I know that sinking feeling when you scan your Citi statement and spot a charge that doesn’t add up. Maybe it’s from a merchant you don’t recognize, or maybe you canceled a subscription months ago, and it’s still billing you.

Either way, you’re probably wondering if you even have a real case, and if you do, exactly what to click, call, or write. Learning how to dispute a Citibank credit card charge starts with understanding your rights and following the steps in the correct order.

Here’s the short answer: you can dispute the charge online through your Citi account, by phone, or by mail, and federal law gives you 60 days from your statement date to do it.

Below, you’ll find every step laid out clearly, from figuring out if your situation qualifies to what happens if Citi says no. By the end, you’ll know exactly what to do next.

Key Takeaways

This guide explains how to dispute a Citibank credit card charge, including which charges qualify, filing methods, the 60-day deadline, and what happens if a dispute is denied.

Core Facts:

- The Fair Credit Billing Act gives cardholders 60 days from the statement date to file a written dispute for a billing error or unauthorized charge.

- Disputes can be filed online through Citi’s website or app, by phone at 1-800-950-5114, or by mail to Citibank Customer Service in Sioux Falls, SD.

- A phone call does not satisfy the federal writing requirement; a written dispute must follow to receive full legal protection.

- Citi has up to two billing cycles, or a maximum of 90 days, to investigate and resolve a dispute.

- The disputed amount is set aside and should not accrue interest while Citi investigates, but the rest of the statement balance still must be paid on time.

- If a dispute is denied, the cardholder generally has 10 days from the notice date to respond before payment on the amount is required again.

Best for:

- Cardholders who spot an unauthorized, duplicate, or incorrect charge on a Citi statement and need to know their filing options.

- Anyone who canceled a subscription but was still billed and wants to formally dispute the charge.

- Readers whose dispute was denied and are looking for the escalation steps to challenge the outcome.

What Charges You Can (and Can’t) Dispute

Not every charge you’re unhappy about counts as something you can formally dispute. Before you spend time gathering documents and filing paperwork, it helps to check whether your situation actually qualifies as a billing error.

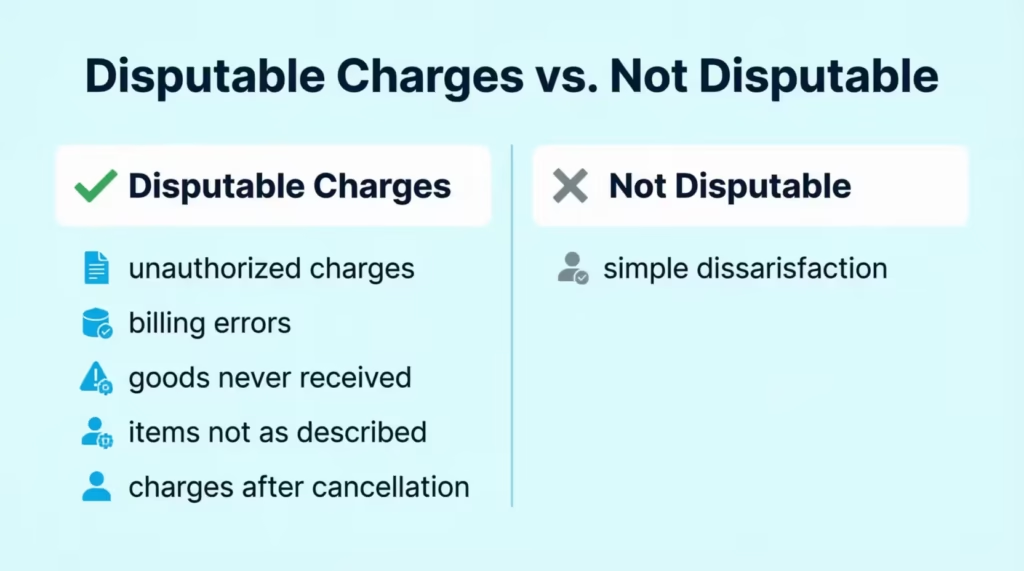

Charges you can typically dispute include:

- Unauthorized or fraudulent charges. Someone used your card, or your card number, without your permission.

- Billing errors. The charge shows the wrong amount, the wrong date, or shows up twice on your statement.

- Goods or services never received. You paid for something that never arrived and never will.

- Items not as described. What you received is significantly different from what the merchant advertised.

- Charges after cancellation. You canceled a subscription or recurring service, but the merchant billed you anyway.

There’s one category that doesn’t qualify on its own: simple dissatisfaction. If the product works exactly as described but you just don’t like it, that’s a return or refund conversation with the merchant, not a billing dispute. The Fair Credit Billing Act treats these as two different things. Billing errors and unauthorized charges get federal dispute protection. Buyer’s remorse doesn’t.

If your situation matches one of the categories above, you have solid grounds to move forward. If you’re not sure which category fits, that’s fine. The next few sections will help you figure out the right path either way.

Try Resolving It With the Merchant First

Before you contact Citi, it’s worth reaching out to the merchant directly, especially if the issue isn’t fraud. Merchants usually have faster access to your order history and can often fix a mistake in minutes rather than weeks.

There’s one clear exception: if you believe your card was used without your knowledge, skip the merchant entirely and go straight to Citi. Contacting a stranger who fraudulently charged your card doesn’t help, and it could tip them off that the card is still active.

For other issues, such as a wrong amount, a canceled subscription that still charges, or a return that was not credited, try contacting the merchant first with a quick call or email. This step is something Citi may ask about, so having an answer ready will make your case stronger.

When you contact the merchant, jot down a few details for your records:

- The date you reached out

- Who you spoke with, if you have a name

- What they told you, in their own words

- Any reference or confirmation number they gave you

If the merchant refuses to help, doesn’t respond, or you’re getting nowhere, you now have a clear reason to escalate to Citi, and you’ll already have documentation ready to support your case.

What to Gather Before You Contact Citi

Walking into a dispute call or online form without the right information usually means starting over later. A little prep work now saves real time down the line.

Before you reach out to Citi, gather the following:

- Your account number and card details, so the representative or system can pull up your account instantly

- The exact transaction date, dollar amount, and merchant name as it appears on your statement

- A clear explanation of why you’re disputing the charge (unauthorized, wrong amount, never received, and so on)

- Supporting documents, such as receipts, order confirmations, cancellation emails, or any messages you exchanged with the merchant

One detail trips people up often: never send original documents. Make copies or scans of everything and keep the originals in your own files. If Citi or the merchant needs additional proof later, you’ll still have the source material on hand.

💡 Pro Tip: Take a screenshot or photo of the charge on your statement the moment you spot it. Statements and account views can update, and having a timestamped record protects you if the transaction detail changes or disappears later.

Once you have these pieces together, you’re ready to file through whichever method works best for you: online, by phone, or by mail.

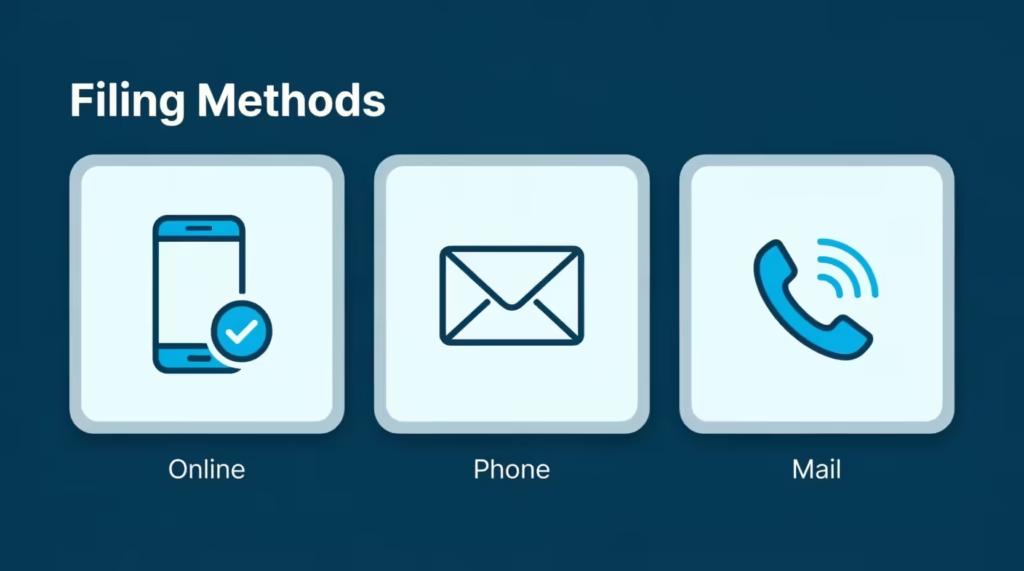

How to Dispute a Charge Online or Through the Citi App

Filing online is the fastest method for most cardholders, and it’s the one Citi steers you toward first. Here’s how it works:

- Log in to your Citi account through the Citi Online website or the Citi Mobile® App, available on the Apple App Store and Google Play.

- Go to your account activity and locate the transaction you want to dispute.

- Select the charge, then look for an option labeled “Dispute Charge” or “Report a Problem.”

- Follow the on-screen prompts, which will ask for the reason behind your dispute and let you upload supporting documents.

- Submit the dispute and watch for a confirmation message or email verifying Citi received it.

After you’ve filed, you can track progress through the Citi Dispute Center inside your online account. This is where you’ll see status updates and any requests for more information as your case moves through investigation.

One small thing worth noting: the exact button names and menu paths can shift slightly with app updates. If you don’t see “Dispute Charge” right away, look for wording like “Something wrong with this transaction?” near the transaction details. The function is there even if the label varies.

How to Dispute a Charge by Phone

Filing by phone works well if you’d rather talk to a person, especially for something urgent like a card you believe was stolen. Call Citi customer service at 1-800-950-5114, or 1-877-693-0218 if you’re hearing impaired. Both numbers are also printed on the back of your physical card.

When you get through, be ready to explain:

- Your name and account number

- The date and amount of the disputed transaction

- The merchant’s name as it appears on your statement

- Why you believe the charge is wrong

The representative will open an inquiry and may resolve simple errors on the spot. For anything more complex, they’ll start a formal investigation.

Here’s the part many cardholders miss: a phone call alone doesn’t fully protect you under federal law. The Fair Credit Billing Act requires disputes to be submitted in writing to get full legal protection.

Calling is a good first step, especially if you want to stop more charges right away, but you should also follow up with a written dispute, either using the online form or sending a letter, to fully protect your rights.

How to Dispute a Charge by Mail (Written Dispute Letter)

Mailing a written letter is the most formal option, and it’s the method that satisfies the Fair Credit Billing Act’s writing requirement without question. Citi doesn’t require a specific dispute form. A clear, well-organized letter works just as well.

Send your letter to:

Citibank Customer Service P.O. Box 6500 Sioux Falls, SD 57117

Your letter should include:

- Your full name and account number

- The date you’re writing the letter

- The transaction date and dollar amount in question

- A clear, specific explanation of why you’re disputing the charge

- What you want Citi to do (typically a full reversal of the charge)

- Copies, never originals, of any supporting documents like receipts or cancellation confirmations

- Your signature and the date

If you’d like a starting template, the Federal Trade Commission provides a sample dispute letter you can adapt to your situation.

Send your letter by certified mail with return receipt requested. This gives you proof of exactly when Citi received it, which matters if there’s ever a question about whether you met the deadline. That deadline is the subject of the next section, and it’s the single most important date in this entire process.

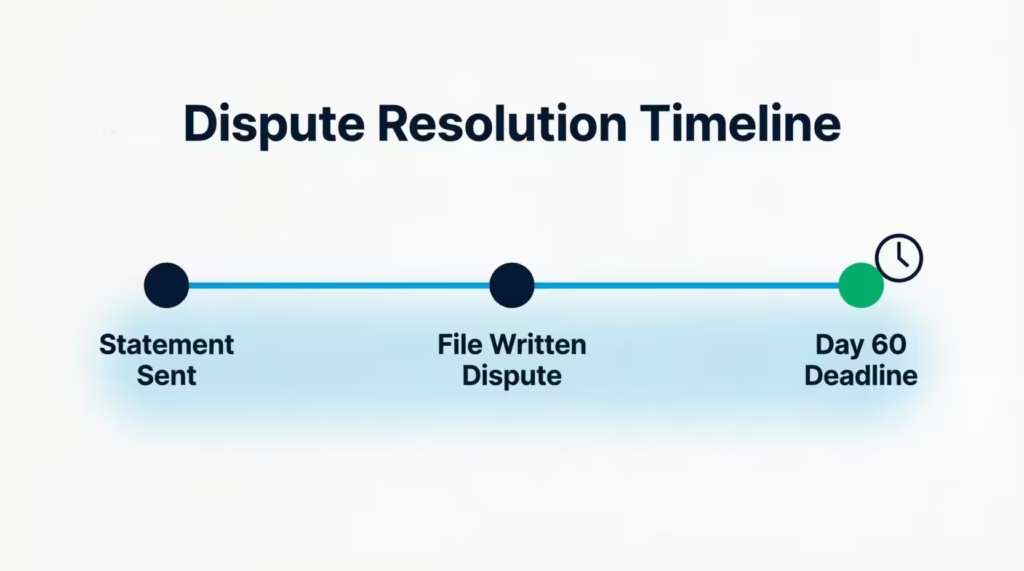

The 60-Day Deadline You Can’t Miss

This is the part of the dispute process that trips up more people than anything else. Under the Fair Credit Billing Act, cardholders have 60 days from the date the statement containing the disputed charge was sent to file a written dispute. Miss that window, and you can lose your right to dispute the charge under federal law entirely, according to the Consumer Financial Protection Bureau.

A few details make this rule easier to work with:

- The clock starts from when your statement was issued, not from the date of the original purchase. If a charge appeared on a statement sent 45 days ago, you still have 15 days left to act.

- To count under the FCBA, your dispute must be in writing. A phone call can get the ball rolling, but it doesn’t stop the clock on its own. Follow up with the online form or a mailed letter within the 60-day window.

- Fraud is treated differently. If someone used your card without authorization, there’s generally no FCBA time limit for reporting it, though acting fast still limits your liability and speeds up resolution.

- If Citi issues a temporary credit and later reverses it, the 60-day window can restart, counted from the statement that shows the reversal. This detail gets missed often, so if this happens to you, don’t assume you’re automatically out of time.

The safest approach is simple: the moment you spot a charge you want to dispute, mark your calendar with the 60-day cutoff and file your written dispute well before it arrives.

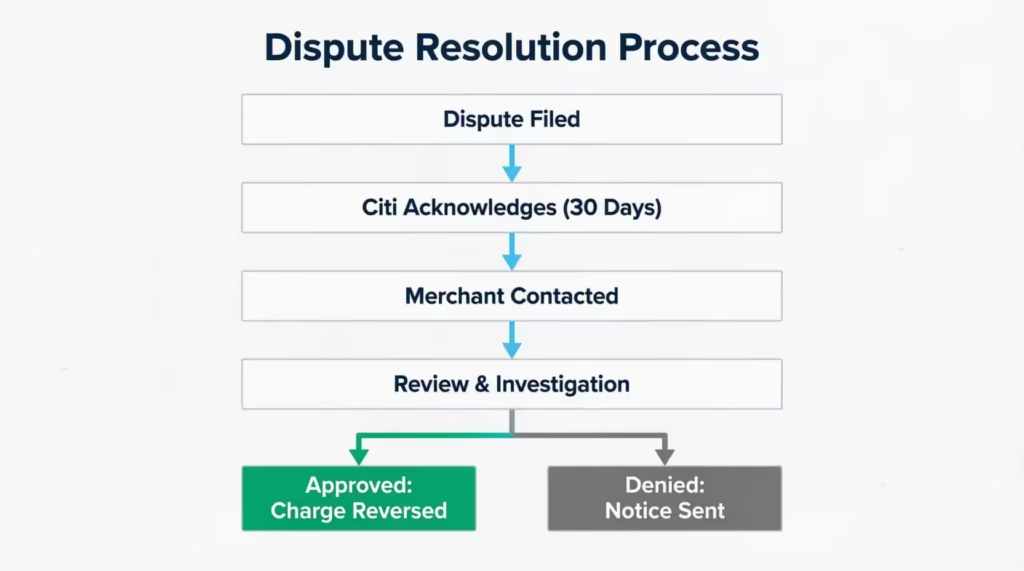

What Happens After You File: Citi’s Investigation Process

Once your dispute is submitted, Citi has specific legal obligations for how quickly it responds and investigates.

Here’s what happens next:

- Acknowledgment. Citi must acknowledge receipt of your dispute within 30 days of getting it.

- Merchant contact. Citi reaches out to the merchant involved and requests their side of the transaction, including any records or evidence they have.

- Review. Citi compares your documentation against whatever the merchant provides to determine whether the charge was valid.

- Normal card use continues. You can keep using your Citi card as usual while the investigation is ongoing. The dispute doesn’t freeze your account.

You generally won’t need to do anything else during this stage unless Citi contacts you for more information. If they do, respond promptly, since delays on your end can slow down the whole timeline.

How Long a Citi Dispute Takes

Under federal law, Citi has up to two billing cycles, or a maximum of 90 days, to complete its investigation and either resolve the dispute or explain in writing why it was denied. Straightforward cases, like a clear duplicate charge, often resolve faster, sometimes within a few weeks. More complex disputes involving conflicting merchant claims tend to take longer.

If a month or more passes with no update, it’s reasonable to check your Dispute Center status online or call to ask where things stand. You’re not being impatient. You’re simply confirming your case hasn’t stalled.

Do You Have to Pay the Disputed Amount While You Wait?

This question adds a lot of stress to the dispute process. The direct answer is: no, you don’t have to pay the disputed amount. Also, Citi cannot charge you interest or fees on that part while the investigation is ongoing.

Here’s what that actually means for your monthly bill:

- The disputed amount is set aside. You don’t need to pay it, and it shouldn’t accrue interest during the investigation.

- You’re still responsible for the rest of your bill. If your statement includes other charges that aren’t part of the dispute, those still need to be paid on time to avoid late fees or interest on those amounts.

- If the dispute is denied, the disputed amount becomes due again, and interest can apply retroactively back to the original purchase date.

⚠️ Mistake to Avoid: Don’t assume the entire statement balance is on hold just because one charge is disputed. Paying only the disputed amount late, while ignoring the rest of your bill, is a common mistake cardholders make during disputes.

Does Disputing a Charge Hurt Your Credit Score?

Filing a dispute itself does not directly damage your credit score. Citi isn’t reporting a mark against you simply because you raised a legitimate question about a charge.

What can affect your credit is how you handle the rest of your account during the process. Paying your non-disputed balance on time keeps your account in good standing throughout the investigation. The only real risk to your score comes later, and only if your dispute is denied and you then fail to pay the amount that becomes due.

If Citi Approves or Denies Your Dispute

Once the investigation wraps up, there are two possible outcomes, and each one comes with a clear next step.

If Citi rules in your favor, the disputed charge is reversed and credited back to your account. In most cases, no further action is needed on your end. You’ll typically see the credit reflected on an upcoming statement, along with a notice confirming the resolution.

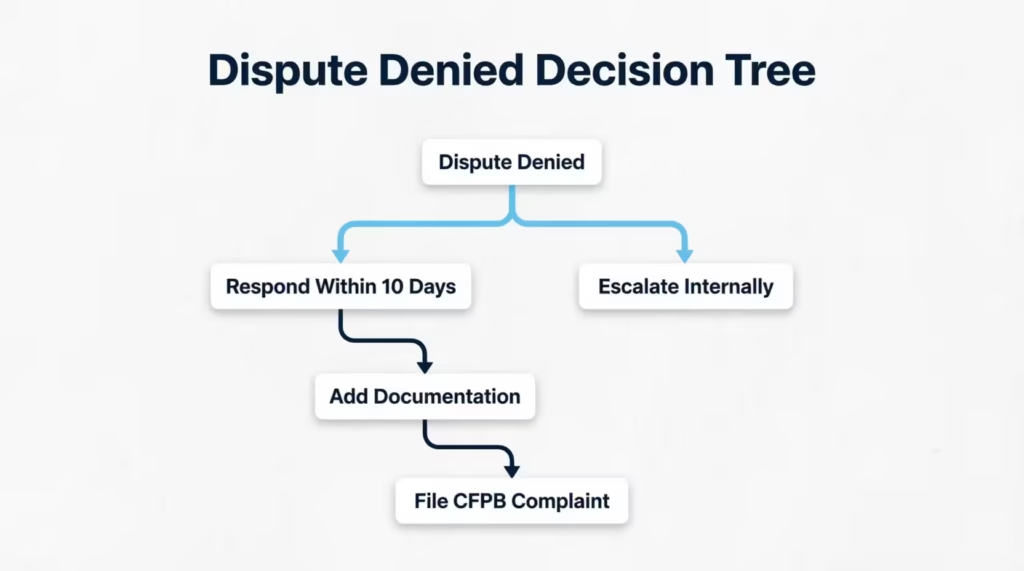

If Citi Denies Your Dispute

If Citi determines the charge was valid, you’ll receive a written notice explaining the decision. That notice will include the reason for the denial and will restate the amount now due, including any interest that accrued during the investigation period.

Here’s a detail worth paying close attention to:

You generally have 10 days from the date of that notice before payment on the disputed amount is required again. That window is short, so read the notice as soon as it arrives and decide quickly whether you plan to accept the decision or push back.

A denial isn’t necessarily the final word. The next section covers exactly what you can do if you believe Citi got it wrong.

How to Escalate If Your Dispute Is Denied

A denied dispute doesn’t mean you’re out of options. Federal law gives you a structured path to challenge the outcome, and knowing it can make a real difference.

Challenge the result within 10 days. You have the right to formally dispute Citi’s investigation findings within that same 10-day window mentioned in the denial notice. Send a written response explaining why you disagree, and include any new evidence you haven’t submitted yet.

Strengthen your case with additional documentation. If your original dispute was thin on evidence, this is the moment to add more. Useful documents include:

- A police report, for cases involving theft or identity fraud

- A signed affidavit describing what happened

- Proof of your location at the time of the transaction, such as a receipt or statement showing you were somewhere else

- Any further correspondence with the merchant

File a complaint with the Consumer Financial Protection Bureau. If Citi still won’t budge, submitting a complaint through the CFPB’s complaint portal creates an official record and often prompts card issuers to take a second, closer look.

Consider protections under the Truth in Lending Act. For cases specifically involving unauthorized charges, Section 1643 of the Truth in Lending Act offers legal protections that don’t carry the same 60-day restriction as the FCBA. This can matter if you’re outside the original dispute window but still dealing with a fraudulent charge.

Persistence matters here. Card issuers process an enormous volume of disputes, and a well-documented, clearly written follow-up often gets more attention than the initial claim.

Dispute vs. Chargeback vs. Fraud Report: Which One Applies to You

These three terms are often confused, but they mean different things. Understanding the differences helps you choose the right approach.

| Term | What It Means | When to Use It |

|---|---|---|

| Dispute | The formal complaint you file with Citi about a charge | Billing errors, wrong amounts, non-delivery, canceled subscriptions still charging |

| Chargeback | The actual reversal Citi performs if your dispute is approved | This isn’t something you file. It’s the outcome Citi issues on your behalf |

| Fraud report | A report specifically for unauthorized or stolen card use | Your card or card number was used without your knowledge or permission |

In plain terms: you file a dispute, and if it’s successful, Citi processes a chargeback to reverse the transaction. A fraud report is a specific claim for cases where the card was compromised. It has different documentation needs and usually no strict 60-day filing limit.

If you’re not sure which one applies, start with the “What Charges You Can Dispute” section above. Matching your situation to the right category from the start makes the rest of the process faster and smoother.

Frequently Asked Questions (FAQs)

How do I dispute a Citibank credit card charge?

File online through Citi’s website or app, by phone at 1-800-950-5114, or by mail to Citibank Customer Service. Federal law gives you 60 days from your statement date to submit a written dispute for full protection.

How long do I have to dispute a charge on Citibank?

You have 60 days from the date the statement showing the charge was sent. This deadline comes from the Fair Credit Billing Act, and missing it can cost you your dispute rights.

How long does Citibank take to resolve disputes?

Citi has up to two billing cycles, or a maximum of 90 days, to investigate and resolve a dispute. Simple cases like duplicate charges often resolve within a few weeks.

Can I dispute a credit card charge that I willingly paid for?

No, simple dissatisfaction with something you willingly bought doesn’t qualify as a billing dispute. That’s a return or refund conversation with the merchant, not a case covered by the Fair Credit Billing Act.

What are valid reasons for disputing a credit card charge?

Valid reasons include unauthorized charges, billing errors like wrong amounts or duplicates, goods never received, items not as described, and charges billed after you canceled a service.

Do I have to pay the disputed amount while Citi investigates?

No, the disputed amount is set aside and shouldn’t accrue interest during the investigation. You still need to pay the rest of your statement balance on time to avoid late fees.

Does disputing a charge hurt your credit score?

No, filing a dispute itself doesn’t damage your credit score. Your score is only at risk if the dispute is denied and you fail to pay the amount that becomes due afterward.

What happens if Citi denies my dispute?

You’ll get a written notice explaining why, and you generally have 10 days before payment is required again. You can challenge the decision in writing within that window and add new supporting documents.

What’s the difference between a dispute, a chargeback, and a fraud report?

A dispute is the claim you file, and a successful one leads Citi to process a chargeback that reverses the transaction. A fraud report is specifically for a compromised card and usually has no strict 60-day filing limit.

Can I call Citi to dispute a charge, or does it need to be in writing?

A phone call can start the process and stop further charges quickly, but it doesn’t count as a formal dispute under federal law. You still need to follow up with a written dispute online or by mail within 60 days.

Wrapping Up

Disputing a charge on your Citi card involves a few steps:

- Confirm your situation qualifies.

- Gather your documentation.

- File in writing within 60 days.

- Follow up if Citi denies your claim.

The Fair Credit Billing Act sets these timelines. Filing online or by mail as soon as possible gives you the best protection. This also starts the investigation right away.

If you face a fake charge or a stubborn subscription, learning how to dispute a Citibank credit card charge helps you take control. Don’t leave it to chance. If you know someone who’s ever stared at a mystery charge on their statement wondering what to do, sharing this could save them the same confusion.