Getting turned down for a mortgage or auto loan because your credit score is too thin or too damaged is stressful. You’ve probably seen ads promising fast score jumps if you buy an authorized user spot on someone’s aged credit card.

The problem is knowing which offers are real, which are scams, and whether the boost will even last long enough to help you close on that loan. That’s why picking the best tradelines to boost credit score results has to be done carefully, with the right facts.

The short answer is that the best tradeline is a seasoned credit card account with low utilization. You should be added as an authorized user, ideally through a trusted family member at no cost. If that’s not an option, think about using a reputable broker, but only if you fully understand the risks involved.

Here’s a quick guide on how tradelines work. You’ll learn about the score boost you can expect, the mortgage red flags to notice, and safer, low-cost alternatives.

Key Takeaways

This guide explains how to evaluate and safely buy the best tradelines to boost credit score, covering which account factors matter, realistic score changes, legal risk, scam signs, and free alternatives.

Core Facts:

- A tradeline boost typically lasts two statement cycles, roughly 60 to 70 days, then the account can remain on the report for another 30 to 60 days before dropping off.

- The four factors that drive score movement are account age, credit limit, utilization under 10 percent, and a perfect payment history on the tradeline.

- Paid tradeline prices in 2026 range from about 200 to 400 dollars for entry-level accounts up to 1,200 to 2,500 dollars or more for premium accounts.

- Fannie Mae underwriting guidelines allow lenders to require proof of relationship for authorized user accounts and can discount the account if proof is not provided.

- Being added as an authorized user is legal, and the Equal Credit Opportunity Act requires lenders to consider authorized user account data on a credit report.

- Free alternatives mentioned include becoming an authorized user on a family member’s card, opening a secured credit card, taking a credit builder loan, and reporting rent payments.

Best for:

- Readers with a thin credit file or high utilization deciding whether a paid tradeline fits their specific credit gap.

- Readers preparing for a mortgage or auto loan who need to understand the legal and underwriting risks before buying a tradeline.

- Readers who want to evaluate a tradeline broker for legitimacy before paying, or who want free alternatives instead.

What “Buying a Tradeline” Actually Means

A tradeline is any account on your credit report. That includes credit cards, auto loans, student loans, and mortgages. When people say “buying a tradeline,” they almost always mean paying a broker to add you as an authorized user (AU) on a stranger’s seasoned credit card account.

Here’s how it works. The primary account holder owns the card. They’ve had it open for years, kept the balance low, and paid on time every month. A broker matches them with a buyer, adds the buyer’s name as an authorized user, and the card’s history starts showing up on the buyer’s credit report. The buyer never gets the physical card. They can’t spend on the account. They’re just borrowing the account’s good history for a short window, usually two statement cycles.

This practice is called credit piggybacking. Family members do it for free all the time. A parent adds a college student. A spouse adds a partner. That’s legal, common, and how many people build their first credit file. Paid tradelines are different because money moves between strangers with no real connection.

It helps to understand what you’re not buying. You’re not buying a loan. You’re not buying a new credit account in your own name. You’re not buying anything that stays on your report forever. You’re renting a slot on someone else’s card, and when that slot ends, the account usually drops off your report within one or two reporting cycles.

That distinction is important. A legitimate tradeline in your name, like a secured card, helps you build credit that you own. When you open and pay on time, it makes a difference. A purchased AU tradeline just borrows someone else’s history to make your file look stronger for a short time.

How Authorized User Tradelines Affect Your Credit Score

When a card issuer reports an authorized user account to the credit bureaus, the account’s full history often gets folded into that user’s credit file. If the card has 12 years of on-time payments, a $25,000 limit, and a $500 balance, all of that data can start counting toward the AU’s score.

Both the FICO scoring model and VantageScore include authorized user accounts in their calculations, though the exact weight can vary. FICO 8, the most widely used version by lenders, gives real weight to AU accounts as long as the issuer reports them. Not every issuer reports AU data to all three bureaus, which is one reason results are uneven.

The score change happens because the added account changes the math on several parts of your credit profile at once. Your average account age can go up. Your total available credit can jump. Your overall utilization ratio can drop. If your file was thin before, you might suddenly have enough account history to generate a score at all.

That said, the newer FICO 10 and FICO 10T versions treat AU accounts more cautiously. Lenders using those models may weight the AU account less if it looks like a piggybacking attempt rather than a real family relationship. VantageScore 4.0 also filters some AU data. So the same tradeline can move your score a lot on one report and only a little on another.

Which Tradeline Factors Matter Most

Not every seasoned account will help you the same way. Four features drive almost all the score movement.

Account age. Older is better. A card opened in 2008 helps more than one opened in 2020. Age of accounts feeds into “length of credit history.” If your own oldest account is only two years old, an aged AU account can pull up your average age fast.

Credit limit. A higher limit gives you more available credit, which lowers your overall utilization ratio. A $30,000 limit card with a $300 balance adds $29,700 of unused credit to your file.

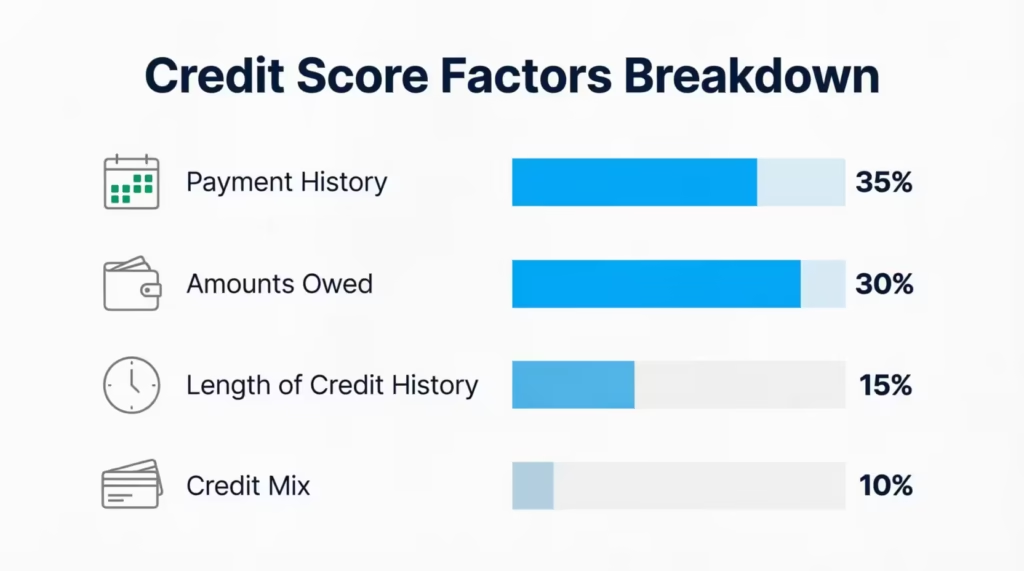

Utilization on that card. Utilization is the balance divided by the limit. You want the AU card to sit under 10% utilization every month. A card that’s maxed out will hurt you, not help you. Amounts owed on accounts make up 30% of your FICO Score, so myFICO reports that debt levels strongly predict future credit performance.

Payment history. One missed payment on the AU card can show up on your report. That’s the biggest risk. Payment history is the single largest scoring factor at 35% of the FICO Score, and one 30-day late can knock 60 to 100 points off a strong file.

The best tradeline stacks all four factors: old, high limit, very low utilization, and a perfect payment record. Miss any one of these and the boost shrinks fast.

Matching the Right Tradeline to Your Credit Gap

Buying the wrong tradeline is like buying vitamins for a broken leg. It doesn’t fix what’s actually wrong. Before spending money, figure out which part of your credit profile is weakest, then pick a tradeline that targets that specific gap.

If you have a thin credit file with only one or two accounts, your problem is not enough history. In this case, a seasoned tradeline with a long age (10+ years) does the most work. Age lifts your average account age, and the extra account gives scoring models more data to work with.

If your issue is a high credit utilization ratio, you need extra available credit to bring the ratio down. Here, pick a tradeline with the highest limit you can afford, even if it’s slightly younger. A $50,000 limit card that’s five years old will drop your utilization ratio more than a $5,000 limit card that’s 15 years old.

If your account age is fine but you have limited account variety, adding one AU credit card won’t do much. Credit mix is only 10% of your FICO Score, and adding another revolving account doesn’t add variety.

If you have recent late payments or a collection, no AU tradeline will erase those. Negative marks stay on your report for up to seven years. The AU account might soften the overall picture, but the negative items keep dragging.

Here’s a quick match-up:

| Your Weak Spot | Best Tradeline Type | Why It Works |

|---|---|---|

| Thin file, no history | Old card (10+ years), any limit | Adds length of credit history |

| High utilization | High-limit card ($20K+), low balance | Adds available credit to lower ratio |

| No revolving credit at all | Any seasoned card | Adds a revolving account to your mix |

| Recent late payments | None will fully fix this | Only time and on-time payments help |

| Just built score under 620 | Old, high-limit, low-utilization card | Hits multiple factors at once |

Pick one weakness. Solve for that. Don’t try to buy your way past every flaw with one purchase.

Realistic Score Boost Expectations

Broker websites love to promise 100-point jumps in 30 days. Real results are usually smaller and more mixed. Score movement depends on where you’re starting from and which scoring model the lender pulls.

A thin file jumping from “no score” to a 680 is realistic when a strong seasoned tradeline posts. So is a 40 to 80 point move from the mid-500s into the 600s when the AU card is high-limit and very old.

A 100+ point jump from an already-established mid-600s file is uncommon. If you already have five open accounts, one added AU card gets averaged into a much bigger pool of data, and the impact is diluted.

Some files see almost no change. This occurs if the issuer fails to report AU accounts to all three bureaus. It can also happen when the buyer’s report has many aged accounts or when the lender uses a scoring model that blocks piggybacking activity.

⚠️ Mistake to Avoid: Don’t count on a specific score number. Brokers who “guarantee” a 100-point boost usually build wiggle-room into their terms so they never have to refund. Judge results by whether you cross a lender’s threshold, not by a promised number.

The takeaway: expect a range, not a fixed number. If a broker guarantees an exact score, treat that as a warning sign, not a selling point.

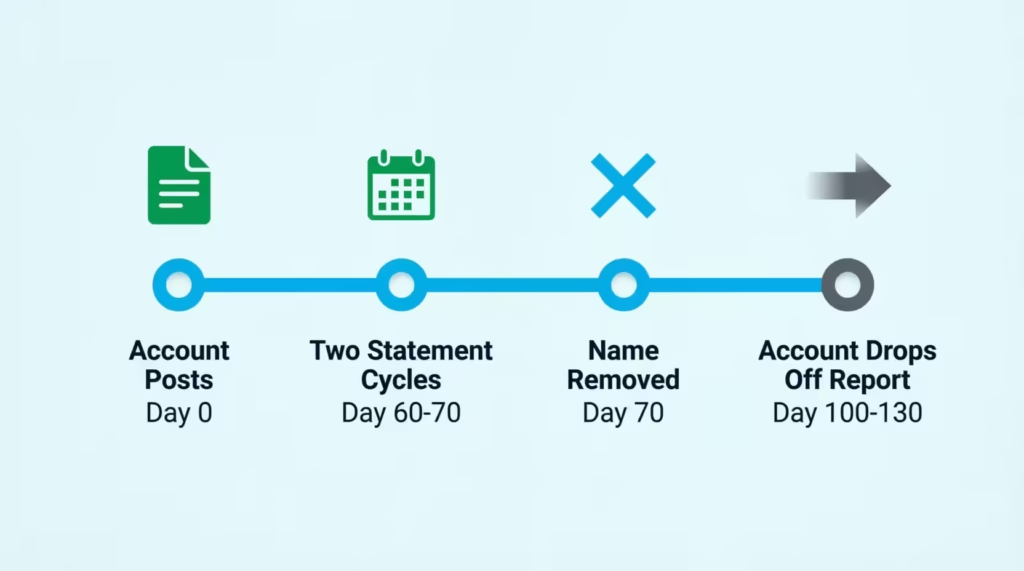

How Long the Boost Lasts After You’re Removed

Most paid tradelines are set to keep you on the account for two full statement cycles. That’s typically 60 to 70 days from the posting date. After that, the primary holder or the broker removes your name.

Once you’re removed, the account keeps showing on your credit report for one or two more reporting cycles, usually another 30 to 60 days. Then it drops off.

When the account drops, everything it added drops with it. Your average account age falls back down. Your available credit shrinks. Your utilization ratio can jump if the AU card was carrying most of your limit.

This decay pattern is why timing matters so much. If you’re buying a tradeline for a mortgage, make sure the account is posted before the lender checks your credit. It should still be visible when they check again at closing. Cutting it too close means the tradeline might vanish before the loan funds. Adding it too early means it might drop off before you even apply.

Plan on a working window of about 45 to 60 days from the day the account first posts. Anything you need done needs to happen inside that window.

Is Buying a Tradeline Legal?

The direct answer: buying an authorized user spot is not illegal for the buyer under federal law. No U.S. statute makes it a crime to be added as an AU or to pay someone for that privilege.

The Equal Credit Opportunity Act (ECOA) actually requires lenders to consider authorized user account data when it’s on a consumer’s credit report. That rule protects spouses, especially those who don’t earn money. It stops them from losing access to credit just because the account is under their partner’s name. FICO and VantageScore keep AU accounts in their models partly because of ECOA.

The problem starts when you use a purchased tradeline to lie on a loan application. Loan applications ask you to certify that your financial information is accurate and complete. If a lender asks about the AU account and you say it’s a personal relationship when it’s not, that misstatement could lead to loan application fraud.

Regulators have taken action against tradeline brokers and credit repair companies that market piggybacking as a fix for bad credit. The FTC blogged in 2020 that piggybacking isn’t the answer for consumers with damaged credit, and the settlement in that case blocked the defendants from marketing tradelines as a credit repair product. The CFPB has also flagged piggybacking-focused credit repair schemes in enforcement actions.

So the layered answer is: the act of being added as an AU is legal. Paying for it exists in a gray area. Using the resulting score to mislead a lender is where legal risk gets serious.

The Mortgage and Loan Application Risk

Mortgages are the highest-risk place to use a paid tradeline. Underwriters closely examine credit files. They re-check reports near closing and compare accounts with your listed relationships.

Fannie Mae underwriting rules specifically address authorized user accounts. Per the Fannie Mae Selling Guide on Authorized Users of Credit, lenders must evaluate AU accounts and can require the borrower to prove the account belongs to a spouse, or that the borrower has been making the payments themselves. If neither is true, the underwriter can discount that account from the credit analysis.

That means the score bump from a purchased tradeline can vanish at the underwriting stage. The lender checks your report. They spot the AU account and ask you to prove your relationship. If you can’t, they might adjust your qualifying score without it. You could get denied even after the tradeline pushed you above their score cutoff.

There’s a heavier risk too. Federal bank fraud statute language (18 U.S.C. § 1344) makes it a crime to knowingly make false statements to a federally insured lender to get credit. If an underwriter asks whether the AU account is a family account and you say yes when it isn’t, that answer could be treated as a material misstatement.

For someone with a thin credit file trying to qualify for a mortgage, the honest path is different.

Ask your mortgage broker about a few things:

- Does the lender accept non-traditional credit?

- Can a manual underwrite be done?

- Would an FHA program with lower score thresholds work?

Those options don’t put you at risk of a fraud finding.

Auto loans and credit cards face less scrutiny than mortgages. Still, the same fraud rules apply to all credit applications. If you’re going to use a purchased tradeline for a loan, be prepared to answer honestly about it.

How to Spot a Tradeline Scam

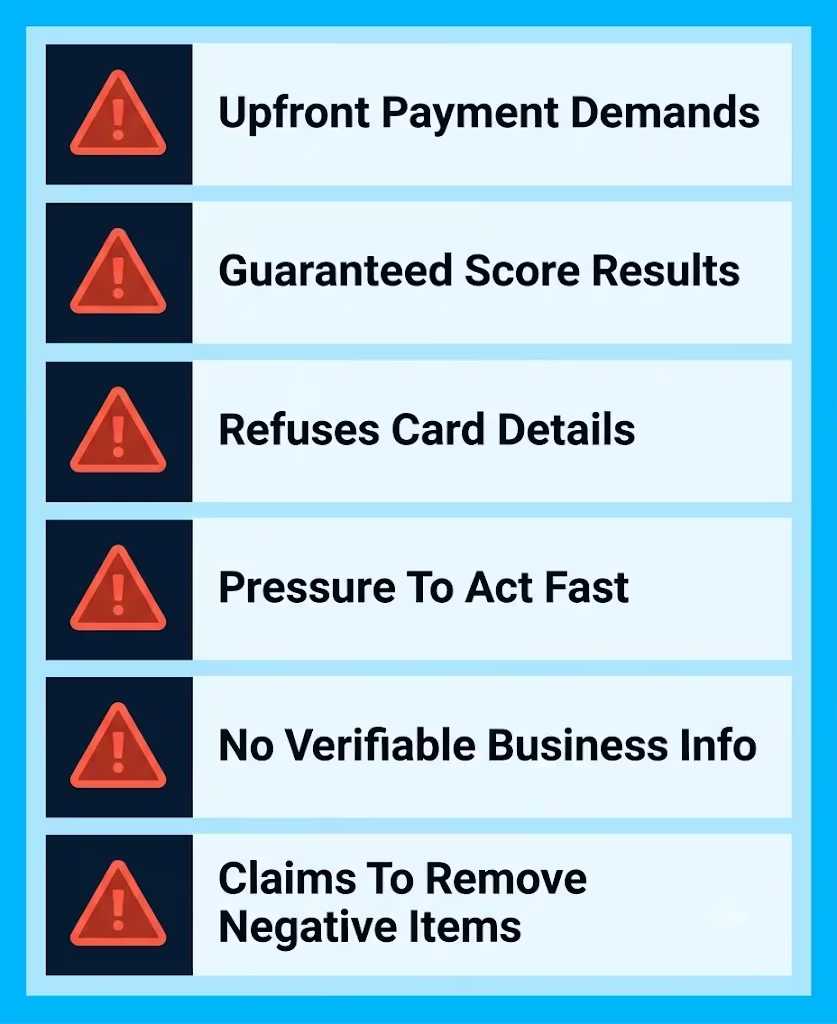

Not every tradeline broker is a scam, but the industry attracts a lot of bad actors. The FTC’s consumer advice on credit repair scams points out common red flags. Watch for these patterns.

Upfront payment demands with no service delivered. Under the Credit Repair Organizations Act, credit repair companies can’t legally charge before services are completed. Tradeline brokers may set fees based on this rule. If a company asks for a big payment upfront with no clear delivery date, be cautious.

Guaranteed score results. No one can guarantee an exact score bump. Too many variables move at the same time. A “150 points or your money back” pitch is a marketing hook, not a real guarantee. Read the terms, and you’ll usually find escape clauses.

Refusal to give the specific card details before payment. Legitimate brokers will share the age, limit, utilization, and issuer of the tradeline you’re buying. They should provide this info before the account posts. If they refuse, you can’t verify what you’re buying.

Pressure to act fast. “Only three slots left” or “price goes up tomorrow” is a classic pressure tactic. Real tradeline inventory refreshes regularly.

No verifiable business address, phone, or reviews. A broker who only communicates through Telegram, WhatsApp, or a burner Gmail is much harder to hold accountable if things go wrong.

Claims that they can remove negative items or add fake tradelines. Adding a fabricated account to your report is straight-up fraud. Anyone selling that service is putting you at legal risk too.

Vetting a Tradeline Company Before You Pay

Before sending money to any tradeline broker or credit repair company, run through this checklist.

Ask for a screenshot of the specific tradeline. You want to see the account age, credit limit, utilization percentage, and payment history. A real broker will share this. A scam won’t.

Confirm which bureaus the issuer reports to. Some card issuers only report AU accounts to one or two of the three bureaus. If your lender pulls the bureau that doesn’t get the report, the tradeline won’t help.

Check the posting guarantee. A legitimate seller will guarantee the account posts to your report within 15 to 30 days or refund the fee. Get that in writing before paying.

Read the refund policy carefully. Look for wording that lets them keep your money if the account “posts” even when your score doesn’t move. That’s a bait-and-switch clause.

Search for the company name plus “scam” or “complaint.” Look at the Better Business Bureau, Reddit’s credit-focused subreddits, and Trustpilot. A company with dozens of complaints about non-posting or no refunds is not worth the risk.

Confirm they’ll provide bureau proof of posting. After the AU account posts, you should be able to see it on your credit reports at Experian, Equifax, and TransUnion. Ask how the broker will help you confirm this.

Check their communication style. Slow replies, refusal to answer direct questions, or pushing you toward a phone call to close the sale are all warning signs.

What Tradelines Typically Cost

Prices for a seasoned tradeline vary widely based on age, credit limit, and reporting reliability. As of 2026, most brokers price by tier.

Entry-level tradelines: $200 to $400. These are usually cards that are 3 to 6 years old with $5,000 to $10,000 limits. Good for a thin file that just needs some data.

Mid-tier tradelines: $500 to $1,000. Cards aged 7 to 12 years, limits $15,000 to $30,000. This is the most common range for people trying to hit a specific mortgage or auto loan cutoff.

Premium tradelines: $1,200 to $2,500+. Cards aged 15+ years, limits $50,000 or higher. These target big score jumps or high-stakes applications.

A tradeline broker takes a cut, often 40% to 60% of the fee. The primary account holder gets the rest. This split explains why cheap tradelines are often the weakest ones. The broker has overhead costs, so a $200 tradeline often means little goes to the primary. Primaries who accept that price usually have less desirable accounts.

Payment is usually required upfront or held in escrow until posting. Watch for:

- Extra “rush” or “expedite” fees

- Charges per bureau instead of a flat rate

- Auto-renewal for a second posting cycle

- Cancellation fees

Compare total cost to the value you’ll actually get. If you’re buying a $1,500 tradeline to qualify for a mortgage that will save you $8,000 over the loan, that math might work. If you’re spending $1,500 for a credit card approval you could get by opening a $200 secured card and waiting 12 months, the math doesn’t.

💡 Pro Tip: Never pay more than the value of the outcome. A $2,000 tradeline for a car loan that saves you $600 in interest is a losing trade. Do the math before you buy.

Free and Low-Cost Alternatives to Buying a Tradeline

Most people looking at paid tradelines don’t need them. Cheaper, safer options usually work just as well over a few months. If your loan isn’t for 60+ days out, start here first.

Ask a family member to add you as an authorized user. This is the original, legal, free form of credit piggybacking. A parent, spouse, sibling, or close friend with an old, low-utilization card can add you in minutes. The card doesn’t have to be given to you. Their account history flows to your report the same way a paid AU tradeline would, but with zero cost and no fraud risk. This is often the single best move for a thin credit file.

Open a secured credit card. A secured credit card requires a refundable deposit, usually $200 to $500, and gives you a real credit line in your own name. On-time payments report to all three bureaus. After 6 to 12 months, many issuers convert the card to unsecured and refund the deposit. Discover it Secured, Capital One Platinum Secured, and Chase’s secured products are widely used starter options.

Take out a credit builder loan. A credit builder loan works backwards. The lender puts a small amount (often $500 to $1,500) into a locked savings account. You make monthly payments for 12 to 24 months. Each payment reports to the bureaus. At the end, the money is released to you. Self, Kikoff, and many credit unions offer these. Payment history is 35% of your score, so 12 clean payments here can move a thin file meaningfully.

Report your rent and utility payments. Services like Experian Boost, Rental Kharma, and RentReporters can add positive rent and utility history to your credit reports. Experian Boost is free and can add years of on-time utility, phone, and streaming payments in minutes.

Pay down credit card balances aggressively. If you have high utilization on your cards, try paying down your balances. Keeping them below 10% of the limit before your statement closes can raise your score by 20 to 50 points in just one cycle. This costs nothing beyond the debt you already owe.

Dispute credit report errors. Around 1 in 5 credit reports contain an error, according to CFPB complaint data. Pulling all three reports at AnnualCreditReport.com and disputing anything inaccurate is free and can produce a real score bump within 30 to 45 days.

Any two or three of these, done together, usually beat a paid tradeline over 6 months. And none of them expose you to loan application questions.

Who Should Avoid Buying Tradelines Entirely

Some readers should skip paid tradelines completely. The risk is bigger than the benefit for these groups.

Mortgage applicants are at the top of the list. Fannie Mae, Freddie Mac, and FHA underwriters often question AU accounts. A misstatement during closing can ruin the loan. It can also expose you to fraud claims. If a mortgage is your goal, focus on legitimate options and give yourself more time.

Anyone dealing with a seller who won’t share account details. If the broker won’t tell you which card, which issuer, and which limit before you pay, you’re buying nothing you can verify.

People with plenty of open accounts already. If your report already shows five or more open lines with good history, an added AU account gets diluted. Fix utilization or dispute errors instead.

Consumers actively in a debt-settlement or bankruptcy process. A short-term score bump won’t undo the negative items on your file, and the money is better spent settling accounts.

Anyone who can’t afford to lose the fee. Tradelines that fail to post do happen. Refunds are inconsistent. If losing $800 would hurt you, don’t spend it on something with this much uncertainty.

How to Buy and Add a Tradeline Step by Step

If none of the alternatives work for your timeline and you’ve decided to move forward with a paid tradeline, follow this process to reduce risk.

Step 1: Pull all three credit reports. Get free reports at AnnualCreditReport.com. Note your current score on each bureau and identify your weakest factor. This tells you what kind of tradeline to shop for.

Step 2: Set a specific target. Write down the score you need and the deadline you need it by. “670 by March 15 for auto loan pre-approval” is useful. “Higher score, soon” is not.

Step 3: Research brokers. Look for companies with at least 3 years in business, verifiable reviews across multiple sites, a real phone number, and a physical address. Compare pricing at three to five brokers before choosing.

Step 4: Ask for tradeline details in writing. Before paying, request the card’s age, credit limit, current utilization, issuer, and which bureaus it reports to. Get the posting guarantee terms in writing too.

Step 5: Confirm the timing matches your deadline. Most tradeline broker postings happen on the primary account’s statement date. Ask when that date falls this month and next month. Buying too close to your deadline is a common mistake.

Step 6: Pay through a traceable method. Use a credit card or a payment platform that offers dispute protection. Never send Zelle, Cash App, cryptocurrency, or a wire transfer to a broker you haven’t verified. If the tradeline fails to post, you’ll need the ability to dispute the charge.

Step 7: Watch your credit reports weekly. The AU account should post within 15 to 30 days. Use a free monitoring service like Credit Karma or the Experian app to track when the account shows up.

Step 8: Pull your score after posting. Check your FICO 8 score after the account has posted for at least one full billing cycle. If your score didn’t move as expected, contact the broker for support before the removal date.

Step 9: Plan the removal timing. Confirm when your name will be removed from the account. If you have a loan closing after removal, understand that the account may drop from your report and your score may fall.

Step 10: Save all documentation. Keep every email, receipt, and screenshot. If a lender asks about the AU account, you need to be able to explain the relationship truthfully.

Done this way, a paid tradeline is still a risk, but it’s a managed risk instead of a blind purchase.

Frequently Asked Questions

Are tradelines legal?

Being added as an authorized user is legal. Under federal law, the Equal Credit Opportunity Act says lenders must consider AU account data. Paying a broker to be added exists in a legal gray area. Using the resulting score to misrepresent your finances on a loan application can cross into fraud.

How much do tradelines cost?

Prices in 2026 range from about $200 for entry-level accounts to $2,500 or more for premium seasoned tradelines. Most people looking for a meaningful score bump end up paying $500 to $1,200 for a mid-tier account.

How long does a tradeline boost last?

The account usually stays on your report for two statement cycles, roughly 60 to 70 days from posting. After removal, the account can linger for another 30 to 60 days before dropping off. Any score gain from the tradeline fades once the account is gone.

Do tradelines work for mortgage approval?

Sometimes, but mortgage underwriters scrutinize AU accounts closely and can require proof of relationship. Fannie Mae guidelines specifically allow lenders to discount AU accounts that appear unrelated to the borrower. Relying on a paid tradeline for a mortgage is one of the riskiest uses.

How do I know if a tradeline company is legit?

Check for a real business address, verifiable customer reviews across multiple platforms, at least 3 years in business, willingness to share card details before payment, clear refund terms, and a posting guarantee in writing. Avoid any broker who pushes for crypto payments, refuses to share account information, or promises exact score gains.

Will buying a tradeline hurt my credit?

Directly, no. Being added as an AU can’t add negative items to your report unless the primary account holder misses a payment. Indirectly, yes. If the tradeline leads you to a loan you can’t afford, or if a lender spots the AU account during review, the consequences can be worse than not buying it at all.

What’s the difference between an authorized user and a purchased tradeline?

A traditional authorized user is a real family member or trusted contact added to a card without payment. A purchased tradeline is a paid arrangement, usually through a broker, where you rent AU status on a stranger’s account for 60 to 70 days. The mechanics on your credit report are the same, but the intent and legal risk are different.

Bottom Line

To get the best and safest score boost, match the tradeline to your specific weakness. Verify the seller carefully. Also, use free alternatives first whenever you can. For many readers, the best step is to ask a family member for authorized user access on an old, low-use card. Pair that with a secured card and a credit builder loan.

Paid tradelines are only worth the risk if you’re short on time and have no other options to meet your deadline.

If you know someone stressing over a mortgage or auto loan score cutoff, share this guide with them.