I know how draining it feels when your Citibank credit card issue drags on. You’ve called customer service, waited on hold, been transferred, and still no fix. Maybe it’s a wrong charge, a fraud alert, a closed account, or a denied dispute that’s now hurting your credit. You’re unsure what to do next. The main point here is important: knowing how to file a complaint against Citibank credit card correctly can save you weeks of stress.

The fastest path is simple: escalate in order, from Citi’s own channels, up to the CFPB, and then to bank regulators or court if needed.

Below, you’ll get the full step-by-step ladder, plus the exact scripts, addresses, and timelines that get results.

Key Takeaways

This guide explains how to file a complaint against a Citibank credit card, including the difference between disputes and complaints, exact escalation channels, FCBA protections, and CFPB filing steps with response deadlines.

Core Facts:

- Billing disputes under the FCBA must be sent in writing within 60 days of the statement showing the error, and only cover errors over $50 on open-end credit.

- Citi must acknowledge a written billing dispute within 30 days and resolve it within two billing cycles, capped at 90 days total.

- While a dispute is open, Citi cannot collect the disputed amount, charge interest or fees on it, or report the account as delinquent.

- CFPB complaints filed at consumerfinance.gov/complaint route to Citi’s executive response team, which has 15 calendar days to respond.

- Unauthorized credit card charges are capped at $50 in liability under federal law, and Citi’s zero-liability policy usually reduces this to $0.

- The OCC’s HelpWithMyBank.gov review process for national banks like Citibank typically takes 45 to 60 business days.

Best for:

- Cardholders with an unresolved billing error, fraud charge, or account issue who have already contacted Citi without success.

- Readers trying to determine whether their situation is a billing dispute (FCBA-protected) or a general service complaint.

- Anyone preparing to escalate a Citibank issue to the CFPB, OCC, BBB, or state attorney general after internal channels stalled.

Dispute vs. Complaint: Which One Applies to Your Issue

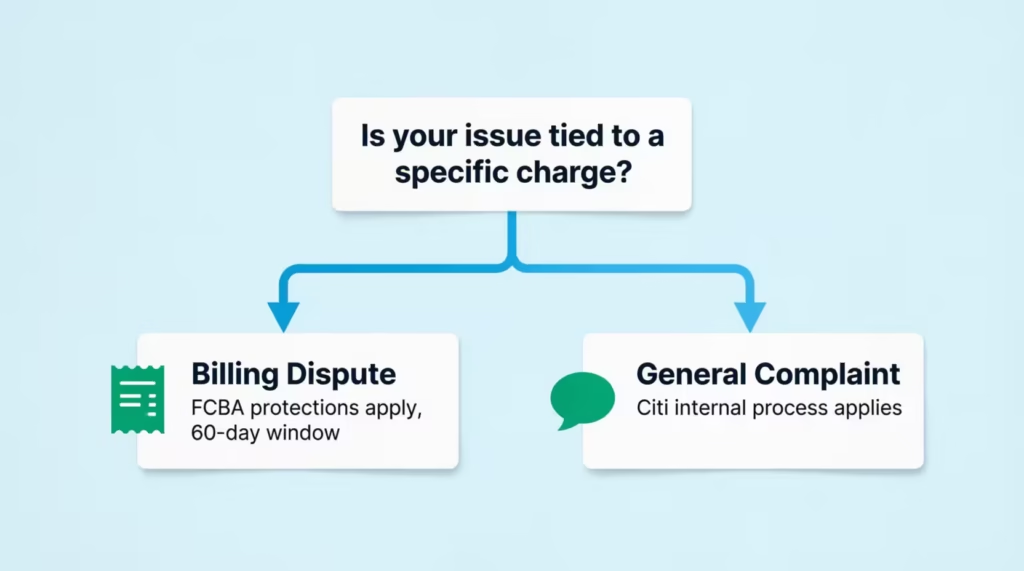

Before you take any action, figure out what you actually have. This one choice changes the rules, the timeline, and your legal protections. A lot of people mix these two up, and it’s why cases stall.

What Counts as a Billing Dispute

A billing dispute is a specific type of problem tied to a charge on your statement.

Under the Fair Credit Billing Act (FCBA), this covers:

- Charges you didn’t make

- Charges for the wrong amount

- Charges for goods or services you never received

- Math errors

- Charges you questioned but Citi didn’t explain

The Federal Trade Commission explains that you must send a written notice to your card issuer so it arrives within 60 days after the first bill with the error was sent to you.

If your problem is a specific bad charge, you have a billing dispute. That means strong federal protections apply.

What Counts as a General Complaint

A general complaint is about service, policy, or how you were treated. Think about problems like rude reps. A card can close unexpectedly. A limit cut might confuse you. There could be errors in credit reporting.

Hardship requests can be denied. Also, a dispute might be refused by Citi. Nothing in FCBA controls the timeline here. Instead, this path uses Citi’s internal complaint process and, if needed, outside regulators.

Why the Difference Matters

The rules split at this fork. A billing dispute triggers strict FCBA timelines and stops Citi from treating the disputed amount as late. A general complaint doesn’t have that shield, so you need to lean on Citi’s own process and outside pressure. Filing the wrong type wastes time and can waive some rights.

Quick Self-Check

Ask yourself: is my problem tied to a single charge or a small set of charges on my statement? If yes, it’s a dispute. If it’s about a decision, policy, service quality, or credit reporting, it’s a complaint. If it’s both (fraud plus poor service), you can run both tracks at once.

📌 Did You Know: The FCBA only covers billing errors of more than $50 on open-end credit like credit cards, and only if the notice reaches Citi within 60 days. Miss that window and you lose the strongest legal path, so act fast.

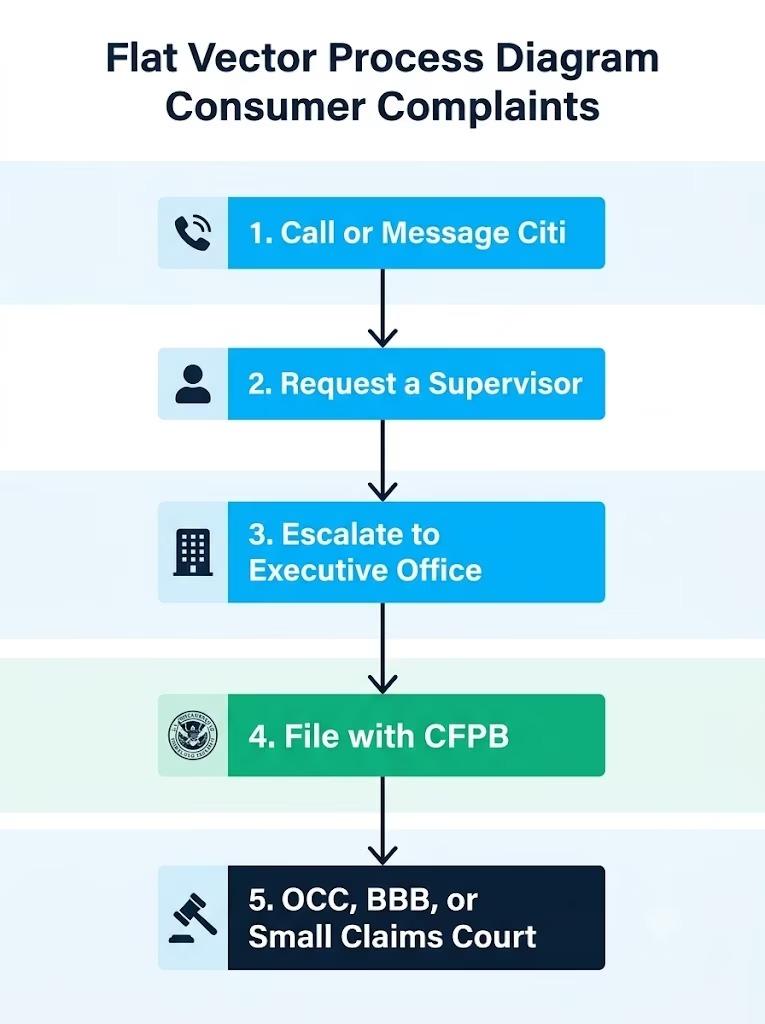

How to File a Complaint with Citi Directly

Every effective escalation starts inside Citi. Regulators want to see that you gave the bank a real chance to fix the issue first. Citi has three main channels, and each fits a different situation.

By Phone

Phone is fastest for time-sensitive issues like fraud, a locked account, or a payment posting problem. Call the number on the back of your card, or use Citi’s general credit card support line at 1-800-950-5114. TTY users can call 711. Before you dial, have your account number, the last four of your SSN, your ID verification info, and a short written summary of the problem in front of you.

When the rep answers, say clearly: “I’d like to file a formal complaint about [specific issue]. Please open a case and give me a reference number.” That phrasing matters. It moves your call from a general question into Citi’s tracked complaint system. Write down the rep’s name, the date and time, and the case reference number before you hang up.

In Writing/By Mail

Mail is slower, but it creates a paper trail regulators and courts respect. Send written complaints to:

Citibank Customer Service, P.O. Box 6500, Sioux Falls, SD 57117

For billing disputes under the FCBA, always send your letter by certified mail with return receipt. That gives you proof of the delivery date, which is how the 60-day window is measured. Keep a copy of everything you send, plus copies of any documents like receipts, screenshots, or prior letters.

Through the Online Account or App

Using secure messaging in your Citi online account or the Citi Mobile app is ideal for non-urgent matters. It gives you written proof without the wait for postal delivery. You can attach files and get a time-stamped record of the conversation, both of which help later. Download the app on the Apple App Store or Google Play if you don’t have it yet.

Use secure messaging for follow-ups, document uploads, and cases where you want a written response. Use phone for urgent fraud, account lockouts, or anything where waiting a day is a problem. Use certified mail when the FCBA clock is running, or you plan to escalate later.

What to Include in an Effective Complaint

A complaint that gets fixed looks very different from a complaint that gets ignored. Frontline reps see thousands of vague messages a week. Yours has to stand out for the right reason: clear facts, clear ask, clear proof.

The Core Elements Every Complaint Needs

A strong complaint has six parts:

- A clear problem statement. One or two sentences. What went wrong, in plain words.

- Dates, amounts, and account details. The last four of your account number, the exact charge amount, the date it posted, and any related transaction IDs.

- Your prior contact history. Every call, letter, or message you’ve already made. Include dates, rep names, and case numbers.

- The desired outcome. Say exactly what you want. “Refund of $214.75,” “removal of the late fee,” “correction of the 30-day-late mark on my credit report,” or “reopen the account.” A vague ask gets a vague answer.

- Supporting documents. Receipts, screenshots, emails from the merchant, a police report for fraud, prior letters from Citi.

- A deadline. A polite one, like “Please respond within 30 days.” This creates urgency and marks the file for follow-up.

Mini-Template You Can Copy

Here’s a short template that works for most cases:

Re: Formal Complaint — Account ending in [XXXX]

On [date], [describe what happened]. The disputed amount is [$XXX.XX]. I have already contacted Citi on [dates] and spoken with [rep names / case numbers], but the issue is not resolved.

I am requesting [specific outcome, e.g., a full refund of $214.75 and a written confirmation]. I have attached [list of documents].

Please treat this as a formal written complaint under Citi’s internal complaint process. Kindly respond in writing within 30 days.

Sincerely, [Name, address, phone, email]

Keep it under one page. Attach everything else. That mix of short letter and thick evidence packet works far better than a long emotional message.

💡 Pro Tip: Write your complaint in a Word or Google Doc first, then paste it into secure messaging or print it for mail. That way you have a clean copy for the CFPB later, and every version tells the same story.

Documentation to Keep Throughout the Process

Good records are what turn a weak case into a strong one. If your complaint ever reaches the CFPB, OCC, or a court, the side with clean documentation almost always wins.

Start a simple log the day you first notice the issue. For every call, write down the date, time, the rep’s full first name and any employee ID they’ll share, the phone number you called, and the case reference number. Note what was said and what was promised. If Citi tells you “we’ll refund it in 5 business days,” write that down word for word.

Save copies of every letter you send and receive. Take screenshots of your online account, secure messages, and any error screens. Keep receipts, merchant emails, shipping labels, and any texts or calls with the merchant if a purchase is involved. For fraud, save the police report or FTC identity theft report.

Ask Citi in writing for a final resolution letter at the end. This is a written statement of Citi’s decision on your complaint. If Citi refuses your request or closes the case, this letter is exactly what the CFPB, OCC, and small claims court want to see. Without it, regulators may assume you did not exhaust internal steps.

Store everything in one folder, physical or digital, sorted by date. This habit takes 5 minutes per event and pays back many hours later.

How to Escalate to a Supervisor or Higher Authority at Citi

Frontline reps have limits on what they can approve. If your issue needs a real fix, like a large refund, a reopened account, or a credit reporting correction, you need to move up the ladder.

Requesting a Supervisor on a Call

The right words open the door. Try this: “I understand you may not have authority to resolve this at your level. Please transfer me to a supervisor who can make this decision, and I’d like their name and employee ID.”

Stay calm. Frustrated shouting slows things down. If the rep says a supervisor is not available, ask for a callback within 24 hours and get the reference number. If the rep refuses to transfer you, ask them to note in the account that you requested escalation and were denied. That note itself becomes evidence for later.

Supervisors can waive fees, override decisions, fix errors, and start cases with internal specialty teams. What they usually cannot do is reverse decisions that involve credit reporting or major policy calls. Those cases need to go higher.

Citi’s Executive/Presidential Office

Large banks have an executive complaints team, sometimes called the Executive Response Unit or Office of the President. This group handles complaints that reach senior leadership. They often have more authority than regular supervisors. They usually work with a shorter response time internally.

You cannot dial this office directly the way you’d call customer service. It is reached in one of these ways:

- File a complaint with the CFPB or OCC, which almost always routes to Citi’s executive response team.

- Send a written letter addressed to Citi’s executive office at the P.O. Box 6500 address, marking it “Attention: Office of the President.”

- Ask the escalated supervisor to formally refer your case to the executive team and get the referral in writing.

At this level, expected outcomes are stronger. Full refunds, credit report corrections, written apologies, and account restorations happen more often. It usually takes 10 to 30 days for a response.

What Happens After You File: Citi’s Response Timeline

Setting the right expectations here saves a lot of anxiety. Citi’s timelines depend on which track you’re on.

For a general complaint, Citi typically acknowledges receipt within 5 to 10 business days. A full response usually follows within 30 days for straightforward issues and up to 60 days for complex ones. If you don’t hear back in that window, follow up in writing and cite your case number.

For an FCBA billing dispute, the timeline is stricter and set by federal law. Under FCBA rules, Citi must acknowledge your written dispute within 30 days of receiving it. Then Citi has up to two billing cycles, but no more than 90 days total, to investigate and resolve the error. During that time, Citi must either correct the charge or explain in writing why it believes the charge is valid.

Understand the difference clearly. A “complaint” is Citi’s internal service process. A “formal dispute” under FCBA is a legal process with a fixed clock. If you want the FCBA clock to start, you must send a written notice to the address Citi lists for billing inquiries, not just call. Phone calls do not trigger FCBA protections. Written notice does.

Your Rights While a Dispute Is Open (FCBA Protections)

Many people don’t file disputes because they fear their credit will crash or Citi will send them to collections. The FCBA is built exactly to stop that from happening while you fight a charge.

Once Citi gets your written billing dispute within 60 days, several protections start automatically. The Federal Trade Commission says that while your dispute is being looked into, the card issuer cannot collect the disputed amount. They also cannot charge interest or fees on that amount, nor can they report you as delinquent or close your account for not paying it.

You also don’t have to pay the disputed amount while the investigation is open. You still need to pay the rest of your bill on time, though. If you have a $500 statement with a $150 disputed charge, pay the $350 by the due date and note in writing that the $150 is under dispute.

Citi may add a notation to your credit report saying the amount is “in dispute.” This does not lower your score. It signals to future lenders that you are actively working to resolve a specific issue.

If Citi violates these rules, that itself becomes strong evidence for a CFPB complaint or a small claims filing. Save every statement, letter, and credit report screenshot from that window.

⚠️ Mistake to Avoid: Don’t stop paying your whole bill because of one disputed charge. You still need to pay the undisputed part on time. If you don’t, Citi can report late payments for that amount. This damage is separate from the dispute.

How to File a Complaint with the CFPB

If Citi’s internal path fails, the Consumer Financial Protection Bureau is your most powerful next step. The CFPB sends your complaint to Citi’s executive response team. They set a strict deadline for a reply. The outcome is published in a public database for regulators, journalists, and future consumers to view.

Go to consumerfinance.gov/complaint. It’s free. No lawyer is needed. You can file in about 20 minutes if your documents are ready.

What to Include in a CFPB Complaint

Fill out the form carefully. Choose “Credit card or prepaid card” as your product. Then, pick the issue that fits your problem, such as “Problem with a purchase on your statement” or “Fees or interest.” In the “What happened?” box, tell the story in short paragraphs: what happened, when, dates you contacted Citi, case numbers, and what outcome you want.

Attach your documents. The CFPB portal allows uploads up to a fixed size per file, so keep files under about 50 MB each. Include your prior letter to Citi, screenshots, receipts, and any responses you already got. When it asks for the company name, type “Citibank, N.A.” so the complaint routes to the right entity.

Do not overwrite. Keep it factual, short, and specific. Complaints that read as emotional rants get lower attention than ones that read as clean case files.

What Happens After You Submit

You’ll get a confirmation email with a tracking number right away. The CFPB then sends your complaint to Citi.

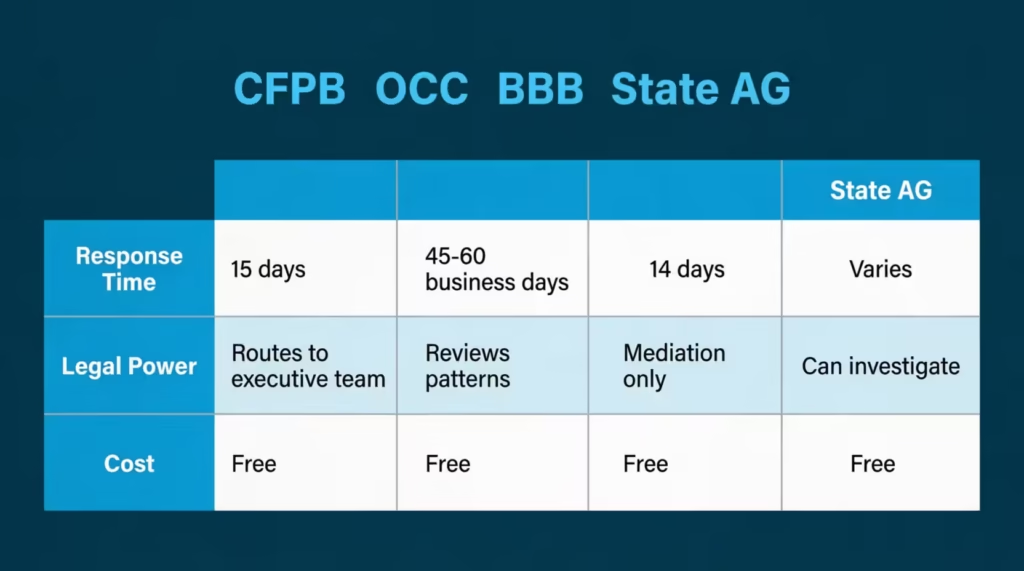

Citi has 15 calendar days to respond, based on the CFPB’s published complaint process. Most banks reply within that window with either a resolution or a “still working on it” update. If it’s the second, they get up to 60 days total to send a final answer.

Once Citi responds, you can post a public reply through your CFPB portal saying whether the outcome resolved your issue. Your complaint (with your name removed) may be added to the CFPB’s public Consumer Complaint Database. That visibility is a real reason banks take these complaints seriously.

Other Places to Escalate If Citi Still Doesn’t Resolve It

If the CFPB round ends without a fix, you still have strong options. Each hits a different pressure point.

Better Business Bureau

The Better Business Bureau is a nonprofit that mediates between consumers and businesses. Filing with the BBB is free. You submit the details online, and the BBB forwards them to Citi. Citi usually replies within 14 days.

Two things to know. First, the BBB has no legal power to force a refund or a credit correction. It only mediates. Second, a public unresolved complaint on Citi’s BBB profile can bring pressure that quietly gets results, especially when combined with a CFPB case. Use BBB as a supplement, not a substitute, for regulatory action.

OCC and State Regulators

The Office of the Comptroller of the Currency (OCC) regulates national banks, and Citibank, N.A. is one. You can file a complaint at HelpWithMyBank.gov, the OCC’s consumer complaint portal. OCC review usually takes 45 to 60 business days, longer than CFPB, but the OCC can look at pattern issues and compliance failures the CFPB might miss.

You can also contact your state banking regulator or state attorney general. They can help with issues like state consumer protection law violations, deceptive practices, or repeated failures. Search “[your state] attorney general consumer complaint” to find the right form. State AGs often hold more influence for policy or reporting complaints. They can launch bigger investigations.

You can file with all three (CFPB, OCC, and BBB) at the same time. There’s no rule against it, and it often speeds things up.

What to Do If Your Complaint Is Denied or Ignored

Sometimes even a CFPB complaint ends with Citi saying no. You still have paths forward. The decision now is how much time, money, and stress you’re willing to spend.

Start by re-escalating. Reply through the CFPB portal that the response did not resolve the issue and explain why. Sometimes a second look moves the case. Add any new documentation you have.

If the amount at stake is under your state’s small claims limit (usually $5,000 to $10,000, depending on the state), small claims court is a real option. Filing fees are typically $30 to $75. You don’t need a lawyer.

You show up with your evidence packet: your complaint letters, Citi’s responses, the CFPB record, and your damages calculation. Judges take clean paper trails seriously. Many banks settle rather than send an attorney over a small claim.

Before filing, check your cardmember agreement for an arbitration clause. Many credit card contracts require disputes to go through arbitration rather than court. Some agreements include a small claims carve-out that lets you use that court anyway. If arbitration is required and small claims is not available, you may be able to file an individual arbitration claim through the American Arbitration Association or JAMS.

For higher-value cases, if your credit report hurt your chances of getting a loan, talk to a consumer protection attorney. Also, check for possible Fair Credit Reporting Act or Truth in Lending Act violations. Many take these cases on contingency, meaning no upfront fees. The National Association of Consumer Advocates has a searchable directory.

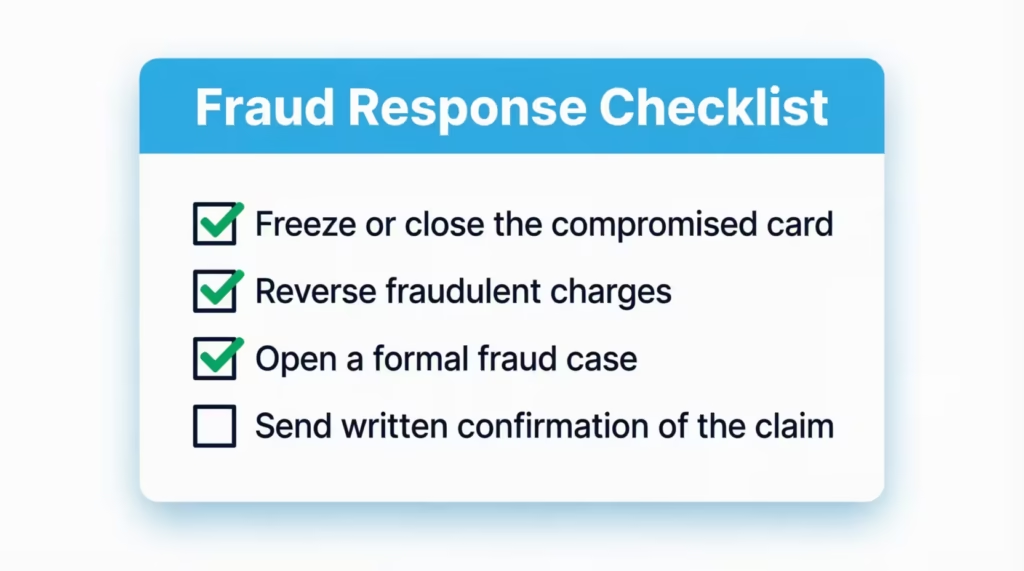

Filing a Complaint for Fraud Specifically

Fraud runs on a different clock. Every hour matters when someone else is using your card.

The moment you spot an unknown charge or lost card, call Citi at the fraud number on the back of your card or 1-800-950-5114. This is the fastest way to freeze the card and block further charges. Under federal law, you’re liable for a maximum of $50 for unauthorized credit card charges. If you report quickly, Citi’s zero-liability policy usually reduces that to $0.

Ask Citi to:

- Freeze or close the compromised card and issue a new one.

- Reverse the fraudulent charges (usually a provisional credit within a few business days).

- Open a formal fraud case with a case reference number.

- Send you a written confirmation of the fraud claim.

Next, put a fraud alert or a credit freeze on your credit files with all three bureaus. You only need to contact one, and it must notify the other two. Start with Equifax, Experian, or TransUnion. If it’s full-on identity theft, file a report at IdentityTheft.gov, which builds an FTC identity theft report you can use with Citi and the credit bureaus.

If Citi won’t reverse the fraud charges, or won’t close the case, that’s a problem. If they report your account late while you’re still disputing, act quickly. It’s time to file a CFPB complaint under the fraud category.

Under the FCBA, unauthorized charges are billing errors, so all the protections above still apply. Keep every police report, ID theft report, and case number in your evidence folder.

Frequently Asked Questions (FAQs)

How do I file a dispute with Citibank credit card?

Send a written notice to Citibank Customer Service, P.O. Box 6500, Sioux Falls, SD 57117, within 60 days of the statement showing the error. Use certified mail with return receipt so you can prove the delivery date that starts your FCBA protection clock.

How long does a Citibank credit card dispute take?

Citi must acknowledge your written dispute within 30 days of receiving it. The full investigation can take up to two billing cycles, but no more than 90 days total, before Citi corrects the charge or explains in writing why it’s valid.

Do I get my money back if I dispute a transaction?

You don’t have to pay the disputed amount while Citi investigates, and Citi can’t charge interest or fees on it during that time. For fraud specifically, Citi usually issues a provisional credit within a few business days after you open a case.

How do I speak with a live person at Citibank?

Call 1-800-950-5114, or use the number on the back of your card, and say clearly, “I’d like to file a formal complaint about [issue]. Please open a case and give me a reference number.” If the rep can’t help, ask to be transferred to a supervisor and get their name and employee ID.

Who do I contact to file a complaint against a credit card company?

Start with Citi directly by phone, mail, or secure messaging, then escalate to the CFPB at consumerfinance.gov/complaint if it’s unresolved. The OCC, BBB, and your state attorney general are additional options that can run alongside a CFPB complaint.

Is it worth filing a complaint with the CFPB?

Yes, it routes directly to Citi’s executive response team and gives Citi only 15 calendar days to respond. Your complaint may also be added to the CFPB’s public Consumer Complaint Database, which adds pressure banks tend to take seriously.

Is Citibank good with disputes?

Citi follows the federally mandated FCBA timeline, acknowledging disputes within 30 days and resolving them within 90 days maximum. Results vary by case, so keeping detailed records and escalating through the CFPB if needed improves your odds of a favorable outcome.

What’s the difference between disputing a charge and filing a general complaint with Citi?

A dispute involves a specific wrong charge and triggers strict FCBA legal protections and timelines. A general complaint covers service or policy issues, like rude reps or account closures, and relies on Citi’s internal process rather than federal law.

Will filing a dispute hurt my credit score?

No, disputing a charge under the FCBA does not lower your credit score. Citi may add an “in dispute” notation to your credit report, but it can’t report you as delinquent or close your account for the disputed amount while the investigation is open.

What’s the maximum I’m liable for if my Citi card is used fraudulently?

Federal law caps your liability for unauthorized credit card charges at $50. If you report the fraud quickly, Citi’s zero-liability policy usually reduces that amount to $0.

Wrapping Up

Getting a Citibank credit card issue fixed comes down to using the right channel in the right order. To start, write a clear complaint to Citi. If that doesn’t work, talk to a supervisor. Then, go to the executive office. If you still don’t get results, contact the CFPB, OCC, BBB, or your state AG.

You can also consider small claims court if needed. Filing with the CFPB is the best step if Citi’s internal channels stall. This process goes directly to executive review and has a 15-day deadline. Keep clean records at every step.

If you know someone stuck in a Citi credit card mess right now, share this guide with them. A clear escalation path can save them weeks of frustration and possibly hundreds of dollars.