Applying for a new credit card feels risky when you’re not sure the bank will say yes. A denial doesn’t just sting; it can drop your score, waste a valuable application slot, and delay your plans. If you’re checking your Citi credit card approval odds before you hit “submit,” you’re already thinking smart, because Citi has some of the strictest, most misunderstood application rules of any major issuer.

Your approval depends on your credit score, income, debt load, recent inquiries, and Citi’s own timing rules like the 8/65 policy.

This guide walks you through every factor Citi weighs, how to read your own profile, and the exact steps to boost your chances before you apply.

Key Takeaways

This guide explains how Citi evaluates credit card applications, including credit score tiers, debt-to-income targets, the 8/65 and 48-month timing rules, pre-qualification checks, and reconsideration steps after a denial.

Core Facts:

- Citi evaluates four factors together: credit profile, income and stability, debt load, and Citi-specific rules like existing card count and total credit exposure.

- The 8/65 rule limits applicants to one Citi card approval every 8 days and only two approvals within any 65 days.

- The 48-month rule blocks earning a repeat sign-up bonus on the same card product family within 48 months, but does not block approval itself.

- Citi’s estimated total credit exposure cap across all cards is around $50,000 per consumer, per industry watchers, though Citi does not publish this figure.

- Six or more hard inquiries on the credit bureau Citi pulls within 6 months often trigger an automatic denial regardless of credit score.

- Pre-qualification uses a soft inquiry with no score impact, and a general rule is to wait at least 90 days between Citi applications after a denial.

Best for:

- People planning to apply for a Citi credit card who want to check their approval odds before submitting.

- Applicants who were recently denied by Citi and want to understand fixed versus negotiable denial reasons.

- Points and miles collectors managing multiple Citi card applications who need to track the 8/65 and 48-month rule windows.

What Determines Your Citi Approval Odds

Many people believe a good credit score is enough to guarantee approval. It’s not. Citi conducts a complete review. They consider your score, income, existing debt, housing costs, and the number of Citi cards you have. A person with a 780 FICO score can still get denied if their debt-to-income ratio is too high or if they broke a velocity rule last week.

Citi looks at four core buckets:

- Credit profile: FICO score, length of history, mix of accounts, and payment record.

- Income and stability: gross annual income, job type, and time at current employer.

- Debt load: monthly payments compared to income, plus total revolving balances.

- Citi-specific rules: how many Citi cards you hold, when you last opened one, and your total credit line with the bank.

Your Citi approval chances improve the most when all four buckets line up, not when one is perfect and another is weak. Understanding each one helps you know where you stand before the hard pull hits your report.

Credit Score Benchmarks by Card Tier

Citi does not publish score cutoffs, but real-world approval data from cardholders points to clear tiers. Use these ranges as a working guide, not a promise.

| Card Tier | Typical FICO Range | Example Cards |

|---|---|---|

| Secured / Rebuilding | 580 to 640 | Citi Secured Mastercard |

| Mainstream Rewards | 670 to 720 | Citi Double Cash, Citi Custom Cash |

| Premium Travel | 720 to 780+ | Citi Strata Premier, Citi / AAdvantage Executive |

A score at the low end of a tier can still work if the rest of your file is strong. A high score with recent late payments or a thin file may still fall short. The tier is a starting point, not a finish line.

💡 Pro Tip: Pull your FICO 8 from myFICO or your bank’s free tool before applying. Citi uses FICO Bankcard 8 in most states. This score focuses more on credit card use than regular FICO 8. So, your reported score might look different to the bank.

Income and Debt-to-Income Requirements

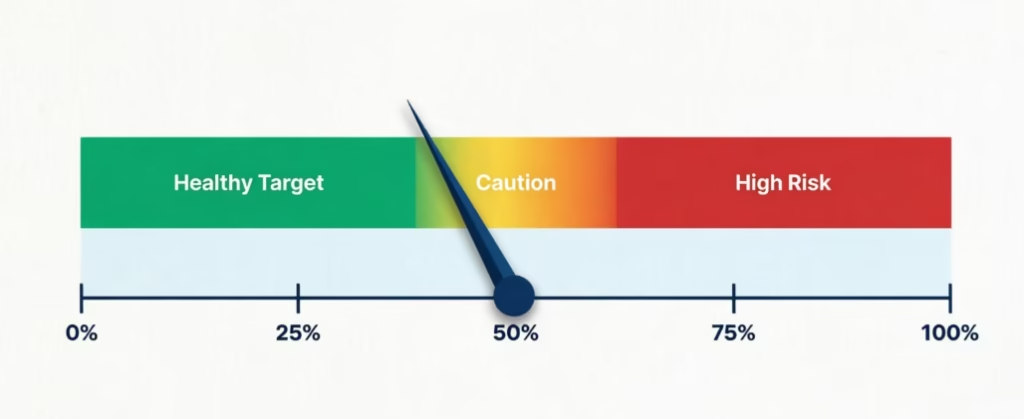

Citi does not post a minimum income figure, but the underwriting model cares deeply about the ratio between what you earn and what you already owe. If you list $60,000 in gross income and $2,800 in monthly debt payments, your back-end debt-to-income sits near 56%, which is a red flag even with a strong score.

The system checks:

- Gross annual income: your full pre-tax pay, including bonuses and side income you can document.

- Housing cost: rent or mortgage, since Citi factors this into your monthly obligations.

- Existing debt payments: minimums on cards, auto loans, and student loans pulled from your credit report.

A healthy target is a total debt-to-income ratio under 40%, with housing under 30% of gross pay. Applicants who fall inside those bands see the fewest income-based denials. Freelancers and gig workers should list net self-employment income, not gross receipts, since Citi may ask for tax returns during review.

How Citi’s Application Rules Affect Your Odds

Citi applies its own timing rules on top of the standard credit review. Break one of these rules and the decision engine will auto-deny even a perfect credit file. These rules are unique to Citi and catch many applicants off guard.

The 8/65 Rule Explained

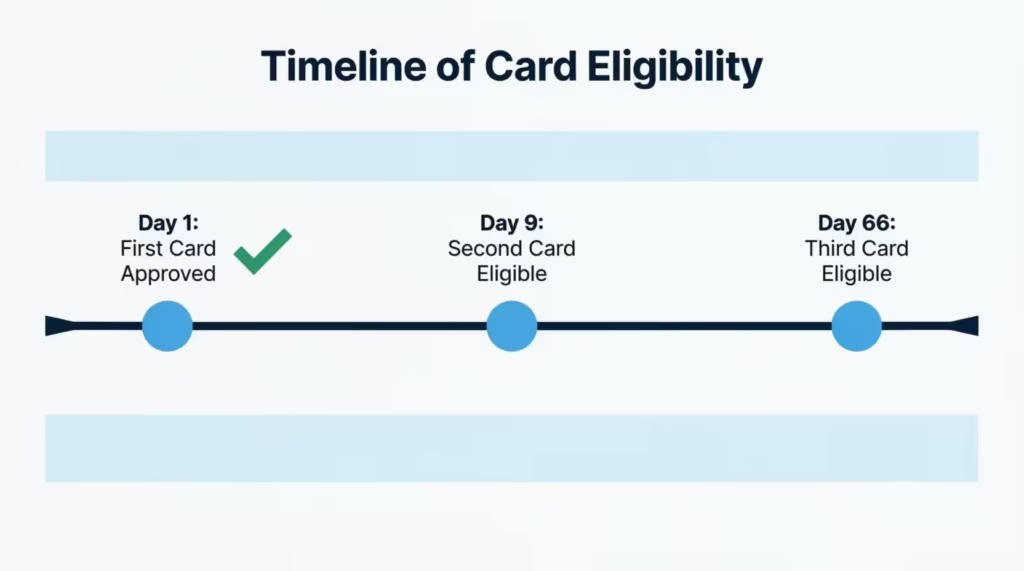

The Citi 8/65 rule limits how quickly you can open new Citi cards. The rule has two parts:

- You can be approved for only one Citi card every 8 days.

- You can be approved for only two Citi cards every 65 days.

The clock starts on the approval date of your last Citi card, not the application date. So if you were approved on day 1, you cannot apply for a second card until day 9. If you were approved for a second card on day 9, you must wait until day 66 from the first approval to try for a third.

Business cards from Citi count toward this rule too. Authorized user accounts do not.

⚠️ Mistake to Avoid: Applying on day 7 hoping the system will “just deny the second one.” It will, and you’ll still take the hard inquiry hit on your report for a card you had zero shot at getting.

The 48-Month Rule and New Approvals

The 48-month rule is different. It does not block approval; it blocks the sign-up bonus. If you earned a welcome bonus on the Citi Strata Premier (or its ThankYou-family cousins) within the past 48 months, you cannot earn that bonus again on the same product family. You can still be approved for the card. You just won’t get the points.

This rule matters most for points-and-miles shoppers chasing sign-up offers. Check your old statements or ThankYou Points history to confirm when you last earned the bonus. This way, you won’t waste an inquiry on a bonus you can’t collect.

How Your Existing Citi Relationship Affects New Approvals

Citi caps how much total credit it will extend to any one person. This cap isn’t published. However, industry watchers estimate it around $50,000 in total credit lines for most consumers. Very strong applicants may see higher amounts.

If you already carry $45,000 in Citi credit across two cards, a new application for a card with a $10,000 starting line will likely push past the cap and trigger a denial. You have two ways around this:

- Ask for a credit line reallocation. Call Citi and ask to move part of the limit from an existing card onto the new one after approval, or offer to lower an existing line before you apply.

- Close a dormant Citi card. If a card sits unused, closing it frees exposure, though it can nudge your utilization ratio up on your other cards, so weigh that trade-off.

Having a Citi checking or savings account can help slightly. It’s not a magic key, but it does give underwriters more data on your finances and can support a manual review.

How Recent Hard Inquiries Affect Citi Approval

Citi is one of the more inquiry-sensitive issuers. Six or more hard inquiries on a single credit bureau in the past 6 months often trigger an auto-decline, even with a strong score. Citi mostly pulls Equifax or Experian depending on your state, so the count on the bureau it pulls matters most.

Inquiries fall off your report after 24 months and stop affecting your score after 12. If you’ve been rate shopping for a mortgage or auto loan recently, wait for the inquiry count to settle before you apply. A soft pull tool, covered in the next section, lets you test the water without adding another hard hit.

Checking Pre-Qualification Before You Apply

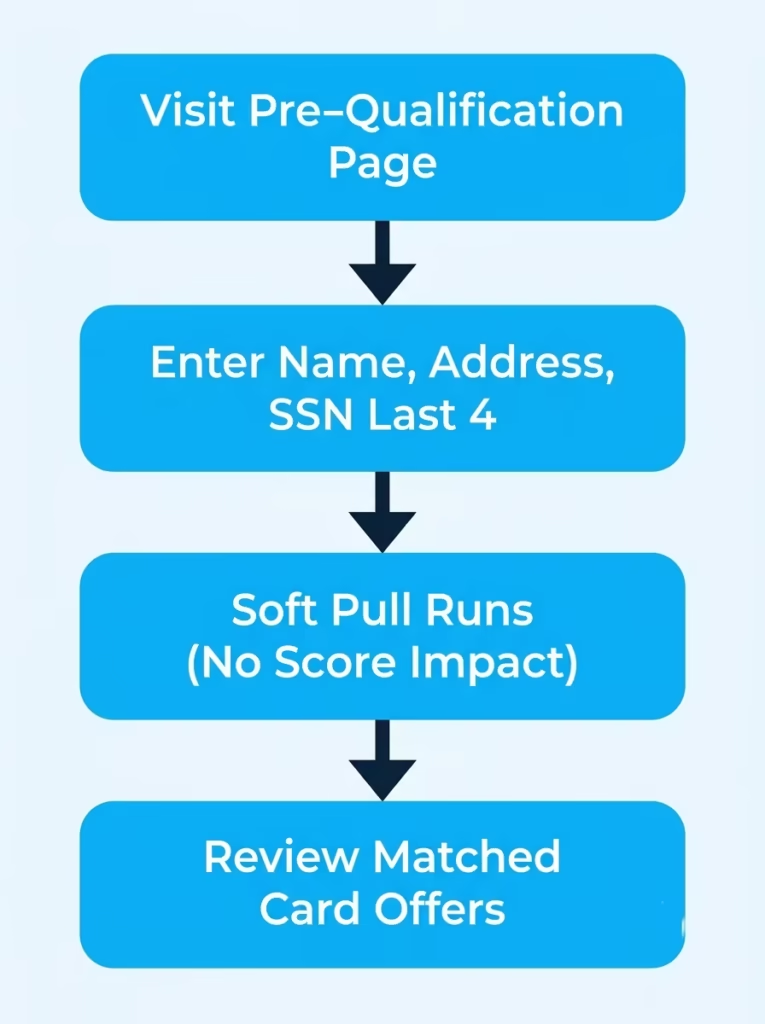

Pre-qualification is a soft inquiry that gives you a strong signal on your Citi approval chances without touching your credit score. It’s the single best move to make before a real application.

To check, visit the Citi Pre-Qualification page and enter your name, address, and the last four digits of your Social Security number. The tool returns a list of Citi cards you’re pre-qualified for, based on a soft pull of your credit file.

A pre-qualified offer is not a guarantee. It means Citi’s marketing model likes your profile, but the full underwriting review still runs when you apply. Even so, pre-qualified applicants see approval rates well above the general pool. If your target card is on the pre-qualified list, your odds are strong. If it isn’t, the profile gap is worth investigating before you spend a hard inquiry.

Matching Your Credit Profile to the Right Citi Card

The right card is the one your profile can actually win. Applying “up” to a premium card with a mainstream file is the most common cause of avoidable denial. Match yourself to your tier:

- Rebuilding tier (FICO 580 to 640): The Citi Secured Mastercard is the realistic pick. It reports to all three bureaus and can graduate to unsecured after a year of on-time payments.

- Mainstream tier (FICO 670 to 720): Citi Double Cash for flat 2% back or Citi Custom Cash for a rotating 5% category. Both approve strong middle-tier files.

- Premium tier (FICO 720+): Citi Strata Premier for travel points or a co-branded card like the Citi / AAdvantage Platinum Select. Expect income verification and a manual review touch on the highest lines.

Read the card page carefully. If the fine print says “excellent credit required” and your score sits at 685, that’s a signal to build first and apply later.

What Happens After You Submit a Citi Application

Once you click submit, one of three things happens:

- Instant approval. The most common outcome for strong files. You see the credit line on screen, and the card ships in 7 to 10 business days.

- Instant denial. Usually caused by a rule break (8/65), a thin file, or a credit freeze. The reasons arrive by mail within 7 to 10 days in an adverse action notice.

- Pending review. Citi’s message says “we need more time” or “your application is being reviewed.” This is a manual review, often triggered by fraud checks, income questions, or being close to the exposure cap.

Pending decisions usually resolve within 7 to 14 days. You can call the application status line at 1-888-201-4523 to check, or call reconsideration to move things forward. Have your income figures, employer details, and existing account balances ready.

Common Reasons Citi Denies Applications

Understanding the top denial reasons helps you spot the problem in your own file before it costs you. Citi’s most common triggers include:

- Too many recent inquiries on the pulled bureau, usually 6 or more in 6 months.

- Thin credit file, meaning fewer than 3 open accounts or under 12 months of history.

- High utilization, typically above 30% across all revolving accounts, and especially above 50%.

- Exceeding Citi’s total credit exposure cap with existing Citi accounts.

- Breaking the 8/65 rule, even by one day.

- Debt-to-income too high, usually above 45% to 50%.

- Recent derogatory items, such as a late payment in the last 12 months or a collection in the last 24 months.

- Unverifiable income or a mismatch between the number on the form and what documents show.

The adverse action notice you receive by mail lists the top four reasons, in Citi’s order of importance. Read it carefully. It’s the roadmap for your next move.

What to Do If Citi Denies Your Application

A denial is not the final answer. Many Citi decisions get flipped through a short phone call and a clear explanation. Move quickly, though, because the window closes fast.

Calling the Citi Reconsideration Line

Call the Citi reconsideration line at 1-800-763-9795 for consumer cards. Some applicants also report success on the general new applications line at 1-800-950-5114.

When the analyst picks up, be brief and specific:

- State your name, application reference number, and the card you applied for.

- Ask which reason on the adverse action notice weighed the most.

- Offer to move credit from an existing Citi card if the issue is total exposure.

- Clarify any income or employment detail that may have been misread.

- Ask politely if the analyst can requeue the application for a second review.

Keep the call under 10 minutes. Analysts respond to prepared, calm applicants. If the phone route stalls, you can also submit a written appeal through the Citi secure message center inside your online account.

What’s Negotiable vs. Fixed Citi Policy

Not every denial reason is open for discussion. Knowing the difference saves you time.

| Fixed (No Appeal) | Negotiable (Worth Asking) |

|---|---|

| 8/65 rule violations | Total credit exposure cap |

| 48-month bonus eligibility | Income figure interpretation |

| Bankruptcy in past 24 months | Recent late payment context |

| Fraud alert conflicts | Utilization at time of pull |

| Active credit freeze (until lifted) | Employment history questions |

If your denial is on the left side, save your credits and reapply later. If it’s on the right, a reconsideration call is worth the effort.

How Long to Wait Before Reapplying

The right wait time depends on the denial reason. Reapplying too soon just repeats the outcome and adds another inquiry.

- 8/65 rule denial: wait exactly the number of days that closes your rule window, then apply.

- Too many inquiries: wait until you’re back under 6 in 6 months, usually 3 to 6 months.

- High utilization: pay balances down and wait one full statement cycle so the lower number reports.

- Income or DTI: wait until you can document a higher figure or lower your monthly debt payments.

- Thin file: wait 6 to 12 months while you build history on your existing accounts.

A general rule holds well: wait at least 90 days between Citi applications unless you have clear evidence the underlying issue is fixed.

Steps to Improve Your Approval Odds Before Applying

You have real control over most approval factors. Work through this checklist in the 30 to 60 days before you apply.

- Pull all three credit reports for free at AnnualCreditReport.com. Look for late payments that shouldn’t be there, accounts you don’t recognize, and old collections past the reporting limit.

- Dispute any errors with the bureau reporting them. Corrections often take 30 days but can lift your score by 20 to 60 points if a real mistake gets removed.

- Lower your utilization. Pay balances down before your statement date, not the due date, so the lower number reports. Aim for under 10% on each card and under 30% overall.

- Do not open other credit accounts in the 60 days before your Citi application. Every new inquiry and new account works against you.

- Confirm your income figure. List gross annual income, including bonuses, tips, and documented side income. Married applicants can include a spouse’s income they have reasonable access to.

- Run the Citi pre-qualification tool the day before you apply. If your target card is not on the list, hold off.

- Check your last Citi approval date to confirm you clear the 8/65 window.

- Unfreeze the bureau Citi pulls in your state (usually Equifax or Experian) before you submit. A frozen file causes an automatic denial.

📌 Did You Know: Paying your credit card before the statement closing date, not just before the due date, is the fastest way to drop your utilization on your next credit pull. This one habit can shift your score by 10 to 40 points in a single month, with no fees and no waiting.

Frequently Asked Questions (FAQs)

Is it hard to get approved for a Citibank credit card?

Citi is stricter than most issuers because it layers timing rules like 8/65 on top of standard credit checks. Even a 780 FICO score can get denied for high debt-to-income, too many recent inquiries, or exceeding Citi’s credit exposure cap.

What is the minimum credit score for a Citi card?

Citi doesn’t publish a minimum score, but real-world data shows secured cards approve in the 580 to 640 range. Mainstream rewards cards like Double Cash typically need 670 to 720.

Can I get a Citi credit card with a 600 credit score?

A 600 score fits the secured or rebuilding tier, so a card like the Citi Secured Mastercard is realistic. Mainstream or premium Citi cards usually require 670 or higher, so a 600 score would likely mean denial on those.

What is the easiest Citi card to be approved for?

The Citi Secured Mastercard is the easiest to get approved for, typically requiring a FICO score between 580 and 640. It reports to all three credit bureaus and can graduate to an unsecured card after a year of on-time payments.

What is the hardest Citi card to get approved for?

Premium travel cards like the Citi Strata Premier or Citi/AAdvantage Executive are the hardest to get, usually requiring scores of 720 or higher. These cards often trigger income verification and manual review for the highest credit lines.

What FICO score does Citibank use?

Citi uses FICO Bankcard 8 in most states, a score that weighs credit card usage more heavily than a standard FICO 8. This means the score you see from a free tool may differ from what Citi actually pulls.

What is better, Chase or Citibank?

This comparison isn’t something a factual answer can be pulled from Citi’s own approval criteria, since it depends on which specific cards, rewards categories, and personal spending habits you’re comparing. Each issuer has different strengths, so the better choice depends on your goals.

How rare is an 830 FICO score?

An 830 FICO score sits at the very top of the 720+ premium tier Citi looks for on its highest-tier travel cards. Scores this high are uncommon and reflect a long history of on-time payments and low utilization, well above what’s needed even for premium Citi approval.

What credit score do I need to get a $5000 credit card?

The credit limit you’re offered isn’t tied to a single score threshold in Citi’s model; it depends on your income, existing debt, and total credit exposure with the bank rather than the limit amount alone. Applicants in the mainstream tier (670 to 720 FICO) with low debt-to-income are more likely to see limits in that range.

How long should I wait before reapplying to Citi after a denial?

The wait time depends on your denial reason. For an 8/65 rule violation, wait exactly until your rule window clears; for too many inquiries or high utilization, waiting 3 to 6 months while the numbers improve is typically enough.

Wrapping Up

Getting a “yes” from Citi comes down to matching a clean credit profile with the right card, staying inside the 8/65 window, and clearing recent inquiries before you apply.

The best way is simple. First, check pre-qualification. Next, fix errors. Then, pay down balances before the statement closes. Finally, time your application to Citi’s rules, not your excitement. Approach it with data, not hope, and your Citi credit card approval odds shift firmly in your favor.

If you know someone stuck at “should I apply?” with a Citi card, share this guide with them; it could save them a hard inquiry and 65 days of waiting.