You want to apply for a Citi card, and before you hit submit, you want to know exactly which credit report they’ll look at. That’s smart. A surprise pull on the wrong bureau can waste a hard inquiry, trigger a denial you didn’t see coming, or run headfirst into a credit freeze you forgot to lift. Figuring out which credit bureau does Citi use for credit cards ahead of time saves you all of that.

Citi pulls Experian most often, but the bureau can shift based on your state and the specific card.

Below, you’ll get the state patterns, the card-type differences, what happens with frozen files, how pre-qualification really works, and how to check which report Citi pulled after the fact.

Key Takeaways

This guide explains what credit bureau does Citi use for credit cards, including bureau pull percentages, state and card-type patterns, double pull triggers, credit freeze issues, and steps to take after a denial.

Core Facts:

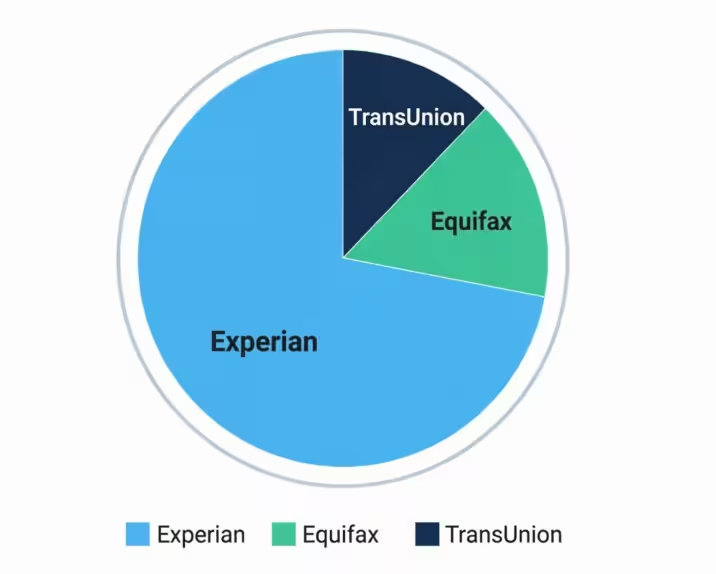

- Citi pulls Experian most often, accounting for roughly 60% to 70% of hard inquiries, based on crowdsourced applicant data rather than an official Citi disclosure.

- Equifax accounts for about 15% to 25% of Citi pulls and TransUnion accounts for about 10% to 20%, according to the same crowdsourced tracking data.

- A double pull occurs when Citi checks two bureaus for one application, often due to a premium card, thin credit file, address mismatch, or a frozen report on the first bureau checked.

- Each hard inquiry typically lowers a FICO score by about 5 points, stops affecting the score after about 12 months, and falls off the credit report after 2 years.

- Citi is legally required to disclose which credit bureau it used in the adverse action notice sent to denied applicants within 30 days.

- Pre-qualification checks use a soft inquiry that does not affect credit scores, while a formal application triggers a hard inquiry that can lower the score.

Best for:

- Readers preparing to submit a Citi credit card application who want to know which credit report to review beforehand.

- Applicants who have a credit freeze in place and need to understand how it could affect a Citi application.

- Anyone denied a Citi card who wants to identify which bureau was used and how to pursue reconsideration.

Which Credit Bureau Does Citi Pull Most Often

For most applicants across the country, Citi pulls Experian. Community-tracked application data over the past several years puts Experian at roughly two-thirds of Citi hard inquiries, with Equifax and TransUnion splitting the rest. So if you can only clean up one report before applying, Experian is the safest bet.

That said, Citi does not publish an official list of which bureau it uses. The bank chooses per application based on its own underwriting rules, your address, and sometimes the card you’re applying for. So “Experian most of the time” is a strong default, not a guarantee.

Knowing the right bureau is important. A hard inquiry stays on that report for two years. If there’s a mistake, like an old collection or a wrong late payment, it can lower your score by 20 to 60 points. If you fix errors on the wrong bureau, the pull may still hurt you.

What the Data Shows

The data on which credit bureau does Citi pull is not official. It comes from crowdsourced trackers where applicants report the exact bureau listed on their denial letter or approval notice. These trackers cover thousands of Citi applications each year.

Here’s roughly what the numbers look like based on the most-cited crowd trackers:

The numbers move a few points year over year, but Experian has stayed on top for a long time. This tells you two useful things. First, if you know nothing else about your application, prep Experian first. Second, do not assume Experian will be pulled just because it usually is. About one in three applicants gets a different bureau. Prepping all three is the only way to remove all doubt.

📌 Did You Know: Citi is legally required to tell you which bureau it used if you’re denied or if you get less favorable terms than you applied for. This disclosure comes in the adverse action notice, mailed or emailed within 30 days.

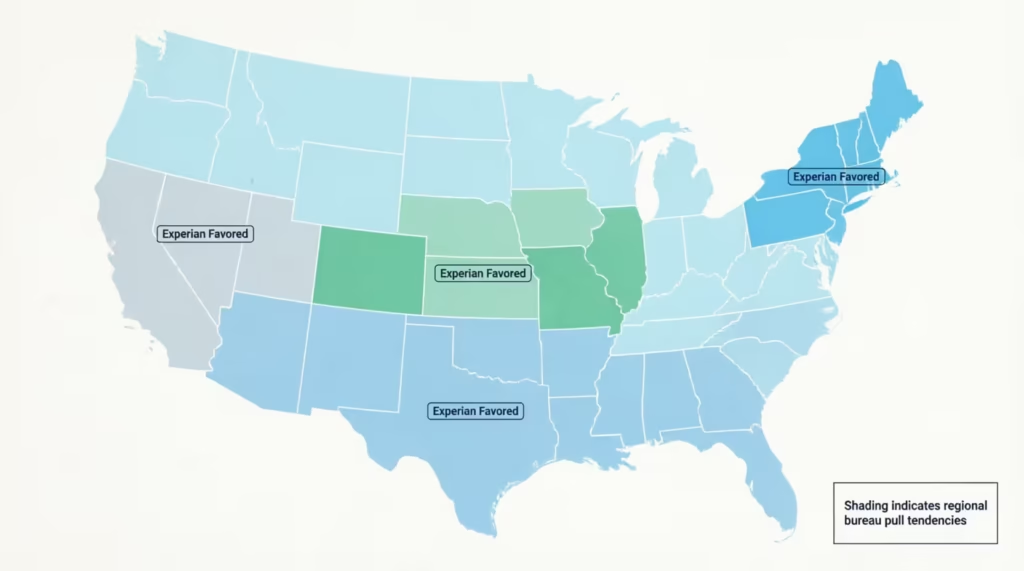

How the Bureau Citi Pulls Varies by State

Where you live can shift the odds. Citi uses different data-sharing agreements and different underwriting flows in different regions. This isn’t random. It’s tied to how each bureau covers different parts of the country and the historical business relationships Citi has in place.

Some rough regional patterns applicants have reported:

- Northeast (New York, New Jersey, Massachusetts, Connecticut, Pennsylvania): Experian is still the most common pull, but TransUnion shows up more often here than in most of the country.

- South (Texas, Florida, Georgia, North Carolina): Experian dominates. Equifax is the usual second pick.

- Midwest (Illinois, Ohio, Michigan, Indiana): Experian first, with a fairly even split between Equifax and TransUnion for the rest.

- West Coast (California, Washington, Oregon): Experian is very strong here. Equifax shows up occasionally.

- Mountain and Plains states: Experian remains the leader, but sample sizes are smaller, so patterns are noisier.

To sanity check this for your own state, look for a recent report from someone in your ZIP code who applied for the same Citi card you want. Reddit’s r/CreditCards and the myFICO forums have long threads where people post their state, card, and the bureau that got pulled. It’s not a scientific sample, but for a single state and a single card, five or ten recent data points usually point in a clear direction.

The state pattern is a probability, not a promise. Citi can still pull a different bureau than the one most common in your state. Prep your top-ranked bureau, and if you want zero risk, review all three.

How the Bureau Citi Pulls Varies by Card Type

The card you apply for also nudges the odds. This isn’t published anywhere. It just shows up in the crowdsourced data over time. Different products go through different underwriting paths, and those paths lean on different bureaus.

Here’s the broad pattern applicants have reported:

- Cash back cards (Citi Double Cash, Citi Custom Cash): Experian is heavily favored. These cards use standardized underwriting, and Experian is the default.

- Travel and premium cards (Citi Strata Premier, formerly Citi Premier): Still Experian-first, but Equifax comes up more often. Premium underwriting sometimes cross-checks a second bureau.

- Co-branded travel cards (Citi / AAdvantage line with American Airlines): More variable. Some applicants report Experian, others Equifax, and a smaller group TransUnion. Co-brand partners can influence the pull.

- Citi business cards (CitiBusiness / AAdvantage): Experian dominates because business underwriting often layers in an Experian Business report alongside your personal credit file.

💡 Pro Tip: If you’re applying for a co-branded card and can’t find the pattern, call Citi’s application status line at 1-800-763-9795 before the pull. They sometimes will tell you which bureau will be used if you ask directly.

The card-type variation is one more reason to lift freezes on all three bureaus before submitting. It’s free, it takes about 10 minutes, and it removes the guesswork entirely.

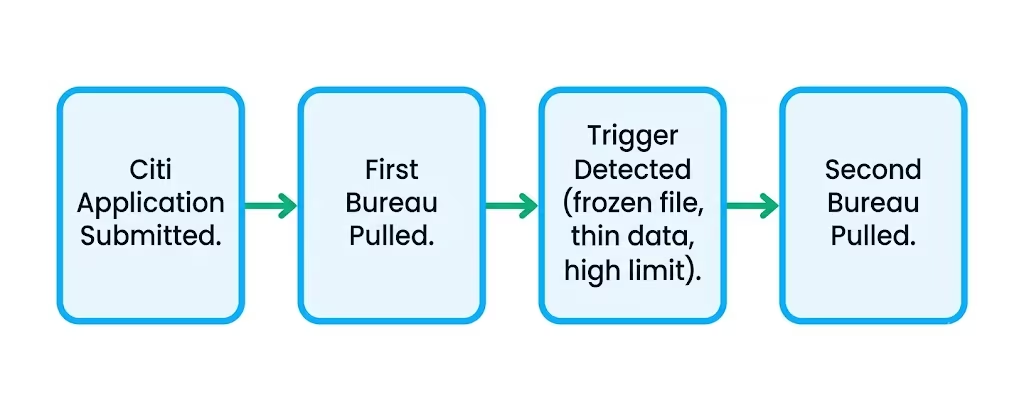

Why Citi Sometimes Pulls More Than One Bureau (“Double Pull”)

Every so often, Citi pulls two bureaus for a single application. This is the “double pull.” It’s not a bug or a mistake. It happens most often when:

- You’re applying for a high-limit or premium card.

- Your file has thin or inconsistent data on one bureau.

- Citi’s system flags something for a second review, like an address mismatch or a recent large inquiry.

- The first bureau returns a file that’s frozen or incomplete.

If Citi pulls your credit twice, you’ll see two hard inquiries on your credit report, one on each bureau. This is what most people worry about, and the worry is usually bigger than the actual impact.

Does a Double Pull Hurt Your Score More Than a Single Pull?

A little, but less than most people think. Each hard inquiry usually drops your FICO score by about 5 points, sometimes fewer. Two inquiries on two different bureaus mean each report shows one new inquiry, not two.

So your Experian score drops around 5 points, and your Equifax score drops around 5 points. Your overall creditworthiness isn’t taking a double hit. It’s taking a normal hit, spread across two reports.

The drop is also temporary. Hard inquiries no longer affect your FICO score after about 12 months, and they fall off the report entirely after 2 years. If you don’t apply for other credit in the next few months, the double pull won’t matter by the time you’re planning your next application.

The real risk with a double pull isn’t the score. It’s the freeze. If either bureau is frozen, Citi can’t finish the second pull, and the application stalls or gets auto-denied. This is why lifting freezes on all three bureaus before applying is the safest move.

What Happens If Your Credit Is Frozen When You Apply

If you have a credit freeze in place and Citi tries to pull that report, one of two things happens. Either the application gets flagged as pending until you lift the freeze, or it gets denied outright with “unable to verify credit” as the reason. Neither is good. Both are avoidable.

A freeze blocks any new lender from seeing your credit file. It doesn’t affect existing accounts, and it doesn’t lower your score. But it does mean Citi’s underwriting system can’t get the data it needs to approve you. If you’ve forgotten which bureaus you froze (or if you froze all three years ago after a data breach), you need to fix this before applying, not after.

The good news: unfreezing is free, takes just a few minutes per bureau, and can be done online or by phone. You can also schedule a temporary lift, which automatically re-freezes your file after a set number of days.

Which Bureau Should You Unfreeze First

Since Experian is the most likely bureau Citi will pull, start there. Log in at Experian’s freeze center, choose “temporary lift,” and set the lift window for 7 to 10 days. That gives Citi enough time to run the pull and complete underwriting.

If you want zero risk of a stalled application, unfreeze all three. It costs nothing, and the extra 10 minutes covers you against a state-driven or card-driven surprise. The official credit freeze guidance from USA.gov walks through the exact steps for each bureau if you’ve never done it before.

Once your Citi application is approved and the pull is done, your freezes will re-lock automatically at the end of your scheduled lift window. You don’t need to remember to re-freeze manually.

⚠️ Mistake to Avoid: Do not fully remove your freezes. Use the temporary lift option instead. A permanent removal leaves your file exposed indefinitely, which defeats the whole reason you froze it in the first place.

Pre-Qualification Checks vs. Formal Applications: Which One Pulls Your Credit

There’s a big difference between checking pre-qualified offers on Citi’s website and submitting a full card application. One is safe. The other affects your score.

Pre-qualification uses a soft inquiry. Citi peeks at a limited version of your credit file, sees whether you match the target profile for any of their cards, and shows you a list. Your score is not affected. Nothing shows up on the version of your report lenders can see. You can check pre-qualified offers as many times as you want.

A formal application uses a hard inquiry. This is the pull we’ve been talking about. It shows up on your report, drops your score a few points, and stays visible to future lenders for two years.

The trick is that pre-qualification isn’t approval. Even if Citi pre-qualifies you for a card, the formal application can still be denied. This is because the hard pull might reveal something the soft pull missed, like a recent late payment, a new balance, or a lower score than expected.

You can check pre-qualified offers at Citi’s pre-qualification tool on their website. It takes about 60 seconds and asks for your name, address, and last four digits of your Social Security number.

Will Checking Pre-Qualified Offers Hurt Your Score

No. A soft inquiry has zero effect on your credit score. It’s the same check you see when you look at your credit report, when a lender checks your account, or when a company sends you a pre-screened offer by mail. Soft inquiries are invisible to other lenders and are not part of FICO’s scoring math.

The only time your score is affected is when you go from pre-qualification to submitting the actual application. That’s when the hard pull happens. So if you’re not sure you want the card yet, run the pre-qualification first. It costs nothing and gives you real information.

How to Find Out Which Bureau Citi Actually Pulled

After you apply, you have two clean ways to find out which bureau Citi pulled.

Option 1: Check your credit reports directly. Go to AnnualCreditReport.com, the only site officially authorized by federal law for free credit reports. According to the FTC, free weekly online credit reports are permanently available from all three bureaus. Pull all three, look at the “recent inquiries” section, and find the one dated the day you applied to Citi. That’s the bureau they used.

Option 2: Wait for your Citi decision letter. Whether you’re approved or denied, Citi is required to tell you the source of the credit report used in the decision. On an approval, it’s usually in the fine print of the welcome kit. On a denial, it’s clearly listed on the adverse action notice. Denial notices are more direct because federal law forces the disclosure to be prominent.

If you’re using a free credit monitoring app (Experian’s free tier, Credit Karma for Equifax and TransUnion), new hard inquiries usually appear within 24 to 72 hours. Set up alerts so you get a push notification the moment a new inquiry hits.

What to Do If You’re Denied Because of a Bureau-Specific Issue

If Citi denies you and the reason ties back to something on your credit report, you have real options. Don’t just accept the denial and try again next month.

Step 1: Read the adverse action notice carefully.

It will list the credit bureau used and the top reasons for the denial (too many inquiries, high utilization, short credit history, derogatory account, etc.).

Step 2: Pull that specific report from AnnualCreditReport.com.

Look for the item the denial mentions. Errors are common. You can dispute old collections, accounts that aren’t yours, and incorrect late payment marks. Often, these can be removed within 30 days.

Step 3: Call the Citi reconsideration line at 1-800-695-5171.

This isn’t a hidden number. It’s a legitimate line where a real underwriter reviews your application by hand. Explain what happened, walk them through any errors you’ve disputed, and ask them to reconsider. Reconsideration approvals happen more often than people expect, especially when there’s a clear error or a specific explanation for a low score.

Step 4: If reconsideration doesn’t work, wait 60 to 90 days.

Clean up the report, let disputed items resolve, and reapply. Don’t chain multiple applications back to back. That creates the exact “too many inquiries” problem that got you denied in the first place.

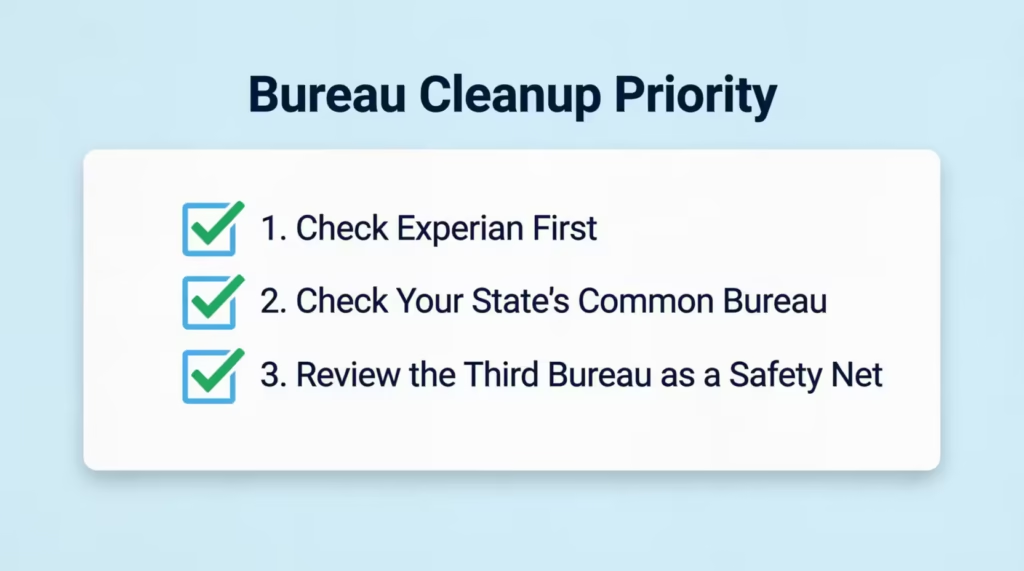

Which Credit Report to Check and Clean Up Before You Apply

Given everything above, here’s the priority order for cleanup, from most important to least:

- Experian first. This is the bureau Citi is most likely to pull. Check it thoroughly. Fix any errors. Dispute anything wrong. This is where 60% to 70% of your risk sits.

- The bureau most commonly pulled in your state next. Look up recent reports from applicants in your state and card type. If TransUnion shows up a lot in your region, clean that one too.

- The third bureau is a safety net. Even if it’s less likely, spending 20 minutes reviewing the third report removes all remaining doubt.

Focus your cleanup on the items that hurt scores the most. High credit card balances (aim to pay them below 30% of your limit, ideally under 10%). Any collection accounts (dispute if incorrect, negotiate a pay-for-delete if correct). Late payment marks (dispute if wrong, wait them out if correct). Old inquiries clean themselves up after 12 to 24 months.

If you want ongoing monitoring, Experian’s free account gives you your Experian report and FICO score. Credit Karma covers TransUnion and Equifax for free. Between the two, you get all three bureaus watched without paying for a premium credit monitoring service.

Give yourself 30 to 60 days between finishing your cleanup and applying. Score changes from disputes and balance drops usually take 30 to 45 days to process. If you apply too early, you might not get credit for your work.

What Citi Reports to the Bureaus After You’re Approved

Once you’re approved and your account is open, Citi starts reporting your activity every month. Unlike the application pull (which usually only hits one bureau), monthly account reporting goes to all three. Every card you have with Citi shows up on all three of your credit reports.

Here’s what Citi typically reports each month:

- Account balance as of your statement closing date

- Credit limit on the card

- Payment status (on time, 30 days late, 60 days late, 90+ days late)

- Payment history for the past several months

- Account age (how long the account has been open)

This is why paying your balance before the statement closes matters more than paying by the due date. The number Citi reports is the statement balance, not the balance after your payment clears. If you charge $2,000 in a month and pay it all off before the statement closes, Citi reports a low balance, which keeps your credit utilization ratio low. That helps your score.

Late payments are the biggest risk. A single 30-day late payment can drop your FICO score by 60 to 100 points and stays on all three reports for 7 years. Setting up autopay for at least the minimum amount protects you from the most damaging reporting mistake you can make.

Missing a payment doesn’t just hurt your score. It also affects your ability to get approved for future cards, including other Citi products. Citi looks at your payment history when you apply for a new card. So, if you consistently pay on time, your next application will go much smoother.

Frequently Asked Questions (FAQs)

What credit bureau does Citi use for credit cards?

Citi pulls Experian most often, accounting for roughly 60% to 70% of hard inquiries based on crowdsourced applicant data. Equifax and TransUnion split the remaining share, and the exact bureau can shift by state and card type.

Does Citi use Experian or Equifax?

Citi favors Experian for most applications, but Equifax shows up more often for premium and travel cards like the Citi Strata Premier. Co-branded cards, like the Citi/AAdvantage line, show more variation between the two.

Is it hard to get approved for a Citi card?

Approval depends on your credit profile rather than the card being universally hard to get. Common denial reasons include too many recent inquiries, high credit utilization, short credit history, or a derogatory account listed on your credit report.

Why would Citi deny me a credit card?

Citi’s adverse action notice typically lists reasons like too many inquiries, high utilization, a short credit history, or a derogatory account. The notice also names the specific credit bureau used, which you can then pull and review for errors.

What’s the difference between a hard inquiry and a pre-qualification check?

Pre-qualification uses a soft inquiry that has zero effect on your credit score, while a formal application triggers a hard inquiry that can lower your score by a few points. Pre-qualifying first lets you gauge your odds without any risk.

Can you apply for a Citi card if your credit is frozen?

A freeze on the bureau Citi tries to pull will stall or auto-deny your application until you lift it. A temporary lift of 7 to 10 days on all three bureaus before applying avoids this problem entirely.

How long does a Citi hard inquiry affect your credit score?

A hard inquiry typically drops your FICO score by about 5 points and stops affecting your score after roughly 12 months. It falls off your credit report completely after 2 years.

Does a double pull from Citi hurt your score more than one pull?

A double pull affects each bureau separately, so your Experian score might drop about 5 points, and your Equifax score drops about 5 points, rather than doubling the damage on one report. The bigger risk is a frozen file stalling the application, not the score impact itself.

What should you do if Citi denies your application?

Read the adverse action notice to find the bureau used and the listed reasons, then pull that specific report from AnnualCreditReport.com to check for errors. You can also call Citi’s reconsideration line at 1-800-695-5171 to have an underwriter manually review your application.

Wrapping Up

Getting approved for a Citi card starts with knowing which credit report they’ll look at. Experian is the safest choice. However, state and card differences, plus occasional double pulls, mean it’s best to check all three reports. Clean up any issues and lift all three freezes before applying.

Pre-qualification is a free, no-risk way to test your odds first. If you’re denied, the reconsideration line is real and worth calling.

Based on everything the data shows, the most effective approach is a full three-bureau prep for anyone serious about approval.

Found this useful? Share it with a friend who’s about to apply for their first Citi card. Ten minutes of prep beats a denial letter every single time.