I know how frustrating it feels when you’re standing at the checkout, ready to save money, and you start wondering if you’ll even qualify for the store’s credit card. Maybe you’ve heard mixed things about the Walmart credit card, or you’re worried a hard pull will drop your score for nothing. The rules also changed recently, so old advice you saw online may be flat-out wrong now.

Shoppers with a FICO score in the mid-600s or higher usually get approved. Those with fair or thin credit might still qualify for the store-only version.

Below, we’ll walk you through the exact score ranges, pre-qualification steps, and backup plans, so you can apply with real confidence.

Key Takeaways

This guide explains what credit score you need for a Walmart card, covering the two OnePay cards issued by Synchrony Bank, typical FICO score ranges for approval, pre-qualification steps, and what to do if declined.

Core Facts:

- Walmart’s credit card program is now issued by Synchrony Bank through OnePay, replacing the discontinued Capital One Walmart Rewards Mastercard, which was converted to a Capital One Quicksilver card.

- The OnePay CashRewards Card is an open-loop Mastercard usable anywhere Mastercard is accepted, while the OnePay Walmart Spend Card is a closed-loop card usable only at Walmart, Walmart.com, and Sam’s Club.

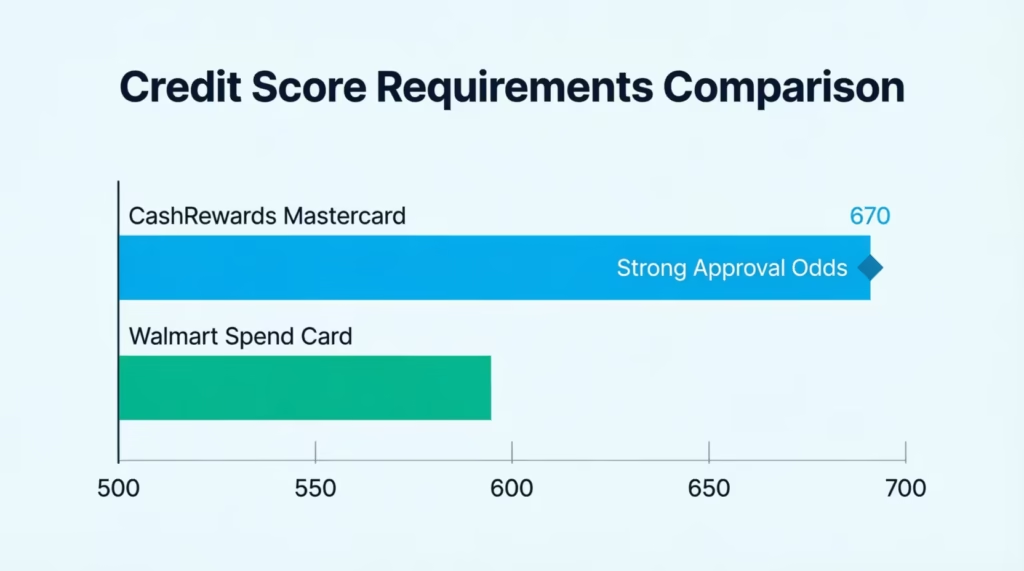

- Applicants approved for the CashRewards Mastercard typically have a FICO score between the upper 500s and mid-600s or higher, with 670+ making approval very likely.

- The Walmart Spend Card is typically approved for applicants with fair or thin credit, often in the low-to-mid 500s FICO range.

- Pre-qualification uses a soft credit inquiry that does not affect a credit score, while a formal application triggers a hard inquiry that can lower a score by 5 to 10 points.

- One application covers both cards, and Synchrony decides whether to approve the CashRewards Mastercard, offer the Spend Card as a step-down option, or decline the application entirely.

Best for:

- Shoppers deciding whether to apply for a Walmart credit card and wanting to know their approval odds before triggering a hard inquiry.

- People who previously held the discontinued Capital One Walmart card and want to understand how the new OnePay program works.

- Applicants offered the Walmart Spend Card who want to understand its role as a step toward the CashRewards Mastercard.

Walmart’s Credit Card Program Has Changed Issuers

If you searched this topic a year ago, you probably saw articles about the Capital One Walmart Rewards Mastercard. That card is gone. Capital One and Walmart ended their partnership, and existing Capital One Walmart cardholders were converted to the Capital One Quicksilver card, which earns a flat 1.5% cash back on all purchases but is no longer tied to Walmart in any special way.

In the fall of 2025, Walmart launched a brand-new credit card program through OnePay, Walmart’s own fintech company. OnePay teamed up with Synchrony Bank to issue the new cards. Synchrony is now the exclusive issuer, and the entire card experience lives inside the OnePay app.

This matters because the underwriting rules are different now. Capital One had its own approval style. Synchrony uses its own credit models, and it is well known for approving customers with fair credit. So if you were denied by Capital One in the past, your odds with the new program may be very different today.

The Two Walmart Credit Cards: CashRewards vs. Spend Card

The new program has two cards, but you only fill out one application. Synchrony decides which card fits your credit profile.

The first is the OnePay CashRewards Card. This is an open-loop Mastercard, which means you can use it anywhere Mastercard is accepted, not just at Walmart. It comes with cash back rewards on eligible purchases, no annual fee, and it works both in stores and online. This is the card most shoppers want.

The second is the OnePay Walmart Spend Card. This one is a closed-loop store card. It only works at Walmart, Walmart.com, Sam’s Club, and select Walmart-owned brands. It has no standard ongoing rewards program, and it also carries no annual fee. Synchrony often offers this card to people who don’t quite qualify for the Mastercard version yet.

You apply once. Based on your credit file, income, and other data, Synchrony either approves you for the CashRewards card, offers you the Spend Card as a step-down option, or declines the application.

| Feature | OnePay CashRewards Card | OnePay Walmart Spend Card |

|---|---|---|

| Card Type | Open-loop Mastercard | Store-only card |

| Where You Can Use It | Anywhere Mastercard is accepted | Walmart, Walmart.com, Sam’s Club |

| Rewards | Cash back on purchases | No standard rewards program |

| Annual Fee | $0 | $0 |

| Typical Credit Profile | Fair to good credit | Fair or thin credit |

| Issuer | Synchrony Bank | Synchrony Bank |

Credit Score Needed for Each Walmart Card

Here is the honest truth: neither OnePay nor Synchrony has published an official minimum score. Their help center confirms only that approval depends on your creditworthiness and that you may be offered either card or declined. So the ranges below come from cardholder reports, common Synchrony underwriting patterns, and what applicants have shared publicly.

One more note before we dive in. Synchrony pulls a FICO score during underwriting, but the score you see for free inside the OnePay app is a VantageScore 4.0. These two scoring models often show different numbers for the same person.

Your VantageScore might be 20 to 40 points off from the FICO score Synchrony actually uses. So don’t panic if your OnePay app score looks a bit different from what you see on Credit Karma or Experian.

OnePay CashRewards Card score range

Most people who get approved for the CashRewards Mastercard have a FICO score in the fair-to-good range, usually somewhere between the upper 500s and the mid-600s or higher. A score of 640 or above puts you in a strong position, and 670+ makes approval very likely if the rest of your file looks healthy.

Reddit users in the r/CreditCards community have reported approvals with starting credit limits around $1,000 for scores in this range. Some higher-score applicants report limits of $2,500 to $5,000 or more.

Keep in mind that a “good” score alone won’t guarantee approval. Your income, existing debt, and recent credit activity all matter too, which we’ll cover in the next section.

OnePay Walmart Spend Card score range

The Walmart Spend Card is the easier card to get. Synchrony typically offers this card to applicants with fair credit, thin credit files, or a few past credit issues. Approvals often happen in the low-to-mid 500s FICO range, and some applicants with limited credit history get approved as well.

If your score sits below the fair range, or if you have very little credit history, the Spend Card is often your realistic starting point. It’s not a rejection. It’s a foot in the door.

💡 Pro Tip: If Synchrony offers you the Spend Card and you accept it, using it responsibly for six to twelve months can help you qualify for the CashRewards Mastercard later. Synchrony often reviews accounts for upgrades or new card offers once you’ve built a positive payment history.

What Affects Approval Beyond Your Score

Your credit score is only one part of the picture. Synchrony looks at several other factors when deciding whether to approve you, and sometimes these can outweigh a mediocre score.

The first big factor is your debt-to-income ratio (DTI). This compares how much you owe each month to how much you earn. If your monthly debt payments eat up more than 40 to 45 percent of your income, approval gets harder even with a decent score.

The second factor is your recent payment history. Missed payments in the last 6 to 12 months are a red flag. One late payment from three years ago won’t sink your application. A 60-day late from last month usually will.

Your credit utilization also matters. This is how much of your available credit you’re currently using. If your other credit cards are maxed out, Synchrony sees you as a higher risk, even if your score is okay. Try to keep utilization on all your cards under 30%.

Recent hard inquiries hurt too. If you’ve applied for several credit cards or loans in the last six months, lenders assume you’re desperate for credit. Space out your applications.

Finally, your history with Synchrony matters. If you already have a Synchrony account in good standing, that helps. If you had a Synchrony account charged off in the past, that will very likely lead to a denial no matter what your current score looks like.

How to Check Pre-Qualification Before You Apply

The safest way to check your odds is to see if you pre-qualify first. Pre-qualification uses a soft credit inquiry, which does not affect your credit score at all. You can check as many times as you want.

To pre-qualify:

- Visit the OnePay Card page on Walmart.com or open the OnePay app.

- Look for the “See if you pre-qualify” button.

- Enter basic information such as your name, address, date of birth, income, and the last four digits of your Social Security number.

- Wait a few seconds for the result.

If you pre-qualify, you’ll see which card you’re likely approved for. Pre-qualification is not a guarantee of approval, but it’s a very strong signal. Most people who pre-qualify and then complete the formal application do get approved, as long as their situation hasn’t changed.

If you don’t pre-qualify, don’t submit the full application. A formal application triggers a hard inquiry, and a hard pull can drop your score by 5 to 10 points. There’s no point taking that hit when the pre-qualification result already told you the answer.

⚠️ Mistake to Avoid: Never apply for a credit card without checking pre-qualification first if the issuer offers it. A denied application costs you a hard inquiry that stays on your credit report for two years, and it gives you nothing in return.

What Happens When You Formally Apply

Once you’re ready to apply, the process is simple. You complete the application inside the OnePay app or on the Walmart site. Synchrony runs a hard credit inquiry, reviews your full credit file, checks your income, and makes a decision.

Most people get an instant decision on the screen. In some cases, the application goes into a “pending” status. That usually means Synchrony needs to verify something, and you may get a mailed decision within 7 to 14 days.

Remember, one application covers both cards. You don’t pick which one you want. Synchrony decides based on your file. You could get:

- Approved for the CashRewards Mastercard. Best outcome. You can use it anywhere.

- Offered the Walmart Spend Card instead. Not a rejection. A step-down option.

- Declined for both. Rare, but it happens with very low scores, recent bankruptcies, or serious delinquencies.

You’ll get your credit limit, APR, and account terms with the approval. Credit limits often start between $300 and $2,000 for fair-credit applicants and can go higher for those with strong profiles.

If You’re Offered the Spend Card Instead

Getting the Spend Card offer is not a denial. Think of it as a bank saying, “We’re not comfortable giving you the Mastercard yet, but we still want you as a customer.”

The Spend Card has some real limits. You can only use it at Walmart locations, Walmart.com, Sam’s Club, and a few Walmart-owned brands. So it won’t help you build a rewards routine at other stores. It also has no ongoing rewards program.

But it does have benefits. It reports to all three major credit bureaus, so it helps you build credit. It has no annual fee. And it can be a stepping stone to the CashRewards Mastercard.

If you accept the Spend Card, here’s your path forward. Use the card for small monthly Walmart purchases. Pay the balance in full every month. Keep your utilization on the card under 30%. Do this for six to twelve months. Then, either check pre-qualification for the CashRewards card, or wait for Synchrony to offer you an upgrade.

If You’re Declined

A denial stings, but it’s not the end of the road. Synchrony is legally required to send you an adverse action notice within 30 days. This letter explains exactly why you were declined. It’s the most valuable document you can get after a denial, because it tells you what to fix.

Common reasons include a credit score that’s too low, too many recent credit inquiries, high credit utilization, insufficient income, past delinquencies with Synchrony, or a thin credit file with too few open accounts.

You also have the option to call the Synchrony reconsideration line. If you believe there was a mistake, or if you can explain a specific issue like a one-time medical hardship, calling can sometimes reverse a denial. Have your denial letter, your income info, and your ID ready when you call.

How long to wait before reapplying

Do not reapply right away. If you get denied and then apply again a week later, you’ll stack up another hard inquiry with no better chance of approval, since nothing about your file has changed.

The general rule is to wait at least six months before reapplying. This gives you time to fix the issues that caused the denial, and it lets some of the older negatives on your report fade in importance. If the denial was tied to a very recent late payment, wait until that payment is at least 12 months old before you try again.

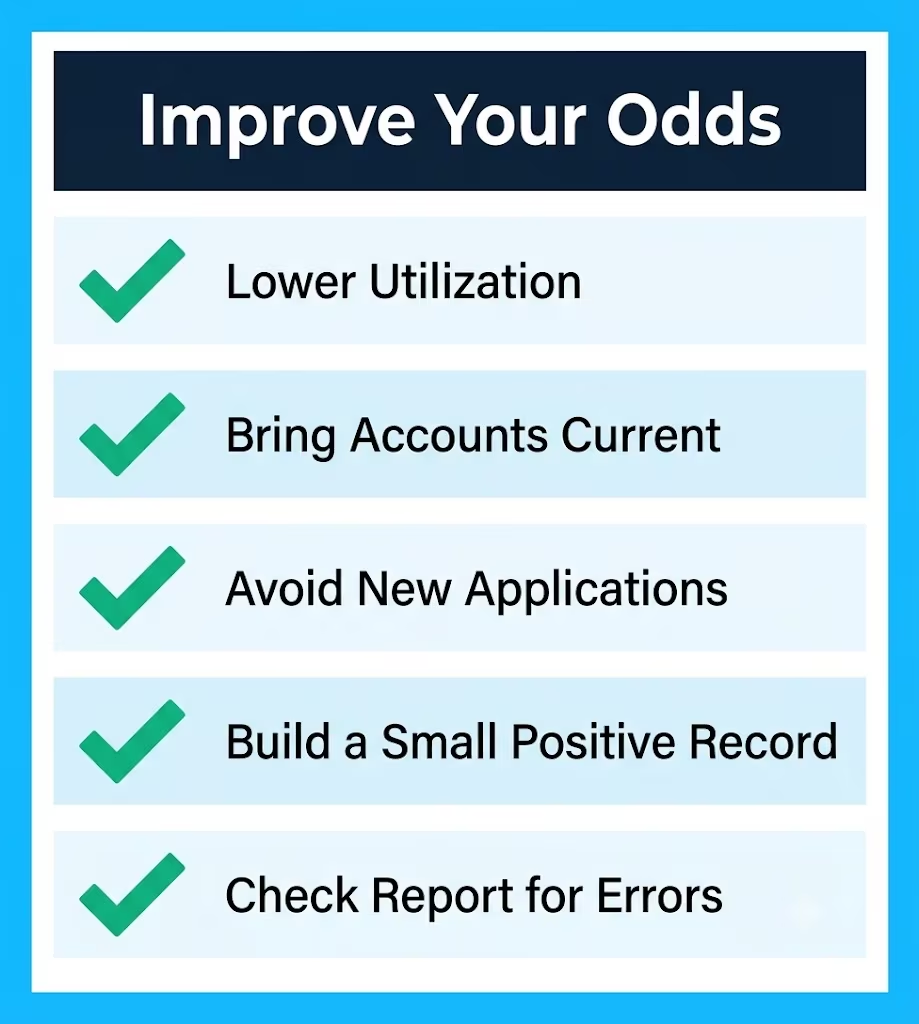

How to Improve Your Odds Before Reapplying

Six months feels long, but it’s plenty of time to make real progress. Focus on the changes that lenders actually notice.

Lower your credit utilization. This is the fastest win. Pay down existing card balances so that each card sits at 30% or less of its limit. Under 10% is even better.

Bring every account current. If you have any past-due balances, catch them up right away. Then keep paying on time, every time, for at least six straight months.

Don’t apply for other credit. Every hard inquiry chips away at your score for a full year and stays on your report for two years. If you’re preparing to reapply for the Walmart card, hold off on all other credit apps.

Build a small positive record. If your credit file is thin, add one anchor account. A secured credit card or a credit-builder loan through a credit union both work well. Use it for one small monthly bill and pay it off every month.

Check your credit report for errors. Order free copies of all three reports at AnnualCreditReport.com. Dispute any account you don’t recognize or any late payment that’s actually incorrect. Fixing a single reporting error can lift a score by 20 to 50 points.

If You Already Have the Old Capital One Walmart Card

If you’re still holding on to a Capital One Walmart card from before the switch, here’s what you need to know. Capital One automatically converted every active Walmart Rewards Mastercard into a standard Capital One Quicksilver card. You didn’t have to do anything, and your account history stayed intact.

The Quicksilver card gives you 1.5% cash back on all purchases. It works anywhere Mastercard is accepted. It’s not tied to Walmart in any way now, so you won’t get bonus rewards at Walmart on that card anymore.

Having the Quicksilver card does not stop you from applying for the new OnePay Walmart cards. They’re completely separate products from a completely separate issuer. You can hold both if you want.

If you rarely used the Quicksilver card and don’t want to keep it, closing it may or may not be the right move. Closing an old card can shorten your average account age and raise your utilization ratio, both of which can lower your score.

If it has no annual fee, most experts recommend keeping it open, using it once every few months for a small purchase, and paying it off. That keeps your credit file strong for future applications, including the new Walmart card.

Frequently Asked Questions

Can I get a Walmart card with bad credit?

Bad credit (usually a FICO score below 580) makes the CashRewards Mastercard very unlikely, but the Walmart Spend Card is still possible for some applicants. Check pre-qualification first to avoid a wasted hard pull.

Does checking pre-qualification hurt my credit score?

No. Pre-qualification uses a soft credit inquiry, which does not appear on your credit report and does not affect your score. Only the formal application triggers a hard pull.

Is the Walmart card still through Capital One?

No. Capital One ended its Walmart partnership. The current cards are issued by Synchrony Bank through OnePay, Walmart’s fintech partner. Existing Capital One Walmart cardholders were moved to the Capital One Quicksilver card.

Which credit bureau does Synchrony use for the Walmart card?

Synchrony pulls from all three major bureaus depending on your state and profile, but it most often uses Equifax or TransUnion. You cannot choose which bureau they pull.

What credit limit will I get on the Walmart card?

Starting credit limits vary widely. Fair-credit applicants often report limits between $300 and $1,000. Applicants with good to excellent credit report limits of $2,500 to $5,000 or more.

How long does approval take?

Most decisions are instant. Some applications go into a pending review and take 7 to 14 days, with the final decision arriving by mail or in the OnePay app.

Bottom Line

Getting approved for a Walmart card in 2026 is easier to plan for once you know the rules have changed. The old Capital One version is gone, and the new OnePay cards are issued by Synchrony, which tends to work with fair-credit applicants.

Check pre-qualification first, based on cardholder reports and Synchrony’s style. Aim for a FICO score in the mid-600s or higher for the CashRewards Mastercard. Also, view the Walmart Spend Card as a useful stepping stone, not a rejection.

If you know someone who’s rebuilding credit or planning a big Walmart shopping trip, share this guide with them on social media. It could save them from a wasted hard inquiry and help them pick the right card the first time.