We know the feeling. You want the Costco Anywhere Visa Card for the gas rewards and travel perks, but you’re worried about a hard inquiry hurting your score if you get denied.

Guessing your Costco credit card approval odds without real data is stressful, especially when a wrong move can cost you points and a Costco membership fee.

Good news: you can estimate your chances with high accuracy before you ever hit “apply.” Below, we’ll walk you through the exact score range, the hidden factors Citi checks, and what to do if the answer is “not yet.”

Key Takeaways

This guide explains how to estimate approval odds for the Costco Anywhere Visa Card before applying, covering the realistic FICO score range, the non-score factors Citi reviews, a self-assessment checklist, and what to do after a denial.

Core Facts:

- A realistic FICO score bar for approval sits around 720 to 740 or higher, with scores below 670 facing very low odds and often instant denial.

- Citi does not offer a soft-pull pre-qualify tool for this card, so every application results in a full hard inquiry with no way to test approval risk-free.

- Citi weighs recent credit activity heavily, and cardholders report denials tied to having 6 or more inquiries in the last 6 months, a pattern nicknamed the “Citi 6/6 pattern.”

- Recommended credit utilization is under 10% for ideal odds, under 30% is workable, and utilization above 70% often triggers denial on its own.

- A denial typically causes only a 3 to 5 point score dip that recovers within a few months, and does not affect an existing Costco membership since memberships are fully refundable at any time.

- If denied, applicants can call Citi’s reconsideration line at 1-800-763-9795 for a manual review, and should wait at least 6 to 12 months before reapplying.

Best for:

- Applicants who want to self-check their approval readiness before triggering a hard inquiry.

- People who have already been denied and want to understand reconsideration options or reapplication timing.

- Readers comparing the Costco Anywhere Visa personal card against the Costco Anywhere Visa Business card for approval odds.

What Credit Score Do You Actually Need for the Costco Anywhere Visa Card

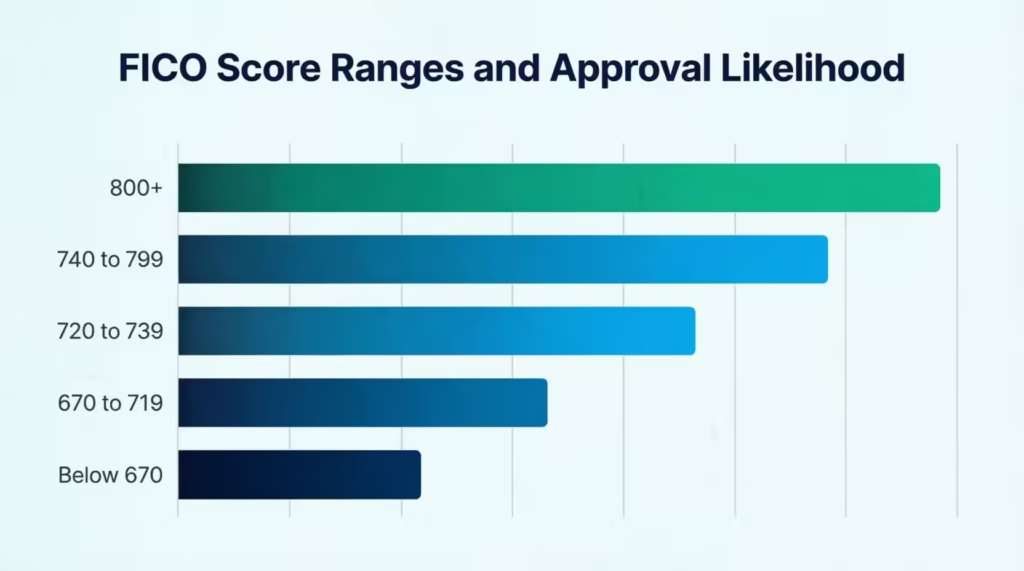

Citi does not publish an official minimum score for this card. That silence is what confuses most applicants. Based on approval data reported by cardholders and card review sites, the realistic bar sits around 720 to 740 or higher on the FICO scale.

The card is marketed to people with “excellent” credit. FICO defines excellent as 800 and above, but “very good” starts at 740. In practice, Citi tends to approve applicants who land in the upper “very good” range or better. A score of 700 might squeak through with a strong profile. A score below 680 will almost always get an instant denial.

Here is a quick view of how FICO ranks scores and how each range lines up with your realistic Costco Anywhere Visa approval chances:

| FICO Range | FICO Label | Realistic Odds for the Costco Visa |

|---|---|---|

| 800+ | Exceptional | Very high |

| 740 to 799 | Very Good | Strong |

| 720 to 739 | Good (upper) | Moderate to strong |

| 670 to 719 | Good (lower) | Low to moderate |

| Below 670 | Fair or Poor | Very low |

Your score is pulled from one of the three major bureaus. Citi most often pulls from Equifax, but reports from Experian and TransUnion happen too, depending on your state. You can check your FICO Score for free through your bank, Experian’s free score tool, or myFICO.

Why Your Credit Score Alone Doesn’t Decide Approval

Here’s the part most articles skip. Citi does not run your score through a simple pass-or-fail gate. They look at your whole credit profile. That’s why people with an 800 score still get denied, and why some folks with a 710 get an instant “yes.”

Think of it like a job interview. Your score is your resume. It gets you in the door. But the interview itself, meaning your full profile, decides if you get the offer. Citi looks at several factors: how many new cards you’ve opened, your current debt, how long you’ve had credit, and if you have a Citi account in good standing.

Real example: David, a marketing manager at a tech startup, had an 805 FICO score. He was denied because he’d opened four new cards in the last 12 months. Sarah, a small business owner, was approved with a 722 score because her utilization was under 5% and she had no new inquiries in two years. Same card. Different profiles. Different results.

So if you’ve been told “your score is fine, you’re good to go,” take that with caution. The score matters, but it is not the finish line.

The Non-Score Factors That Actually Drive Citi’s Decision

Once your score clears the basic threshold, four other factors do the heavy lifting. Fixing these before you apply can flip a denial into an approval.

Recent Credit Inquiries and New Accounts

Citi is very strict about recent activity. If you’ve applied for more than a few cards in the last 12 to 24 months, your odds drop fast. Cardholders often call this the “Citi 6/6 pattern.” Many report denials when they have 6 or more inquiries in the last 6 months. They also face issues if they have too many new accounts in the last year or two.

Every application triggers a hard inquiry, which stays on your report for two years. Each one can shave a few points off your score. More importantly, a stack of recent inquiries signals risk to Citi, even if your score still looks great.

Before applying, pull your reports from all three bureaus for free at AnnualCreditReport.com. Count your inquiries from the last 24 months. If you’re above 5 or 6, wait it out.

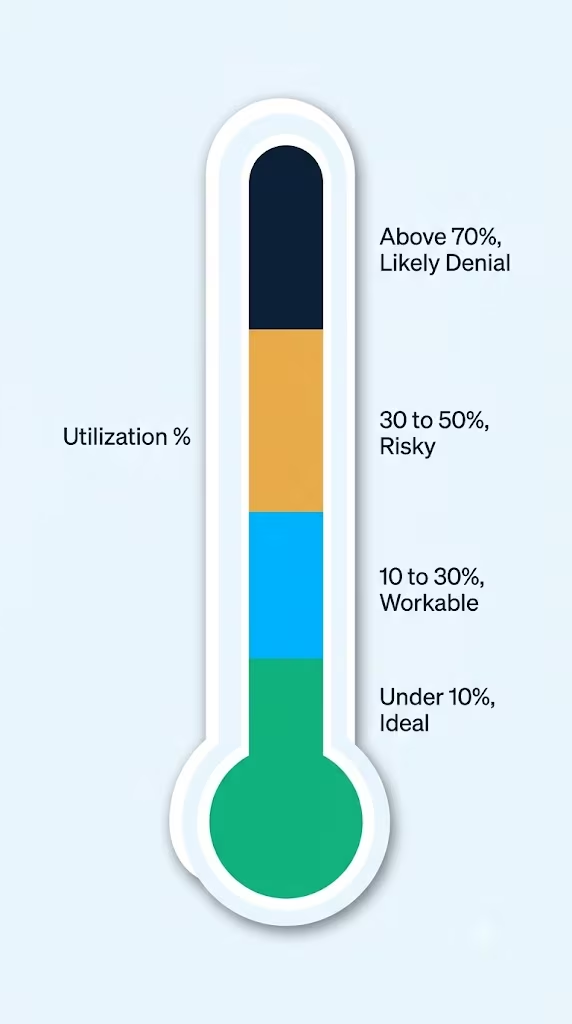

Credit Utilization Ratio

Your credit utilization ratio is the percent of your total credit limit you’re currently using. If your total limit across all cards is $20,000 and your balances add up to $6,000, your utilization is 30%.

Citi wants to see this number low. Under 10% is ideal. Under 30% is workable. Anything above 50% starts to look risky, and above 70% often triggers a denial on its own.

💡 Pro Tip: Pay down your balances before your statement closing date, not just before the due date. The balance that gets reported to the bureaus is usually the one on your statement date. Time it right, and your reported utilization can drop to near zero without you doing anything different with your spending.

Income and Debt-to-Income Ratio

Citi asks for your annual income on the application. They don’t publish a required minimum, but the card is aimed at solid earners who spend meaningfully at Costco, on gas, and on travel. Applicants reporting under $30,000 in income tend to see lower approval rates, though it’s not a hard cutoff.

They also look at your debt-to-income (DTI) ratio, which is your monthly debt payments divided by your monthly gross income. A DTI under 36% is considered healthy. Over 43% starts to hurt your odds across most major card issuers, including Citi.

Existing Relationship With Citi

If you already have a Citi card in good standing, your odds go up. Citi likes to reward loyal customers, and they can see your payment history on their own accounts instantly. If you’ve had a Citi account for a year or more with on-time payments, you have a real edge.

The flip side: if you’ve had a past charge-off, bankruptcy, or settled account with Citi, you may be on their internal blacklist. That can block approval even with a perfect score.

Can You Pre-Qualify for the Costco Visa Without a Hard Inquiry

Short answer: no. Citi does not offer a soft-pull pre-qualify tool for the Costco Anywhere Visa Card. This is a real pain point, because most other major issuers do offer this.

Chase, Capital One, American Express, and Discover all let you check your odds with just a soft pull that does not affect your score. Citi has a general pre-approval tool on their site, but the Costco Anywhere Visa is often missing from it. Some users see other Citi cards there, but not this one.

That means every real application is a full hard inquiry. There is no “safe test.” You either apply and take the hit, or you don’t.

Your best move is to self-check your profile against the factors listed above. If you clear all of them, your approval odds are strong enough to justify the application. If any red flags exist, wait and clean them up first.

Self-Assessment Checklist: Are You Likely to Be Approved

Use this checklist to gauge your likelihood of Costco card approval before you apply. Score yourself honestly on each item.

- FICO score of 720 or higher on Equifax or TransUnion

- Fewer than 4 hard inquiries in the last 12 months

- Fewer than 6 hard inquiries in the last 24 months

- No new credit card accounts opened in the last 6 months

- Total credit utilization under 10% across all cards

- No single card maxed out or above 70% utilization

- Reported annual income of at least $30,000 (higher is better)

- Debt-to-income ratio under 36%

- No late payments in the last 12 months, and none over 30 days late in the last 24 months

- No open bankruptcy, charge-off, or collection in the last 7 years

- An active Costco membership in your name

- Bonus: at least one existing Citi card in good standing

If you check every box, your approval odds are very strong. Miss one or two, and you’re still in decent shape. Miss three or more, and you should wait, fix the weak spots, and try later.

⚠️ Mistake to Avoid: Don’t apply for the Costco card at the same time as other new cards. Even if you’re approved for the others, the fresh inquiries and new accounts can trigger a denial from Citi. Space major applications at least 3 to 6 months apart.

What Happens to Your Costco Membership if You’re Denied

This is the fear that stops a lot of people. You join Costco just to get the card, get denied, and now you’re stuck paying $65 or $130 for a membership you didn’t want.

Good news: Costco has one of the most generous refund policies in retail. Their Member Privileges and Conditions state that you can cancel your membership at any time for a full refund of the annual fee. There is no time limit and no penalty. If you join, get denied, and decide Costco isn’t for you, walk up to the membership desk, ask for a refund, and you’ll get every dollar back.

So the “wasted membership” risk is basically zero. The only real cost of a denial is the hard inquiry on your credit report and a small ding to your score, usually 3 to 5 points, which recovers within a few months.

What to Do If You’re Denied

A denial is not the end. Citi sends every denied applicant a letter explaining the reasons. That letter is your roadmap. It will list the top reasons, often things like “too many recent inquiries,” “high balances on revolving accounts,” or “insufficient credit history.”

Read it carefully. Then take one of two paths.

Calling the Citi Reconsideration Line

Citi has a reconsideration line where a real person reviews your denial. This is not widely advertised, but it works. You call, explain your situation, and ask them to take a second look.

Call Citi’s application services at 1-800-763-9795. Ask to speak with someone about a recent credit card decision, and mention you’d like a manual review. Be prepared with your reasons. Explain any questions, like if you were rate-shopping for a mortgage since that’s handled differently. Clarify your income if it was under-reported. Also, if you have an existing Citi card, offer to move some credit from it.

Be polite, brief, and clear. Reconsideration works most often when the denial was borderline, not when the reasons were serious like bankruptcy or maxed cards.

When to Reapply After a Denial

If reconsideration doesn’t work, don’t rush to reapply. Applying again too soon will just add another hard inquiry and likely another denial.

Wait at least 6 months, and ideally 12, before you apply again. Use that time to fix the specific issues cited in your denial letter. Pay down balances, avoid new applications, and let old inquiries age off your report. A second application from a cleaned-up profile has much better odds.

📌 Did You Know: A hard inquiry only counts against your FICO score for 12 months, even though it stays visible on your credit report for 24 months. So the score impact fades faster than most people think.

Approval Odds for the Costco Business Card vs. the Personal Card

Costco actually offers two Citi-issued cards: the Costco Anywhere Visa Card by Citi (personal) and the Costco Anywhere Visa Business Card by Citi. The rewards structure is very similar, but the approval process has some differences.

The business card requires a legitimate business, but that bar is lower than most people think. Sole proprietors, freelancers, and gig workers all qualify. You use your Social Security Number as your tax ID if you don’t have an EIN, and your personal credit still drives the decision.

Because both cards are tied to your personal credit, your approval odds for the business version are almost identical to the personal version. Same score expectations. Same inquiry sensitivity. Same utilization checks.

Two small differences to know:

- Business income: The application asks for your business’s income, not just your personal income. If your side gig is new or small, that can hurt slightly.

- Personal guarantee: You sign a personal guarantee, meaning you are personally on the hook for any business card debt. That’s normal for small business cards, but worth knowing.

If you have both a personal need and business spending at Costco, some cardholders carry both cards. But applying for both at the same time is risky. Two hard inquiries and two new accounts in one week will spook Citi’s system. Space them out by at least 6 months.

Frequently Asked Questions (FAQs)

Is the Costco Anywhere Visa hard to get?

It requires a strong profile, not just a good score. Citi typically wants a FICO score of 720 or higher plus low utilization, few recent inquiries, and a manageable debt-to-income ratio.

Why would I be denied a Costco Credit Card?

Common reasons include too many hard inquiries, high credit utilization, insufficient income, or a past charge-off with Citi. Citi sends a denial letter listing the exact reasons for your specific application.

Can I get a Citi credit card with a 600 credit score?

A 600 score falls well below the realistic 720+ range Citi looks for on the Costco Anywhere Visa. Applicants below 670 face very low approval odds and will almost always see an instant denial.

What is the average credit score for a Costco Credit Card?

There’s no official published average, but approval data from cardholders points to a realistic bar of 720 to 740 or higher on the FICO scale. Scores below 680 rarely get approved.

What credit bureau does Costco use?

Citi most often pulls from Equifax for the Costco Anywhere Visa Card, though Experian and TransUnion pulls happen too, depending on your state. You can check your score for free through Experian’s tool or myFICO.

Is the Costco Anywhere Visa worth it?

It’s built for solid earners who spend meaningfully at Costco, on gas, and on travel, offering rewards in those categories. Whether it’s worth it depends on your spending habits, but it carries no annual fee beyond a Costco membership.

Can you get pre-qualified for the Costco Visa without a hard inquiry?

No. Citi does not offer a soft-pull pre-qualify tool for the Costco Anywhere Visa, unlike Chase, Capital One, Amex, and Discover, which do offer this feature.

What happens to my Costco membership if I’m denied for the card?

Nothing bad. Costco allows a full refund of your membership fee at any time with no time limit and no penalty, so a denial won’t leave you stuck paying for an unwanted membership.

How does the Costco Business Visa compare to the personal card for approval odds?

Approval odds are nearly identical since both rely on your personal credit profile, with the same score expectations and inquiry sensitivity. The business card also asks for business income, which can hurt slightly if your side income is new or small.

Final Thoughts

Getting the Costco Anywhere Visa Card is not just about your credit score. Citi looks at your full picture, including recent inquiries, utilization, income, and any history with them. The score you need is realistically 720 or higher, but even a 780 can be denied if your profile has other red flags.

To start, use the self-assessment checklist. Fix any weak areas. Then, apply only when you meet all the criteria. If you’re denied, use the reconsideration line before giving up, and remember your Costco membership is fully refundable.

If you know someone weighing the Costco card, share this guide with them. It could save them a needless hard inquiry and a lot of second-guessing.