We get this question a lot, and it makes total sense. You just got your Venmo debit card, and now you’re worried that swiping it, overdrafting, or letting fees pile up could show up on your credit report. That fear grows when you can’t tell if the Venmo debit card works like a bank card or a credit card. One wrong move, you think, and your score drops.

Here is the short answer. Using a Venmo debit card does not affect your credit score in any direct way.

Keep reading. You’ll learn the exact reasons why, the rare edge cases that could still cause trouble, and smart steps to build credit the right way.

Key Takeaways

This guide explains whether a Venmo debit card affects your credit score, covering how debit spending differs from credit reporting, the ChexSystems overdraft risk, and how the separate Venmo credit card impacts your score instead.

Core Facts:

- The Venmo debit card does not affect your credit score directly because it spends existing balance funds rather than borrowed money, so it is never reported to Experian, Equifax, or TransUnion.

- Applying for the Venmo debit card triggers no hard inquiry or credit check, though Venmo may review ChexSystems, a separate checking account history database.

- A negative Venmo balance alone does not appear on your credit report, but an unpaid balance sent to collections can lower your score by 50 to 100 points or more.

- The Venmo credit card is a Visa issued by Synchrony Bank, requires a hard inquiry to apply, and reports payment history and utilization to all three credit bureaus monthly.

- Venmo Pay Later can affect your credit score since missed payments may be reported, while on-time payments may help depending on the service’s reporting practices.

- Credit-building alternatives mentioned include the Venmo credit card, secured credit cards, becoming an authorized user, and credit-builder loans offered through credit unions.

Best for:

- Venmo debit card users worried that everyday spending could be lowering their credit score.

- Readers trying to understand the difference between Venmo’s debit card and its separate credit card product.

- Anyone with an unpaid negative Venmo balance who wants to understand the collections risk before it escalates.

Does the Venmo Debit Card Affect Your Credit Score?

No. The Venmo debit card does not affect your credit score. It will not help your score, and it will not hurt it. You can swipe it for coffee, gas, groceries, or bills, and none of that spending shows up on your credit report.

The reason is simple. A debit card pulls money you already own. It does not borrow money. Credit scores track how you handle borrowed money, not how you spend your own cash. So the Venmo Mastercard debit card sits outside the whole credit reporting system.

You do not need to worry about “using it too much” or “using it too little.” There is no credit limit to max out. There is no monthly bill to miss. It works like any other bank debit card tied to your Venmo balance or your linked bank account.

If you were hoping the card would help build your credit, that will not happen either. To build credit, you need a product that reports to the three big credit bureaus. A standard debit card, including this one, does not.

What Venmo Debit Card Transactions Actually Show Up As

Every time you use the card, the charge shows up in two places. It hits your Venmo activity feed, and it lands on your bank or Venmo balance statement. That is it. No credit bureau ever sees the transaction.

Think of it like using cash from your wallet. The store logs the sale. Your bank logs the withdrawal. But no one calls Experian, Equifax, or TransUnion to tell them what you bought.

This is true for online buys, in-store swipes, tap-to-pay, and ATM withdrawals. All of it stays inside the banking system, not the credit system.

Do Personal Venmo Transfers Affect Credit at All?

No. Sending your friend $20 for pizza has zero effect on your credit. Receiving $100 from a family member has zero effect too. Peer-to-peer transfers are just money moving between accounts.

Credit bureaus only care about loans, credit cards, and other borrowed money. A cash transfer is not a loan. It is not credit. So it never shows up in your credit file.

Why Debit Cards Can’t Affect Your Credit Score

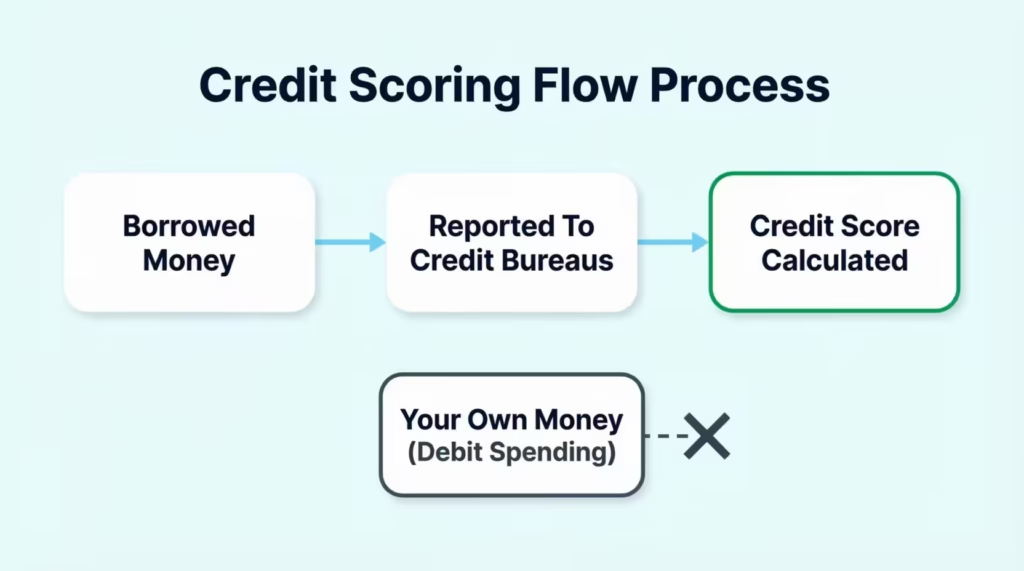

To understand why, you need to know what a credit score actually measures. Your score reflects how well you manage borrowed money. Lenders report your activity to the three big credit bureaus, Experian, Equifax, and TransUnion. Those bureaus then build your credit report.

A debit card does not fit into that system at all. When you swipe a debit card, you are spending your own money from your checking or Venmo balance. No lender is involved. No money is being borrowed. So there is nothing to report.

Credit scores are built from five main factors. Payment history and credit utilization ratio make up the biggest chunks. Both of those need revolving credit, like a credit card, or an installment loan, like a car payment. A debit card is neither.

Since a debit card offers no credit line, there is no utilization to measure. Since there is no monthly bill, there is no payment history to track. This is why the credit bureau reporting process skips debit cards completely.

📌 Did You Know: Debit card activity never touches your FICO or VantageScore. Even if you use your debit card every day for 10 years, your credit file will show nothing from that spending.

Some people ask if heavy debit card use can somehow “prove” you are good with money. It cannot. Lenders only look at what the bureaus report. If it is not in your credit file, it does not count.

Venmo Debit Card vs. Venmo Credit Card: Key Differences

These two cards look similar, share the Venmo name, and live in the same app. But they work in totally different ways. Mixing them up is the number one reason people get confused about credit impact.

The Venmo debit card is a Mastercard debit card issued through The Bancorp Bank. It pulls from your Venmo balance or linked bank account. It does not extend credit. It does not report to any credit bureau.

The Venmo credit card is a Visa credit card issued by Synchrony Bank. It gives you a credit line. Every swipe borrows money that you must pay back later. It reports to all three credit bureaus every month.

Here is a quick side-by-side view:

| Feature | Venmo Debit Card | Venmo Credit Card |

|---|---|---|

| Card type | Mastercard debit | Visa credit |

| Issuer | The Bancorp Bank | Synchrony Bank |

| Source of funds | Your Venmo balance or bank | A credit line |

| Credit check to apply | No | Yes, hard inquiry |

| Reports to credit bureaus | No | Yes |

| Can build credit | No | Yes |

| Can hurt credit | No, in most cases | Yes, if misused |

So the confusion clears up fast when you focus on one thing. Debit spends your money. Credit borrows the bank’s money. Only the borrowed kind touches your credit report.

Does Applying for the Venmo Debit Card Trigger a Credit Check?

No. Signing up for the Venmo debit card does not trigger a hard inquiry. There is no credit check, no soft pull, and no impact on your score.

Venmo may check ChexSystems or a similar bank-focused database. That is a checking account history check, not a credit history check. It tells them if you have a record of unpaid overdrafts at other banks. It does not touch your FICO or VantageScore.

So you can apply with zero risk to your credit file. This is very different from applying for the Venmo credit card, which does trigger a hard inquiry.

Can a Negative Venmo Balance or Overdraft Hurt Your Credit?

For most users, no. A negative Venmo balance by itself does not hit your credit report. Venmo will try to pull the missing amount from your linked bank account. If that fails, you may see an overdraft fee or a negative balance sitting in your Venmo account.

At that stage, your credit score is still safe. Venmo does not report a small negative balance to Experian, Equifax, or TransUnion the way a credit card would report a missed payment.

But there is a path where trouble can start. If the negative balance grows large, and you ignore it for a long time, Venmo can send the debt to a collections agency. Collections accounts do show up on your credit report. That is the one indirect way this debit card could affect your score.

To keep things safe, cover any negative balance quickly. Even a few dollars is worth resolving before it grows.

ChexSystems and Checking Account Reporting Agencies

ChexSystems is not a credit bureau. It is a reporting agency that tracks checking and debit account behavior. Think of it as a credit report, but for bank accounts.

If you overdraft repeatedly, bounce payments, or leave a negative balance unpaid, that history can land in ChexSystems. Future banks may see it when you try to open a new checking account. But it will not show up on your Experian, Equifax, or TransUnion file.

So a ChexSystems mark can make it harder to get a new bank account, but it will not lower your credit score by itself.

What Happens If You Don’t Pay Off Venmo Fees or a Negative Balance

This is the one real risk to your credit. If you leave a negative balance or unpaid fees on your Venmo account long enough, Venmo can charge off the debt and sell it to a third-party collections agency.

That agency can then report the debt to the credit bureaus. Once it lands on your credit report, it counts as a collections account. Collections can drop your score by 50 to 100 points or more, and the mark can stay on your file for up to seven years.

The good news is this rarely happens by accident. It takes months of ignored notices, unpaid fees, and unanswered emails. Pay off any negative balance right away, and you never enter this danger zone.

⚠️ Mistake to Avoid: Do not ignore a negative Venmo balance thinking it is “too small to matter.” Even a $15 unpaid balance can grow with fees, get sent to collections, and damage your credit for years.

Does the Venmo Credit Card Affect Your Credit Score?

Yes. The Venmo credit card is a true credit card, and it works like any other. When you apply, Synchrony Bank runs a hard inquiry, which can shave a few points off your score for a short time.

Once approved, every action you take on the card gets reported to the credit bureaus. Your payment history, your credit utilization, your balances, and your account age all go into the mix. Pay on time and keep balances low, and your score can climb. Miss payments or max out the card, and your score can drop.

The utilization ratio matters a lot. If your card has a $1,000 limit and you carry a $700 balance, that is 70% utilization.

Does Venmo Pay Later Affect Credit Score?

Yes, it can. Venmo Pay Later is a buy now, pay later product. Some BNPL services report to credit bureaus, and some do not, but the industry is moving toward full reporting.

If you use Pay Later and miss a payment, that missed payment can be reported and hurt your score. On-time payments may help your score if the service reports positive history. Read the terms before you use it so you know what gets shared with the bureaus.

Does the Venmo 1099-K Form Affect Your Credit Score?

No. A 1099-K is a tax form, not a credit record. Venmo sends this form to users who receive over a certain amount in business payments during the year. The IRS gets a copy too.

Tax forms and tax debts are separate from your credit report. Even if you owe the IRS money, that debt itself does not show up on your credit file the way it used to. So the 1099-K has zero direct effect on your credit score.

How to Actually Build Credit If the Venmo Debit Card Won’t Do It

Since a debit card cannot build credit, you need a product that does report to the bureaus. Good news, there are several beginner-friendly options.

1. Apply for the Venmo credit card

If you have some credit history already, this can be a fit. It reports to all three bureaus and offers cash back through the Venmo app. Use it for small buys, pay the full balance every month, and your score can grow over time.

2. Get a secured credit card

Secured cards are made for people with no credit or bad credit. You put down a small cash deposit, usually $200 to $500, and that becomes your credit line. The card reports to the bureaus like any regular credit card. After 6 to 12 months of on-time payments, many issuers will upgrade you to a regular unsecured card.

3. Become an authorized user

Ask a parent, spouse, or trusted family member to add you as an authorized user on their credit card. Their good payment history can show up on your credit file too. You do not even need to use the card. Just being on the account can help.

4. Try a credit-builder loan

Many credit unions offer these. You “borrow” a small amount, but the money sits in a savings account while you make payments. Every payment gets reported. At the end, you get the money back, and your credit file has a new positive tradeline.

💡 Pro Tip: Keep your credit utilization ratio below 10% for the fastest score gains. If your credit limit is $500, try not to carry a balance above $50 at statement close, even if you spend more during the month.

The key across all of these is on-time payments. Payment history is the single biggest factor in your credit score, making up about 35% of your FICO score.

Tips to Avoid Any Credit-Adjacent Risk on Your Venmo Debit Card

Even though the card itself cannot hurt your credit, sloppy account habits can still lead to trouble through the collections path. Follow these steps to stay safe.

Monitor your Venmo balance often

Check the app at least once a week. Know how much sits in your Venmo balance and what is scheduled to come out.

Turn off or manage auto-reload settings

Auto-reload pulls money from your linked bank account when your Venmo balance runs low. That is helpful, but only if your bank account has enough to cover it. If your bank is short, you could face overdraft fees on both sides.

Keep your linked bank account funded

Any bill pay, auto-reload, or scheduled transfer needs money in your account. A failed pull can lead to a negative Venmo balance, which starts the risk clock.

Resolve any negative balance the same day

If you notice a negative balance in Venmo, transfer money in right away. Do not let it sit for weeks.

Read every email and app notification from Venmo

If Venmo is trying to collect a debt, they will contact you first. Ignoring those messages is what pushes an unpaid balance toward collections.

Never use the debit card for money you do not have

Since it is not a credit card, it will simply decline. But if you have overdraft protection linked to a bank account, an overdraft could still happen there and cost you fees.

Keep records of any dispute

If a charge looks wrong, dispute it fast through the Venmo app. Screenshots and emails help if things escalate.

Follow these steps, and your Venmo debit card stays exactly what it should be, a simple way to spend your own money with no credit report drama.

Frequently Asked Questions (FAQs)

Is the Venmo debit card actually a credit card?

No, the Venmo debit card is a Mastercard debit card issued through The Bancorp Bank. It pulls money from your Venmo balance or linked bank account instead of offering a credit line.

Does a Venmo card build credit?

The Venmo debit card does not build credit because it never reports to Experian, Equifax, or TransUnion. The Venmo credit card does build credit since Synchrony Bank reports your payment activity to all three bureaus monthly.

Are there any downsides to a Venmo debit card?

The main downside is an indirect one: an unpaid negative balance can eventually get sent to collections, and collections accounts do hurt your credit score. Otherwise, normal debit card use carries no credit risk.

Does applying for a Venmo debit card run a credit check?

No, signing up for the Venmo debit card triggers no hard inquiry and no credit check. Venmo may check ChexSystems for your checking account history, but that is separate from your FICO or VantageScore.

Is my Venmo card a credit or debit card?

Venmo offers two separate cards: a Mastercard debit card that spends your own money, and a Visa credit card issued by Synchrony Bank that extends a credit line. Check your card design or account settings to confirm which one you have.

Is the Venmo credit card good for building credit?

Yes, the Venmo credit card reports to all three credit bureaus every month, so on-time payments and low balances can help your score grow. Missed payments or high utilization can hurt it instead.

Does a negative Venmo balance affect your credit score?

A small negative balance alone does not hit your credit report right away. If it goes unpaid for a long time, Venmo can send it to collections, which can drop your score by 50 to 100 points or more.

Does Venmo Pay Later affect your credit score?

Yes, Venmo Pay Later is a buy now, pay later product, and missed payments can be reported and hurt your score. Some Pay Later services also report on-time payments, which can help your score.

How does Venmo debit card spending compare to using cash?

Using the Venmo debit card works like spending cash from your wallet since it pulls money you already own rather than borrowing. The store and your bank log the transaction, but no credit bureau ever sees it.

Wrapping Up

Here is the bottom line. The Venmo debit card does not affect your credit score directly. It does not report to any bureau, does not build credit, and cannot hurt your score through normal use. The only real risk comes from ignoring a negative balance long enough for it to reach collections.

Based on how credit scoring works, the most effective approach is simple. Use the debit card freely for daily spending, keep your balance out of the red, and pair it with a credit-building product like a secured card or the Venmo credit card if you want your score to grow.

If you know a friend or family member who worries their debit card might be quietly hurting their credit, share this guide with them. It could save them from a big misunderstanding and help them make smarter money moves.