I get this question a lot from friends and family: someone offers to add you as an authorized user, or you’re thinking about adding your teenager, spouse, or parent to your card. You pause because you’re not sure if this move will lift your score, drag it down, or do nothing at all. The doubt around being an authorized user and its credit impact stops many people from making a smart, easy choice.

Here’s the short answer: yes, it can affect your credit, but only if the card issuer reports the account to the credit bureaus.

Below, we’ll walk through both sides of this setup, the real risks, the hidden perks, and simple steps to keep your score safe.

Key Takeaways

This guide explains whether being an authorized user affects your credit, covering when accounts get reported, how utilization and payment history transfer to your file, and what happens if you are removed.

Core Facts:

- Authorized user accounts only affect your credit score if the card issuer reports the account to Equifax, Experian, and TransUnion; unreported accounts cause no score change at all.

- Payment history makes up about 35% of your FICO score, and account age contributes another 15%, so a well-managed authorized user account can improve both factors.

- Adding a high-balance authorized user can raise your utilization sharply; the article’s example shows utilization jumping from 10% to 60% after a $5,000 charge on a $10,000 limit.

- Experian excludes negative authorized user payment history from your report, while Equifax and TransUnion do include it, creating differences across your three credit reports.

- Being removed as an authorized user typically drops the tradeline from your report within one to two billing cycles, and scores can fall between 40 and 100 points as a result.

- You can be added as an authorized user without receiving the physical card, and some issuers charge a fee or run a soft credit pull when adding you.

Best for:

- People considering adding a spouse, teenager, or parent as an authorized user and want to understand the score impact first.

- Individuals with a thin or nonexistent credit file who are weighing authorized user status as a way to build history.

- Authorized users who want to know how removal or the primary’s spending habits could affect their own score.

Does Being an Authorized User Affect Your Credit at All?

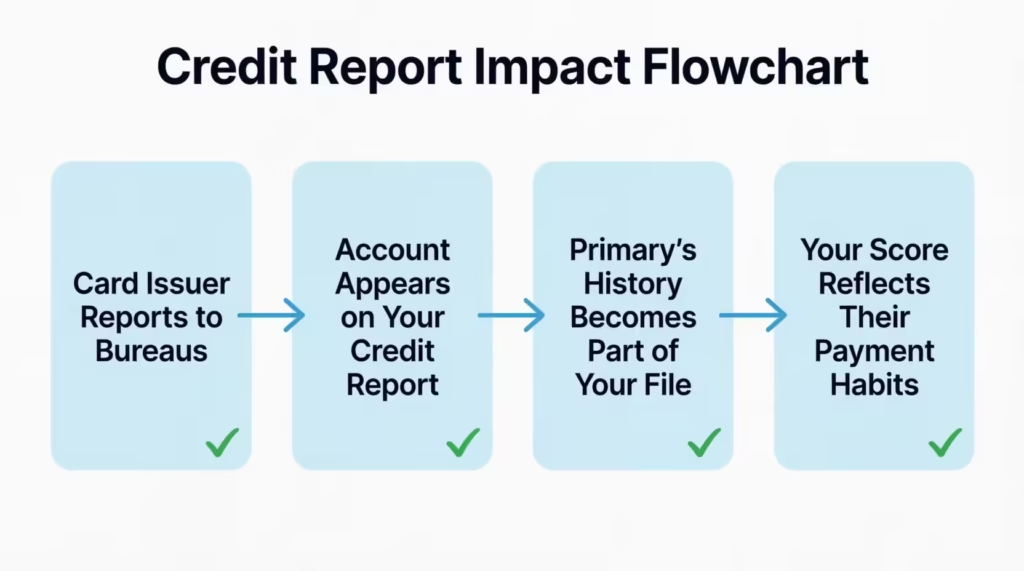

Authorized user status only shows up on your credit report if the card issuer sends that account to the credit bureaus. If it doesn’t get reported, nothing changes. Your score stays the same. So the first step is knowing whether the account will actually appear as a tradeline on your file.

Most big banks do report authorized user accounts. Chase, Citi, Bank of America, American Express, Wells Fargo, and Discover all pass this data to Equifax, Experian, and TransUnion.

Some smaller banks and credit unions skip this step. If you’re not sure, just call the card issuer and ask. The Consumer Financial Protection Bureau also confirms that credit bureau reporting is what drives any score change from this setup.

Once the account posts to your report, it can help or hurt your score. That depends on how the primary user handles the card. If nothing gets reported, you can skip the rest of this worry.

📌 Did You Know: Even if you never touch or swipe the card, the full account history can still land on your credit report. Reporting is tied to the account itself, not to who uses it.

Will Being an Authorized User Help My Credit?

Yes, being added to a well-managed card can boost your score. You inherit the account’s history the moment it starts reporting. That means the primary’s on-time payments, low balances, and long account age can all show up on your file. For someone with little or no credit, this can be a fast way to build a profile.

Experian data shows that authorized user tradelines can lift scores for people with thin files, sometimes by dozens of points. The exact bump depends on the card’s age, its credit utilization, and the primary’s payment history.

How Being an Authorized User Builds Credit History

Two big scoring factors get a lift here. First, payment history counts for about 35% of your FICO score. When the primary pays on time, those clean months land on your report too. Second, the card’s age adds to your average age of accounts, which shapes another 15% of your score. A card that’s been open for 10 years can pull your average age way up if your own accounts are new.

Both FICO Score 8 and VantageScore models include authorized user tradelines. So the boost shows up in most of the scores lenders check.

Can Adding an Authorized User Improve Credit With No Credit History

Yes, this is one of the fastest paths for someone with no file at all. A young adult, a new immigrant, or anyone starting from scratch can go from “no score” to a real FICO score in one or two billing cycles once the account posts. The card just needs to be old, paid on time, and kept at a low balance. Getting added to a fresh card with high usage won’t help much and could even hurt.

Will Adding an Authorized User Hurt My Credit?

For the primary cardholder, the risk is mostly about spending. Adding someone doesn’t directly ding your score. But if that person runs up the balance, your credit utilization jumps, and utilization is the second-biggest factor in your score.

Say your limit is $10,000 and you normally carry a $1,000 balance. That’s 10% utilization, which is healthy. If your new authorized user charges $5,000 in one month, your utilization jumps to 60%. Your score can drop 30 to 80 points until the balance goes back down.

You’re also on the hook for every dollar charged. The primary cardholder’s responsibility is total, even if the other person made the purchase. Missed payments, over-limit fees, and interest all fall on you.

⚠️ Mistake to Avoid: Don’t hand out the physical card to someone you can’t fully trust with money. Even a family member’s one bad month can wreck both your utilization and your relationship.

Will Being an Authorized User Hurt My Credit?

Yes, it can. If the primary starts missing payments or maxing out the card, those negatives can show up on your report too. Late payments stay on credit files for up to seven years, per the Fair Credit Reporting Act.

This is the biggest risk of accepting authorized user status. You have no control over the card. You can’t force the primary to pay on time. You can’t lower the balance. But their choices land on your file.

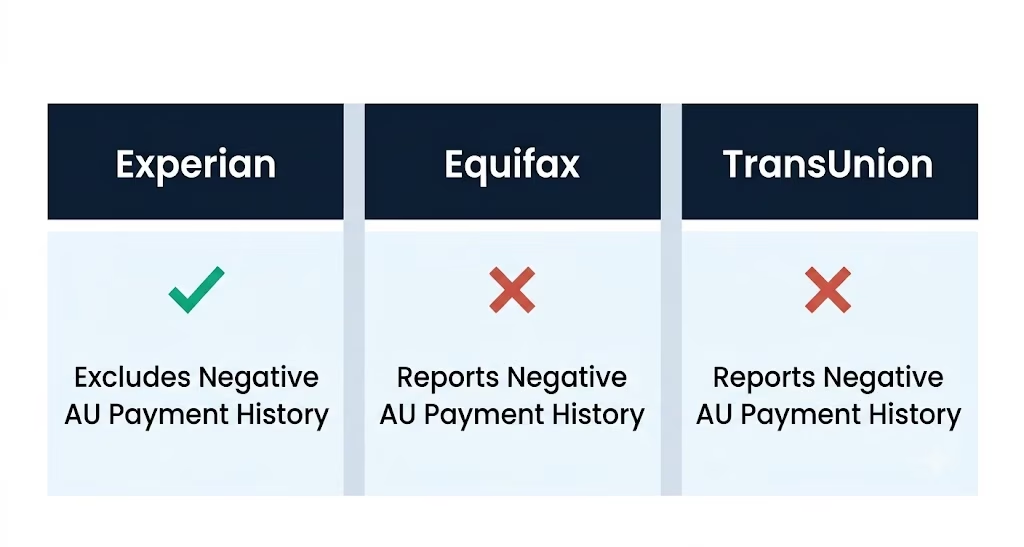

The Experian Exception for Negative Payment History

There’s one quirk worth knowing. Experian does not include negative authorized user payment history on the AU’s own credit report. So if the primary misses a payment, that late mark won’t show up in your Experian file, though the account itself still will.

Equifax and TransUnion don’t have this same rule. Late payments can appear on those reports. That’s why one score might look fine while another drops. If you’re worried about a primary who might slip up, check all three reports at AnnualCreditReport.com to see the full picture.

Does Being an Authorized User Affect Your Credit Utilization?

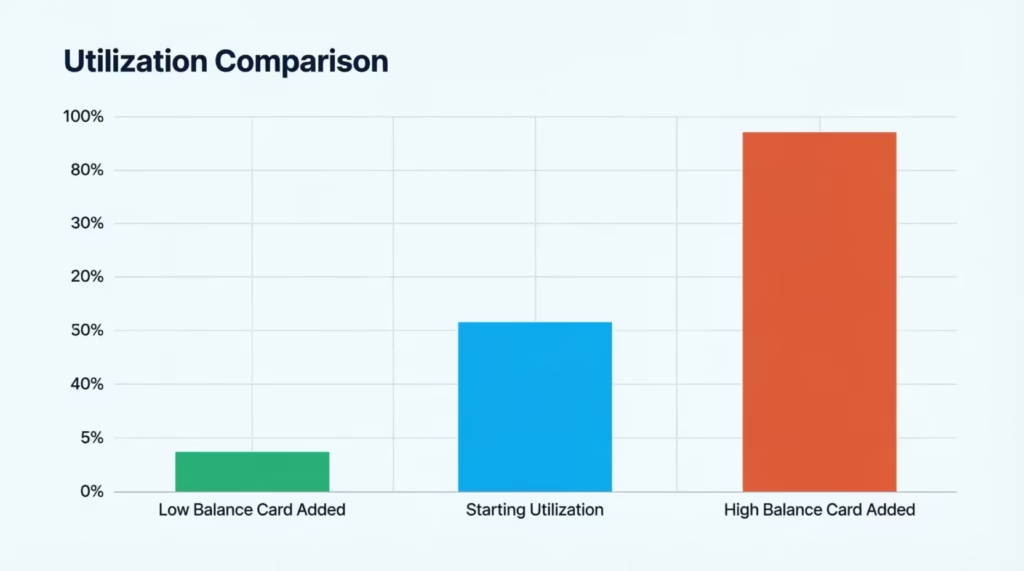

Yes, and this catches people off guard. When you become an authorized user, the card’s full balance and full credit limit both show up on your report. Your credit utilization ratio now includes that card.

Here’s how it plays out. Say your only card has a $2,000 limit and a $400 balance. Your utilization is 20%. Now you get added to a parent’s card with a $15,000 limit and a $500 balance. Your total limit becomes $17,000, and your total balance is $900. Your utilization drops to about 5%. That’s a big win.

But it works the other way too. If that parent’s card is maxed out at $14,000 out of $15,000, your combined utilization shoots up to nearly 88%. Your score will take a hit. Always check the card’s usage pattern before you accept AU status.

Does Being Removed as an Authorized User Affect Credit?

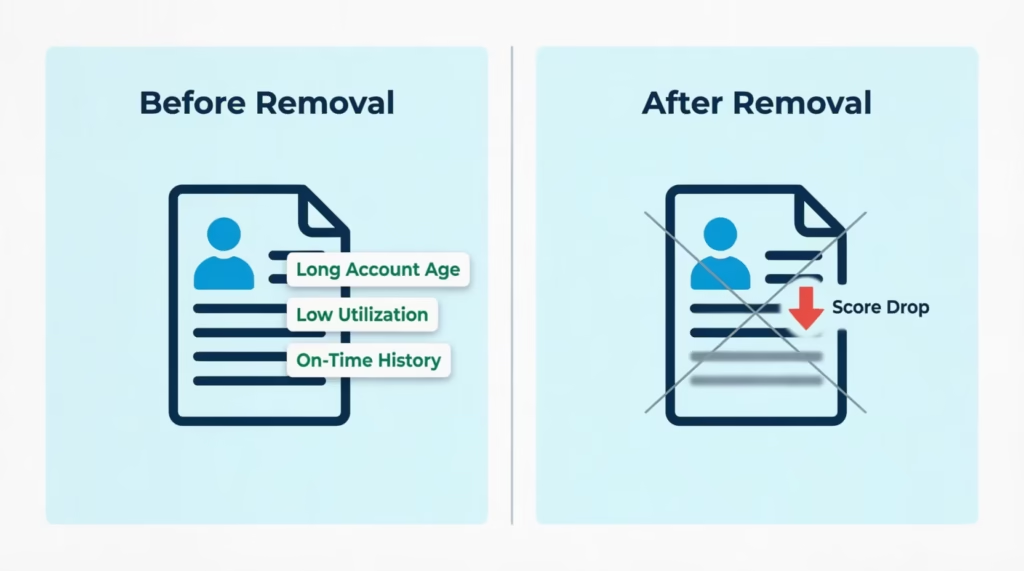

Yes, and the change can be sharp. Once you’re removed, the tradeline usually drops off your credit report within one or two billing cycles. Every good thing tied to that card- the long history, the on-time payments, the low utilization disappears with it.

For someone whose credit was built on that one account, the drop can be severe. Scores can fall 40 to 100 points. Your average age of accounts shrinks. Your total credit limit goes down, which pushes utilization up. If the account was your oldest, you lose that anchor.

This is why removal is one of the trickiest parts of the whole setup. Before you agree to be removed, or before you remove someone else, know what leaves the report with them.

💡 Pro Tip: If you built your file mostly on an authorized user account, open one or two of your own accounts before removal. That way, you have your own history in place when the AU tradeline drops off.

Is There a Downside to Adding a Friend as an Authorized User (and Not Giving Them a Card)?

Not really, and this is a common workaround. You can add a friend or family member as an authorized user without ever handing over the physical card. The account still gets reported. They still get the history boost. You keep full control of the actual card.

The main downside is administrative. Some issuers charge a fee to add an AU. American Express, for example, charges for extra Platinum cards but not for basic AU status on many cards. Some banks also do a soft pull on the AU, though this doesn’t hurt their score.

There’s also a small legal risk. If the friend later claims you owe them something or the relationship turns sour, having them tied to your account can get messy. Keep records. Know that you can remove them at any time with one phone call.

How to Protect Your Credit in an Authorized User Relationship

Both sides of this setup have simple ways to stay safe. The rules are different depending on which seat you’re in.

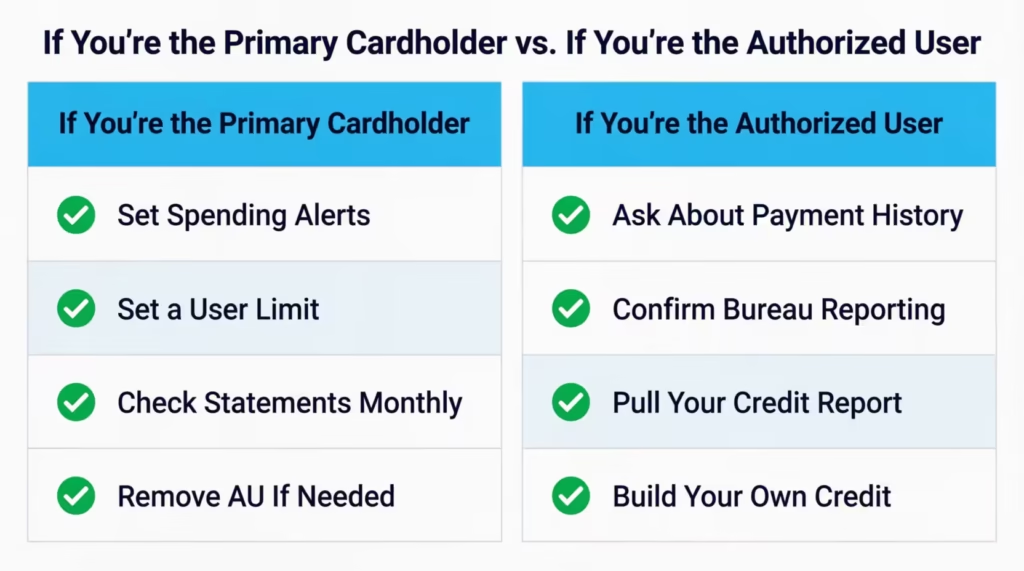

If You’re the Primary Cardholder

Keep control of the account no matter what. Try these steps:

- Set spending alerts through your bank’s app so you see every charge as it happens.

- Set a user spending limit if your issuer allows it. Many major banks now support this.

- Don’t hand out the physical card unless you fully trust the person and have talked about limits.

- Check your statement every month, not just the balance.

- Remove the AU right away if you see spending patterns you didn’t agree to.

If You’re the Authorized User

Your job is to check the account before and during the setup:

- Ask the primary about their payment history and current balance before you agree.

- Confirm the issuer reports AU accounts to all three bureaus.

- Pull your credit reports one or two billing cycles after being added to make sure the tradeline shows up.

- Watch the primary’s usage. If balances start climbing, ask to be removed before your score drops.

- Build your own credit alongside this account. A secured card or credit-builder loan gives you a safety net when the AU tradeline eventually leaves your file.

Frequently Asked Questions (FAQs)

Will being an authorized user affect my credit?

Yes, but only if the card issuer reports the account to Equifax, Experian, and TransUnion. Most major banks like Chase, Citi, and American Express report AU accounts, so the primary’s payment history and balance typically show up on your credit file within one to two billing cycles.

Is there a downside to being an authorized user?

The main downside is that you have no control over the account, so missed payments or a maxed-out balance from the primary can drag your score down too. Equifax and TransUnion will show these negative marks, though Experian excludes negative AU payment history from your report.

How much will my credit score go up if I become an authorized user?

The exact boost varies, but authorized user tradelines can lift scores for people with thin credit files by dozens of points. The gain depends on the card’s age, how low its balance is kept, and the primary’s payment history.

When should I stop being an authorized user?

Stop and ask to be removed if the primary’s balance starts climbing or their utilization creeps toward the card’s limit, since that spike can hurt your score too. It’s also smart to build your own credit accounts before removal, since scores can drop 40 to 100 points once the tradeline disappears from your report.

Why did my credit score drop when I was added as an authorized user?

Your score can drop if the primary’s card carries a high balance relative to its limit, since that utilization gets added to your own credit profile. For example, being added to a card that’s nearly maxed out can push your combined utilization close to 88%, which lowers your score.

How long does it take for an authorized user to show on a credit report?

Most authorized user accounts post to your credit report within one to two billing cycles after being added. It’s worth pulling your credit reports during that window to confirm the tradeline actually appears.

Does adding an authorized user affect the primary cardholder’s own credit score?

Adding an authorized user doesn’t directly change the primary’s score, but the primary stays fully responsible for every charge the AU makes. If the AU runs up the balance, the primary’s own utilization rises, which can lower the primary’s score until the balance is paid down.

Do I have to give an authorized user the physical card?

No, you can add someone as an authorized user without ever handing over the physical card. The account still gets reported, and the AU still gets the credit history benefit, while you keep full control of actual spending.

Wrapping Up

Being added as an authorized user can be one of the fastest, cheapest ways to build or boost credit, but only when the primary handles the card well. The account shows up on your report as a full tradeline, which means their payment history, utilization, and account age all become part of your score.

Based on the mechanics above, the most effective approach is to check the primary’s habits first, confirm the issuer reports to all three bureaus, and build your own accounts on the side.

If you know someone weighing this decision for a child, spouse, or parent, share this guide so they can protect their score before signing on.