I know how frustrating it feels to hit your Citi card limit right when a big expense pops up, or to watch your credit utilization climb and drag your score down. Maybe you’ve thought about asking for a Citi credit card limit increase, but you’re worried a denial or a hard pull will make things worse.

Here’s the good news: you can request one online in under three minutes, and in most cases Citi uses a soft pull that won’t touch your score.

Keep reading for the exact click path, the smart amount to ask for, and what to do if you get denied.

Key Takeaways

This guide explains how to request a Citi credit card limit increase online, by phone, or automatically, including how much to ask for, soft-pull versus hard-pull risk, and what to do after a denial.

Core Facts:

- Online credit limit increase requests are usually decided within 30 seconds, while requests needing manual review take 7 to 10 business days.

- Citi reviews accounts for automatic increases every six to twelve months using a soft pull, which does not affect your FICO score.

- The recommended request amount is 10% to 25% above your current limit; requests over 50% often trigger manual review and a hard pull.

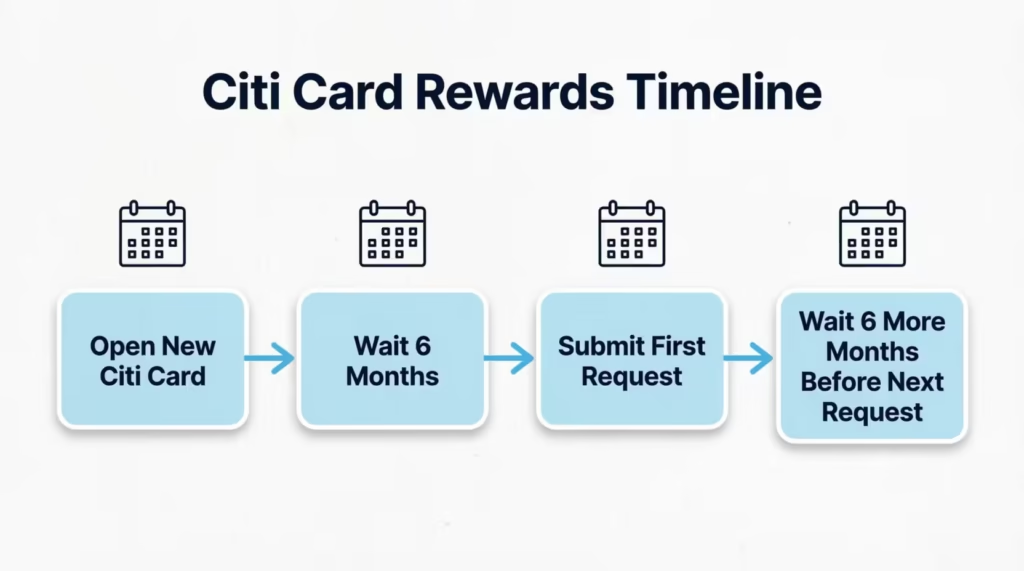

- Wait at least six months after opening a new Citi card before your first request, and six months between requests on the same card.

- Common denial reasons include an account under six months old, a recent late payment, high utilization, and insufficient income for the requested amount.

- Under the Fair Credit Reporting Act, Citi must send an adverse action letter with specific denial reasons within 30 days of a denial.

Best for:

- Cardholders who want to raise their credit limit without triggering a hard inquiry on their credit report.

- People who were recently denied a Citi credit limit increase and want to understand why and how to reapply successfully.

- Citi cardholders deciding how large of an increase to request without appearing risky to underwriting.

How to Request a Citi Credit Limit Increase

If you’ve been sitting there wondering where the button even is, you’re not alone. Citi hides the credit line request tool a few clicks into your account. The wording is a bit different on the desktop site and the mobile app. Once you know the path, the whole thing takes less than five minutes.

Log in to your account at citi.com or open the Citi Mobile app on iOS or Android. From the main dashboard, tap Services or Card Services, then look for Credit Limit Increase Request. Some card types show it under “Manage Card” instead. If you can’t find it, try the search bar inside the app and type “credit limit.”

Before you hit submit, Citi will ask you to update three key numbers:

- Total annual income (include salary, side income, and, if you’re 21 or older, income from anyone who regularly deposits money into your account)

- Monthly housing or rent payment

- Requested new credit line (a specific dollar amount, not a percentage)

The form takes about two minutes to fill out. Citi’s system usually gives you an answer on screen within 30 seconds. If it needs a manual review, you’ll get a decision by mail or secure message within 7 to 10 business days.

💡 Pro Tip: Submit your request after your statement closes but before your next payment posts. Citi’s system tends to review a “clean” account snapshot more favorably than one showing a heavy mid-cycle balance.

Requesting by Phone

Some people just prefer talking to a real person, especially if the online form denied them or if the card has a special status like secured. Calling can also help when you want to explain a recent income jump that isn’t fully reflected in your account yet.

Dial Citi’s general cards line at 1-800-950-5114. You can also call the number on the back of your card. Once connected, say “credit limit increase” to the automated system, and it’ll route you to the right department.

Have these details ready before you dial:

- Your current annual income and monthly housing cost

- The specific new limit you want (not a vague “more, please”)

- A short reason for the request, like an upcoming home repair, a wedding, or planned business travel

- Your last two payment dates and amounts, in case the rep asks

The best time to call is Tuesday through Thursday, mid-morning. Wait times are shortest, and reps have more flexibility to escalate borderline cases before the end-of-day rush.

Does Citi Increase Credit Limits Automatically

Yes, and this is the safest path to a bigger limit because it doesn’t touch your credit score. Citi runs periodic account reviews, usually every six to twelve months, to see which cardholders have earned a bump. These reviews use a soft credit inquiry, which is invisible to lenders and has zero impact on your FICO score.

Citi looks for a small set of positive signals before offering an automatic increase:

- On-time payments for at least the last six to twelve months

- Responsible card use, meaning you’re using the card but not maxing it out

- A stable or rising income on file (this is where updating your profile matters)

- Aging of the account, typically six months or more since opening

You’ll usually find out through an in-app notification, a letter, or an email that says something like “Good news, we’ve increased your credit line.” No action is required on your end. The new limit shows up in your account the same day.

If you’ve never received one, that doesn’t mean Citi has forgotten you. It often means the system doesn’t have current information to work with. Keeping your income and employment updated (covered later in this article) is the single easiest way to become eligible for these silent bumps.

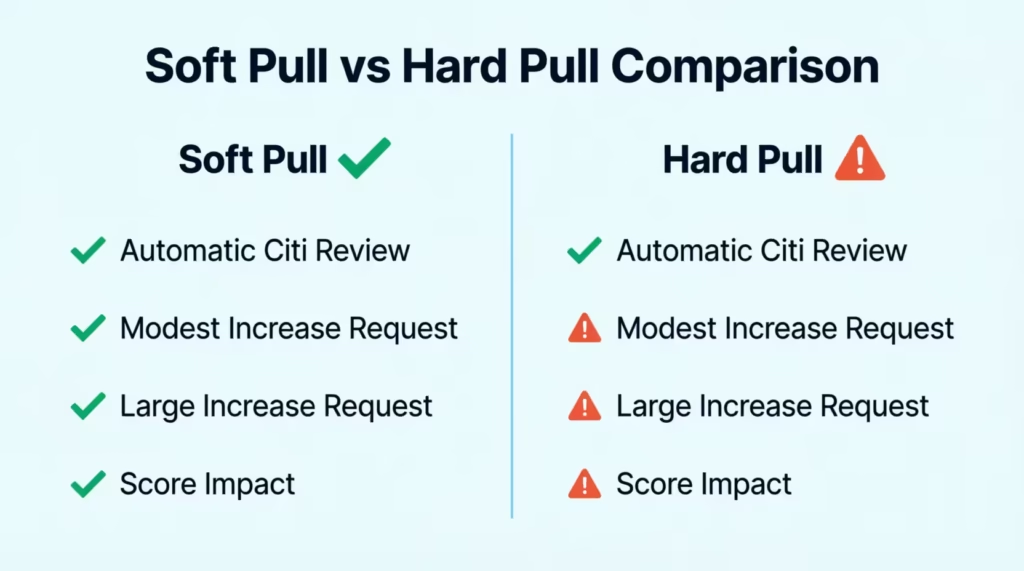

Hard Pull vs. Soft Pull: What Triggers Each

This is the part most people worry about, and honestly, it’s the right thing to worry about. A hard inquiry can lower your credit score by a few points. It stays on your credit report for two years, but its effect on your score lessens after about twelve months. A soft inquiry does neither.

| Scenario | Type of Inquiry | Score Impact |

|---|---|---|

| Citi offers you an automatic increase | Soft pull | None |

| You request a modest increase and Citi has recent data on you | Usually soft pull | None |

| You request a very large increase (like doubling your limit) | Often hard pull | Small dip, recovers in months |

| You haven’t updated income in over a year | May trigger hard pull | Small dip possible |

| Your account is under six months old | Often declined or hard pull | Small dip if approved |

Here’s the important part: Citi does not always disclose the pull type before you submit. That’s why the phone route is useful. You can ask the representative directly, “Will this request be a soft pull or a hard pull?” If they say hard, you can decline right there and try again in a few months after strengthening your file.

⚠️ Mistake to Avoid: Submitting a credit line increase request right after applying for another new card. Multiple hard inquiries within 30 days can compound the score damage, and Citi’s system may auto-deny the request because your recent inquiry list looks risky.

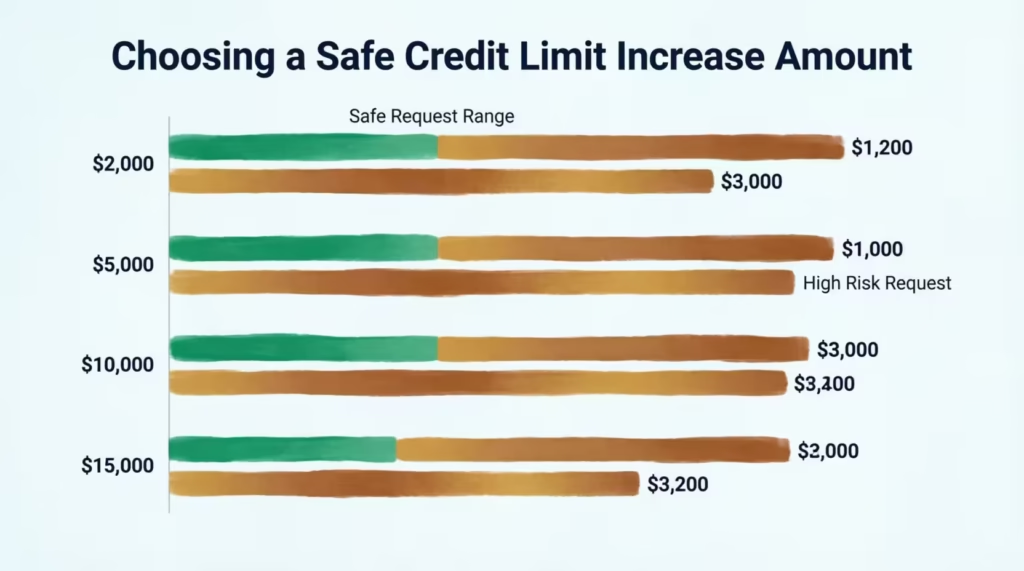

How Much of a Credit Limit Increase to Request

The sweet spot most cardholders miss is asking for 10% to 25% above your current limit. That range signals confidence without setting off Citi’s risk filters. Ask for too little, and you’ll get it, but you’ll be back in six months. Ask for too much and the system flags you as a spending risk.

Here’s what those numbers look like in practice:

| Current Limit | Reasonable Request (10-25%) | High-Risk Request (over 50%) |

|---|---|---|

| $2,000 | $2,200 to $2,500 | $4,000+ |

| $5,000 | $5,500 to $6,250 | $10,000+ |

| $10,000 | $11,000 to $12,500 | $20,000+ |

| $15,000 | $16,500 to $18,750 | $30,000+ |

Why does doubling backfire? Citi’s underwriting model looks at your requested limit. It compares this to your income, current debt, and how your credit lines have grown over time. Jumping from a $5,000 limit to $15,000 at once is unusual. So, the system either denies the request or sends it for manual review. This review nearly always leads to a hard pull.

If you genuinely need a much larger limit, ask for a moderate increase now, wait six months, then request another. Two 20% jumps compound to roughly a 44% total increase, and both can happen with soft pulls if your account looks healthy.

📌 Did You Know: Citi’s internal soft-pull threshold shifts based on your card type. Reddit and myFICO users say that Double Cash and Custom Cash cardholders often get soft pulls for small requests. In contrast, Simplicity and older store-branded cards usually trigger hard pulls more frequently. Choose your request size with that in mind.

What Citi Looks at When Reviewing Your Request

Understanding the checklist Citi runs through will help you time your request for maximum success. The reviewer, whether human or algorithm, weighs the same handful of factors every time.

Payment history carries the most weight. Even one late payment in the last twelve months can sink your request. Citi wants to see at least six, ideally twelve, consecutive on-time payments before considering a bump.

Account age matters more than most people realize. Citi rarely approves increases on accounts younger than six months, and the sweet spot is one to three years of history on the specific card you’re asking about.

Credit utilization ratio on the Citi card and across all your cards is scrutinized. If you’re carrying a balance close to your existing limit, Citi may read that as financial stress rather than a good reason to lend you more. Consumer Financial Protection Bureau guidance suggests keeping utilization below 30%, and Citi’s underwriters use a similar internal threshold.

Debt-to-income ratio (DTI) compares your monthly debt payments to your monthly income. A DTI above 40% often triggers a denial or a smaller-than-requested increase.

FICO score trend matters as much as the number itself. A 720 score that’s climbing looks better than a 750 score that’s dropping. Experian data shows the average U.S. FICO score sits at 713 in 2025, so scores in that range or higher are generally in safe territory for a modest Citi increase.

Recent credit activity is the final filter. Too many new accounts, new inquiries, or new balances in the last six months signal risk.

Update Your Income and Housing Information First

This is the highest-leverage move you can make before requesting an increase, and almost nobody does it. Updating your income triggers no hard pull, takes about 60 seconds, and can qualify you for both automatic increases and larger manual ones.

To update in the Citi Mobile app:

Tap Profile > Personal Information > Income and Housing. On desktop, go to Profile & Settings > Contact & Personal Information > Update Financial Information.

Please enter your total annual income, including any extra income you have. Also, share your employment status and your monthly rent or mortgage payment. Save the changes.

Wait 24 to 48 hours for the update to filter into Citi’s underwriting system, then submit your credit limit increase request. This one-two sequence, updating income before requesting, is the single most effective tactic experienced cardholders use.

How Often You Can Request a Citi Credit Limit Increase

Timing is everything with Citi, and asking too soon is a top reason for denials. Citi has two specific waiting rules you need to respect.

Rule 1 — Wait at least six months after opening a new Citi card before your first credit limit increase request. Some sources say four months is enough, but six is the safer floor because Citi’s system flags accounts under six months as “unseasoned.”

Rule 2 — Wait at least six months between requests on the same card. If you were approved recently, this window resets from the approval date. If you were denied, it resets from the denial date, and you should also wait six months to give your credit profile time to improve before trying again.

Some cardholders have had success with requests every 91 days. However, this varies a lot and can lead to hard pulls or auto-denials. The six-month rhythm is the pattern that reliably produces soft-pull approvals.

If you have multiple Citi cards, you can request increases on each one, but stagger them by at least 30 days. Submitting requests for two cards on the same day can signal financial trouble to the underwriting system. This often leads to hard pulls on both cards.

What to Do If Your Citi Credit Limit Increase Is Denied

A denial stings, but it isn’t the end of the road. In fact, the denial letter itself is a roadmap for getting approved next time, if you know how to read it.

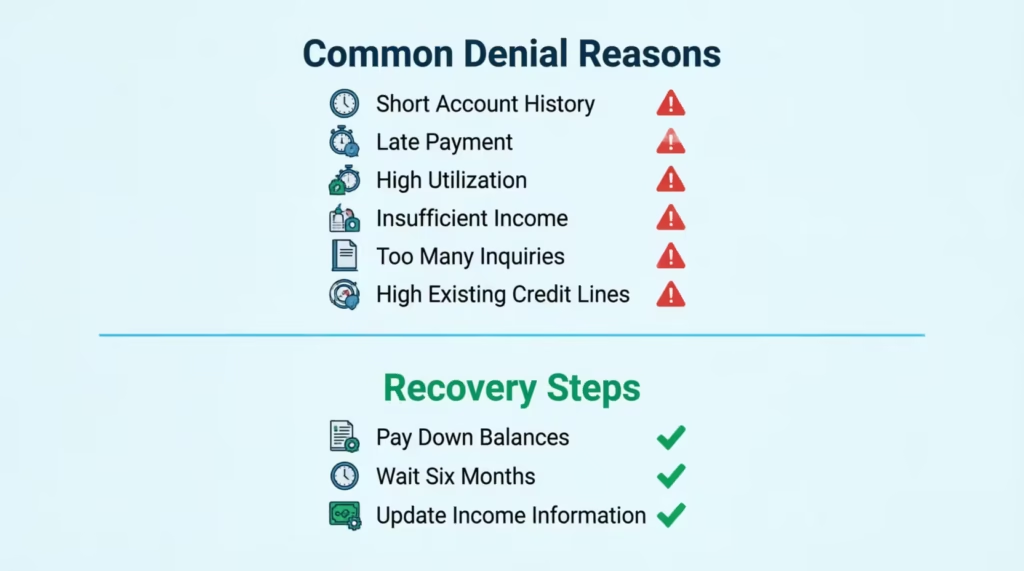

The most common denial reasons Citi cites are:

- Insufficient account history (account too new or too little activity)

- Recent late or missed payment on any account, not just Citi

- High credit utilization across your cards

- Income does not support the requested increase

- Too many recent credit inquiries or new accounts

- Existing Citi credit lines are already high relative to your income

Once you know the reason, the recovery plan writes itself. Pay down balances to get utilization below 30% (and ideally below 10% on the Citi card itself). Wait six months without opening new accounts. Update your income if it changed. Then try again.

Do not immediately submit another request after a denial. Citi’s system often auto-denies a second request within 30 days without review. Each denial can lead to a new hard pull if your file has changed.

Finding Out Why You Were Denied

Federal law is on your side here. Under the Fair Credit Reporting Act, Citi must send you an adverse action letter within 30 days of a denial. This letter should include the specific reasons for the denial. Watch your mail and secure inbox on citi.com for it.

If the letter’s reasons feel vague, call 1-800-950-5114 and ask for the credit analyst team. Say plainly: “I was denied a credit limit increase on [date]. Can you tell me the specific factors that led to that decision, and what would need to change for approval?” Representatives can often view notes not included in the letter. These notes may show the internal risk score or the specific credit bureau data point that led to the denial.

If your denial was based on incorrect credit report information, request a free copy of your credit report through AnnualCreditReport.com and dispute the error before reapplying.

Increasing the Limit on a Citi Secured Card

The Citi Secured Mastercard works differently from Citi’s regular cards, and the “increase” path is not a manual request. You have two options.

Option 1 — Add to your security deposit. With a secured card, your credit limit equals your deposit (up to the card’s cap). To raise your limit, you add money to the deposit. Call 1-800-950-5114 and ask to increase your secured deposit.

The new funds usually clear within a few business days, and your limit rises by the same amount. This is the fastest way to get more spending room on a secured card.

Option 2 — Graduate to an unsecured card. Citi reviews Secured Mastercard accounts for graduation after about 18 months of responsible use, according to the Citi Secured Mastercard product page. If you’re approved, you’ll get your deposit back.

Your account then changes to an unsecured Citi card, usually with a higher limit and maybe rewards. Graduation isn’t guaranteed. Cardholders who don’t graduate at 18 months typically stay on the secured card for another 12 months before another review.

To improve your graduation chances, use the card every month, keep utilization under 30% of the deposit-based limit, and pay in full by the due date. Never miss a payment. One missed payment can push graduation back another year.

Benefits and Risks of a Higher Citi Credit Limit

A higher limit is not automatically a good thing. It’s a tool, and like any tool, it helps or hurts depending on how you use it.

The biggest benefit is the boost to your credit utilization ratio. If you’re carrying a $2,000 balance on a $5,000 limit, that’s 40% utilization, which drags on your score. Raise the limit to $8,000, and the same balance drops to 25% utilization.

Your FICO score often jumps within one to two billing cycles. Experian’s 2024 State of Credit Cards report shows the average U.S. credit utilization rate sits at 29%, so pushing yours below that puts you in stronger territory than most Americans.

Other real benefits include:

- More spending power for planned large purchases, emergencies, or business expenses

- Better approval odds on future credit applications, because lenders see more available credit

- A higher “safety cushion” in your financial life, without needing to actually use the extra credit

- Improved chances of automatic future increases, since Citi rewards cardholders who use their limits responsibly

The risks, though, are just as real. A higher limit tempts many people to spend more, which defeats the purpose of the increase. If a $3,000 limit was keeping you disciplined, an $8,000 limit can quietly become a debt trap.

Avoiding the Overspending Trap

Discipline is what separates a helpful limit increase from a financial mistake. A few simple habits keep you on the right side of that line.

Pay the statement balance in full every month. Not the minimum, not “as much as you can.” The full statement balance, on or before the due date. This is the only way to use a higher limit without paying interest.

Set a personal spending ceiling that ignores the new limit. If your budget said $800 a month on the card before the increase, keep it at $800 after. The extra credit is a safety cushion, not a spending permission slip.

Watch your balance mid-cycle, not just at the statement date. Log in weekly and check what you’ve charged. This alone catches most overspending before it becomes a problem.

Turn on alerts. In the Citi app under Alerts, set a text or push notification for any single purchase over $100 and for when your balance hits 25% of your new limit. These small nudges keep the higher ceiling from becoming invisible.

Never treat available credit as savings. Available credit is borrowed money you haven’t borrowed yet. Real savings sit in a bank account, earning interest, not in a credit line that costs you interest the moment you touch it.

Frequently Asked Questions (FAQs)

Will Citi increase my credit limit automatically?

Yes, Citi reviews accounts every six to twelve months and can raise your limit without you applying. This uses a soft credit pull, so it won’t affect your FICO score, and the new limit appears in your account the same day you’re notified.

Why won’t Citi increase my credit limit?

Common reasons include an account under six months old, a recent late payment, high credit utilization, or income that doesn’t support the requested amount. Too many recent credit inquiries or already-high existing limits relative to income can also trigger a denial.

How long does a Citibank credit limit increase take?

Most online requests get a decision within 30 seconds of submitting the form. If your request needs manual review, expect an answer by mail or secure message within 7 to 10 business days.

How often can I request a credit limit increase with Citi?

Wait at least six months after opening a new Citi card before your first request, and at least six months between requests on the same card. If you have multiple Citi cards, stagger increase requests by 30 days to avoid triggering hard pulls on both.

Does requesting a Citi credit limit increase hurt my credit score?

It depends on the size of your request. Modest increases (10-25%) with recent income data on file usually trigger only a soft pull, while requesting a much larger jump, like doubling your limit, often results in a hard inquiry that can cause a small, temporary score dip.

How much of a credit limit increase should I request from Citi?

Ask for 10% to 25% above your current limit. This range signals responsible growth without triggering Citi’s risk filters, while requests over 50% of your current limit often get flagged for manual review and a hard pull.

Can I increase the limit on a Citi Secured Mastercard?

Yes, but not through the standard request form. You can add more money to your security deposit to raise your limit immediately, or wait about 18 months for Citi to review your account for graduation to an unsecured card.

What information does Citi look at when reviewing a credit limit increase request?

Citi weighs your payment history, account age, credit utilization, and debt-to-income ratio most heavily. It also checks your FICO score trend and any new credit inquiries or accounts opened in the last six months.

Wrapping Up

Getting a Citi credit card limit increase is easier than you might think. Just follow these steps:

- Update your income first.

- Request a small increase of 10-25%.

- Wait six months since your last request.

- Know your card’s soft-pull habits before you apply.

Based on the way Citi weighs payment history and account age, the most effective approach is patience over aggression. Waiting a few extra months usually beats forcing a large request that ends in a hard pull.

If a friend or family member is worried about hurting their credit while asking for more spending room, share this guide with them. It could save them a real ding on their credit report.