You just pulled your credit report, maybe for a mortgage or an auto loan, and there it sits: a strange three-letter code called CBNA, sometimes with a prefix like THD/CBNA or BBY/CBNA. Your stomach drops a little. Is this a real account? A hard inquiry you forgot about? Or worse, a sign that someone stole your identity? I get why that feels stressful, especially when the code doesn’t match any bank name you remember.

Here’s the short answer: CBNA almost always stands for Citibank, N.A., the legal name Citibank uses when it issues or services a credit card or loan.

In this guide, we’ll walk through every version of CBNA you might see, how to tell if it’s a hard inquiry or an open account, what to do if you don’t recognize it, and how to protect your credit going forward.

Key Takeaways

This guide explains what CBNA means on a credit report, including its most common identity as Citibank, N.A., how to distinguish it from Community Bank, N.A., and what to do if the entry is unfamiliar.

Core Facts:

- CBNA most often stands for Citibank, N.A., the legal name Citibank uses when reporting accounts or inquiries to the credit bureaus.

- In Upstate New York, Northeastern Pennsylvania, Vermont, and parts of Massachusetts, CBNA can instead refer to Community Bank, N.A., a separate regional bank.

- Citi Retail Services issues co-branded and private-label cards for retailers including The Home Depot, Best Buy, Costco, Exxon Mobil, L.L.Bean, and Tractor Supply Company, which appear as prefix codes like THD/CBNA or BBY/CBNA.

- A hard inquiry from CBNA stays on a credit report for up to two years, though most scoring models only weigh it for the first 12 months.

- An open CBNA account in good standing can remain on a report for as long as it stays open plus roughly 10 years after closing, while derogatory entries follow a seven-year rule.

- Being added as an authorized user on someone else’s Citi account can cause CBNA to appear on a report without the reader ever applying for credit themselves.

Best for:

- Readers who spotted an unfamiliar CBNA entry while reviewing their credit report for a mortgage, auto loan, or other application.

- Anyone trying to determine whether a CBNA line is a hard inquiry, a soft inquiry, or an open account.

- People who don’t recognize a CBNA entry and need a step-by-step process to verify it or dispute it as fraud.

What CBNA Stands For on Your Credit Report

On the vast majority of U.S. credit reports, CBNA stands for Citibank, N.A., which is the legal name of Citibank North America. When a lender pulls your credit, or reports an account to Equifax, Experian, or TransUnion, they use their official corporate name. Citibank shortens that name to CBNA on the report.

So if you see CBNA on your file, it usually means one of two things. Either Citibank checked your credit because you applied for a card or loan, or Citibank is the actual issuer behind a credit card you already have.

The code may show up on its own, like just “CBNA,” or with a store name in front of it, such as THD/CBNA or BBY/CBNA. Those prefixes point to specific retail cards Citibank issues, which we’ll break down in a later section.

Why Citibank Uses This Particular Abbreviation

Banks report to the credit bureaus using their chartered legal name, not their marketing name. Citibank’s chartered entity is Citibank, N.A., where “N.A.” means “National Association.” That’s a federal designation for banks chartered under the Office of the Comptroller of the Currency.

So when Citibank pushes an entry to the bureaus, the reporting system trims “Citibank, N.A.” down to CBNA. It’s the same bank you know from checking accounts and Citi credit cards. The abbreviation just looks unfamiliar because the report shows the legal ID rather than the brand you see on your card.

Other Entities CBNA Can Stand For

While Citibank North America is the most common match, a few other companies share the same three letters. This can cause real confusion, so it helps to know the alternatives before you panic.

The most notable one is Community Bank, N.A., a regional bank with more than 200 branches across Upstate New York, Northeastern Pennsylvania, Vermont, and parts of Massachusetts.

This bank also uses the abbreviation CBNA and even owns the domain cbna.com. If you live in that region and applied for a mortgage, personal loan, or checking-related credit product with a local bank, this could be your match instead of Citibank.

You might also see references to Comenity Bank, which is a separate retail card issuer. Comenity is now part of Bread Financial, which rebranded from Alliance Data in 2022.

Comenity issues store cards for brands like Victoria’s Secret, Ulta, and many others. Comenity is usually reported as “COMENITY” or “COMENITYBANK,” not CBNA, but people sometimes mix the two up because both are card issuers. If your entry actually reads Comenity, that’s a completely different company from Citibank.

Some rare or historical matches exist, like small credit unions with similar initials. However, they rarely show up on national credit reports today. For most readers, CBNA on a U.S. credit file means Citibank.

How to Tell Which Entity Applies to Your Report

To confirm which company is behind your entry, look at the account details section for these clues:

- Full name and address. Most reports list the creditor’s mailing address next to the entry. A New York or Pennsylvania address often means Community Bank, N.A. A Sioux Falls, South Dakota address usually means Citibank. Citibank handles many cards from that spot.

- Phone number. Call the number listed on the report. The person who answers will identify the company by name.

- Account type. A retail store card or a co-branded Citi card almost always means Citibank. A mortgage, HELOC, or local checking-related loan more likely points to Community Bank, N.A.

A one-minute check of these three fields is usually enough to know which CBNA you’re dealing with.

Common Citi-Issued Retail Cards That Trigger a CBNA Entry

A big reason people don’t recognize CBNA is that they don’t think of their store card as a “Citibank” card. But Citibank’s division called Citi Retail Services issues co-branded and private-label cards for many of the country’s largest retailers. When you apply for one of those store cards, or when the issuer reports your account, the entry shows up under CBNA.

Some of the best-known partners include:

- The Home Depot Consumer Credit Card and Commercial Card

- My Best Buy Credit Card and My Best Buy Visa

- Costco Anywhere Visa (this is a Citi-issued card)

- Exxon Mobil Smart Card+

- L.L.Bean Mastercard

- Tractor Supply Company (TSC) credit cards

- Macy’s and various department store cards

You can see the current lineup on Citi’s retail store credit cards page. Some retailers have moved issuers over the years, so a card that used to be issued by Synchrony or Comenity may now be issued by Citi, or the other way around. Always check the fine print on the back of your card for the actual issuer.

Full List of CBNA Prefix Codes and What They Mean

When Citi Retail Services reports a store card, the credit bureau entry often uses a short retailer prefix followed by “/CBNA.” Here are the ones people ask about most:

| Prefix / Code | What It Means | Retailer |

|---|---|---|

| THD/CBNA | The Home Depot card | The Home Depot |

| BBY/CBNA | Best Buy card | Best Buy |

| CBNA/COSTCO or COSTCO/CBNA | Costco Anywhere Visa | Costco |

| EXXON/CBNA | Exxon Mobil Smart Card | ExxonMobil |

| MACYS/CBNA | Macy’s store card | Macy’s |

| LLBEAN/CBNA | L.L.Bean Mastercard | L.L.Bean |

| TSC/CBNA | Tractor Supply card | Tractor Supply Co. |

If your entry has a prefix that isn’t on this list, look up the letters in the account name field. It’s almost always a shorthand for the retailer whose card you carry.

💡 Pro Tip: If you have a store card and forgot who issued it, flip the card over. The issuer’s name is printed on the back in small text, right above the customer service phone number. That one glance solves most CBNA mystery entries.

Is the CBNA Entry a Hard Inquiry, Soft Inquiry, or an Open Account?

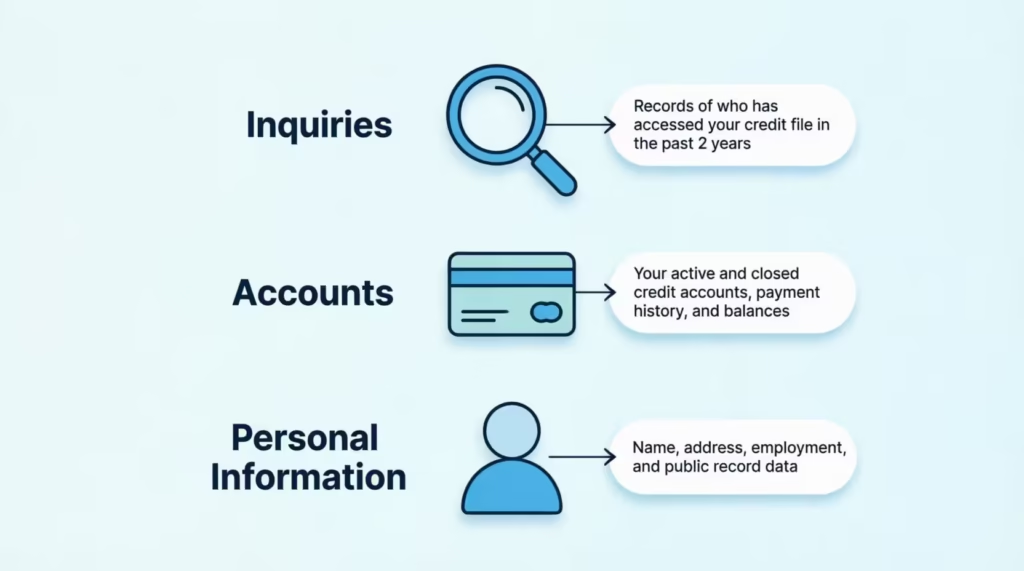

Once you know CBNA is Citibank, the next question is what kind of entry you’re looking at. A CBNA line can be a hard inquiry, a soft inquiry, or an open account. Each type sits in a different section of your credit report and has a different effect on your score.

Hard inquiries show up in the “Inquiries” section, sometimes labeled “Requests Viewed by Others” or “Hard Inquiries.” These happen when you apply for new credit, and the lender pulls your full file. The Consumer Financial Protection Bureau explains that hard inquiries are visible to other lenders and can affect your score.

Soft inquiries appear in a separate section, often called “Requests Viewed Only by You” or “Soft Inquiries.” These happen when Citi checks your credit for a pre-approved offer, when you check your own credit, or when an existing lender reviews your account. Soft inquiries do not affect your credit score at all.

Open accounts show up in the “Accounts” or “Trade Lines” section, which is the main body of the report. This section lists your balance, credit limit, payment history, and account status. An open account is very different from an inquiry, because it can help or hurt your score depending on how it’s managed.

Quick way to tell them apart:

- If CBNA appears in the inquiries section with only a date and a company name, it’s an inquiry.

- If CBNA appears with a balance, credit limit, and payment history, it’s an open account.

- If CBNA appears in the “soft” or “promotional” list with a date, it’s a soft inquiry, and you can ignore it.

How a CBNA Hard Inquiry Affects Your Credit Score

A single hard inquiry from Citibank has a small, temporary effect on most credit scores. FICO’s general guidance is that one hard inquiry usually costs fewer than five points, and many people see no change at all.

The impact is bigger when several inquiries stack up in a short window, since that pattern can signal financial stress. Applying for one Citi retail card is low risk. Applying for a Home Depot card, a Best Buy card, a Costco card, and an auto loan in the same month is a much bigger score dip.

The good news is that inquiries fade fast. Their effect on your score usually drops off within a few months, even though the record itself stays on the report longer.

How Long a CBNA Inquiry or Account Stays on Your Report

A hard inquiry from CBNA stays on your credit report for up to two years. Most credit-scoring models only weigh it for the first 12 months, so the score damage clears up well before the record disappears.

Open accounts follow different rules. A CBNA account in good standing can stay on your report for as long as it’s open, plus roughly 10 years after you close it. That long tail is a good thing, because a well-managed account keeps helping your credit age even after you shut it. Negative marks, like late payments or collections, follow the seven-year rule.

CBNA Showing Up as an Open Account vs. a New Inquiry

Not every CBNA entry means the same thing for your score. The exact wording next to the account tells you whether this is a positive credit builder or a warning sign.

A CBNA open account in good standing usually looks like this on the report:

- Status: “Open” or “Paid as agreed”

- Payment history: rows of “OK” or green markers

- Balance: current balance and credit limit both listed

- Past due: $0

An entry like that is a neutral or positive signal. It shows you have an active line of credit, you’re using it, and you’re paying on time. Long-standing accounts in this shape actually help your credit score by adding to your account age and payment history.

A CBNA derogatory entry looks very different:

- Status: “Late,” “30 days past due,” “Charge-off,” or “Collection”

- Payment history: red markers or “30,” “60,” “90,” “120” codes

- Balance: may still show a balance owed

- Comments: may include “account closed by creditor” or “placed for collection”

These entries hurt your score, sometimes badly. A charge-off happens when the issuer writes the debt off as a loss, usually after about 180 days of missed payments. A collections entry means the debt was sold or referred to a collection agency. Both are serious and stay on the report for seven years from the first missed payment.

The exact three letters (CBNA) look identical in both cases, but the numbers and status codes next to them tell the real story. Always read those before you decide whether an entry is helping or hurting you.

CBNA From Being Added as an Authorized User

Sometimes a CBNA account shows up on your report even though you never applied for anything. The usual reason is that a family member or partner added you as an authorized user on their Citi credit card.

Being an authorized user means you can use the card, but you are not legally responsible for the debt. The primary cardholder still owns the account. Even so, Citibank reports the account to the credit bureaus under your name too, which is why it appears on your report.

This setup can help your credit if the primary cardholder manages the account well. A long history of on-time payments and low balances flows onto your report and can boost your score, especially if you have a short credit history of your own. Parents often use this as a way to help their kids build credit.

The flip side is real, though. If the primary cardholder pays late, runs the balance near the limit, or lets the account go to collections, that damage also lands on your report. You didn’t cause it, and you don’t owe the money, but your score can still take a hit.

To get removed as an authorized user, you have two paths:

- Ask the primary cardholder to call Citibank and remove you. This is the fastest option, since most issuers process the removal within one billing cycle.

- Contact Citibank directly using the number on the back of the card or on the credit report entry. Citi will usually remove an authorized user from the account when the person asks, even without the primary cardholder’s approval.

After removal, the account should stop reporting on your credit file, though it may take one to two months to fully clear.

⚠️ Mistake to Avoid: Don’t leave yourself on a struggling relative’s Citi card just to be polite. If they start missing payments, that damage lands on your report too. Ask to be removed the moment the account stops being managed well.

What to Do If You Recognize the CBNA Account

If CBNA lines up with a Citi card or a store card you actually applied for, the answer is simple: there’s nothing you need to do. The entry is legitimate, and your report is doing its job.

That said, take one minute to check the details for accuracy. Confirm the account open date, the credit limit, the current balance, and the payment history. Small errors do happen, and even a small mistake on a positive account can slightly affect your score. If anything looks off, dispute it with the bureau directly.

If the entry is a hard inquiry from a card you applied for, you’ll just need to wait it out. The record fades from your score within about a year and drops off the report after two.

When You Cannot Remove a Legitimate CBNA Entry

An accurate, legitimate hard inquiry cannot be removed early, no matter what “credit repair” ads promise. Credit bureaus are required to keep accurate data on your file, and Citibank has no reason to retract an inquiry it correctly reported.

The same rule applies to open accounts. A CBNA account you opened yourself will stay on the report while it’s active, and for years after you close it. Trying to dispute an accurate entry to erase it wastes your time and can even get flagged as frivolous under bureau rules.

The one exception is if you can prove the inquiry was made without your permission. In that case, it’s no longer legitimate, and the steps in the next section apply.

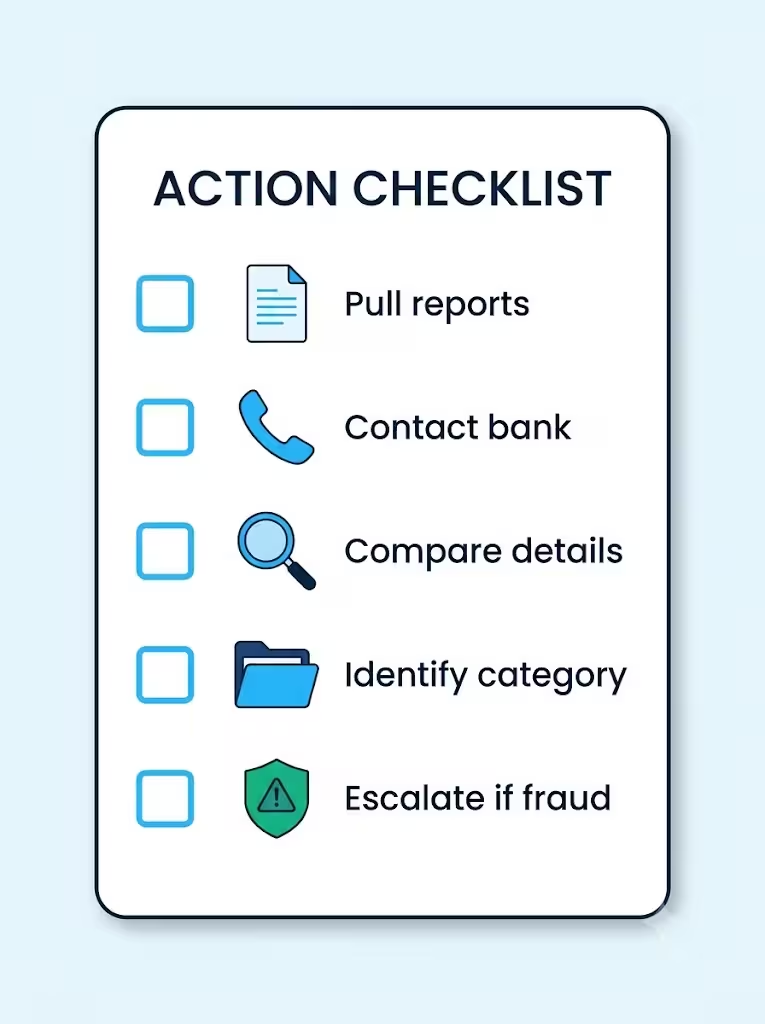

What to Do If You Don’t Recognize the CBNA Account

This is the highest-stakes scenario, so take it step by step. Not every unfamiliar entry means fraud. Some are simple errors, some come from authorized-user setups you forgot about, and some are old accounts you didn’t remember. Work through this list in order.

Step 1: Pull all three credit reports. Go to AnnualCreditReport.com, which is the only site the FTC officially recognizes for your free credit reports. Free weekly reports from Equifax, Experian, and TransUnion are now permanent, so you can pull all three today. Check whether CBNA appears on all three or just one.

Step 2: Contact Citibank directly. Use the phone number listed next to the entry on the credit report. Don’t Google a number, since scam sites often mimic real bank listings. Ask the Citibank representative to look up the account by your Social Security number and name. If they find an account, ask when it was opened, from where, and what card it’s tied to. If they find no account under your info, that alone tells you the entry may be a reporting error.

Step 3: Compare the details. Look at the name, address, and account open date on the credit report entry. If the address is one you never lived at, or the open date is a month you weren’t applying for credit, that’s a red flag.

Step 4: Figure out the category. Based on Steps 2 and 3, the entry is probably one of these:

- Simple error. Citibank has no record, or the account is under someone with a similar name or SSN.

- Forgotten authorized-user status. A relative added you years ago and never told you.

- Identity theft. Someone opened a Citibank or Citi-issued store card in your name.

Step 5: Escalate if fraud is confirmed. If Citibank confirms an account was opened without your permission, file an identity theft report at IdentityTheft.gov, which is the FTC’s official reporting site. That report gives you a personalized recovery plan and legal proof you can send to bureaus and creditors.

How to Dispute an Unauthorized or Incorrect CBNA Entry

Once you’ve confirmed the entry is wrong, dispute it with each credit bureau that shows it. Each bureau has a free online dispute portal:

In your dispute, include:

- Your full name, current address, and date of birth

- A clear statement that the CBNA account or inquiry is not yours

- Copies of your Citibank confirmation (if they told you there’s no account)

- Your FTC identity theft report number, if fraud is involved

Under the Fair Credit Reporting Act, the bureau must investigate your dispute, usually within 30 days. If the bureau can’t verify the entry with Citibank, they must remove it. If they do verify it and you still disagree, you can add a personal statement to your file and take further action directly with Citibank.

Also file a dispute directly with Citibank at the same time. That way, if the bureau contacts them, Citi already has your case on record.

Protecting Your Credit Going Forward

Whether your CBNA entry turned out to be legitimate or fraudulent, a few habits will keep future surprises off your report.

Set up a credit freeze if you suspect any fraud. A freeze blocks new creditors from pulling your report, which stops most identity thieves from opening accounts in your name. Freezes are free, and you can turn them on or off at each bureau’s site anytime.

Add a fraud alert if you’re not ready to freeze. A fraud alert tells lenders to take extra steps to verify your identity before opening new credit. You only need to file it with one bureau, and that bureau will notify the other two. It’s a lighter option than a freeze and lasts one year (or seven if you have a police or FTC identity theft report).

Check your credit reports on a schedule. With free weekly access at AnnualCreditReport.com, a smart routine is to check one bureau every four months, so you’re always looking at fresh data. That catches new mystery entries early, when they’re easier to fix.

Keep an eye on account alerts. Turn on email or text alerts through your Citibank account and any other card issuer. Get real-time alerts for new inquiries, big purchases, or address changes. These warnings help you spot issues before they show up on your credit report.

📌 Did You Know: The FTC’s rule for free weekly reports from all three bureaus is now permanent, not a pandemic-era stopgap. That means you can check your credit 52 times a year at no cost, forever.

Frequently Asked Questions (FAQs)

Who does CBNA collect for?

CBNA itself is Citibank, N.A., the issuer, not a collection agency. If a Citibank account goes unpaid long enough, the debt may be sold or referred to a separate collection agency, and that entry would show a different company name.

Which credit bureau does Citibank pull from?

Citibank can pull from any of the three major bureaus (Equifax, Experian, or TransUnion) depending on the application. Check the “Inquiries” section of each of your three reports separately to see exactly where Citibank looked.

What is the CBNA credit card limit?

There is no single CBNA credit limit, since Citi Retail Services issues many different cards under this code, from Home Depot to Costco. Your limit depends on the specific card and appears in the account details section of your credit report.

What is the CBNA credit card on my Credit Karma?

A CBNA entry on Credit Karma is the same Citibank, N.A. account or inquiry that appears on your official credit reports. Check the account details for the address, phone number, and account type to confirm which Citi-issued card it belongs to.

Is CBNA a legitimate credit inquiry?

Yes, CBNA is a legitimate inquiry when it matches a Citi card or store card you actually applied for. It only becomes a problem if you don’t recognize the account, in which case you should call Citibank directly to verify it.

What is the bank name for CBNA?

CBNA stands for Citibank, N.A. in most cases, with N.A. meaning “National Association,” a federal charter designation. In parts of Upstate New York, Northeastern Pennsylvania, and Vermont, CBNA can instead mean Community Bank, N.A., a separate regional bank.

Is Best Buy the same as CBNA?

No, Best Buy is a retailer, not a bank. Citibank issues the My Best Buy Credit Card and My Best Buy Visa, so they report as BBY/CBNA on your credit file.

What other cards are affiliated with Citibank?

Citi Retail Services issues cards for The Home Depot, Best Buy, Costco Anywhere Visa, Exxon Mobil, L.L.Bean, Tractor Supply Company, and Macy’s. Some retailers have switched issuers over time, so it’s worth checking the back of your card for the current issuer name.

How do I dispute an incorrect CBNA entry?

File a free dispute with Equifax, Experian, or TransUnion online, including your name, address, and a statement that the account isn’t yours. The bureau must investigate within 30 days and remove the entry if Citibank can’t verify it.

How long does a CBNA hard inquiry stay on my report?

A CBNA hard inquiry stays on your report for up to two years, but it only affects your score for the first 12 months. A well-managed CBNA open account can stay on your report for as long as it’s open plus roughly 10 years after you close it.

Bottom Line

A CBNA line on your credit report almost always traces back to Citibank, N.A., often through a Citi-issued retail card like Home Depot, Best Buy, or Costco. The three letters can appear as a hard inquiry, a soft inquiry, or an open account, and each carries a very different weight on your score.

To respond quickly, first check your records against the entry. If something seems wrong, contact Citibank directly. Dispute promptly if you confirm fraud.

Share this guide with a friend who just spotted a strange code on their report; it may save them hours of worry.