Getting a “sent to collections” letter about a small toll can feel scary. Maybe you tossed an E-ZPass invoice, moved states, or a rental car racked up charges you never saw. Now you’re worried the whole thing will hurt your credit before you can even sort it out. The confusion around unpaid tolls and credit score damage is real, because the process is not what most people think.

Here’s the quick answer: An unpaid E-ZPass toll won’t hurt your credit by itself. But if the debt goes to a collector who reports it, your score may drop.

Here’s a quick guide on how it happens, how to find it on your report, what damage to expect, and the steps to fix it and prevent it from returning.

Key Takeaways

This guide explains whether EZ Pass collections affect your credit score, including how the referral process works, credit score impact factors, dispute rights, and resolution options for an existing collection account.

Core Facts:

- An unpaid toll does not directly affect your credit score because toll authorities are government agencies that do not report to Experian, Equifax, or TransUnion.

- A credit score impact only occurs if the toll debt is referred to a third-party collection agency, which does report to the credit bureaus.

- Referral to collections typically happens 30 to 90 days after the last unpaid notice, though this varies by state and toll system.

- Under the Fair Credit Reporting Act, a collection account can remain on a credit report for up to seven years from the date of the original delinquency, even after it is paid.

- Newer scoring models treat paid collections more favorably: VantageScore 4.0 ignores paid collection accounts entirely, and FICO 9 and FICO 10 reduce their impact.

- Credit consequences and vehicle registration suspensions are separate issues; paying a collection agency does not automatically lift a DMV registration hold from the toll authority.

Best for:

- Drivers who noticed an unfamiliar collection account on their credit report and want to determine if it originated from an unpaid toll.

- Anyone who received a toll violation notice and wants to understand when and how it could turn into a credit issue.

- Readers trying to resolve an existing toll-related collection account through payment, settlement, or dispute.

How an Unpaid E-ZPass Toll Actually Turns Into a Credit Problem

An unpaid toll by itself does not sit on your credit file. Toll authorities, like the New Jersey Turnpike Authority or the PA Turnpike Commission, are government agencies. They do not send data to Experian, Equifax, or TransUnion. What they do send is a toll violation notice, then reminders, then late fees. If you keep ignoring those bills, the account gets sold or assigned to a third-party collection agency. That collector can report the debt to the credit bureaus, and that is the moment your credit score is at risk.

So the trigger isn’t the toll. The trigger is the referral. Think of it as a two-step process. Step one is the toll authority trying to collect on its own. Step two is the outside agency taking over. Only step two touches your credit file.

Some drivers pay a small toll fine and notice no impact on their score. But others may be surprised months later by a strange collection account on their report. The difference is whether the account was passed to a collector who reports.

📌 Did You Know: A single unpaid $2 toll can grow into hundreds of dollars once administrative fees, late penalties, and collection fees pile on. In many E-ZPass bankruptcy cases, collection costs and fees make up more than 90% of the total debt owed.

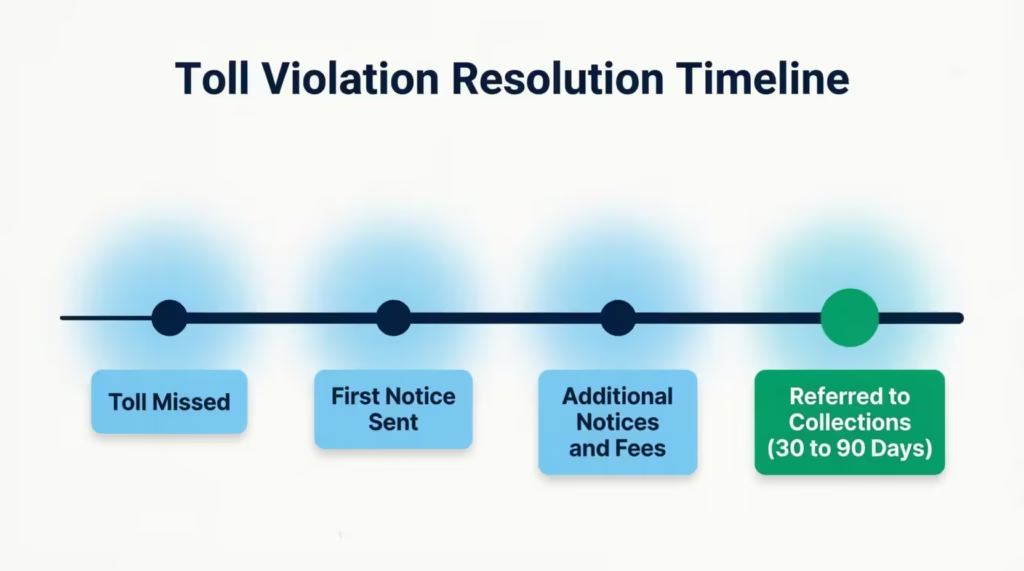

How Long It Takes Before a Toll Goes to Collections

There is no fixed national timeline. It depends on the state, the toll system, and the account status. Most drivers see the first invoice or violation notice within a few weeks of the missed toll. If it stays unpaid, more notices follow, each with added fees. The referral to a collector usually happens somewhere between 30 and 90 days after the last unpaid notice, though it can stretch longer.

For example, the Pennsylvania Turnpike notes that unpaid invoices become eligible for further collection action once they sit past 60 days, according to the PA Turnpike. Other agencies follow similar patterns but with their own dates.

The key point: you almost always get several written warnings before it hits collections. If you act during that window, you can settle the toll directly with the authority and avoid the credit risk entirely.

Does This Vary by State or Toll System?

Yes, and this trips up a lot of drivers. E-ZPass is not one company. It’s a network of separate state agencies that share the same transponder technology. New Jersey, New York, Pennsylvania, Massachusetts, Virginia, and other states each run their own billing and collections process. Timelines, late fees, and even the collection agencies they hire are different.

If you drive through multiple states, you can end up with several unrelated toll debts in different systems. Someone who lives in New Jersey but rents a car in Florida may get a bill from SunPass, not E-ZPass, and never realize it. Each system has its own path to collections, so one missed toll in one state does not warn you about another.

Why the Toll Authority Itself Doesn’t Report to Credit Bureaus

Credit bureau reporting works through a system of “data furnishers.” These include lenders, credit card issuers, and collection agencies. They have agreements with Experian, Equifax, and TransUnion to share account information. Toll authorities are not set up that way. They’re government entities focused on running roads, not on furnishing consumer credit data. They don’t have the reporting relationships, and it isn’t part of their job.

That’s why the toll itself never shows up as a line item on your credit report. What can show up is the collection account created after the debt is handed off. The collector, unlike the toll authority, is a private business that does report to bureaus. When they add the account, that’s when your credit gets touched.

Understanding this split matters because it tells you where to focus. Fighting the toll authority won’t remove a credit entry. The credit entry belongs to the third-party collection agency, and that’s who you deal with for anything credit-related.

How to Tell If a Collections Entry on Your Report Is From an EZ Pass Toll

This is one of the most confusing parts. The EZ Pass collections credit report entry rarely says “E-ZPass.” Instead, you see a random company name, something like “Credit Collection Services,” “Transworld Systems,” or “Linebarger.” Drivers see this and panic, thinking someone stole their identity, when the truth is a $6 toll from last summer grew legs.

Start by pulling your free reports from all three bureaus at AnnualCreditReport.com. This is the only federally authorized site for free reports, and it doesn’t require a credit card. Look for any collection account you don’t recognize. Note the collector’s name, the balance, the “original creditor” field if listed, and the date opened.

Next, match the timing. Did you drive on a toll road roughly six to eighteen months before that date opened? Did you rent a car, move, or change your address around that time? Do the account balances look small, like $50 to a few hundred dollars? These are all signals it may be toll-related.

The most reliable way to confirm is to send a debt validation letter to the collector. Once they respond, the paperwork will name the original creditor, which is usually the toll authority. That’s your confirmation.

What to Do the Moment You Spot It

Move fast, but don’t panic-pay. First, do not call the collector and admit the debt is yours before you have proof. Second, save every letter, envelope, and voicemail. Third, send that validation letter in writing within 30 days of first contact from the collector. This locks in your rights and forces the collector to prove the debt is valid, that they own it, and that the amount is correct.

💡 Pro Tip: Send the validation letter by certified mail with a return receipt. It gives you a legal paper trail if the collector later claims they never got your request. A $5 tracking number can save you from a $400 dispute headache.

How Much Can a Toll Collection Lower Your Credit Score?

Nobody can promise you an exact number, and any article that gives you a clean “50 to 100 points” figure is guessing. Your credit score drop depends on where you started, what else is on your report, and which scoring model your lender uses. That said, there are useful patterns.

If your credit is strong (say, 780+) with no other negatives, a new collection account can hit harder in raw points because you have more to lose. If your credit already has late payments or other collections, a small toll debt adds less on top. Recency matters more than dollar amount. A fresh collection from last month drags scores down more than a two-year-old one, even if the balances are identical.

Newer scoring versions treat small collections more gently. FICO Score 9 ignores paid collections and reduces the impact of unpaid medical collections, according to myFICO. VantageScore 4.0 goes further and does not count paid collection accounts at all, Equifax reports.

So a $60 toll collection you pay off may barely register on VantageScore 4.0, while older FICO models used by some auto lenders may still ding you. That’s why one lender pulls a “no problem” score and another flags the same file.

Do Newer Credit Scoring Models Ignore Paid Collections?

Yes, but with limits. VantageScore 4.0 ignores paid collection accounts entirely. FICO 9 ignores paid collections and softens the impact of unpaid medical ones. FICO 10 continues that pattern.

The catch is that many lenders still use older models like FICO 8, or even older versions for mortgage underwriting. So the same paid toll collection can be invisible on one score pull and visible on another. If a lender uses an older model, a paid collection can still cost you points until it ages off your report.

Does Paying Off an EZ Pass Collection Remove It From Your Credit Report?

Short answer: no, not automatically. This is the most common misconception drivers have. Paying the debt changes the account status from “unpaid” to “paid” or “settled,” but the entry stays on your report. That surprises a lot of people who expected the line to vanish the day their check cleared.

Under the Fair Credit Reporting Act, negative items like collections can stay on your credit file for up to seven years. This time starts from the date of the original delinquency, according to the CFPB. Paying it doesn’t reset that clock, and it doesn’t erase the entry. A paid collection simply looks better than an unpaid one to lenders reading the report.

There’s still a real benefit. As covered above, newer scoring models treat paid collections much more kindly, sometimes ignoring them completely. And when a human underwriter reads your file, “paid in full” looks a lot better than an open, unpaid account. So paying helps, even if it doesn’t delete.

How Long Does a Toll Collection Stay on Your Report?

Up to seven years from the date of first delinquency on the original toll account. That is the seven-year reporting window set by the FCRA. The date of first delinquency is not when the collector took the account. It’s when you first missed the underlying obligation.

So if you missed a toll payment in March 2024, the maximum reporting date runs to about March 2031, even if the collector didn’t add it to your report until 2025. Once the seven years are up, the collection must come off. If it doesn’t, you can file a dispute with each bureau to have it removed.

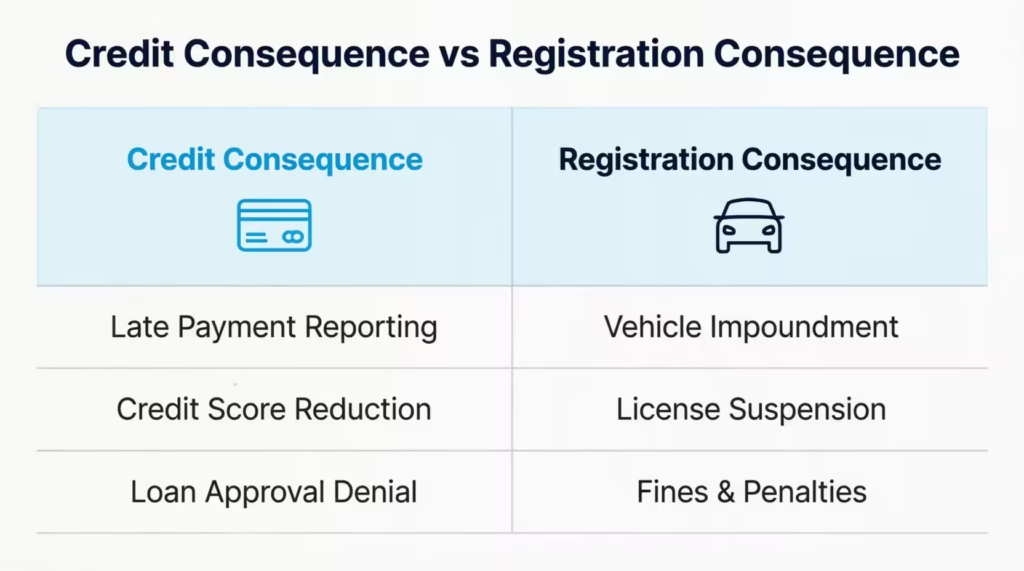

Credit Score Impact vs. Registration and License Consequences: Don’t Confuse Them

This trips up so many drivers that it deserves its own section. Unpaid toll debt can create two totally separate problems:

The credit consequence, which we’ve covered, happens only if a collector reports the debt. It affects your credit score and any loan, credit card, or apartment application that checks your report.

The registration suspension consequence is completely different. It’s a toll authority and DMV matter, not a credit matter. If you owe enough unpaid tolls, some state DMVs will hold your vehicle registration or block your renewal.

New York is a well-known example. The NY DMV can suspend your registration for failing to pay tolls related to three or more violations, or when the balance hits $200 or more within five years, according to the New York DMV. Other states have their own thresholds.

Here’s the crucial part: fixing one does not fix the other. Paying the toll authority to lift a registration hold does not remove a collection account already reported by a third party. Clearing a debt with a collector doesn’t lift a DMV registration hold. If the toll authority still has an open balance, the hold remains.

You may need to resolve both sides separately. That means calling the toll authority to clear the DMV side and dealing with the collection agency to address the credit side. Skipping one leaves you with a lingering issue.

⚠️ Mistake to Avoid: Paying only the collection agency and assuming the DMV will lift a registration hold. In many states, the toll authority still shows the account as unpaid on its own system and won’t release the hold until it gets paid too.

Your Rights When an EZ Pass Debt Goes to Collections

Once a debt collector contacts you, federal law gives you specific rights. Knowing them changes the balance of the conversation.

Under CFPB Regulation F, collectors must send you a written validation notice with details about the debt, including the creditor, the amount, and your rights, per the CFPB. You then have a 30-day validation window to dispute the debt in writing or request verification.

Send a debt validation letter during that window. In it, ask for:

- The name of the original creditor (the toll authority)

- The total amount owed, broken down between the original toll and any added fees

- Proof that the collector has legal authority to collect this debt

- The date of the original charge

If the collector cannot verify the debt, they must stop collection activity and cannot report the account to the bureaus. This is one of the strongest protections you have.

The FDCPA also blocks abusive tactics. Collectors can’t call before 8 a.m. or after 9 p.m. They also can’t contact you at work if you ask them not to. They must not threaten legal action unless they mean it. Lastly, they cannot lie about the debt’s amount or nature. If a collector breaks these rules, save every call log and message. You may have a claim.

How to Dispute an Inaccurate Toll Collection

You can dispute a credit report with all three bureaus if:

- The debt isn’t yours.

- The amount is wrong.

- The dates don’t match.

- The collector didn’t validate it.

Steps to dispute:

- Gather your evidence.

- Bank statements showing your payments.

- Proof that you didn’t own the car.

- Rental agreements with another driver.

- Your original toll transponder statements.

- File the dispute online with Experian, Equifax, and TransUnion. Each has its own dispute portal.

- Include copies (never originals) of your evidence and a short written explanation.

- The bureau must investigate within 30 days and get back to you with results.

- If they can’t verify the account, they must remove it.

You can also dispute directly with the collector. In writing is always better than by phone.

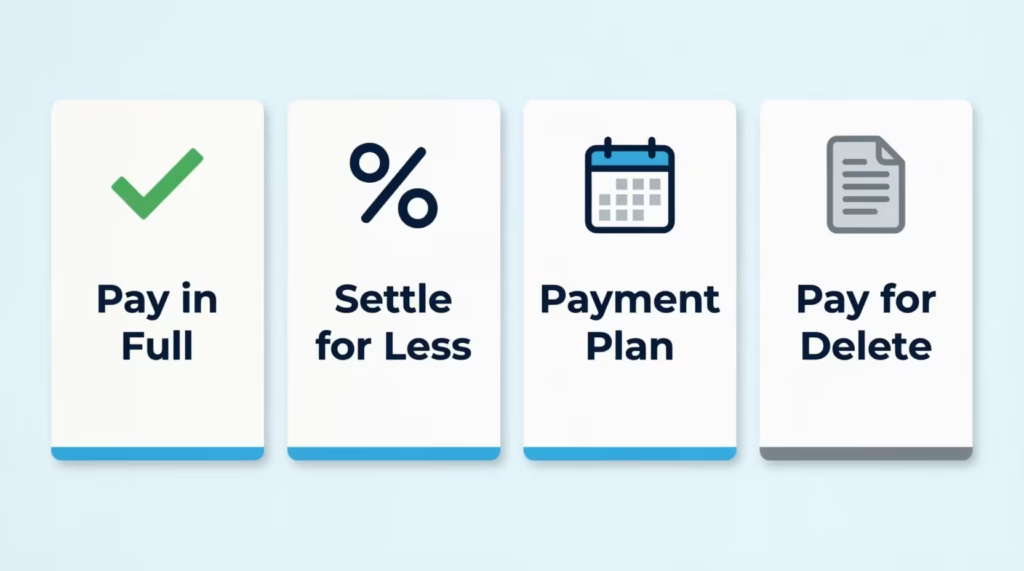

How to Resolve an EZ Pass Collection Once You’ve Confirmed It’s Valid

If the debt is real and yours, focus on the cleanest resolution. Do not just pay the full amount blindly. You have a few options:

Option 1: Pay in full. Simple and closes the matter. The account gets marked “paid” but stays on your report. On VantageScore 4.0 and FICO 9/10, a paid collection can lose most of its impact.

Option 2: Settle for less. Many collectors will accept a lump-sum payment for 40% to 70% of the balance, especially for older accounts. Ask in writing. Never give a debit card over the phone before you have the settlement terms in writing.

Option 3: Negotiate a payment plan if you can’t pay a lump sum. Get every term in writing, including start and end dates and the final “paid” status they’ll report.

Option 4: Attempt pay for delete. This is where you offer to pay in exchange for the collector removing the account from your credit report. Some collectors agree, many refuse, and most large collectors have policies against it. Ask, but don’t count on it. If they agree, get it in writing before you send a single dollar.

After any of these, monitor all three credit reports for 60 to 90 days to make sure the account updates correctly. If a collector said they would delete or mark it paid but didn’t, use the credit report dispute process. Your written agreement can serve as proof.

Meanwhile, do not lose sleep over old advice about “waiting it out.” Ignoring the debt won’t make it vanish from your report for seven years. During this time, an unpaid collection damages your score more than a paid or settled one.

How to Avoid Future EZ Pass Collections and Protect Your Credit Going Forward

The best win is not needing this article next year. A few practical habits can keep small toll issues from ever becoming a credit hit.

First, keep your E-ZPass account current. Log in every few months and verify your registered license plate, mailing address, email, and credit card on file. Most drivers who end up in collections had an expired card, a moved address, or a new plate they never updated.

Second, turn on auto-replenish. This lets the account pull funds from your card or bank automatically when your balance is low. So, you won’t run out of money on a Sunday drive or rack up unpaid toll invoices.

Third, watch your linked email. Every state E-ZPass system sends bill notices and low-balance warnings by email first. If those go to an old inbox or a spam folder, you’ll never see the toll violation notice until fees have already piled up.

Fourth, if you drive across multiple states, keep a note of which toll systems you use. Some regions use SunPass, FasTrak, or Peach Pass. E-ZPass works on many roads, but not all, and cross-system billing can generate unexpected mail.

Fifth, check your credit report at least once every four months, rotating between the three bureaus at AnnualCreditReport.com so you get free coverage year-round. If a strange collection appears, catching it early gives you the best shot at removing or minimizing it before it drags your score down for months.

Finally, if you sell a car, transfer the plate, or move, close or update your toll accounts the same day. A single unpaid $3 toll on a car you no longer own can turn into a $200 collection two years later. A quick five-minute update prevents it.

Frequently Asked Questions (FAQs)

Does E-ZPass report to credit bureaus?

No, the toll authority itself does not report to Experian, Equifax, or TransUnion. Only a third-party collection agency that the debt gets referred to can report it.

How long does it take for an unpaid EZ Pass toll to go to collections?

There’s no fixed nationwide timeline. It varies by state and toll authority. Escalation usually occurs after several ignored notices, often within 30 to 90 days, but this can change.

Will paying off an EZ Pass collection remove it from my credit report?

No. Paying changes the account status to “paid” or “settled.” This is better than leaving it unpaid. However, the entry remains on your report; it won’t be deleted just because it’s resolved.

How long does an EZ Pass collection stay on your credit report?

Up to seven years from the date of the original delinquency (not from when you pay it), under the Fair Credit Reporting Act.

How many points does a toll collection take off your credit score?

There’s no set number. The impact depends on how recent the collection is, your current credit profile, and which scoring model the lender uses. Newer FICO and VantageScore versions sometimes ignore paid or smaller collections altogether.

Why doesn’t my credit report show “E-ZPass” for a toll collection?

Collections entries typically show the agency’s name instead of the original toll authority. So, the debt type often appears as just “collection,” lacking a clear toll reference. This is why many people don’t recognize it right away.

Can unpaid tolls affect my credit score even if I never got a notice?

It’s unlikely to hurt your credit at that point. The credit risk begins only when a collections agency gets involved, not from the toll or the first violation notice alone.

Is an unpaid toll the same as a suspended registration for credit purposes?

No. A registration suspension is a DMV action linked to the toll authority and state law. It won’t impact your credit report. Fixing one issue doesn’t mean the other is resolved.

Can I dispute an EZ Pass collection on my credit report?

Yes. If you think the entry is wrong, you can ask the collector for debt validation. You can also file a dispute with the credit bureau reporting it.

Can I negotiate an EZ Pass collection instead of paying the full amount?

Yes, collectors often agree to payment plans or reduced settlements for those facing financial hardship. However, a full “pay-for-delete” (removal for payment) isn’t guaranteed. It depends on the specific agency.

Bottom Line

Unpaid tolls don’t hit your credit directly, but the collection referral that follows can. The real risk happens when a third-party collector reports the debt to Experian, Equifax, or TransUnion. Also, even a paid collection can stay on your record for seven years due to the FCRA rule.

The best way is to first validate the debt. If you find anything wrong, dispute it. Then, pay or settle in writing. Newer scoring models, like VantageScore 4.0, view paid collections more favorably than older FICO scores.

Small habits, like auto-replenish and address updates, keep it from coming back. If you know someone who commutes on toll roads or rents cars often, share this so a $3 toll never becomes a credit headache.