Losing a vehicle to the lender is stressful enough. Then you check your credit report and see the damage, and the panic hits all over again. How many points does a repossession drop your credit score? The answers online swing wildly, from “just 50 points” to “over 200,” and none of them explain why the range is so wide or which number fits your situation.

Here’s the short answer: most repossessions drop a credit score by 50 to 150 points, with around 100 points being typical.

Below, we’ll break down exactly what drives your number, what recovery looks like, and the smart moves to make right now.

Key Takeaways

This guide explains how many points a repossession drops a credit score, covering the typical 50 to 150 point range, the factors that determine your exact number, and a realistic multi-year recovery timeline.

Core Facts:

- A repossession typically drops a credit score by 50 to 150 points, with around 100 points cited as a common average figure.

- The point drop depends on starting credit score, existing derogatory marks, account mix, and which scoring model the lender pulls.

- Higher starting scores lose more points: a 750 score can drop 130 to 150 points, while a 580 score may drop only 50 to 70 points.

- Missed payments at 30, 60, and 90 days often cause more cumulative score damage than the repossession entry itself.

- Voluntary and involuntary repossession are both reported as repossessions and cause a similar score impact, staying on reports for seven years.

- Recovery is fastest in the first two years, with 30 to 50 points often regained in year one and 40 to 60 more in year two.

Best for:

- Readers who recently had a vehicle repossessed and want to understand the actual size of the score impact.

- People deciding between voluntary surrender and waiting for involuntary repossession.

- Anyone planning a credit recovery timeline after a repossession, including deciding when to apply for new credit.

How Many Points Does a Repossession Drop Your Credit Score?

A repossession typically drops your credit score by 50 to 150 points, and the most commonly cited average is right around 100 points. Capital One’s auto finance education team puts the figure at “approximately 100 points or more,” which lines up with what most credit experts see in the real world.

But this is a range, not a fixed number. Two people can have the same car repossessed on the same day and see very different point drops. The next section explains why that happens.

One more thing to know up front. This 50 to 150 point range reflects the combined damage. It’s not just the repossession line item on your report. It also includes the missed payments that came before it and any charge-off that gets added after. The repossession by itself is only one piece of the total credit score drop.

Why the Point Drop Varies So Widely

The reason the number moves so much comes down to how credit scoring models work. A repossession is a derogatory mark, meaning it’s a serious negative entry. But scoring models don’t apply a flat “minus 100” to everyone. They look at your full credit picture and decide how much this new mark shifts your risk profile.

Four main variables control your personal number:

- Your starting credit score before the repo hit

- Existing derogatory marks on your report (past lates, collections, another repo)

- Your account mix (how many other loans and cards you have in good standing)

- The scoring model the lender pulls (FICO 8, FICO 9, VantageScore 3.0, VantageScore 4.0)

If you had a clean credit file with one auto loan and nothing else, a repossession is a huge shock to the system. If you have late payments, a maxed-out credit card, and high credit use, a repo adds to your troubles. So, its impact is less significant.

The next two subsections cover the two biggest drivers.

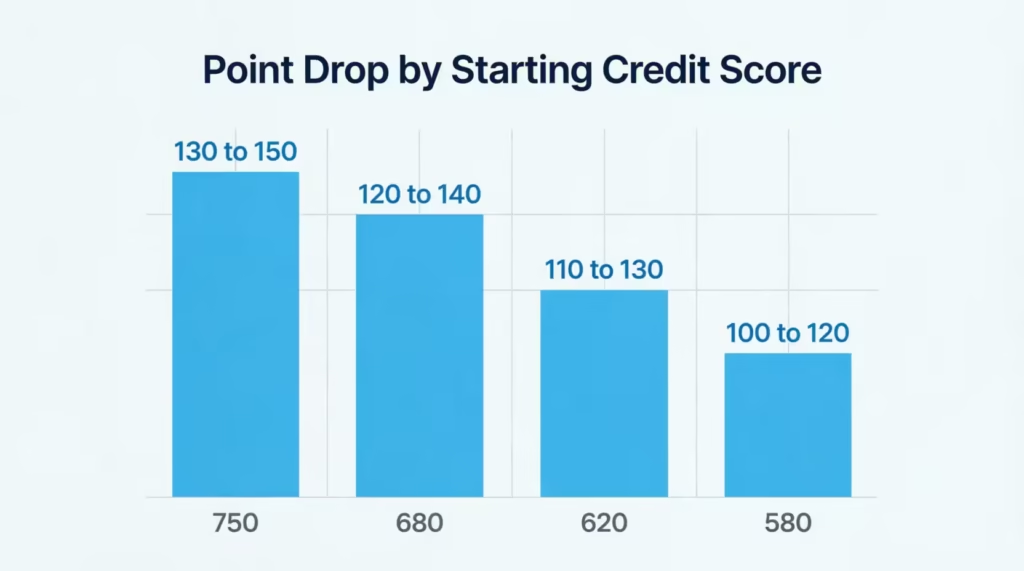

Your Starting Credit Score Is the Biggest Factor

This one surprises people, but the higher your score before the repo, the more points you lose. Scoring models penalize the fall from “good credit” harder than the fall from “already-damaged credit.”

Here’s roughly how it plays out:

| Starting Credit Score | Typical Point Drop After Repossession | Where You Land |

|---|---|---|

| 750 (very good) | 130 to 150 points | Around 600 to 620 |

| 680 (good) | 90 to 110 points | Around 570 to 590 |

| 620 (fair) | 60 to 80 points | Around 540 to 560 |

| 580 (poor) | 50 to 70 points | Around 510 to 530 |

A borrower at 750 has more to lose. The scoring model already assumes low-score borrowers carry more risk, so adding a repo doesn’t change the risk picture as sharply. That’s why a subprime borrower at 580 might only drop 50 to 70 points, while a prime borrower at 750 can lose 130 to 150.

📌 Did You Know: Two people can start at very different scores, get the same repossession, and end up at almost the same low score. Scoring models tend to push most people with a fresh repo into the 500 to 600 range no matter where they began.

FICO vs. VantageScore Can Calculate It Differently

Here’s a detail that catches people off guard. You have more than one credit score. FICO and VantageScore are the two main scoring companies, and each one has multiple versions. Your bank might pull FICO 8. Your credit card app might show VantageScore 3.0. Your auto lender might use an auto-specific FICO version.

Because each model weighs the repossession slightly differently, the same event can show a different point drop on each score. It’s normal to see, say, a 95-point drop on your Experian FICO and a 120-point drop on your Equifax VantageScore for the same repo.

This is also why the “how many points” question doesn’t have one true answer. There is no single credit score. There are many, and they don’t have to agree.

The Repo Entry vs. the Missed Payments That Led to It

This is the biggest misconception around repossession credit damage, so it’s worth slowing down.

When people say “the repo dropped my score 100 points,” they’re usually looking at their payment history damage plus the repossession entry combined. Those are two separate things, and much of the harm is done before the car ever leaves the driveway.

Here’s how the layering works:

- You miss a payment. At 30 days late, the lender reports it to the bureaus. Your score can drop 50 to 100 points from this single late alone if you had a high starting score.

- You miss another payment. At 60 days late, a second late payment posts. Another 20 to 40-point hit is possible.

- You miss a third. At 90 days late, a third late shows up. Score keeps dropping.

- The lender repossesses the vehicle. A “repossession” entry gets added to the account tradeline. This is a fresh derogatory mark on top of everything above.

- Often, a charge-off gets added a few weeks later when the lender writes off the remaining balance. Another negative entry.

So by the time the tow truck actually arrives, most of the score damage may already be locked in from the 30, 60, and 90-day lates. The repossession line item itself adds more damage, but it’s the final blow, not the whole fight.

This matters because it changes what you can and can’t undo. You can’t remove accurate late payments. You also can’t remove an accurate repossession. But knowing the damage came in layers helps you understand why “fixing” the repo won’t reverse the whole score drop.

⚠️ Mistake to Avoid: Don’t assume that catching up on payments right before repossession will prevent all the score damage. The 30, 60, and 90-day lates are already reported and are already dragging your score down before the vehicle is taken.

Does Voluntary Repossession Affect Your Score Differently Than Involuntary?

Short answer: no, not in a meaningful way.

Both voluntary and involuntary repossession get reported to the credit bureaus as a repossession. Both stay on your credit report for seven years. Both cause a similar point drop. Experian’s credit education team confirms that a voluntary surrender is still considered a negative mark because it shows you couldn’t meet your obligation to repay the loan.

So what’s the actual benefit of voluntary surrender? It’s real, but it’s not about your credit score:

- Lower fees: You avoid tow truck charges, storage fees, and sometimes legal costs the lender would otherwise add to what you owe.

- More control over timing: You can pick when and where to drop off the vehicle instead of getting surprised at 6 AM in the driveway.

- Less stress: No public repo event, no scene at your workplace, no chase.

Also, the missed payments that pushed you into surrender are the same missed payments that would have led to involuntary repo. The secured debt was going to default either way. Voluntary just changes the last step.

In short, if you have to pick between voluntary and involuntary, go for voluntary. Choose it for the financial and personal benefits, not just to protect your credit score. It won’t.

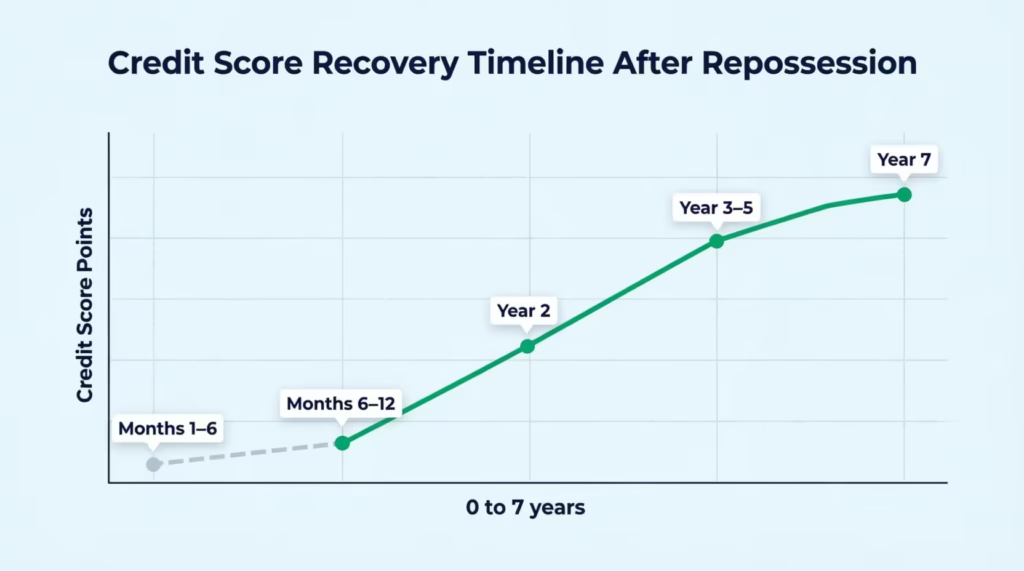

How Long the Score Drop Lasts and How Recovery Looks

A repossession stays on your credit report for seven years, starting from the date of the first missed payment that led to the default. This is confirmed by Experian and applies to both voluntary and involuntary repos.

But here’s the part that gets missed. “Seven years on the report” is not the same as “seven years of maximum damage.” The impact fades, and it fades a lot faster than most people expect if you add positive credit behavior.

A realistic recovery curve looks like this:

- Months 1 to 6: Score is at its lowest. Getting approved for new credit is hard. Existing credit card interest rates may go up.

- Months 6 to 12: With on-time payments on any remaining accounts, low credit utilization, and no new missed payments, the score starts creeping back. A 30 to 50 point recovery is common in year one.

- Months 12 to 24: The repo starts to “age.” Newer positive activity carries more weight in the scoring model. Many people recover another 40 to 60 points in this window.

- Years 2 to 5: Continued positive activity pushes the score higher. By year three or four, some people are back to near-prime scores even with the repo still on their report.

- Year 7: The repo drops off entirely, and any remaining drag on your score disappears.

Does the Impact Stay the Same the Whole Time?

No. This is one of the most important things to understand about recovery. The score hit is heaviest in the first 12 months. After that, the damage decays steadily.

Scoring models are designed to weight recent behavior more than old behavior. A repossession from six months ago screams “current risk.” A repossession from four years ago, with four years of on-time payments after it, says “past problem, current stability.” Same entry, very different weight in the score.

That’s why waiting isn’t a strategy, but working the timeline is. Every month of clean payments after the repo pushes it further into the past and lowers its scoring weight.

How a Repossession Compares to Other Negative Credit Events

Context helps. A repossession is serious, but it’s not the worst thing that can happen to a credit report. Here’s how it stacks up against other common negative events:

| Negative Event | Typical Point Drop | Time on Credit Report |

|---|---|---|

| Single 30-day late payment | 50 to 100 points | 7 years |

| Multiple lates + repossession | 50 to 150 points combined | 7 years |

| Charge-off | 50 to 150 points | 7 years |

| Collection account | 50 to 100 points | 7 years |

| Chapter 7 bankruptcy | 130 to 240 points | 10 years |

| Chapter 13 bankruptcy | 130 to 200 points | 7 years |

Two takeaways for the subprime borrower or anyone comparing options:

- A repossession is roughly comparable to a charge-off in severity, which makes sense because most repos come with a charge-off attached.

- Bankruptcy is worse, both in point drop and how long it stays on the report. Chapter 7 sits for 10 years, three years longer than a repo.

If you’re thinking about letting a car go or filing for bankruptcy to keep it, remember this: repossession often hurts your credit score less. A repo is serious. Bankruptcy is more serious and lasts longer.

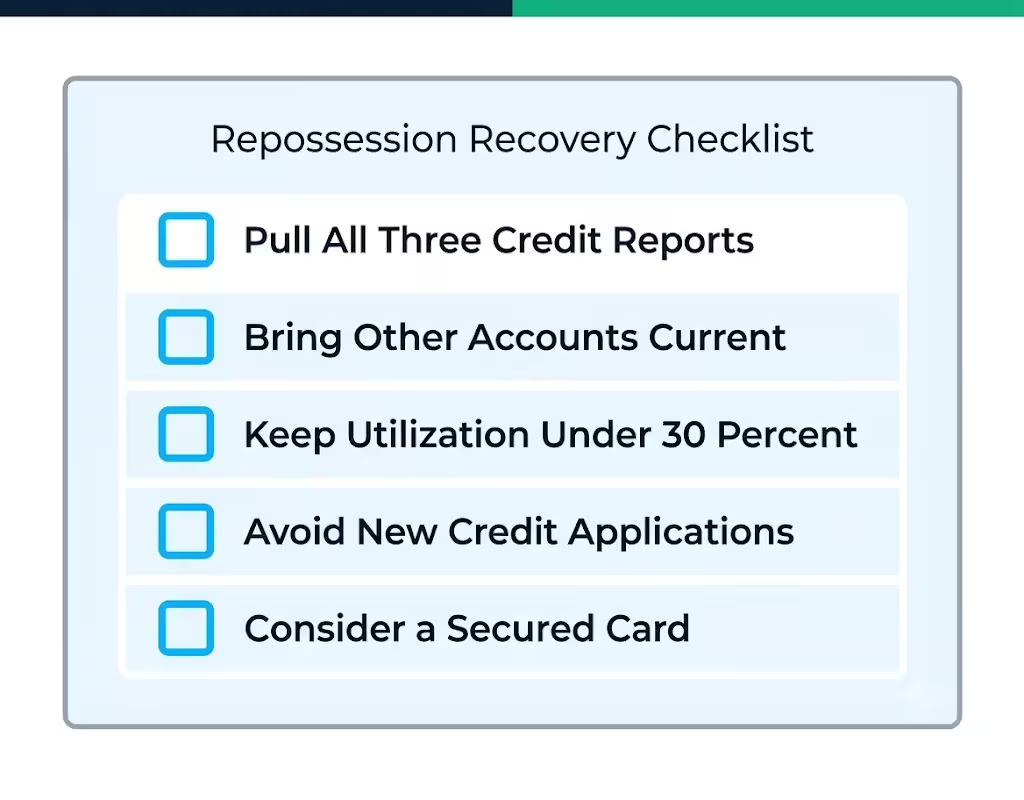

What You Can Do Right Now About the Score Drop

You can’t erase an accurate repossession. But you can make sure the damage isn’t worse than it should be, and you can start the recovery clock today.

Step 1: Pull all three credit reports for free. Get one from each bureau at AnnualCreditReport.com. Check that the repo is reported accurately on each. Look for:

- Wrong dates (the “date of first delinquency” controls the 7-year clock)

- Wrong balance owed

- Duplicate entries (same repo showing twice)

- A repo reported by both the original lender and a collection agency as two separate accounts

If any of this is wrong, dispute it in writing with the bureau that has the error. An inaccurate entry can be fixed. An accurate one can’t.

Step 2: Bring every other account current. If you have credit cards or other loans, do not miss a payment on those. Right now, every on-time payment is a green flag the scoring model needs to see.

Step 3: Keep credit utilization low. Try to keep credit card balances under 30% of their limits, and under 10% is better. Utilization is one of the fastest levers to move a score in the short term.

Step 4: Don’t apply for a bunch of new credit. Every hard inquiry drops the score a few more points. Wait until the score has recovered before shopping for new cards or loans.

Step 5: Consider a secured credit card or credit-builder loan. Adding a new positive tradeline (with on-time payments) after the repo helps the scoring model see you as trending in the right direction.

💡 Pro Tip: Set up autopay on every account you keep, even for just the minimum payment. One missed payment can undo months of progress. Most late payments happen because people forget due dates, not because they lack money.

Does Paying Off the Deficiency Balance Help Your Score?

A deficiency balance is what you still owe after the lender sells the repossessed vehicle at auction. If the car sold for less than the loan balance plus fees, that leftover amount is your deficiency.

Paying it off is a good idea, but here’s the honest truth about credit impact:

- Paying the deficiency does not remove the repossession entry from your report.

- It does update the status to “paid” or “settled” instead of “unpaid,” which looks slightly better to future lenders reviewing your report manually.

- It prevents further damage, like the debt being sold to a collection agency, which would add a brand new collection entry to your report.

So the credit repair benefit is modest. Some scoring models, like FICO 9 and VantageScore 4.0, ignore paid collections. However, older models still include them. The bigger reason to pay the deficiency is to stop new damage, not to reverse old damage.

If you can settle for less than the full amount, get the settlement agreement in writing before you pay. Confirm it will be reported as “paid” or “settled in full” to all three bureaus.

How This Affects Getting Approved for Credit Going Forward

In the first 12 to 24 months after a repossession, expect these realities:

- Auto loans: You can still get approved, but almost only through subprime lenders at high APRs, often 15% to 24% or more. Down payments of 20% or more are typically required.

- Credit cards: Prime cards will decline you. Secured cards and subprime unsecured cards will approve you, often with low limits (200 to 500 dollars) and annual fees.

- Mortgages: Most lenders want to see 2 to 4 years of clean credit after a repo before approving a mortgage, though FHA and VA loans can be more flexible.

- Apartment rentals: Some landlords deny applicants with a recent repo. Others accept with a larger security deposit.

The good news is that this tightens up quickly. By month 18 to 24 with clean behavior, doors start opening again. By year 3, you’re usually back to standard, not subprime, offers on most products.

Frequently Asked Questions (FAQs)

How much will my credit score go down with a repossession?

Most repossessions drop a credit score by 50 to 150 points, with around 100 points being typical. Your exact number depends on your starting score, existing derogatory marks, and which scoring model gets pulled.

Should I pay off a repossession?

Paying off the deficiency balance won’t remove the repossession entry from your report, but it updates the status to paid or settled and stops new damage like a collection account being added. The bigger benefit is preventing further harm, not reversing old damage.

Do repossessions fall off after 7 years?

Yes, a repossession stays on your credit report for seven years starting from the date of the first missed payment that led to default. Once that period ends, the entry drops off completely, and any remaining drag on your score disappears.

Is it better to surrender or repo a car?

Voluntary surrender doesn’t reduce the credit score impact compared to involuntary repossession, since both get reported the same way and stay for seven years. Voluntary surrender does help you avoid tow and storage fees and gives you more control over timing.

How fast can you rebuild credit after a repo?

A 30 to 50 point recovery is common in the first year with on-time payments and low credit utilization. Another 40 to 60 points often comes back in months 12 to 24 as the repo starts to age.

Can you have a 700 credit score with a repo?

It’s uncommon in the first year but becomes realistic over time, since the repo’s scoring weight fades as more positive activity builds up after it. Some people reach near-prime scores by year three or four even with the repo still listed.

How long can you be behind before they repo your car?

Lenders typically begin repossession after three missed payments, around the 90-day mark, though this varies by lender and state. Score damage from 30, 60, and 90-day late payments builds up well before the vehicle is actually taken.

How does a repossession compare to other negative credit events?

A repossession’s 50 to 150 point drop is roughly similar to a charge-off, since most repos come with one attached. Bankruptcy is worse, dropping 130 to 240 points and staying on reports for 10 years instead of 7.

Can I get approved for a car loan after a repossession?

You can usually still get approved through subprime lenders in the first 12 to 24 months, but expect APRs of 15% to 24% or more. Lenders typically require a down payment of 20% or more during this period.

Does paying off the deficiency balance help my credit score?

Paying the deficiency updates your account status to paid or settled but doesn’t erase the repossession entry itself. Some newer scoring models like FICO 9 ignore paid collections, while older models still count them.

Wrapping Up

A vehicle repossession usually drops a credit score by 50 to 150 points, with a starting score, existing derogatory marks, and the scoring model deciding where in that range you land. Most of the damage happens from missed payments before the repo. The repo entry itself doesn’t cause as much harm. Also, voluntary surrender doesn’t lessen the credit impact.

To improve your score, check all three reports for accuracy. Keep your accounts current and add positive tradelines in the first year.

If you know someone facing a repo notice, this guide could save them from making costly assumptions about their credit damage. Please share it.