If you’re staring at a high APR credit card balance and thinking about the Citi Diamond Preferred Card as your way out, you want one thing before applying: a clear read on your Citi Diamond Preferred Card approval odds. A hard inquiry with no card in return is not just a small ding. It delays your debt payoff and costs you more interest every month you wait.

Approval usually goes to applicants with a good FICO score (670+), stable income, and manageable credit utilization, not just a high score alone.

We’ll walk you through the real score cutoff, how your existing debt fits in, the credit limit you can expect, and what to do if you get denied.

Key Takeaways

This guide explains what actually determines Citi Diamond Preferred approval odds, including score thresholds, utilization limits, income factors, credit limit ranges, and steps to take if denied.

Core Facts:

- A FICO score of 700 or higher gives applicants a strong chance of approval, while scores between 670 and 699 depend heavily on the rest of the profile, and scores under 670 rarely get approved.

- Credit utilization above 50% is a risk flag, and above 75% is nearly an automatic denial, while utilization under 30% across all revolving accounts is considered healthy.

- Citi’s 8/65 rule limits applicants to two card applications within any 65-day window, with at least 8 days required between applications.

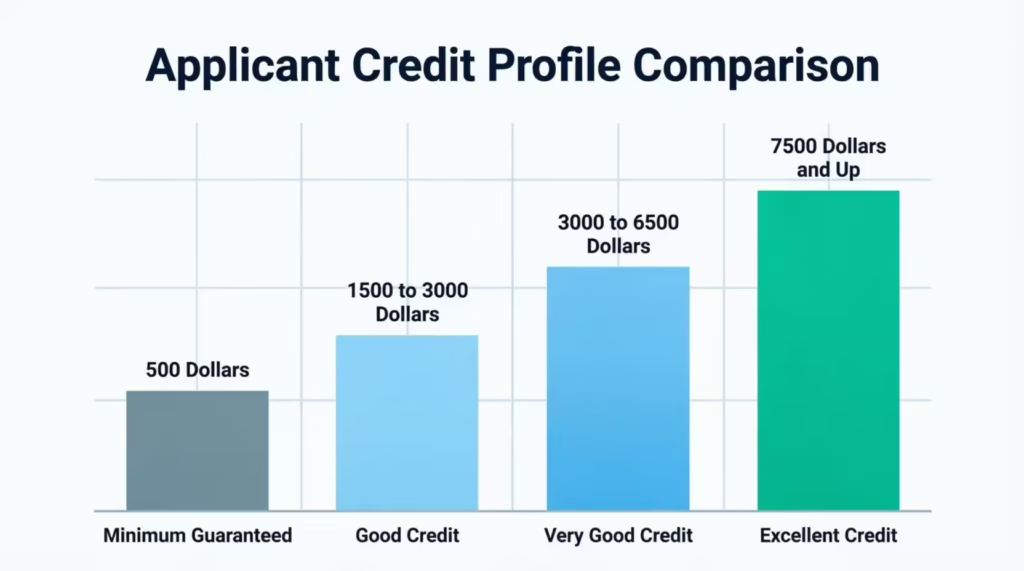

- Starting credit limits typically range from a $500 minimum for weak approvals up to $7,500 or more for applicants with excellent credit and low debt, with $3,000 commonly reported as a typical starting limit.

- Card approval and balance transfer approval are separate decisions, and Citi caps the transferable amount at around 95% of the assigned credit limit, meaning any excess balance stays on the original card.

- Checking pre-qualification uses a soft credit pull that does not affect the credit score, but full underwriting still applies a hard pull that can result in denial even after pre-qualifying.

Best for:

- Applicants with good to very good credit who want to understand why a strong score alone may not guarantee approval.

- People planning a balance transfer who need their assigned credit limit to cover their full debt payoff target.

- Anyone recently denied for Diamond Preferred who wants to understand the adverse action notice and the reconsideration process.

Credit Score You Need for the Citi Diamond Preferred Card

Citi does not publish an official minimum credit score for the Diamond Preferred Card. That gap in public info is exactly why so many good-credit applicants get denied and feel blindsided. What we can do is look at what actually gets people approved.

The card is built for people with good to excellent credit. Based on the standard FICO scale, a “good” score sits between 670 and 739, and “very good” starts at 740. myFICO reports that a good credit score is considered to be in the 670–739 range.

Community data from applicant forums and card review sites shows most approved profiles land in the 700+ range. Some people report approvals with scores in the high 600s, but they usually have very high income and low card balances. Applicants under 670 rarely get through unless something else on the file is unusually strong.

So a working benchmark looks like this. A FICO score of 700 or higher gives you a real shot. A score between 670 and 699 is a maybe, and it depends heavily on the rest of your profile. A score under 670 is a long shot, and you’re better off working on your credit for a few months first.

Two more things matter here. First, Citi pulls credit reports from all three bureaus, but reports suggest Equifax is common in many regions. Second, your score today is what counts. Not last month’s score. Not the score in your banking app if it’s outdated. Pull a fresh number before you apply.

📌 Did You Know: The Citi Diamond Preferred Card gives you 0% intro APR for 21 months on balance transfers from account opening. That’s one of the longest 0% periods available, according to Citi’s product page. That long runway is why score alone doesn’t tell the full story. Citi has to feel confident you’ll actually pay it off in 21 months.

Why Good Credit Alone May Not Be Enough

Here’s the tension that trips up so many applicants. Your score is good. Maybe even great. And you still get denied. How?

The score is one input. Citi looks at the whole picture. That means your current debt load, your recent credit activity, your income, and how much room you already have on other cards. A 720 FICO score with $15,000 in credit card balances is a very different risk than a 720 FICO score with $500 in balances.

This is a card built to move debt around, so the bank pays close attention to how much debt you already carry. If you look overextended, they may pass, even with a strong score. Your Citi Diamond Preferred approval chances improve when the rest of your file looks calm, not just when your score is high.

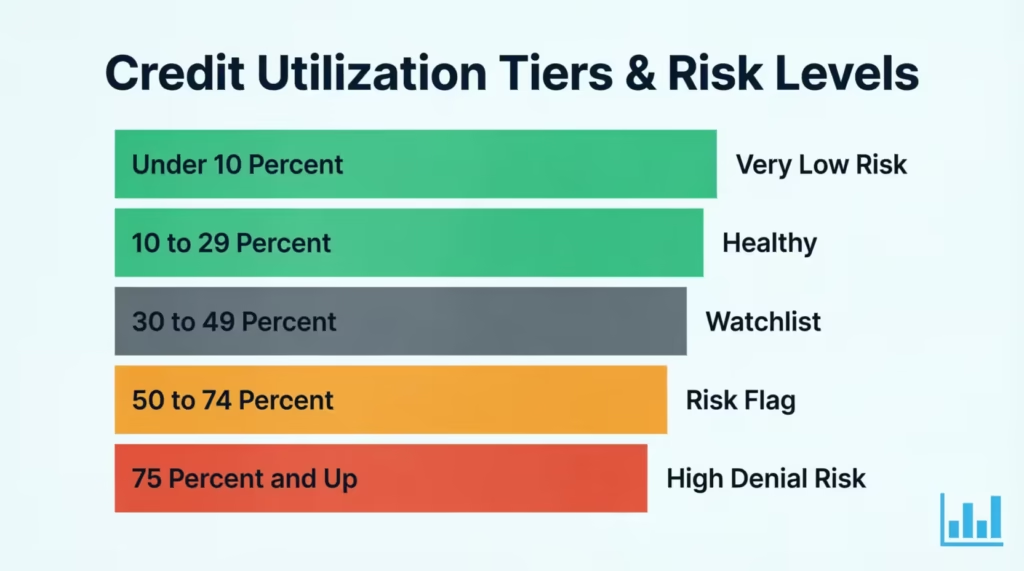

How Existing Debt and Utilization Affect Your Odds

Credit utilization is the share of your available credit that you’re actively using. Under 30% is generally seen as healthy. Under 10% looks even better to underwriters. If you’re carrying balances that push your utilization above 50%, expect trouble, even with a 720+ score.

The tricky part is this. The balance you want to transfer counts against you until it moves. Say you have $8,000 in debt on a card with a $10,000 limit. Your utilization on that card is 80%. Citi sees that when they pull your report. They don’t know you plan to shift it over. To their model, you look maxed out.

Aim for utilization under 30% across all your revolving accounts before you apply. If you can, pay a chunk of your existing balance down first. Even a small drop, from 65% to 45%, can move your approval odds in a real way. Then apply.

Target utilization ranges to keep in mind:

| Utilization Level | How Citi Likely Sees It |

|---|---|

| Under 10% | Very low risk, strong signal |

| 10% to 29% | Healthy, no concern |

| 30% to 49% | Watchlist, may reduce limit offered |

| 50% to 74% | Risk flag, denial possible |

| 75% and up | High denial risk regardless of score |

How Recent New Debt (Loans, Other Cards) Can Hurt Your Application

Opening new accounts or loans right before you apply can sink you. Here’s why.

A new auto loan, a personal loan, or a mortgage adds fixed monthly payments to your file. Citi factors these into your debt-to-income calculation. Even if the score barely dipped, your ability to take on new debt just dropped in the bank’s eyes.

New credit cards hurt in a different way. Each recent hard inquiry and each new tradeline suggests you’re seeking a lot of credit fast. Citi’s own timing rules make this worse. The 8/65 rule limits Citi applications to two card apps in any 65-day window, with at least 8 days between them, per NerdWallet’s guide to Citi application rules.

If you opened a big loan in the last 3 to 6 months, or added two or more new cards recently, your approval odds drop even with the same score. Waiting three to six months and letting the file settle can make a real difference.

Income and Debt-to-Income Expectations

Citi asks for your annual income on the application because it matters. There’s no published minimum. But underwriting uses income to check two things: whether you can afford a new credit line, and how your total debt compares to what you earn.

Debt-to-income ratio (DTI) is your monthly debt payments divided by your gross monthly income. Credit card issuers generally like to see DTI under 40%. Under 30% is stronger.

Report your income accurately. That includes salary, wages, self-employment income, and, if you’re 21 or older, income you have reasonable access to (like a spouse’s income). Don’t inflate it. If Citi asks for verification and the numbers don’t match, that’s an automatic denial.

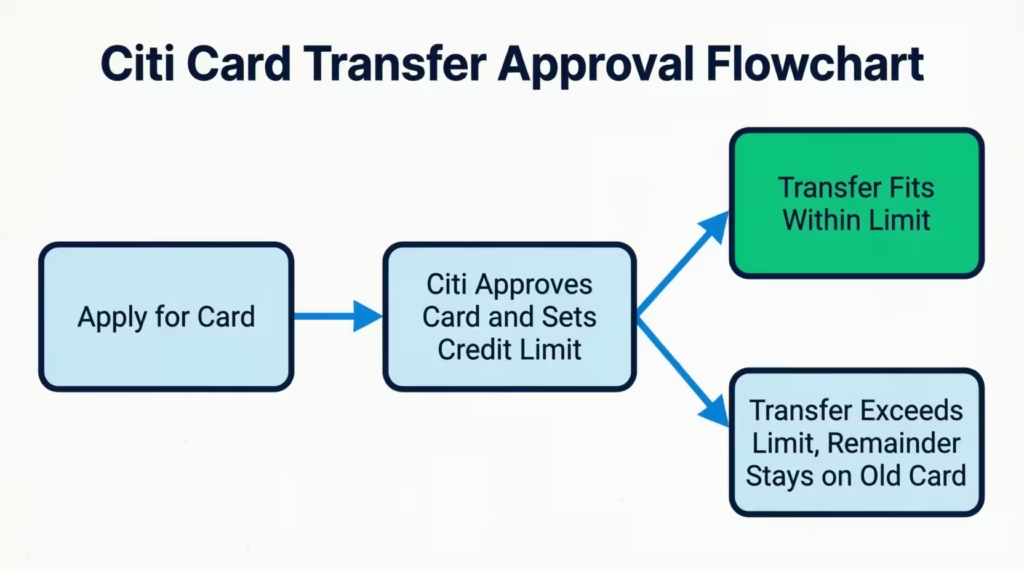

Card Approval vs. Balance Transfer Approval: Two Separate Decisions

This is the part most articles skip, and it catches people off guard.

Getting approved for the Citi Diamond Preferred Card and for your full balance transfer are two different decisions. Citi first decides whether to give you the card. Then, separately, they decide how much of your requested transfer they’ll actually process.

Here’s how the process works in practice: Say you get approved for the card with a $5,000 credit limit. You asked to transfer $8,000 from another card. Citi will not transfer $8,000 onto a $5,000 line.

They may transfer up to about 95% of your new limit (rules vary), meaning around $4,750 gets moved. The remaining $3,250 stays on the old card at the old high APR. That’s a transfer request decline in practice, even though your card was approved.

The Citi Diamond Preferred balance transfer approval decision is capped by your assigned credit limit. That’s why the credit limit you’re offered is not just a “nice to know.” It’s the ceiling on your debt payoff plan.

💡 Pro Tip: Before you apply, list every balance you want to transfer and add them up. If your total transfer target is $7,000, you need Citi to approve you for a limit above that. If you’re offered less, you’ll have to keep part of your balance on the old card, or transfer the rest to a second card later.

The lesson: don’t just plan for card approval. Plan for a credit limit that actually covers your debt payoff goal.

What Credit Limit to Expect If You’re Approved

The Citi Diamond Preferred credit limit varies widely, and it directly shapes how useful the card is for your payoff plan. Here’s what applicants report seeing.

The starting credit limit on the Diamond Preferred typically falls in these bands:

| Applicant Profile | Common Starting Credit Limit |

|---|---|

| Minimum guaranteed limit (weakest approvals) | $500 |

| Good credit (670-720), some debt on file | $1,500 to $3,000 |

| Very good credit (720-760), stable income | $3,000 to $6,500 |

| Excellent credit (760+), high income, low debt | $7,500 to $10,000+ |

The $500 floor is the minimum by federal card guidelines. Citi rarely goes below that. On the high end, $10,000 and above shows up for strong profiles, but it’s not the norm.

The most commonly reported starting limit is around $3,000. That’s fine if you’re moving $2,500 in debt. It’s not enough if you’re trying to shift $8,000. Set expectations before you apply so a lower-than-hoped limit doesn’t derail your plan.

Citi looks at the same things for your credit limit and approval. These include your score, income, current Citi credit exposure, and total revolving balances. A higher-income applicant with clean utilization usually gets a bigger limit than the same score with maxed-out cards.

If your assigned limit falls short, you have three options. Accept it and transfer what you can. Call Citi within a few days and ask for a credit limit increase (rarely granted on new accounts, but possible). Or plan to open a second balance transfer card after this one settles in.

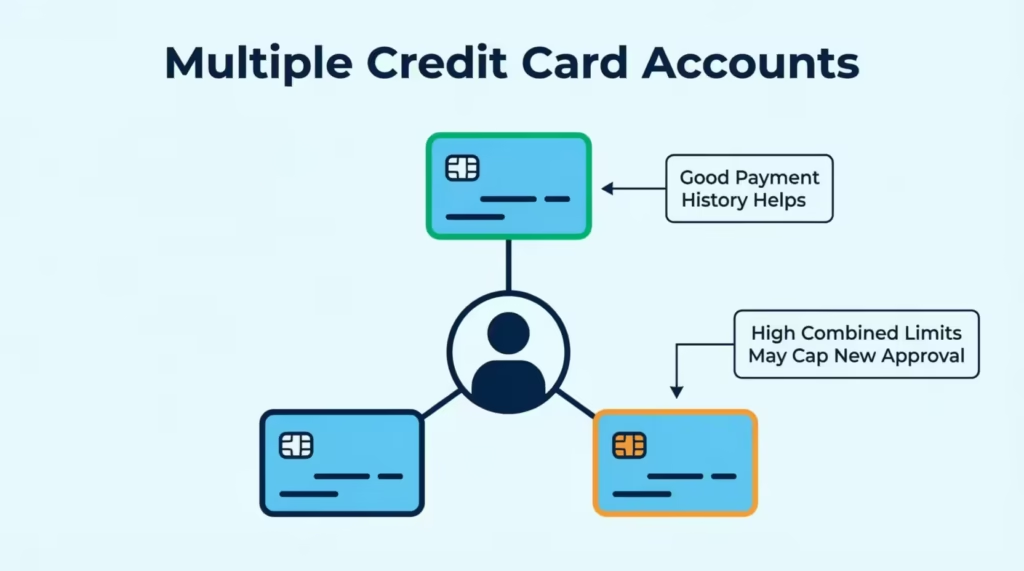

How an Existing Citi Relationship Affects Your Approval

If you already bank with Citi or hold another Citi credit card, that history can cut either way. It’s not automatically a plus.

An existing account in good standing helps. Citi can see your on-time payment record on other Citi products, your average balances, and how long you’ve been a customer. That data can support your approval and sometimes push toward a higher starting limit.

On the other side, Citi caps how much total credit any one customer can hold. This is your existing Citi relationship ceiling. If you already carry two or three Citi cards with high combined limits, adding another may push you over their internal exposure cap. In that case, the answer is often to lower one of your existing Citi limits before applying, freeing up space in their internal budget for you.

Practical steps if you’re a current Citi customer:

- Check the combined credit limit across all your open Citi cards

- Consider requesting a limit decrease on an unused Citi card before applying

- If you have a Citi card you rarely use, closing it is another option (though closing accounts can affect your average account age)

- Log into Citi’s site and look for pre-qualified offers, which factor in your existing relationship

A past bankruptcy, charge-off, or closed account with Citi can block your approval for years. This can happen even if your score has improved in other areas.

Checking Pre-Qualification Before You Apply

The single smartest move before applying is to check pre-qualification. It costs nothing, protects your score, and gives you a real signal.

Citi runs a free pre-qualification tool on its site. When you use it, Citi performs a soft pull on your credit. A soft pull does not affect your score at all. It’s the same kind of inquiry that happens when you check your own credit or when a card issuer sends you a promotional offer.

The tool checks your basic file against Citi’s current marketing criteria. If you match, you’ll see the Diamond Preferred (and possibly other Citi cards) listed as pre-qualified offers. That’s a strong signal, though not a guarantee.

Two important limits to know. A pre-qualified match does not lock in approval. When you formally apply, Citi does a full hard-pull underwriting review. Even those who pre-qualify can still be denied.

This happens because full underwriting may reveal issues the soft pull missed, like recent debt spikes or DTI problems. And second, not appearing pre-qualified doesn’t always mean you’d be denied. Citi’s marketing filter and its underwriting filter aren’t identical.

Still, checking is a no-cost, no-risk move that answers the question “am I pre-qualified for Citi Diamond Preferred” before you commit to a hard inquiry. Do it every time.

⚠️ Mistake to Avoid: Applying for the card directly without checking pre-qualification first. A hard inquiry stays on your report for two years and can drop your score by 5 to 10 points. That drop can push a borderline applicant just below the next approval tier, hurting you for both this card and any future ones.

Common Reasons Diamond Preferred Applications Get Denied

If you got a Citi Diamond Preferred denial after applying, the reason usually falls into one of a few clear buckets. Understanding which one applies to you tells you what to fix.

The most common denial reasons include:

- Credit score below Citi’s internal threshold. Even if you’re at 670, some underwriting decisions land above that in practice. Scores in the low 600s or below almost always get denied.

- High credit utilization on existing cards. As covered earlier, high balances signal that you’re already stretched. Utilization above 50% is a red flag. Above 75% is nearly automatic denial.

- Recent major financing. A new mortgage, auto loan, or personal loan in the last 3 to 6 months. Or two-plus new credit cards in that window. This is the “too much new debt, too fast” flag.

- Insufficient income relative to requested credit. If your income is low or you didn’t report accessible household income, Citi may decide the risk is too high.

- Existing Citi credit exposure cap. As explained above, if Citi already has significant credit extended to you, they may cap adding more.

- Recent Citi application, or violation of the 8/65 rule. If you applied for another Citi card in the last week, or three or more Citi cards in the last 65 days, you’ll be auto-denied by their system.

- Serious derogatory marks. Recent late payments, collections, charge-offs, or a bankruptcy in the last 4 to 7 years often prevent approval, no matter your current score.

- Frozen credit report. If you froze your credit and forgot to lift the freeze at the bureau Citi pulls from, the application can’t complete.

The denial letter (called the adverse action notice) will list your specific reason. Read it carefully. It tells you exactly what to fix.

What to Do If You’re Denied for the Citi Diamond Preferred Card

A denial is not the end of the road. Two next steps can still turn things around.

First, read the adverse action notice in full. Under federal law, when a creditor denies your application, they must send this notice within 30 days. It has to state the specific reasons for denial and the credit bureau they used. The Consumer Financial Protection Bureau’s rules on adverse action notices also give you the right to a free copy of the credit report used, if you request it within 60 days.

Read the exact denial reasons. If it says “too high a balance on revolving accounts,” you know utilization sank you. If it says “too many recent inquiries,” recent apps did it. This is your action list.

Second, call the Citi reconsideration line. Citi’s reconsideration line looks at denied applications. It allows a human to review cases that the automated system denied. This review might lead to a different decision. This is worth the call.

You can usually reach the Citi reconsideration line for personal credit cards at 1-800-763-9795. Check Citi’s website or your denial notice to confirm the number, as it may change. Call within about 30 days of denial for the best chance.

When you call, be prepared with:

- Your application reference number (in the denial notice or email)

- The specific denial reason from the letter

- A short, calm explanation of context they may have missed

For example, if you were denied for high utilization, explain that most of that balance is exactly what you plan to transfer, and that you have a plan to pay it down using the 0% intro period. Ask if they can reconsider based on your full profile.

Sample script: “Hi, I’m calling about my application for the Citi Diamond Preferred, reference number [X]. I received a denial citing my current credit utilization. I wanted to explain that the balance in question is the debt I’m looking to transfer to this card as part of a payoff plan I can complete during the 0% period. My income is stable at [X], and I’ve had [Y] years of on-time payment history. Can you review my application again?”

Reconsideration isn’t guaranteed. But real approvals happen this way when the applicant explains the context. And even if it doesn’t work, you’ll learn more about why.

If reconsideration also fails, don’t apply again right away. Wait at least 3 to 6 months. Fix the specific issue the notice named. Then try again, or consider a different balance transfer card whose underwriting rules match your profile better.

Steps to Improve Your Approval Odds Before Applying

If you’re not applying today, you have time to strengthen your file. Small changes make a real difference. Here’s what actually moves the needle.

1. Pay down credit utilization first. This is the single fastest lever. If your utilization is 60% today, get it under 30% before applying. Even better, target under 10% on any single card. Utilization updates when your card issuer reports to the bureaus, usually monthly. Pay balances down at least a week before your statement closes, so the lower number gets reported. Then wait for the new report to hit before you apply, usually 30 to 45 days.

2. Wait out recent large financing. If you opened an auto loan, mortgage, or personal loan in the last few months, or added new cards, give it time. Waiting 3 to 6 months lets your file settle. Hard inquiries lose most of their weight after 12 months.

3. Check your pre-qualification. Use Citi’s tool. If you’re not pre-qualified today, that’s useful info. Check again in 30 to 60 days after you’ve paid down debt.

4. Fix credit report errors. Get your free reports at AnnualCreditReport.com, the official site authorized by federal law. Dispute anything that’s wrong. Wrong late payments, accounts that aren’t yours, or balances that don’t match reality. Fixing errors can boost your score by 10 to 40 points fast.

5. Don’t open new accounts right before applying. Every new tradeline lowers your average account age and adds an inquiry. Give yourself a clean runway of at least 60 to 90 days with no new applications before Diamond Preferred.

6. Report your accurate, full income. Include salary, side income, and (if you’re 21 or older) reasonable access to household income. Higher reported income can bump your assigned credit limit.

7. Time your application right. Apply after your statement cycles have posted the lower balances. Apply on a weekday during business hours if possible. Approval processing can sometimes resolve faster.

Following just the first two steps (utilization + waiting out new debt) tends to give the biggest lift for people trying to figure out how to improve Citi Diamond Preferred approval odds. They’re free, they’re within your control, and they work.

Frequently Asked Questions

What credit score do I need for Citi Diamond Preferred?

There’s no official published minimum, but approvals cluster around 700 and above. A score of 670 to 699 can work with a strong profile, meaning low utilization, stable income, and no recent new debt. Below 670, approval becomes uncommon.

Can I get approved for Diamond Preferred with high credit card debt?

It’s harder. High existing balances raise your utilization ratio, which is one of Citi’s biggest underwriting factors. Even with a good score, utilization above 50% often leads to denial. Paying balances down before applying is the most effective fix.

Will my balance transfer be declined even if I’m approved for the card?

Yes, it can happen. Card approval and balance transfer approval are separate. Citi caps your total transfer amount at your assigned credit limit (typically around 95% of it). If your requested transfer is larger than your new limit, only the portion that fits will be moved. The rest stays on the original card.

Why was I denied for Diamond Preferred with good credit?

The most common reasons are high utilization on your existing cards, recent large loans or new credit accounts, insufficient reported income, or hitting Citi’s internal credit exposure cap if you already hold other Citi cards. The adverse action notice will list the specific reason.

Does Citi Diamond Preferred have pre-approval?

Yes. Citi offers a free pre-qualification tool on its website that uses a soft credit pull (no impact on your score). Getting pre-qualified is a strong signal but not a guaranteed approval, since final underwriting includes checks the soft pull doesn’t do.

Wrapping Up

Getting the Citi Diamond Preferred approved comes down to more than just your score. A FICO score between 670 and 700+ helps, but other factors are key too. Keep your utilization low, manage recent debt well, report your income honestly, and avoid new applications. These things matter just as much.

To meet Citi’s underwriting criteria, pay down your current debt before applying. Also, use the free pre-qualification tool first. This one-two step protects your score while giving you a real signal on your Citi Diamond Preferred approval odds.

If you know someone stuck paying high interest on credit card debt, share this article. It could save them a wasted hard inquiry and shave months off their payoff plan.