If you’ve been checking your credit score and noticed it dipping for no clear reason, you’re not alone. Many people pay their cards on time, yet still see scores drop because their credit utilization ratio is quietly working against them. It’s confusing, frustrating, and often blamed on the wrong things.

Credit utilization is the percentage of your revolving credit you’re using at the time it gets reported to the credit bureaus.

In the next sections, we’ll walk through how it’s calculated, why the 30% rule is misleading, and the exact steps you can take to lower it fast.

Key Takeaways

This guide explains how credit utilization ratio works, including how to calculate both overall and per-card percentages, why the 30% rule is a warning floor rather than a goal, and the fastest strategies to lower your ratio within one billing cycle.

Core Facts:

- Credit utilization accounts for roughly 30% of your FICO score and is calculated by dividing total revolving balances by total revolving credit limits.

- The target for maximum credit score points is under 10% utilization, not 30%; consumers with FICO scores above 800 typically carry around 7%.

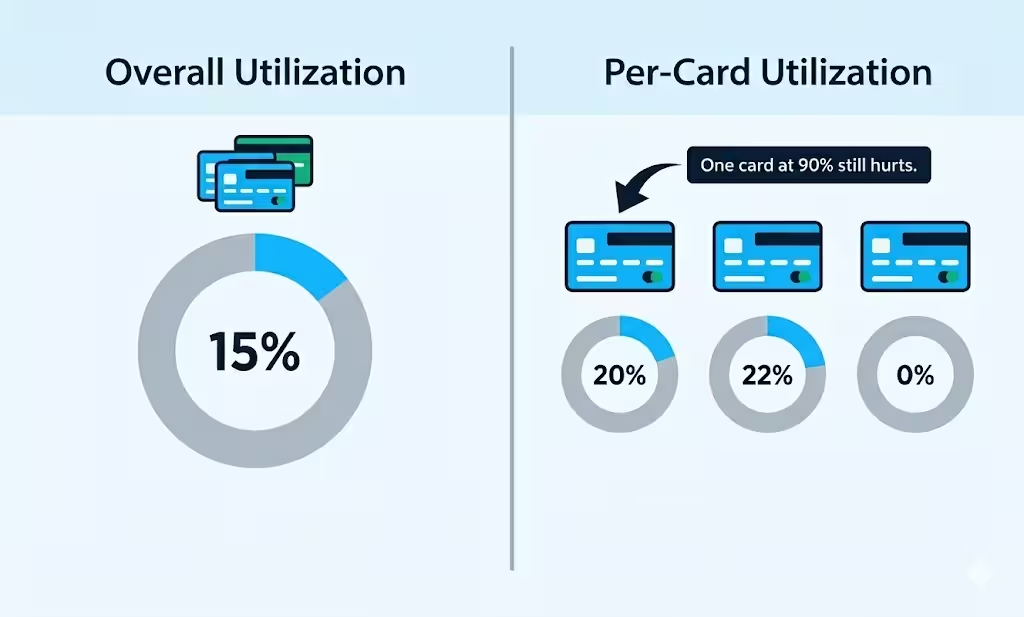

- Both overall utilization and per-card utilization are scored separately; one card at 90% can drop your score significantly even when your overall ratio looks healthy.

- Card issuers report balances on the statement closing date, not the payment due date, so paying before the statement closes is what lowers reported utilization.

- Closing a paid-off credit card removes its limit from your available credit, which raises your utilization ratio and can drop your score immediately.

- The AZEO method (paying all cards to zero except one small reported balance) is the fastest way to maximize your score before a mortgage or major loan application.

Best for:

- People who pay their credit cards in full each month but still see unexpectedly high utilization on their credit reports.

- Anyone preparing to apply for a mortgage, auto loan, or other major credit product within the next 30 to 60 days.

- Cardholders who want to understand why closing a paid-off card or carrying a balance on just one card is hurting their credit score.

What Is a Credit Utilization Ratio?

Your credit utilization ratio is the share of your revolving credit that you are actively using. It compares the balances on your revolving accounts to your total credit limits, then turns that into a percentage. So if you owe $1,000 across cards and your limits add up to $10,000, your ratio is 10%.

This ratio sits inside the “amounts owed” category of your FICO score. That category alone accounts for about 30% of your FICO score, which makes the balance-to-limit ratio one of the most powerful score levers you control day to day. Payment history matters more over time, but utilization can move your score within a single billing cycle.

There are two levels you need to know:

- Overall utilization: All revolving balances divided by all revolving credit limits.

- Per-card utilization: One card’s balance divided by that card’s limit.

Scoring models look at both. A clean overall number can still hide a maxed-out single card, and that single card can drag your score down.

Which Accounts Count Toward Your Credit Utilization

Only revolving accounts count. That means:

- Credit cards (Visa, Mastercard, American Express, Discover, store cards)

- Home equity lines of credit (HELOCs) in most cases

- Personal lines of credit with revolving terms

Installment loans do not count. Your auto loan, mortgage, student loan, and personal installment loans are tracked separately. They affect your credit, but they don’t push your utilization number up or down. So paying off a car loan won’t lower this ratio, and taking on a mortgage won’t raise it.

Charge cards (which require full payment each month) are handled differently across scoring models, and most modern FICO versions exclude them from the standard utilization calculation.

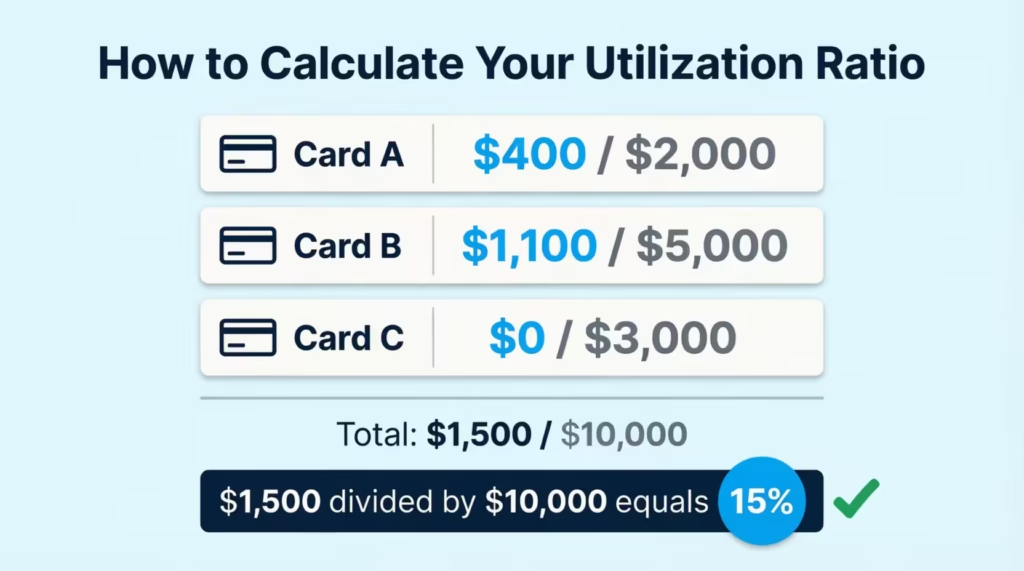

How to Calculate Your Credit Utilization Ratio

The formula is simple:

(Total revolving balances ÷ Total revolving credit limits) × 100 = Utilization %

Here’s a clear three-card example:

| Card | Balance | Credit Limit |

|---|---|---|

| Card A | $400 | $2,000 |

| Card B | $1,100 | $5,000 |

| Card C | $0 | $3,000 |

| Total | $1,500 | $10,000 |

Run the math: $1,500 ÷ $10,000 = 0.15, or 15% overall utilization.

This is the number most people focus on. But it’s only half the picture. You also need to check each card on its own, because one high card can quietly hurt your score even when the overall number looks fine.

How to Calculate Per-Card Credit Utilization

For a single card, use the same formula on just that account:

(Card balance ÷ Card limit) × 100 = Per-card utilization %

Using the example above:

- Card A: $400 ÷ $2,000 = 20%

- Card B: $1,100 ÷ $5,000 = 22%

- Card C: $0 ÷ $3,000 = 0%

None of these cards is flagged as high-risk. But if Card A had a $1,800 balance instead of $400, its per-card ratio would jump to 90%. That single number can pull your score down even if your overall ratio stays modest. So scan every card, find your highest, and treat that one as the priority.

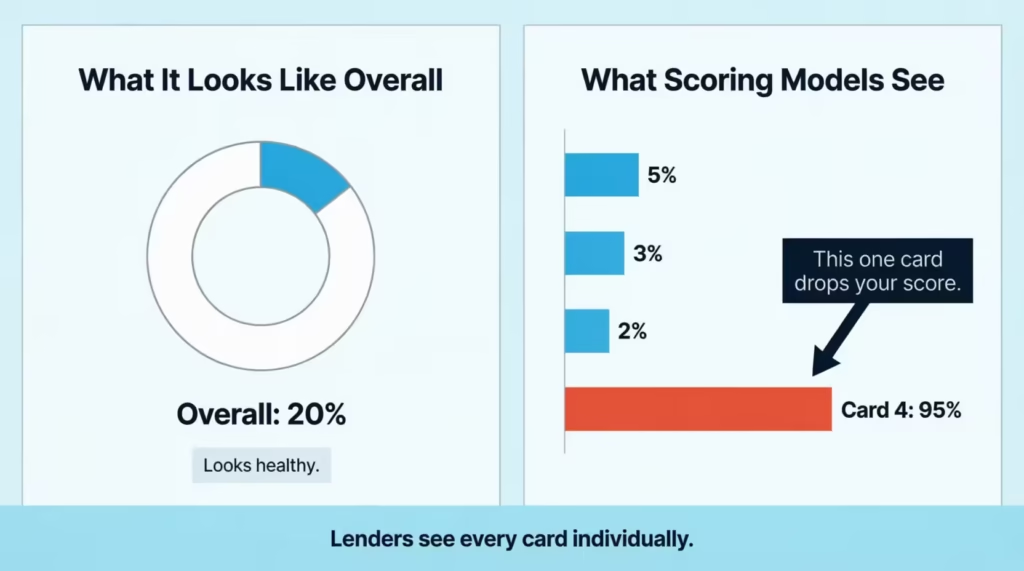

Per-Card vs. Overall Utilization: Why Both Numbers Matter

Both scoring models, FICO and VantageScore, look at your overall number and your worst single card. This is where many people get blindsided.

Picture this. Jennifer, a marketing manager, has four cards with $20,000 in total limit of $20,000. She owes $4,000 across them, so her overall balance sits at a healthy 20%. But $3,800 of that sits on one card with a $4,000 limit, putting that card at 95% utilization. Her overall looks fine, yet her FICO score drops by 40 points because the system flags that single maxed-out card as a risk signal.

Lenders read a near-maxed card as a sign of cash flow stress. Even if your other cards are spotless, that one outlier can trigger:

- Credit score drops

- Higher interest rate offers

- Denied credit limit increase requests

- Failed mortgage pre-approval

The fix is balance distribution. Spread spending across cards so no single card crosses 30%, and ideally stay under 10% on each one. We’ll cover the steps for this in the following section.

How Credit Utilization Affects Your Credit Score

The “amounts owed” category drives roughly 30% of your FICO score, and credit utilization is the dominant piece inside it. That makes this ratio second only to payment history in score impact.

Why do lenders care so much? Because high utilization predicts default risk. A person using 80% of their revolving credit is statistically more likely to miss a payment than someone using 5%. Credit bureaus and lenders use this signal to forecast whether you can handle more debt. So when your utilization climbs, your score drops, even if you’ve never missed a payment.

The impact is also non-linear. Going from 10% to 20% might cost a few points. Going from 50% to 70% can cost 30 to 50 points. Going from 80% to maxed out can drop you 60 points or more on a strong file. The damage scales sharply at higher tiers.

Here’s the encouraging part. Utilization has no memory. Late payments can sit on your report for seven years, but a high utilization month vanishes from the calculation as soon as a lower balance is reported. Fix the number, and the score recovers fast.

How FICO 10T and VantageScore 4.0 Use Trended Data

Older scoring models took a snapshot. They looked at your utilization on one date and judged you on that single moment. FICO Score 10T and VantageScore 4.0 changed that by adding trended data, which tracks your balances over the past 24 months.

What does that mean for you? These newer models can tell the difference between:

- A person who carries a balance and slowly pays it down

- A person who charges and pays in full every month

- A person whose balances keep climbing month after month

Two people with the same current utilization can now get different scores based on their trajectory. If your balances have been steadily falling for two years, trended models reward you. If they’ve been creeping up, those models penalize you, even if your snapshot ratio looks acceptable today.

Mortgage lenders and major credit card issuers increasingly use these trended scores. So consistent low utilization over time is now more valuable than a one-time clean-up before a loan application.

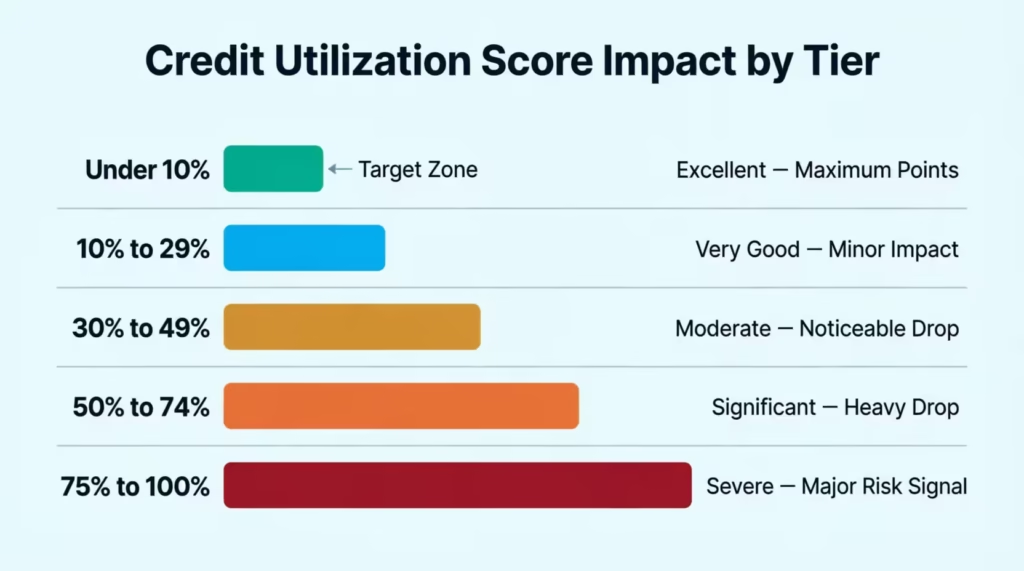

What Is a Good Credit Utilization Ratio?

The honest answer surprises most people. The lower, the better, with one exception: 0% across all cards can be a small negative because it suggests no recent revolving activity. A tiny bit of usage looks better than none.

Here’s the tier breakdown most scoring models follow:

| Utilization Tier | Range | Score Impact |

|---|---|---|

| Excellent | Under 10% | Maximum points |

| Very Good | 10% – 29% | Minor impact |

| Moderate Damage | 30% – 49% | Noticeable score drop |

| Significant Damage | 50% – 74% | Heavy score drop |

| Severe Damage | 75% – 100% | Major risk signal |

According to data from Experian, consumers with FICO scores of 800 or higher typically carry an average utilization of around 7%, sometimes lower. That’s the real target for top-tier scores, not 30%.

💡 Pro Tip: If you want to maximize your score, aim for under 10% overall and under 10% on every single card the month before you apply for a mortgage, car loan, or any major credit decision.

Why 30% Is the Floor — Not the Target

You’ve probably heard the phrase “keep your utilization under 30%.” It’s the most repeated and most misunderstood rule in personal finance. 30% is not a goal. It’s a warning floor. It’s the line where serious score damage begins, not the line where you earn maximum points.

Think of it like a speed limit on a highway. Driving 65 mph isn’t the “best” speed. It’s the maximum before consequences start. Same idea here. At 30% utilization, you’ve already left the excellent range. At 31% to 49%, the damage grows. Above 50%, the drop is steep.

People with the highest scores treat 30% as a hard ceiling they never cross, and they aim much lower. So if you want a healthy score, set your personal cap at under 10%, treat 30% as the danger line, and avoid it the way you’d avoid a missed payment.

Why You Can Pay in Full Every Month and Still Have High Utilization

This is the most common credit score frustration. You pay your card off in full each month, yet your utilization shows 40%, 60%, or higher. The fix starts with understanding when your balance gets reported.

Most card issuers send your balance to the credit bureaus on your statement closing date, not your due date. Those are two different days. Your statement date is when the billing cycle ends, and the balance is locked in. Your due date is usually about three weeks later.

So here’s what happens. Your statement closes on the 5th with a $2,000 balance on a $4,000 limit card. That’s 50% utilization, and it gets reported. You then pay the full $2,000 by the due date on the 28th. Your card balance is now $0, but the bureaus have already recorded 50%. Your score will reflect that 50% for weeks until the next statement reports a lower number.

Paying in full protects you from interest charges, but it does not protect your score on its own. The timing of your payment matters as much as the amount.

⚠️ Mistake to Avoid: Waiting for the due date to pay is the single biggest reason responsible cardholders see high utilization. Paying full balances early, before the statement closes, fixes this overnight.

When and How Your Balance Gets Reported to the Bureaus

Each card reports separately, and most do it once a month on or near the statement closing date. That creates a few important quirks:

- Different cards report on different days. A four-card wallet might have statement dates on the 3rd, 12th, 18th, and 25th. Each gets reported around its own date.

- The reported balance is whatever sits on the card that day. Spend $500 the day before? That counts. Pay $500 the day before? That helps.

- The bureaus update once the report arrives. Most scores refresh within a few days of new data hitting your file.

- Three bureaus, three timelines. Experian, Equifax, and TransUnion don’t always update on the same day, so a score check on one might lag the others.

The takeaway: if you want low reported utilization, pay your balance down before the statement closes, not before the due date. Many people set a payment for a few days before each card’s statement date, which keeps the reported balance low without any other changes.

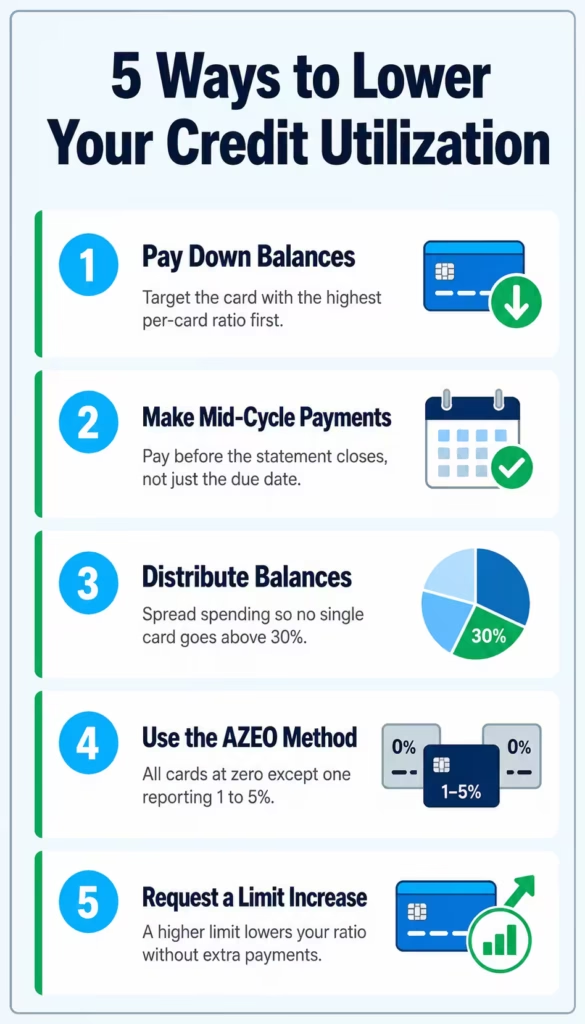

How to Lower Your Credit Utilization Ratio

There are five reliable strategies for lowering this ratio, and most people only know one of them.

1. Pay down balances aggressively.

This is the obvious one. Apply extra money first to the card with the highest per-card utilization, not the highest interest rate, when your goal is score improvement. Then move to the next highest.

2. Make mid-cycle payments.

Pay a chunk of the balance before the statement closing date. This shrinks the number that gets reported. Many people make two payments a month, one before the statement closes and one before the due date. Sometimes called the “two-payment trick,” it’s the fastest score booster.

3. Distribute balances across cards

If one card is at 80% and another is at 5%, move spending or pay down the high one. Spreading usage keeps every per-card utilization low, which protects you from the single-card score hit we covered earlier.

4. Use the AZEO method before applications.

AZEO stands for All Zero Except One. Pay every card down to $0 before the statement closes, except one, and let that one report a tiny balance (1% to 5% of its limit). This setup is known to produce the highest FICO scores for short-term events like mortgage applications.

5. Request a credit limit increase.

A bigger denominator means a smaller ratio without paying anything down. Used carefully, this is the easiest lever in the toolbox.

📌 Did You Know: David, a software engineer with a 740 score, used the two-payment trick and AZEO for two months before applying for a mortgage. His score climbed to 798, which moved him into a tier that saved him roughly $11,400 in interest over the life of his loan.

How to Request a Credit Limit Increase

A credit line increase shrinks your utilization instantly. If you have a $5,000 limit and a $1,500 balance (30%), bumping the limit to $10,000 drops you to 15% without paying a cent.

Here’s how to do it well:

- Wait until you’ve had the card for at least 6 months with on-time payments.

- Ask online or through the app first. Many issuers, like Capital One, Chase, and Discover, offer a quick request form.

- Confirm whether the issuer uses a soft or hard inquiry. A soft pull doesn’t affect your score. A hard pull can shave a few points and stay on your report for two years.

- Ask for a meaningful jump. Issuers often grant 10% to 25% of your current limit. So a $5,000 limit might rise to $6,250 or so.

- Have your income updated in their system. Higher reported income improves your odds.

Avoid this if you tend to spend up to your limit. A larger denominator only helps if your balance stays low. Otherwise, you’re just unlocking more debt.

Why Closing a Paid-Off Card Can Hurt Your Credit Utilization

It feels logical. The card is paid off, so you close it to clean up your wallet. The problem is that closing a card removes its credit limit from the denominator of your utilization formula. Your usable credit shrinks, and your ratio jumps.

Consider Sarah, a project manager who paid off a store card with a $5,000 limit. Before closing, her total revolving credit was $20,000 with $3,000 in balances, giving her 15% utilization. After closing the card, her total limit dropped to $15,000 with the same $3,000 balance, pushing her to 20% utilization. Her FICO score dropped by about 10 points that month.

Closing also affects the average age of your accounts over time, especially if the card was one of your oldest. Both factors can pull your score down.

Better options for a card you don’t use:

- Keep it open with no annual fee and use it for one small recurring charge like a streaming subscription on autopay.

- Downgrade an annual fee card to a no-fee version with the same issuer. The account history stays intact.

- Close it only if the annual fee is high and you have plenty of other long-standing credit cards, so the impact stays small.

How Quickly Does Credit Utilization Affect Your Credit Score?

Faster than almost any other credit factor. Once your card issuer reports a lower balance, the credit bureaus update your file within a few days, and most scoring models reflect the change right away. So a single billing cycle can move your score in either direction.

Typical timeline for a score recovery:

- Days 1 to 30: You pay down balances.

- Days 25 to 35: Statement closes, and the new balance gets reported.

- Days 30 to 45: Bureaus, update your file, and your score reflects the change.

- Days 45 to 60: Most scoring models, including newer FICO and VantageScore 4.0 versions, show the full effect.

So most people see results within 30 to 60 days of changing their behavior. Compare that to a late payment, which sits on your report for seven years, or a bankruptcy, which can stay for up to ten. Utilization is one of the few score factors with no long memory.

If you need a faster fix, ask your mortgage lender about rapid rescoring. It’s a service mortgage lenders can use to push updated balance information to the bureaus and refresh your score in 3 to 5 business days. You can’t request it directly. It must come through a lender, and it’s used to clean up a file right before underwriting.

Common Mistakes That Spike Your Credit Utilization Without Warning

A few habits quietly push the ratio up without people noticing. Watch for these:

Waiting for the due date to pay.

As covered above, the statement date is what matters for reporting, not the due date. Late payment timing alone can lock in high utilization.

Closing zero-balance cards.

Removing unused credit limits shrinks your denominator and raises your overall ratio overnight.

Maxing out a new card.

A new card with a low limit fills up fast. A $500 charge on a $1,000 limit is 50% utilization, which can sting even if your overall number stays low.

Only making minimum payments.

A minimum payment barely dents the balance. The reported number stays high month after month, and trended data models pick up on the pattern.

Big one-time purchases.

A vacation, a wedding deposit, or a medical bill on a card can push that single card past 70% in one swipe. Even paying it off later won’t help until the next statement reports a lower number.

Ignoring authorized user accounts.

If you’re an authorized user on someone else’s card and they run up the balance, that utilization can flow into your file, too.

Letting an old card auto-close from inactivity.

Some issuers close cards with no activity for 12 to 24 months. That quietly trims your available credit. Run one small charge a year to keep the account active.

Scan your wallet against this list each month. Catching one of these early can save your score the same way smoke detectors save houses, before damage scales.

Frequently Asked Questions (FAQs)

What is a good credit utilization ratio?

Under 10% is the target for maximum credit score points, not 30%. The 30% threshold is where serious score damage begins. People with FICO scores above 800 typically carry around 7% utilization, and that is the real benchmark to aim for.

What is the highest balance I should have on a $3,000 credit card?

Keep your balance at $300 or less to stay under the 10% utilization target that maximizes your credit score. A $900 balance hits the 30% warning floor, which is where score damage begins and should be treated as a hard ceiling, not a goal.

Will 20% utilization hurt my credit?

At 20%, you are in the “very good” tier with only minor score impact. You will not see heavy damage until you cross 30%, but scores at the highest level typically reflect utilization below 10%, so 20% still leaves room for improvement.

Will 50% credit utilization hurt me?

Yes. At 50% utilization, you are in the “significant damage” tier, and you can expect a heavy score drop compared to someone carrying 10% or less. Paying down the balance before your statement closing date is the fastest way to recover.

Is 70% utilization bad?

Yes. Utilization between 50% and 74% falls in the “significant damage” range, and at 70%, you are approaching the severe tier where lenders flag your file as high risk. Even one card sitting at 70% can drop your score sharply, regardless of your overall ratio.

What happens if I use 90% of my credit card limit?

At 90%, you are in the “severe damage” tier, which can drop a strong credit file by 60 points or more. Lenders read near-maxed cards as a cash flow warning, which can trigger higher interest rate offers, denied limit increases, and failed loan pre-approvals.

What is the biggest killer of credit scores?

Payment history is the single largest factor, accounting for about 35% of your FICO score, and a single missed payment can stay on your report for seven years. Credit utilization is the second biggest factor at roughly 30%, but it can be corrected within one billing cycle.

If I pay my credit card in full every month, why is my utilization still high?

Your card issuer reports your balance on the statement closing date, not the due date, which is usually three weeks later. Paying in full before the due date eliminates interest charges but does not lower the balance that gets reported; paying before the statement closes is what fixes utilization.

Does closing a paid-off credit card hurt your credit score?

Yes. Closing a card removes its credit limit from your total available credit, which shrinks the denominator in your utilization formula and raises your ratio immediately. Keeping a no-annual-fee card open with one small recurring charge is usually the better move.

Bottom Line

Credit utilization is one of the fastest-moving levers on your credit score, and it rewards small habit changes more than dramatic ones.

To improve your score, keep both your overall and per-card ratios below 10%. Pay down balances before the statement closes, not just before the due date. Also, avoid closing paid-off cards unless the fee is more significant than the score impact. We’ve covered the math, the myths around 30%, and the exact steps to lower the number fast.

If you know someone stressed about a credit score drop they can’t explain, share this guide. It could be the single thing that helps them save thousands on their next loan.