances well below your limits (below 30% is a good target, below 10% is even better), and don’t open many new accounts at once. Over 6 to 12 months, small changes add up.

For a lower rate today, ask for a reduction or do a balance transfer. For a lower rate over the next year or two, build the score. Use both levers together, not just one.

Frequently Asked Questions (FAQs)

What is a good variable APR for a credit card?

A margin 5 to 10 points lower than average is good, which typically means scores above 750 land well under the current average APR of 21.16%. Anything close to or below that average counts as competitive.

Why is my variable APR so high?

Your APR equals the prime rate plus your margin, and the margin is set by your credit risk at account opening. A high margin, often 18% or more, usually points to a lower credit score when you applied.

Can I negotiate a lower APR on my card?

Yes, call the number on the back of your card and ask for a rate reduction. Issuers often lower your margin by 2 to 5 percentage points if you’ve paid on time for a year or more and your score has improved.

How can I lower my credit card APR?

Ask your issuer for a rate reduction, transfer your balance to a 0% APR card for 12 to 21 months, or build your credit score over 6 to 12 months. Paying on time and keeping balances under 30% of your limit both help lower your margin.

What does 24.99% variable APR mean on a credit card?

It means your yearly interest rate is currently 24.99%, made up of the prime rate plus your personal margin, and it can rise or fall as the prime rate changes. The rate only moves when the Federal Reserve changes the federal funds rate.

Do you pay APR if you pay on time?

Paying on time avoids a penalty APR, but you only avoid regular interest entirely by paying your full statement balance each month. Paying just the minimum on time still means the remaining balance accrues interest daily.

Is it better to have a fixed or variable APR?

For most people, the difference is small, since both charge interest the same way using a daily periodic rate. If you always pay in full each month, neither type matters because you pay zero interest either way.

Does variable APR go down?

Yes, a variable APR falls when the Federal Reserve lowers the federal funds rate, which pushes the prime rate down by the same amount. Your margin stays fixed, so only the index portion of your rate moves.

How much is 26.99 APR on $3000?

Using the quick formula of balance times rate divided by 12, a 26.99% APR on a $3,000 balance costs roughly $67 per month in interest if the full balance is carried. That adds up to over $800 a year if the balance isn’t paid down.

Can you switch from variable to fixed?

Contact your card issuer directly to find out if that option is available on your account.

Wrapping Up

Understanding how a variable rate works turns a scary term into a simple one. Your APR moves with the prime rate, your margin stays mostly the same, and only your balance and habits decide how much any of it actually costs you.

Paying the balance in full each month is the best step for most cardholders. The grace period eliminates interest, regardless of the rate. If you carry a balance, lowering your margin (by asking, transferring, or building your score) will save you far more than tracking every Fed meeting.

If you know someone confused by “(V)” on their statement or worried about their next bill, share this guide. It could save them real money and a lot of stress.