You’ve decided to add a spouse, parent, or teen to your Citi credit card, but the menu inside your account isn’t obvious, and you’re not sure what info you’ll need or whether it’ll ding your credit. Getting stuck on a simple task like adding an authorized user to your Citi card can waste an evening and leave you second-guessing every click.

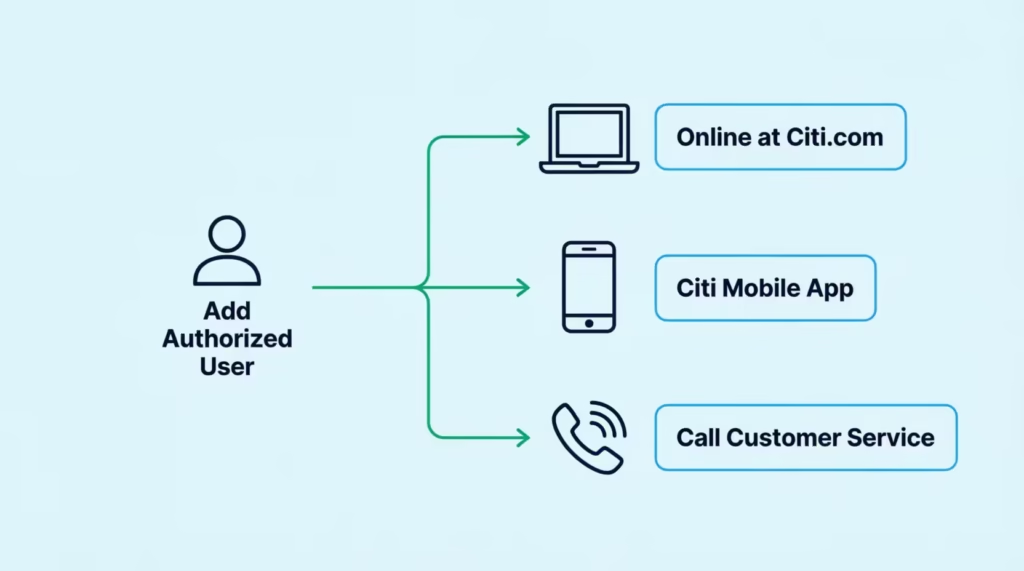

The quickest way is to log in at Citi.com or the Citi Mobile App. Then, open Services, choose Authorized Users, and enter the person’s name, date of birth, and address.

Below, we’ll cover age rules, including the Costco Anywhere Visa exception. We’ll also explain the credit impact and share tips to help you get it right the first time.

Key Takeaways

This guide explains how to add an authorized user to a Citi credit card online, through the mobile app, or by phone, including age rules, the Costco Anywhere Visa exception, and credit impact.

Core Facts:

- Adding an authorized user requires the Services then Authorized Users menu on Citi.com or the Citi Mobile App, or a call to 1-800-950-5114.

- You need the person’s full legal name, date of birth, Social Security number, and mailing address to complete the request.

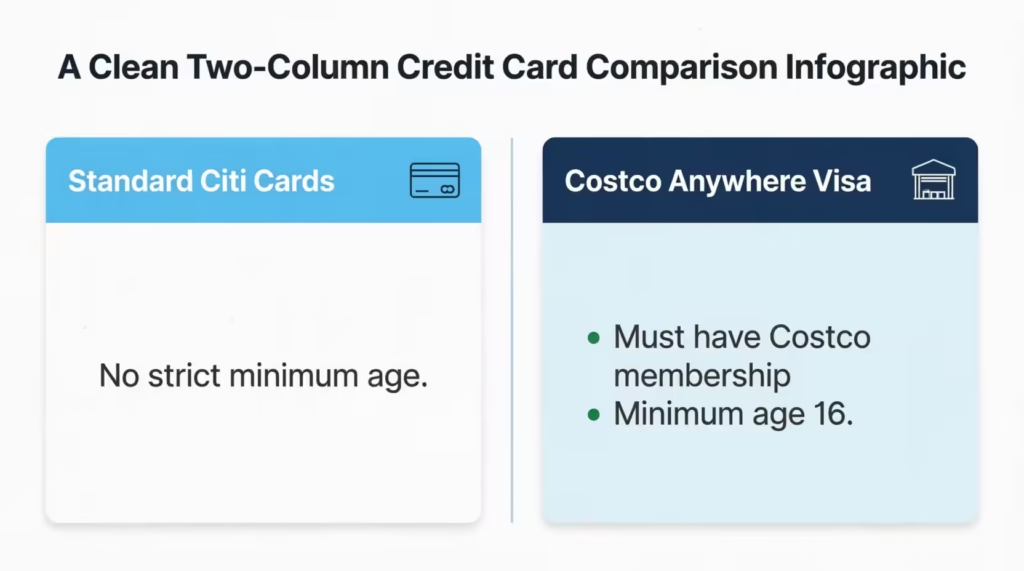

- Citi has no published minimum age for most cards, but the Costco Anywhere Visa requires the person to hold their own Costco membership with a minimum age of 16.

- Adding an authorized user does not trigger a hard inquiry on either person’s credit, since it is a tradeline extension rather than a new credit application.

- Citi reports authorized user activity to Equifax, Experian, and TransUnion only when it can match the person’s information to an existing credit file.

- The authorized user’s card typically arrives 7 to 10 business days after the request is approved, based on standard U.S. mailing timelines described in the article.

Best for:

- People deciding whether to add a spouse, parent, or teen as an authorized user on a Citi card.

- Cardholders trying to understand the Costco Anywhere Visa’s different age and membership rules.

- Anyone weighing the credit impact, including utilization and bureau reporting, before adding someone to their account.

What You Need Before You Start

Before you open the app or website, gather a few details. Having them ready keeps the process to under five minutes and prevents you from starting over.

You’ll need the following information for the person you’re adding:

- Full legal name as it appears on their government ID

- Date of birth (month, day, year)

- Social Security Number (Citi may ask for this, especially for adults you want reported to credit bureaus)

- Current mailing address where their card should be sent

- Phone number and email (optional but helpful for account alerts)

You should also confirm your own account is in good standing. As the main cardholder, you’re fully responsible for all charges made by the authorized user. So, check that the card isn’t overdue or over the limit before adding anyone.

One more thing to think about: decide in advance whether you want the new user to have online account access. Citi lets you toggle this on or off during setup, and it changes what the person can see and do with the account.

💡 Pro Tip: Text the person you’re adding and ask for their SSN and DOB in a secure way, like a password manager share link. Typing this from memory often leads to a mismatch that delays the card by a week.

How to Add an Authorized User Online at Citi.com

The web version gives you the fullest view of the process, which is helpful if it’s your first time. Follow these steps to add someone through your desktop or laptop.

Step 1: Go to Citi.com and sign in with your username and password. If you use two-factor login, have your phone nearby for the verification code.

Step 2: On the account dashboard, find the card you want to share. Click on that specific card so you’re viewing its details.

Step 3: Look for the Services tab in the top menu. On some accounts, it may be labeled Card Services or sit under a Manage Card dropdown.

Step 4: Inside Services, scroll to the section for account management and click Authorized Users. You may also see it as “Add an Authorized User.”

Step 5: Fill out the form with the person’s legal name, date of birth, Social Security Number, and mailing address. Double-check every field, since typos here can cause the card to bounce back.

Step 6: Choose whether to grant online account access. If you toggle this on, the authorized user can log in and view transactions, but they cannot change account settings or add other users.

Step 7: Review the terms, agree to the primary cardholder liability disclosure, and submit. You’ll get an on-screen confirmation and usually an email within a few minutes.

If a step doesn’t match your screen, Citi occasionally updates the layout. The core path stays the same: Services → Authorized Users → Add.

How to Add an Authorized User in the Citi Mobile App

The Citi Mobile App works well when you’re away from your computer. The screens are smaller, but the flow is nearly identical to the website.

Step 1: Open the Citi Mobile App on your phone. If you don’t have it, you can download it from the Apple App Store or Google Play.

Step 2: Sign in with Face ID, Touch ID, or your username and password.

Step 3: Tap the card you want to share from the home screen.

Step 4: Tap the Services icon, which usually appears at the bottom of the card details screen or inside a menu marked with three lines or dots.

Step 5: Scroll down and tap Authorized Users under the account management options.

Step 6: Tap Add and fill in the personal details on the mobile form.

Step 7: Set the permission toggle for online account access, review the terms, and submit.

The app confirms the request right away. You’ll see the new user listed under your account within a minute or two, though their physical card takes longer to arrive.

If the option seems missing in the app, log out and back in, or update the app to the latest version. Older versions sometimes hide newer features behind the web login.

How to Add an Authorized User by Phone

Some people prefer to talk with a real person, especially if the app isn’t cooperating or the details feel sensitive. Citi customer service can add an authorized user for you over the phone.

Call the number on the back of your card, or dial the general Citi cards support line at 1-800-950-5114. Representatives are available around the clock.

Before you call, have this ready:

- Your Citi card in front of you for verification

- Your Social Security Number and account details

- The authorized user’s full legal name, date of birth, SSN, and mailing address

The rep will verify your identity, ask for the new user’s info, confirm the permission settings, and read the disclosure about primary cardmember liability. The whole call usually takes 10 to 15 minutes.

Using the phone is the best way to confirm that the authorized user will be reported to the credit bureaus. It’s also useful if you’re adding someone to a Costco Anywhere Visa, which has additional rules detailed below.

Age Requirements for Citi Authorized Users

Citi doesn’t publish a strict minimum age for authorized users on most of its cards. Citi has no minimum age listed, while other issuers like Discover set 15 and U.S. Bank sets 16.

That means many parents can add a young child, teen, or college student to help them build a credit history early. However, since Citi may not always report authorized user activity to all three bureaus for younger users, the credit-building benefit isn’t guaranteed.

If credit history is your goal, add the young person as early as reasonable, then check their credit report a few months later to confirm the account shows up.

Also keep in mind that once your authorized user turns 18, they can apply for their own starter card. Adding them earlier as an authorized user gives them a head start on credit age of accounts, which is one of the factors in a FICO score.

Costco Anywhere Visa by Citi Exception

The Costco Anywhere Visa by Citi works differently. This card is tied to a Costco membership, and the authorized user rules follow Costco’s rules rather than Citi’s standard policy.

To be added as an authorized user on a Costco Anywhere Visa, the person must:

- Have their own Costco membership. Citi confirms this on its Costco Visa application page, which notes that anyone added must also be a Costco member.

- Meet Costco’s membership age minimum of 16. Costco’s member privileges page states that membership is available to individuals 16 and over.

So even though most Citi cards let you add a young child, the Costco Anywhere Visa effectively caps the minimum at 16 because of the membership tie. If you’re adding a spouse, they’ll usually already be on your household Costco membership as a free member, which qualifies them.

⚠️ Mistake to Avoid: Don’t try to add a family member to your Costco Anywhere Visa without confirming their Costco membership first. The request will be declined, and you’ll waste time re-doing it.

Does Adding an Authorized User Require a Hard Inquiry?

No. Adding an authorized user does not trigger a hard inquiry on either your credit or theirs. This is one of the biggest worries people have, and the answer is a clear no.

A hard inquiry happens when a lender checks your credit as part of a new loan or credit card application. That kind of check can shave a few points off your FICO score and stay on your report for up to two years. Citi’s own explainer on soft vs. hard credit inquiries confirms that hard pulls happen when you apply for credit, not when a name is added to an existing account.

Since an authorized user isn’t applying for credit and isn’t legally responsible for the debt, no lender needs to review their credit report. Citi typically doesn’t even run a soft inquiry in most cases. The new user’s information is added to your account as a tradeline extension, not as a new credit application.

This distinction matters because it removes one of the biggest reasons people hesitate. Adding your spouse, teen, or parent won’t cost you a single credit score point on the way in.

How Adding an Authorized User Affects Credit

While the act of adding someone doesn’t cost you any points, the ongoing account activity can affect credit, both yours and theirs. This is where things get more nuanced.

For you as the primary cardholder, the authorized user’s spending shows up on your statement and counts toward your credit utilization. If your teen puts $600 on a card with a $2,000 limit, your reported utilization jumps by 30 percent that month. High utilization can pull your FICO score down temporarily, so keep an eye on how much the added user charges each cycle.

For the authorized user, the impact depends on whether Citi reports the account to the credit bureaus for that specific user. Citi usually reports authorized-user activity to the three major bureaus: Equifax, Experian, and TransUnion. However, they only match it if the user’s info connects to an existing credit file. Citi reports authorized users only when it can match their credit profile to the card.

If the account is reported, the authorized user gets the full card history. This can boost credit quickly, especially if the card has a long history and low usage. If the account isn’t reported, being an authorized user does not affect their credit at all.

To check if the reporting worked, the authorized user can pull a free credit report from AnnualCreditReport.com about 30 to 60 days after being added. If the Citi card doesn’t show up, call customer service and ask them to confirm the reporting flag is turned on.

Does Being an Authorized User Affect Credit Utilization

Yes, especially on high-limit cards. Credit utilization is the percent of available credit you’re using, and it’s one of the biggest drivers of your FICO score.

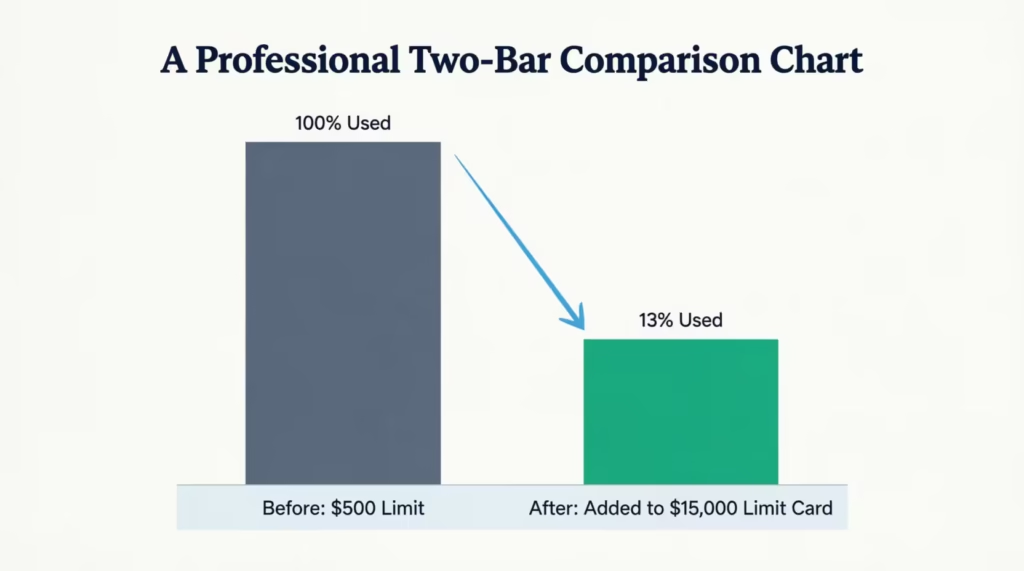

When an authorized user is added to a card with a high limit and low balance, their utilization ratio can drop overnight. For example, if a college student has a $500 secured card that’s maxed out, their utilization is 100%.

If their parent adds them to a Citi card with a $15,000 limit and a $1,500 balance, the student’s combined utilization drops to about 13%. That kind of change often bumps a FICO score up meaningfully within a month or two.

The reverse is also true. If the primary card is running high utilization, adding a young person to that card could hurt their score once the account reports. Before you add someone, check your usual monthly balance against the credit limit. A card that stays under 30 percent utilization is a strong candidate. A card that runs at 70 percent is not.

According to myFICO’s guide on authorized user accounts, newer FICO scoring models give authorized user accounts less weight than primary accounts, so the boost may be smaller than it once was. Still, for someone with a thin file or damaged credit, even a modest lift can matter.

What Permissions an Authorized User Has

An authorized user gets a card in their name that draws from your account. They can swipe, tap, use it online, and use it for recurring bills. But their access stops well short of full account control.

Here’s what an authorized user typically can do on a Citi card:

- Make purchases at any merchant that accepts the card

- Get their own card with their name on it

- Access online account details if you grant that permission

- View transactions, statements, and the current balance (with online access on)

- Dispute charges they made themselves

- Call customer service for basic help related to their card

Here’s what an authorized user cannot do:

- Add or remove other authorized users

- Close the account

- Request a credit limit increase

- Change the primary cardholder’s contact info or password

- Redeem rewards (in most cases; only the primary can redeem)

- Take on legal responsibility for the balance

That last point is the one to underline. As the primary cardmember, you are 100 percent responsible for every charge, whether you made it or your authorized user did. If they max out the card and stop returning your calls, you’re still the one on the hook with Citi. That’s why most experts recommend adding only people you trust deeply and communicate with often.

📌 Did You Know: You can set a spending alert on your Citi card that pings you every time a charge goes through above a set amount, like $100. This gives you real-time visibility into your authorized user’s activity without having to log in every day.

Can You Remove an Authorized User Later

Yes. Removing an authorized user is fast and simple, and you can do it any time without a fee or penalty.

You have three ways to remove someone:

- Online at Citi.com: Go to Services → Authorized Users, find the person’s name, and click Remove.

- In the Citi Mobile App: Follow the same path, tap the user’s name, and select Remove Authorized User.

- By phone: Call 1-800-950-5114 and ask the rep to remove them. This is often the fastest way to make sure the card is also deactivated right away.

Once removed, the authorized user’s card is canceled, and any pending charges they try to make will decline. Citi will update the credit bureaus. The account will eventually drop off the former user’s credit report, but this might take one or two billing cycles.

If you’re removing someone due to a dispute, ask Citi to freeze the card right away, before the removal is complete. This closes the risk window between when you make the request and when the card actually stops working.

How Long It Takes for the Authorized User’s Card to Arrive

Once you submit the request, the new card is usually printed and mailed within a few business days. Standard shipping in the U.S. typically puts the card in the authorized user’s hands in 7 to 10 business days after approval.

Here’s a rough breakdown of what happens after you submit:

| Timing | What’s Happening |

|---|---|

| Same day | Request is confirmed on your account |

| 1 to 2 business days | Card is printed and prepped for mailing |

| 3 to 5 business days | Card is in transit through USPS |

| 7 to 10 business days | Card arrives at the address on file |

A few things can slow this down:

- Wrong or old mailing address on the request form

- High-volume periods like the holidays

- New account status if the primary card was recently opened

- Postal service delays in the destination area

If it’s been over 10 business days and the card hasn’t arrived, call Citi customer service. Confirm your mailing address and ask for a replacement. Rush shipping is sometimes available for a fee, and in many cases the rep will waive it if the delay wasn’t your fault.

The authorized user can activate the card as soon as it arrives by calling the number on the sticker or using the Citi Mobile App.

Tips When Adding an Authorized User to a Citi Card

A few small choices at setup can save you headaches later. Use these tips to make the arrangement work well for both people.

Start with clear ground rules.

Before the card even arrives, talk about what the authorized user can buy, a monthly spending cap, and how they’ll let you know before a big purchase. A short text conversation up front prevents most surprises.

Keep utilization low.

Even after adding a trusted user, aim to keep the combined monthly balance under 30 percent of the credit limit. This protects your FICO score and, if the account reports, theirs too. High credit utilization is one of the fastest ways to lose points on a card that could otherwise be helping.

Turn on transaction alerts.

In the Citi app, go to Alerts and enable notifications for every purchase, or for purchases over a set dollar amount. You’ll know within seconds when the authorized user swipes the card. This is far more effective than checking your statement once a month.

Confirm reporting for credit-building.

To help someone build credit, call Citi after 60 days. This checks if the account is reported to Equifax, Experian, and TransUnion for that user. Pull a free report from AnnualCreditReport.com to verify.

Review the setup annually.

Life changes, and the person you added five years ago may not be the right fit today. Do a quick review each year to decide whether to keep, remove, or adjust the arrangement. Removing someone takes two minutes and avoids issues down the road.

Consider timing for big goals.

If the authorized user is applying for a mortgage or car loan soon, adding them a few months in advance gives the credit boost time to show up. Adding them the week before a big application is usually too late.

Following these small steps turns a simple card addition into a real credit-building or convenience tool for the whole family.

Frequently Asked Questions (FAQs)

Can I add an authorized user after I get my credit card?

Yes, you can add an authorized user any time after opening your account. Just log in at Citi.com or the Citi Mobile App and go to Services, then Authorized Users.

Will my son build credit if I add him to my credit card?

It depends on whether Citi reports the account to the bureaus for his profile, since Citi only reports when it can match his info to an existing credit file. If it reports, he gets the full card history, which can boost a thin credit file quickly.

Is there a downside to adding an authorized user?

The biggest risk is that you stay 100 percent responsible for every charge they make, even if they stop communicating with you. Their spending also counts toward your credit utilization, so a big purchase can temporarily lower your score.

Can I add someone to my credit card with poor credit?

Yes, Citi doesn’t check the authorized user’s credit before adding them, and no hard or soft inquiry is run on their file. Adding someone with poor credit won’t hurt your score, but their spending will still count against your utilization.

Will my credit limit increase if I add an authorized user?

No, adding an authorized user doesn’t change your credit limit. Only the primary cardholder can request a credit limit increase.

Can my wife use my Costco Citi card?

She can use it as an authorized user, but she must have her own Costco membership first since the Costco Anywhere Visa follows Costco’s rules instead of Citi’s standard policy. If she’s on your household membership as a free member, she already qualifies.

How many authorized users can be on a Costco Citi card?

The article doesn’t state a specific limit on Costco Anywhere Visa authorized users.

Does adding an authorized user help build their credit?

Only if Citi reports the account activity to Equifax, Experian, and TransUnion under their name. If it isn’t reported, being an authorized user does not affect their credit at all.

Can I add my husband as an authorized user on my credit card?

Yes, you can add a spouse the same way as anyone else, through Services, then Authorized Users on Citi.com or the app. You’ll need his legal name, date of birth, Social Security number, and mailing address.

Is it better to have a joint credit card or authorized user status?

An authorized user gets a card and can spend, but carries no legal responsibility for the balance, unlike a joint account holder. The article doesn’t compare joint accounts directly, but notes the primary cardholder alone remains fully liable for authorized user charges.

Wrapping Up

Adding someone to your Citi card is easy. First, gather their info. Then, go to Services → Authorized Users on Citi.com or the Citi Mobile App. You can also call 1-800-950-5114 for help. You won’t face a hard inquiry. Most cards don’t have a strict minimum age, except for the Costco Anywhere Visa, which needs a Costco membership.

The card typically arrives in 7 to 10 business days. Add a trusted person to a low-utilisation card. Then, check the bureau reporting after 60 days.

This is the best approach based on the credit and liability rules mentioned. If you know a parent helping a teen build credit, or a spouse merging finances, share this guide so they get it right the first time.