I’ve spent years helping readers figure out whether their credit profile actually stacks up before they hit “submit” on a card application. And the Citi Double Cash is one of the trickiest to gauge, because it sits in that awkward space between “starter cash-back card” and “prime credit product.”

A lot of borderline applicants aren’t sure if their score, income, or existing Citi account will help them or hurt them. That’s exactly why understanding the real Citi Double Cash approval odds matters before you apply.

Most applicants with a FICO score of 700 or higher, clean recent credit activity, and stable income get approved. Keep reading for the exact score ranges, non-score factors, pre-qualification steps, and a full reconsideration plan if you’re denied.

Key Takeaways

This guide explains how credit score, income, utilization, recent inquiries, and existing Citi relationships determine Citi Double Cash approval odds, plus reconsideration steps after a denial.

Core Facts:

- A FICO score of 670 or higher is the general baseline for approval, though most approved applicants have scores between 700 and 750.

- Citi enforces an 8/65 rule: no more than one Citi application every 8 days and no more than two Citi applications every 65 days, and breaking either triggers automatic denial.

- Citi generally prefers fewer than 6 hard inquiries from any lender in the past 12 months and no more than 2 in the past 6 months.

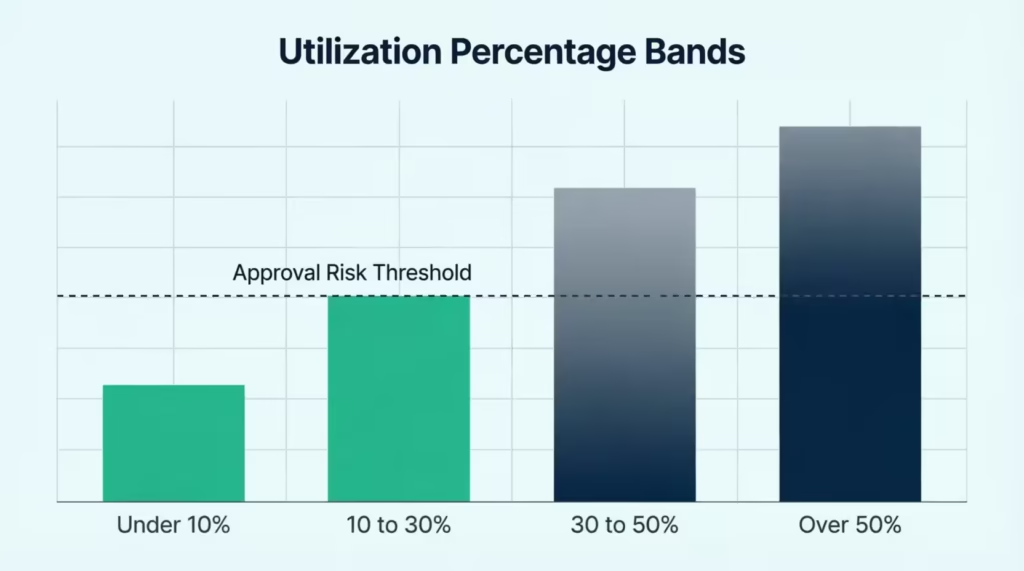

- Keeping credit utilization under 10% at the time of application supports approval, while utilization above 50% is a common denial trigger.

- Citi’s pre-qualification tool uses a soft credit pull that does not affect your score, and results appear within seconds.

- If denied, applicants can call Citi’s reconsideration line at 1-800-695-5171 within 30 days of the adverse action notice to request a review.

Best for:

- Applicants with borderline credit scores between 630 and 670 deciding whether to apply now or wait.

- People who were recently denied and want to understand reconsideration options before reapplying.

- Existing Citi customers evaluating how their current account and credit exposure affect a new application.

Credit Score You Need for the Citi Double Cash Card

The Citi Double Cash Card is marketed to people with “good to excellent” credit. In FICO terms, that means a score of 670 or higher sets the baseline, though most approvals cluster around 700 to 750. Citi does not publish an official minimum score, but underwriting patterns and reader reports point to the same range.

A FICO score of 670 marks the start of the “good credit” tier, according to FICO’s own scoring bands. Anything below that is in the “fair” range. In this case, flat-rate 2% cash back cards from major issuers usually won’t approve applicants unless there are strong offsetting factors.

Citi typically pulls your Equifax report, though this can vary by state and region. If your Equifax score is weaker than your TransUnion or Experian score, that alone can shift your odds. Check all three before you apply.

Here’s a quick view of how score bands tend to play out with this card:

| FICO Score Range | Typical Result | What Usually Helps |

|---|---|---|

| 750+ | Very likely approved | Clean file, low utilization |

| 700 to 749 | Likely approved | Steady income, few inquiries |

| 670 to 699 | Possible, not certain | Low balances, no recent apps |

| 630 to 669 | Long shot | Existing Citi account, high income |

| Below 630 | Very unlikely | Build score first |

Keep in mind, the score is just the entry ticket. Citi still looks at your full credit file before deciding.

If Your Score Is in the Borderline Range (630–670)

Applying with a score between 630 and 670 is a gamble. Some readers in this band do get approved, but the odds tip against you unless something else in your file is strong. What can offset a borderline score?

- A long, clean payment history with no late payments in the last 24 months

- Low credit utilization, ideally under 10% across all cards

- Steady, verifiable income that comfortably covers your existing debts

- Few or no hard inquiries in the past 6 months

- An existing Citi account in good standing

If none of these apply to you, a hard inquiry from a likely denial can cost you 5 to 10 points and stay on your report for two years. Waiting a few months to build your score is often the smarter move. A safer first step is Citi’s pre-qualification tool, which uses a soft pull and won’t hurt your credit.

💡 Pro Tip: If your score is 660 and you have a late payment from 2023, work on aging out that late payment. Also, make sure your utilization is below 10% before you apply. A three-month wait can lift your score enough to move from “maybe” to “very likely.”

Non-Score Factors That Affect Your Approval Odds

Your credit score gets the most attention, but Citi’s decision doesn’t rest on it alone. Underwriting looks at your whole financial picture. Three factors matter most beyond the score itself: income and debt, credit utilization, and recent hard inquiries.

Income and Debt-to-Income Expectations

Citi asks for your annual income because it wants to see that you can handle a new credit line. There’s no published income minimum for the Double Cash, but most approved applicants report household incomes of $30,000 or more. Higher incomes generally support higher starting credit limits.

Your debt-to-income ratio (DTI) also matters. This is the share of your monthly gross income that already goes to debt payments. A DTI below 36% is considered healthy by most lenders. If your DTI is above 45%, expect a lower limit or a decline even with a decent score.

Be honest on the application. Overstating income can trigger a verification request and delay your approval by weeks.

How Credit Utilization Affects Your Application

Credit utilization is the percentage of your available credit that you’re currently using. It’s one of the biggest levers in credit scoring, second only to payment history. Aim to keep total utilization under 30%, and ideally under 10% in the month you apply.

Here’s why this matters for the Double Cash specifically. Citi sees high utilization as a sign of cash flow stress. If your other cards are near their limits, Citi worries about adding more exposure. That can push your file into the “decline” pile even with a 700+ score.

Pay balances down before you apply. Some readers pay their statement balance a week early to make sure the lower number is reported to the bureaus before Citi pulls the file.

Recent Hard Inquiries and Your Odds

Citi is one of the stricter issuers on inquiries. Too many recent hard pulls signal that you’re actively seeking credit, which raises the risk of default.

Citi also enforces its own application limits, known as the 8/65 rule. According to Doctor of Credit, the rule works like this: no more than one Citi application every 8 days, and no more than two Citi applications every 65 days. Breaking either rule triggers an automatic denial, even if your credit is strong.

For inquiries from other lenders, Citi generally prefers to see fewer than 6 hard pulls in the last 12 months, and no more than 2 in the last 6 months. If you’ve been shopping for a mortgage, auto loan, or several cards, wait a few months before adding this one.

⚠️ Mistake to Avoid: Applying for the Double Cash within 7 days of another credit card application. Citi is known to auto-deny if any inquiry, from any issuer, hits your report within the past week.

How an Existing Citi Relationship Affects Your Approval

If you already hold a Citi card, your odds shift in interesting ways. On one hand, Citi already knows how you handle their credit. A well-managed account with on-time payments and low utilization builds trust. On the other hand, Citi has an overall exposure cap for each customer. That means the total credit line Citi is willing to extend across all your cards is limited by their view of your file.

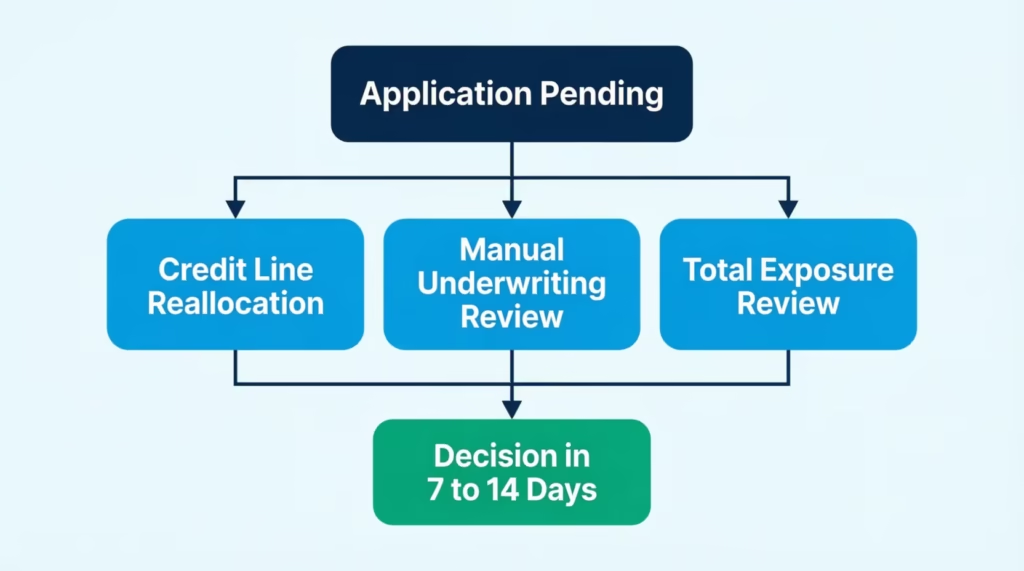

If you’re already near that internal cap, a new application often ends in one of three ways. Citi may approve you with a smaller starting limit. Citi may ask you to reallocate credit from an existing card to the new one. Or Citi may pause the decision and mark it as “application pending” while it reviews your total exposure.

Being a longtime customer helps, but it doesn’t override the score, income, or inquiry rules. If your existing Citi card has late payments or was recently charged off, your new application will almost certainly be denied.

What “Application Pending” Usually Means

If your application status shows “pending” or “under review” instead of an instant approval or denial, don’t panic. This usually happens for one of these reasons:

- Credit line reallocation needed — Citi wants to move part of an existing card’s limit to the new card.

- Manual underwriting — A human reviewer is checking something specific, like income verification or a recent inquiry.

- Total exposure review — Citi is deciding whether to raise their overall exposure to you.

The typical timeline is 7 to 14 business days. You can check status through the Citi application status page using your application ID and ZIP code.

If the wait drags past 10 days, call Citi. Ask if they need any documents from you, or offer to reallocate credit from an existing card if you already have one with Citi. That single phone call has flipped many “pending” cases into approvals.

Checking Pre-Qualification Before You Apply

Before you risk a hard inquiry, check pre-qualification first. This is the single most important step for anyone with a borderline profile, and it’s free.

Citi’s pre-qualification tool uses a soft credit pull, which does not affect your score. You enter your name, address, and the last four digits of your Social Security number. Citi checks your file and shows you which of their cards you’re likely to be approved for.

Access the tool directly at the Citi pre-qualification page. Results appear in seconds.

A few things to know about the results:

- If the Double Cash appears in your offers, your odds of approval are strong, though not guaranteed.

- If it doesn’t appear, Citi’s soft pull found something that puts approval in doubt. This is not a hard denial, but it’s a warning sign.

- The tool doesn’t guarantee your final credit limit or the exact APR you’ll receive.

- Pre-qualification offers refresh periodically, so check back in a few weeks if you don’t see the card the first time.

The soft pull vs. hard pull distinction matters. As Citi explains in its own pre-qualification guide, soft inquiries are only visible to you and don’t lower your score. A hard inquiry, which happens when you submit a full application, can drop your score by 5 to 10 points.

📌 Did You Know: Even if you don’t see the Double Cash in your pre-qualified offers today, checking monthly is free and safe. Citi’s targeting model updates regularly, and the same profile that gets “no offer” in March might see the Double Cash in June.

Does Payment Timing Affect Approval, or Just Rewards?

This is one of the most common points of confusion for Double Cash applicants. The card’s headline feature is 2% cash back, structured as 1% when you buy and 1% when you pay off those purchases. That payment mechanic is a rewards structure, not an approval factor.

To be clear:

- For approval: Citi looks at your overall payment history across all your credit accounts. Late payments in the last 24 months hurt your odds. On-time payments help.

- For rewards: Once you’re approved, you earn the second 1% only after you pay for the purchase. Carrying a balance means you still earn the first 1%, but you’ll pay interest that wipes out the value.

The two are separate. Paying your bill on time is critical for both, but for different reasons. Approval underwriting looks at your payment history on your credit reports. The rewards engine looks at whether that specific purchase has been paid off.

So no, the 2% rewards structure has zero effect on whether Citi approves you. What matters is your track record on other accounts. According to FICO’s official breakdown, payment history makes up 35% of your credit score, the single largest factor.

Common Reasons Citi Double Cash Applications Get Denied

Even applicants who feel confident sometimes get denied. Understanding the top reasons helps you spot risk before you apply. These are the most frequent triggers for a Double Cash denial:

- Credit score below 670. The card is designed for good-to-excellent credit. Scores under 670 rarely clear the automated screen.

- High credit utilization. Anything above 50% on your existing cards signals stress. Even a great score can be overridden by high balances.

- Too many recent inquiries. More than 5 to 6 hard pulls in the past year is a red flag. Any inquiry within the past 7 days often triggers an auto-decline.

- Breaking the Citi 8/65 rule. Applying too soon after another Citi card is an automatic denial, regardless of your other qualifications.

- Income too low relative to requested credit. If your stated income can’t support additional debt, Citi passes.

- Existing Citi exposure is already high. If Citi already extends you significant credit, they may decline a new card to limit their risk.

- Recent negative marks. Late payments in the last 12 months, collections, charge-offs, or bankruptcy filings make approval very difficult.

- Data errors or fraud alerts. A frozen credit file, a mismatched address, or an active fraud alert can block the application. Check your reports before applying.

If more than one of these applies to you, hold off. Fix the biggest issue first, then reapply in 3 to 6 months.

What to Do If You’re Denied for the Citi Double Cash Card

A denial isn’t necessarily final. Citi is one of the more reconsideration-friendly issuers, and a well-timed phone call can flip a decline into an approval.

Step 1: Read your adverse action notice. Citi is required by federal law under the Equal Credit Opportunity Act to send you a written explanation within 30 days. This notice lists the exact reasons for the denial. Read it before you do anything else.

Step 2: Call the Citi reconsideration line. The number is 1-800-695-5171. Call within 30 days of your denial for the best chance at a review.

Step 3: Use a clear, calm script. A sample script:

“Hi, I recently applied for the Citi Double Cash Card and received a denial. I’d like to request a reconsideration. I understand the reasons listed in my adverse action notice, and I’d like to address them. Can you review my application again?”

Then, respond to the specific reason from your notice. If it was too many inquiries, explain why (mortgage shopping, one-time card review) and confirm you have no plans to apply for more. If it was high utilization, mention that you’ve paid balances down since the application. If it was credit exposure with Citi, offer to reallocate credit from an existing Citi card.

Step 4: Know when reconsideration is a lost cause. If your denial was for a score under 620, a recent bankruptcy, a very recent charge-off, or breaking the 8/65 rule, reconsideration rarely works. Save the phone call and focus on rebuilding.

Step 5: If reconsideration fails, wait at least 6 months before reapplying. Use that time to fix the specific issues from your denial notice.

Steps to Improve Your Approval Odds Before Applying

If you’re not sure your profile is strong enough today, the good news is that most weak spots can be fixed in a few months. Work through this checklist before you apply.

Pay down your credit card balances. Target under 10% utilization on each card and across your total credit. This is the single fastest lever. Paying down $2,000 on cards that were at 60% utilization can raise your score by 20 to 40 points within one billing cycle.

Check your credit reports for errors. Pull your free reports from all three bureaus at AnnualCreditReport.com, the only federally authorized source. Dispute any incorrect late payments, collections, or account balances. Errors are more common than most people realize.

Use Citi’s pre-qualification tool. Before you apply, check the Citi pre-qualification page. A soft pull tells you your odds without any risk to your score.

Space out your applications. Avoid applying for any other credit card within 30 days before or after your Double Cash application. If you’re a Citi customer, respect the 8/65 rule strictly. One Citi app every 8 days, no more than two every 65 days.

Increase your reported income if it’s changed. If you’ve had a raise, a new job, or a new income stream that isn’t reflected on your last credit application, update it. Higher verified income supports a higher approval likelihood and a bigger credit limit.

Age your accounts. If you have new cards from the last 6 months, wait until they’ve been open a bit longer. Citi views very new files as riskier. A little patience often does more for your odds than any other single change.

Address specific denial reasons if you’ve been declined before. Don’t reapply blindly. Fix what the adverse action notice flagged first.

Follow this checklist for 60 to 90 days, and most borderline applicants see their odds move from “risky” to “likely.”

Frequently Asked Questions

What credit score do I need for the Citi Double Cash card?

A FICO score of 670 or higher is generally required, though most approved applicants have scores of 700 or above. Citi does not publish an official minimum. Anything below 670 is unlikely to get approved. Strong offsetting factors, like low utilization or a current Citi relationship, can help.

Can I get approved for Double Cash with a 650 score?

It’s possible but not likely. A 650 score sits in the “fair” credit range, below the card’s target audience. Approval at this level usually needs low utilization. It also requires stable high income, no recent late payments, and few or no hard inquiries. Check pre-qualification first before risking a hard pull.

Does Citi Double Cash have pre-approval?

Yes. You can check pre-qualification through Citi’s official pre-qualification tool, which uses a soft credit pull and does not affect your score. If the Double Cash appears in your pre-qualified offers, your approval odds are strong. If it doesn’t appear, applying is riskier.

Why did I get denied for Citi Double Cash with good credit?

Even with a score over 670, you can be denied for high credit utilization, too many recent hard inquiries, insufficient income, high total exposure with Citi, or breaking the 8/65 rule. Read your adverse action notice carefully to see the exact reason, then call the reconsideration line at 1-800-695-5171.

Does having a Citi card already help or hurt my Double Cash application?

It usually helps, as long as your existing account is in good standing with on-time payments. Citi values existing customer relationships. However, if your total credit exposure with Citi is already high, your new application may get a smaller limit or a “pending” status while Citi decides whether to reallocate credit or extend more.

Wrapping Up

Applying for the Citi Double Cash Card is not a coin flip if you know what to check first. Your score matters, but so do utilization, recent inquiries, income, and any existing relationship with Citi.

For borderline applicants, start by checking pre-qualification. Then, address the biggest issue in your file. Finally, submit a full application. That single sequence protects your score and gives you the strongest shot at approval.

If you know someone weighing a cash-back card application while sitting on a borderline score, share this guide with them. It could save them a wasted hard inquiry and a bruised credit report.