You checked your Credit Karma app before heading to the dealer. It showed a solid number. Then you sat in the finance office, and the manager quoted you a score that felt way lower. That gap is stressful, and it’s the main reason many buyers feel blindsided at signing. The truth is, the dealer credit score you see rarely matches your free app.

Dealers pull an industry-specific FICO Auto Score, not the general VantageScore on most free apps.

Here’s what you’ll find below: the exact scoring models, which bureau is pulled, the 2026 rate tiers, and a complete pre-visit checklist. This way, you’ll know what to expect when you arrive.

Key Takeaways

This guide explains what credit score dealerships use, covering FICO Auto Scores, the 250-900 scoring scale, bureau variation, 2026 APR rate tiers, and how to prepare before financing a car.

Core Facts:

- Dealerships primarily use FICO Auto Score 8 or Auto Score 9, which run on a 250 to 900 scale, not the 300 to 850 VantageScore shown on free apps like Credit Karma.

- Auto lenders pull credit data from Equifax, Experian, or TransUnion depending on the lender’s own contract, and some lenders pull two or all three bureaus.

- FICO’s rate shopping window treats multiple auto loan inquiries as one inquiry if submitted within 14 days on older models or 45 days on newer models.

- Experian’s Q1 2025 data shows average new car APR ranges from 5.18% for super prime (781+) buyers to 15.81% for deep subprime (300-500) buyers.

- On a $35,000 new car loan over 60 months, the interest difference between super prime and subprime tiers is nearly $8,000.

- A single late auto payment or past repossession carries more weight in a FICO Auto Score than in a general-purpose FICO or VantageScore.

Best for:

- Car buyers preparing to apply for financing who want to understand why their dealer-quoted score differs from their free app score.

- Buyers wanting to check their real auto score and pre-qualify with outside lenders before visiting a dealership.

- Shoppers comparing multiple loan offers who want to understand why lenders quote different scores for the same application.

Which Credit Score Dealerships Actually Use

The short answer: dealers and their lending partners mainly use a FICO Auto Score, not the general-purpose score you check on free apps. This is the same core FICO data reworked to predict one thing: whether you’ll pay back a car loan on time.

The most common versions in the finance office today are FICO Auto Score 8 and FICO Auto Score 9. Auto Score 8 remains the go-to tool for many banks and captive lenders, like Ford Credit and Toyota Financial Services.

Auto Score 9 is newer and reads certain data, like paid collections, more forgivingly. Which version shows up depends on the lender’s contract with the bureau, so two lenders can legitimately quote you different numbers on the same day. myFICO explains that industry-specific FICO Scores run on a 250 to 900 range for exactly this reason.

Some smaller lenders and credit unions still run on earlier auto versions, such as FICO Auto Score 2, 4, or 5, because their systems haven’t been updated. This is normal in auto lending and it explains why you sometimes see wildly different scores across offers.

VantageScore does show up too, but usually as a supplemental data point, not the number the lender actually approves you on. So when your Credit Karma VantageScore says 720 and the finance manager says 682, both can be right at the same time.

Why the Score at the Dealership Looks Different From Your Free App

The gap between your Credit Karma number and the dealer’s number isn’t a mistake, and it isn’t a sales trick. It’s two different scoring models reading the same credit file and asking two different questions.

Free consumer apps like Credit Karma, NerdWallet, and most bank dashboards show a VantageScore, usually VantageScore 3.0 or 4.0. VantageScore was built by the three bureaus as a general-purpose model. It tries to predict whether you’ll default on any type of debt, from a credit card to a personal loan to a mortgage.

Auto lenders use an industry-specific model built for one job: predicting whether you’ll repay a car loan specifically. This model looks at the same credit file, but it puts extra weight on things like past auto loans, missed car payments, and repossessions. Recent on-time car payments help you more here than they would on a VantageScore.

Because the two models weigh the same data differently, they naturally produce different numbers. Same person, same day, same credit file, two very different scores. This is not an error, and no one is running a bait-and-switch on you.

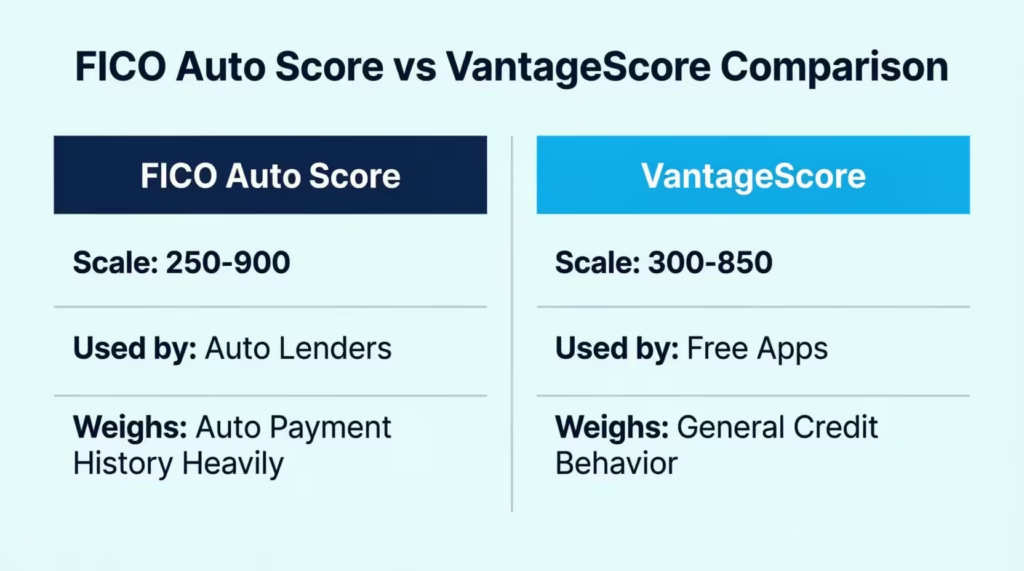

FICO Auto Score’s Different Number Scale (250–900)

Here’s the piece that catches most people off guard: FICO Auto Scores run on a 250 to 900 scale, not the 300 to 850 you’re used to seeing on free apps. That extra range at both ends is why the numbers can feel unfamiliar.

Higher is still better, and lower is still riskier. But because the top ceiling is 900 instead of 850, direct one-to-one comparisons with your Credit Karma score don’t work. A 780 on VantageScore is not the same as a 780 on FICO Auto Score 8, and neither of them slots neatly into the same tier.

The practical takeaway: don’t panic if your dealer number lands 20 to 50 points off your app score in either direction. Different scale, different model, different math.

Which Credit Bureau Dealerships Pull

There isn’t one universal bureau every dealer uses. Auto lenders pull from Equifax, Experian, or TransUnion, and which one shows up depends on the lender’s own preferences, not the dealer’s.

Some lenders pull only one bureau to save on cost. Others pull two, and a few pull all three, then use the middle score or the lowest score for underwriting. Captive lenders (like Honda Financial Services or GM Financial) often have long-standing contracts with one specific bureau. Big banks and national credit unions are more likely to pull multiple bureaus.

Data can also differ slightly from bureau to bureau. Not every creditor reports to all three, and update timing varies. So your Equifax file might show a paid-off card that your TransUnion file still shows as open. This can move your score five to fifteen points either way, depending on the account.

VantageScore vs. FICO in Auto Lending

In auto lending, FICO is the primary decision-maker. VantageScore may appear on the printout, but the approval, the rate, and the loan structure are almost always driven by a FICO Auto Score.

The reason is regulatory and historical. FICO has been the standard in the industry for decades. Lenders base their underwriting policies, risk models, and pricing sheets on FICO scores. VantageScore is gaining ground in credit cards and personal loans, but auto lending has moved more slowly.

If the finance manager quotes you a “credit score,” it’s almost certainly a FICO Auto Score, not a VantageScore.

TransUnion CreditVision and Equifax Beacon 9.0 as Alternatives

A few lenders use bureau-branded scores instead of, or alongside, FICO Auto Scores. TransUnion CreditVision and Equifax Beacon 9.0 are the two you’ll see mentioned in loan disclosures.

CreditVision analyzes trended data. It looks at how your balances and payments have changed over the past 24 to 30 months, not just one moment in time. If you’ve been steadily paying down balances, CreditVision can score you higher than a static model would.

Beacon 9.0 is Equifax’s proprietary score, built to be more predictive for lenders who prefer Equifax’s data. It runs on the same 300 to 850 scale as a base FICO but uses different weightings.

These options are not as common as a FICO Auto Score. Still, it’s good to know them if your loan paperwork includes a score you don’t recognize.

Why Multiple Lenders Can Give You Different Scores for the Same Application

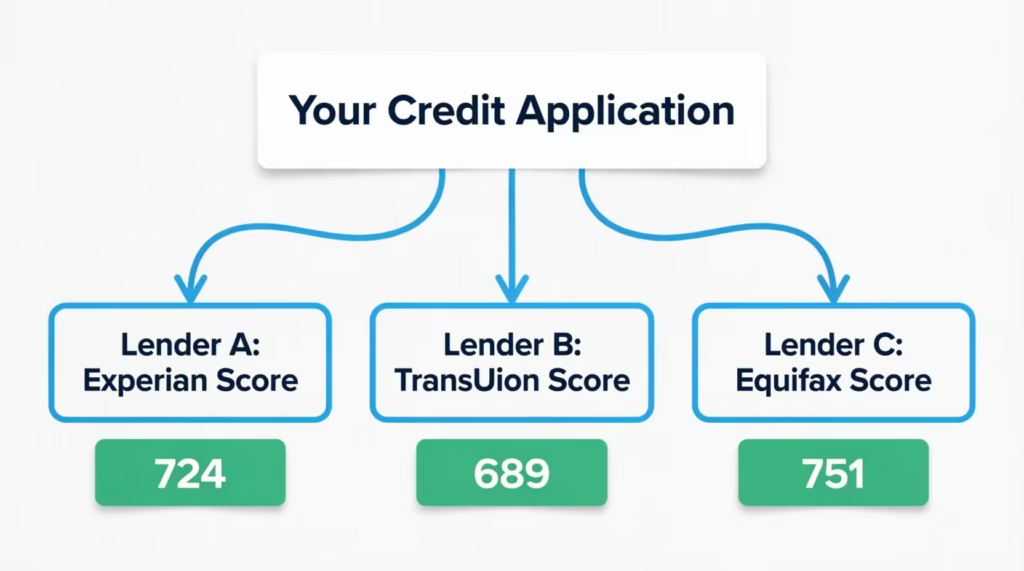

When you sit down in the dealer finance office, the F&I manager often submits your application to several lenders at once. This is called a multi-lender pull. Within an hour, you might see three, five, or even ten different credit scores come back, all on the same you, on the same day.

That’s not a glitch, and no one is playing games with your file. Each lender works with one credit bureau: Equifax, Experian, or TransUnion. They also use their own scoring model.

This could be FICO Auto Score 8, Auto Score 9, an older Auto version, or a bureau-branded score. So Lender A might pull an Experian FICO Auto Score 8 and read 702. Lender B pulls TransUnion FICO Auto Score 9 and reads 688. Lender C pulls Equifax Beacon 9.0 and reads 715.

All three numbers are legitimate. They’re just three different measurements of the same underlying credit file.

This is a structural feature of how auto lending works, not something the dealer controls or manipulates. Knowing this helps you focus on the right question. Instead of asking “why is my score different?”, ask “which lender’s offer gives me the best rate and terms?” That’s the number that actually matters for which credit score for auto loan decisions to trust.

💡 Pro Tip: If a lender quotes a score that seems way off from the others, ask which bureau and which scoring model they used. You have the right to know, and the answer usually explains the gap immediately.

How the Auto Score Weighs Your Credit History Differently

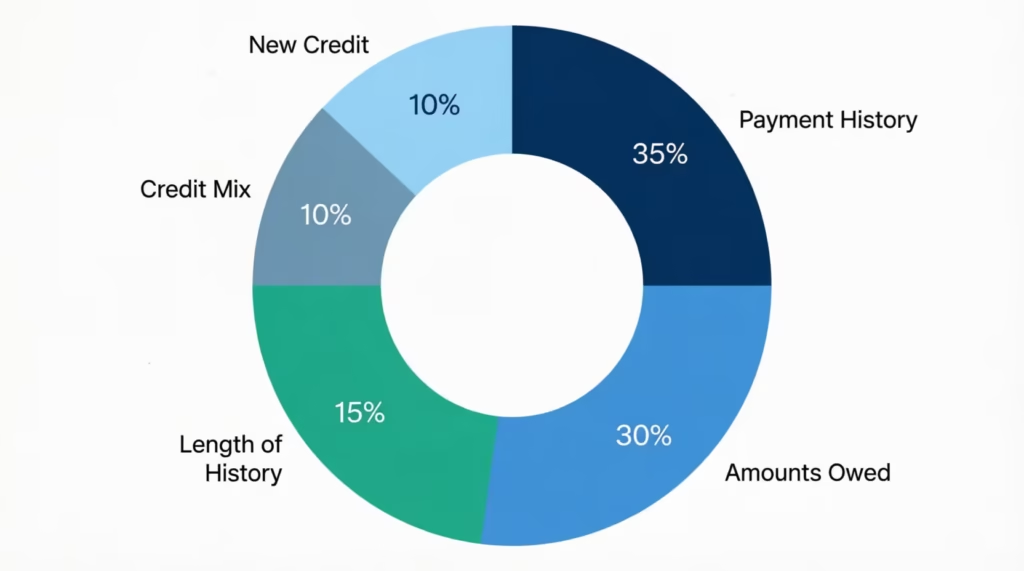

The auto scoring model looks at the same five core factors as a regular FICO score, but the weights shift in ways that matter for a car buyer.

Payment history is still the biggest driver at roughly 35% of the score. Amounts owed (your credit tier depends heavily on this), length of credit history, credit mix, and new credit fill in the rest. That much is standard.

What changes is the emphasis inside payment history. Auto-loan-specific behavior gets more weight in a FICO Auto Score than it does in a base FICO. That means:

- On-time car payments over the last 24 months help your auto score more than they help your general score.

- A single late auto payment can hurt your auto score more than a late credit card payment would.

- A past repossession or auto-loan charge-off is a much bigger drag here than on a general score.

The practical implication: if you have limited time before applying, prioritize anything auto-related. Bringing a past-due car payment current will move your auto score faster than paying down an unrelated credit card. Same effort, more result.

If your auto history is clean but your general credit needs work, don’t stress. A clean car-payment record boosts your FICO auto score. This means you’re doing better than your general score might show.

What Your Score Means for Your Interest Rate Right Now

This is where the score turns into real money. Your credit tier determines your APR, and even small tier differences translate into thousands of dollars over a five- or six-year loan.

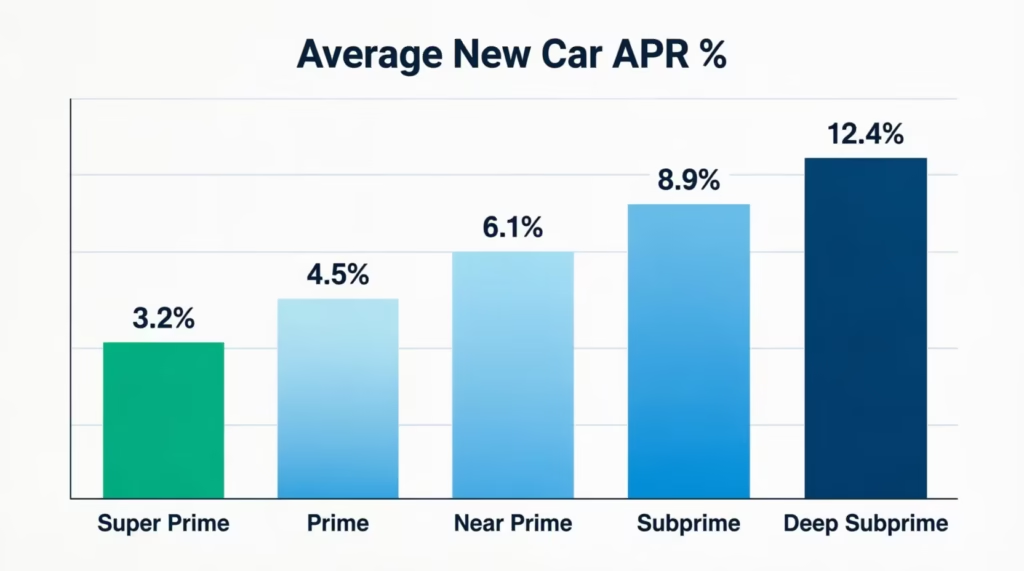

The most recent data from Experian’s State of the Automotive Finance Market Report breaks down the average auto loan interest rate by credit score as follows:

| Credit Tier | Score Range | Avg. New Car APR | Avg. Used Car APR |

|---|---|---|---|

| Super prime | 781+ | 5.18% | 6.82% |

| Prime | 661–780 | 6.70% | 9.06% |

| Near prime | 601–660 | 9.83% | 13.74% |

| Subprime | 501–600 | 13.22% | 18.99% |

| Deep subprime | 300–500 | 15.81% | 21.58% |

Source: Experian (rates published Q1 2025 data; individual rates vary by lender and updated quarterly)

Here’s what that looks like in real dollars. Take a $35,000 new car loan over 60 months:

- Super prime at 5.18%: monthly payment about $664, total interest around $4,830.

- Near prime at 9.83%: monthly payment about $741, total interest around $9,478.

- Subprime at 13.22%: monthly payment about $797, total interest around $12,829.

The gap between super prime and subprime on the same car is nearly $8,000 in extra interest. That’s why even a 30-point score bump before you apply can be worth the wait.

Keep in mind these are averages. Your actual rate depends on the lender, the vehicle, the loan term, your down payment, and whether you’re financing new or used. Used car rates run 2 to 6 points higher across every tier because used vehicles carry more risk for the lender.

📌 Did You Know: Experian’s data shows the average monthly new-car payment hit a record $770 in early 2026, per LendingTree’s analysis of the latest Experian figures. Score tier is now a bigger factor in affordability than it was five years ago.

Does Shopping for a Car Loan Hurt Your Credit?

Short answer: not if you do it in a focused window. The fear of hurting your score is what stops most buyers from rate shopping, and that fear costs them real money.

First, understand the soft inquiry vs hard inquiry difference. A soft inquiry happens when you check your own credit, or when a lender pre-screens you for an offer. Soft inquiries don’t affect your score at all. Ever.

A hard inquiry happens when a lender formally pulls your credit as part of an application. Each hard inquiry can drop your score by less than five points, according to myFICO’s rate shopping guidance. The impact is small and fades within a year.

The important part for car buyers: the rate shopping window. FICO’s scoring models treat multiple auto-loan inquiries as a single inquiry, as long as they happen within a focused time frame. Newer FICO versions use a 45-day window. Older versions use 14 days. FICO also ignores any auto-loan inquiries from the past 30 days when calculating your current score, giving you breathing room.

Practical rule: keep all your rate shopping inside a 14-day window, and you’re safe on every FICO version, old or new. Get quotes from your bank, a credit union, and the dealer, all in the same two-week stretch, and your score sees it as one shopping event, not five.

So the answer to does checking credit hurt score is: your own checks never do, and formal applications only do if you spread them out over months. Shop smart, shop fast, and rate-shopping is free.

How to Check Something Closer to Your Real Auto Score Before You Go

You can get much closer to the score the dealer will see. It takes about 20 minutes and, in one case, a small fee.

1. Buy your actual FICO Auto Scores.

Go to myFICO.com and pull the “3-Bureau” report package. It shows your FICO Auto Score 8 and Auto Score 9 from all three bureaus. This is the closest number to what the dealer will pull. There’s a fee, usually around $30 to $40 for a one-time pull, but it’s the only way to check FICO auto score numbers directly.

2. Use free apps for a directional read.

Credit Karma (VantageScore), Experian’s free app (base FICO 8), and your bank’s free score tool won’t match the auto number exactly. But if all three show you in the 700s, you’re very likely prime tier at the dealer too. If they show you in the 550s, expect subprime pricing.

3. Review your full credit report for accuracy.

Get all three reports free once a week at AnnualCreditReport.com. Look specifically at:

- Any auto loans in the last 5 years, current and paid-off. Verify payment history is correct.

- Repossessions, charge-offs, or collections tied to a car. These hurt your auto score more than they hurt a general score.

- Overall credit report accuracy — wrong balances, wrong open/closed status, or accounts that aren’t yours.

4. Get a pre-qualification, not a pre-approval.

A pre-qualification with a bank or credit union uses a soft pull. It gives you an estimated rate without touching your score. Capital One Auto Navigator, Chase Auto pre-qualification, and most credit unions offer this. It’s the safest way to get a real rate estimate before the dealer runs a hard inquiry.

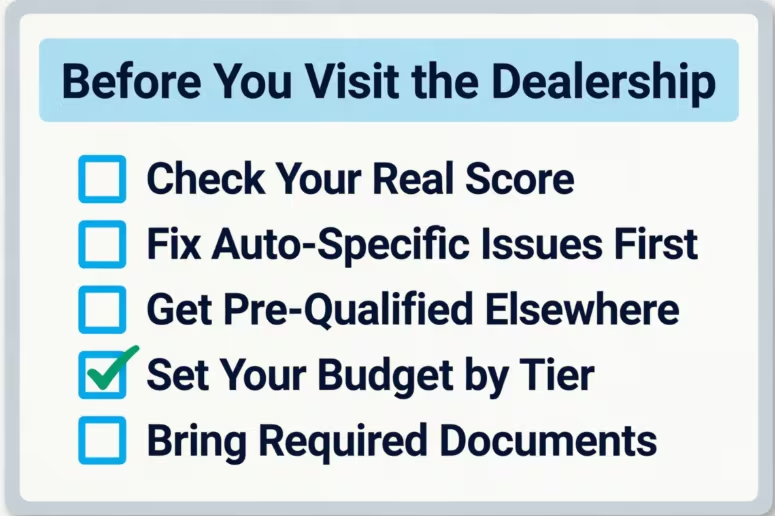

How to Prepare Before You Visit the Dealership

Everything above becomes useful only if you turn it into action. Use this checklist in the day or two before your visit.

Step 1: Know your real credit standing.

Pull your FICO Auto Scores from myFICO if possible, or at least check your VantageScore and base FICO 8 on free apps. Note which credit tier you likely land in (super prime, prime, near prime, subprime, deep subprime). This becomes your rate benchmark.

Step 2: Fix auto-specific issues first.

If you have late car payments, a repossession, or an unpaid auto-loan collection, handle those first. Then, you can pay down unrelated credit cards. In the auto-scoring model, one clean car-payment history moves your number faster than clearing a $2,000 credit card balance. This is the single biggest way to prepare for dealership financing.

Step 3: Get pre-qualified with an outside lender.

Before you walk into the dealer finance office, get a pre-qualification or a full pre-approval from your own bank or a credit union. Credit unions in particular tend to offer rates 0.5% to 1.5% below dealer averages for the same tier. Bring the pre-approval paperwork with you. It gives you a hard number to compare against whatever the dealer offers.

Step 4: Set your budget based on your tier.

Match your expected APR to the Experian tier table above, then plug it into a loan calculator with your target price and down payment. Now you know your realistic monthly payment range before you fall in love with a specific vehicle. This stops upselling before it starts.

Step 5: Bring your documents.

- Driver’s license

- Proof of income: two recent pay stubs or last year’s tax return (if self-employed)

- Proof of residence

- Proof of insurance

- Trade-in title (if applicable)

Missing documents is the fastest way to lose leverage in the finance office.

⚠️ Mistake to Avoid: Never let the dealer be your first credit pull of the day. Once they submit your application to multiple lenders, you’ve committed to their process. Get your outside pre-approval first so you’re negotiating from strength.

What to Do If Your Score Is Lower Than You Expected

You did your homework, walked in prepared, and the finance manager still quoted a number 40 points below what you expected. Here’s what to do next, in order.

Ask which bureau and which model were used

You have a legal right to know. Ask for the specific reason codes on the report as well; these are short phrases like “too many recent inquiries” or “balances too high on revolving accounts.” Reason codes tell you exactly what pulled the score down. If one error causes the drop, like a paid account showing as unpaid, the finance manager can often rerun the application after you dispute it.

Offset the tier with structure, not desperation

A larger down payment can move you into better loan terms even if your score doesn’t change. So can a shorter loan term (48 months instead of 72), which lenders view as lower risk. Both can shave 1 to 3 points off the APR a lower-than-expected credit score would otherwise get you.

Get quotes elsewhere before signing

Remember that a single lender’s read is not the final verdict. Because of multi-lender variance, your credit union or bank might read the same file 20 to 40 points higher. Walk out with the paperwork, run one more application at a credit union that afternoon, and compare. This one step often saves buyers thousands over the loan.

Consider pausing to improve credit

If the rate difference between your current tier and the next tier up is more than 3%, and the score fix would take under 90 days (paying down a maxed card, disputing an error, waiting for an old late payment to age past the 12-month FICO cutoff), pausing is often the better financial move. On a $30,000 loan, moving from near prime to prime can save $4,000 to $6,000 in total interest. That’s worth three months of driving your current car.

Explore alternate financing paths

Dealer financing optionsaren’t your only route. Credit unions often approve borrowers dealer lenders decline. Buy-here-pay-here lots exist for deep subprime buyers, but rates and terms are usually harsh, so treat them as a last resort. Some manufacturers also run subprime programs on specific models. Ask about them explicitly.

Frequently Asked Questions (FAQs)

What credit score do dealerships use?

Dealers rely on FICO Auto Scores, usually version 8 or 9, not the VantageScore you see on free apps like Credit Karma. These scores run on a 250 to 900 scale and weigh auto-loan history more heavily.

Do car dealerships use TransUnion or Equifax?

Dealerships don’t stick to one bureau. Lenders choose Equifax, Experian, or TransUnion based on their own contracts, and some pull two or all three before deciding which score to use.

Which FICO score do most car dealerships use?

FICO Auto Score 8 is the most common version, used by many banks and captive lenders like Ford Credit and Toyota Financial Services. FICO Auto Score 9 is newer and treats paid collections more forgivingly.

Do auto lenders use FICO 8 or 9?

Both are common, and which one appears depends on the lender’s contract with the credit bureau. Some smaller lenders and credit unions still use older versions like Auto Score 2, 4, or 5.

What credit score do you need to buy a $30,000 car?

A score in the near-prime range (601 to 660) or higher gives you a reasonable shot at approval, though your rate improves significantly at prime (661 to 780) and super-prime (781+) tiers. Near-prime buyers averaged 9.83% APR on new cars as of Q1 2025.

Why is my TransUnion score higher than Equifax?

Not every creditor reports to all three bureaus, and reporting timing varies between them. A paid-off card might show as closed on one bureau’s file and still open on another’s, shifting your score by five to fifteen points.

Does shopping around for a car loan hurt your credit?

Checking your own credit or getting pre-qualified never affects your score, since those are soft inquiries. Hard inquiries from formal applications drop your score less than five points each, and FICO treats multiple auto inquiries within a 14-day window as a single inquiry.

What is a good TransUnion credit score to buy a car?

A score of 661 or higher puts you in prime territory, qualifying you for an average 6.70% APR on a new car. Scores above 781 land in super-prime, dropping the average new-car rate to 5.18%.

What should I do if my score is lower than expected at the dealership?

Ask which bureau and scoring model the lender used, since results vary widely between lenders. You can also request a larger down payment or shorter loan term to offset the tier, or get a second quote from a credit union before signing.

What documents should I bring to the dealership?

Bring your driver’s license, proof of income like recent pay stubs, proof of residence, proof of insurance, and your trade-in title if applicable. Missing documents can weaken your negotiating position in the finance office.

Wrapping Up

Walking into a dealership is a lot less stressful once you know the rules of the score behind the desk. Dealers rely on FICO Auto Scores on a 250 to 900 scale, not the VantageScore on your free app, and multiple lenders can legitimately produce different numbers for the same file on the same day.

To get the best deal, most buyers should check their FICO Auto Scores first. Then, they should get a pre-approval from a credit union. Finally, shop for quotes within a 14-day window.

If you know someone buying a car soon, share this guide. A wrong assumption in the finance office can cost them thousands over the loan’s life.