Getting a denial from Citi feels frustrating, especially when the online message just says “we could not approve your request” with no clear reason. You may be second-guessing your credit score, your income, or that one inquiry from last month. If you’re wondering why did Citibank rejected my application, the answer usually comes down to a mix of credit score, recent inquiries, income, and Citi’s own internal rules.

The fix is simple: read your adverse action letter, then call the reconsideration line before the denial becomes final.

Below, you’ll get the exact reasons, a call script, timing rules, and a step-by-step plan to turn this “no” into a future “yes.”

Key Takeaways

This guide explains why Citibank rejects credit card applications, covering credit score and inquiry triggers, Citi-specific rules like credit exposure limits, the adverse action letter, and how to use the reconsideration line to reverse a denial.

Core Facts:

- Most Citi rewards cards target a FICO score of 690 or higher, and applications below that threshold may be auto-declined before human review.

- Citi is stricter than most issuers on recent inquiries, and 4 to 6 hard pulls in six months can trigger an automatic decline regardless of score.

- Federal law requires an adverse action letter within 30 days of a completed application, listing the specific denial reasons, credit bureau used, and credit score.

- The reconsideration line can override an automatic denial without a new hard inquiry, and calling within 48 hours of denial gives the best odds of success.

- Citi limits total credit exposure across all cards a person holds, and existing customers can ask to shift a credit limit to a new card to stay under that ceiling.

- Recommended reapply wait ranges range from 1 to 2 weeks for clerical errors up to 6 to 12 months for a low score or recent late payment.

Best for:

- Applicants who just received a Citibank credit card denial and want to understand the reason before taking next steps.

- Existing Citi cardholders applying for an additional card who want to manage total credit exposure or product overlap issues.

- Anyone deciding between calling reconsideration, correcting an application error, or waiting before reapplying.

Common Reasons Citibank Denies a Credit Card Application

Before you dig into Citi’s fine print, it helps to rule out the basic causes. Most denials come from a short list of credit profile issues. If one of these describes you, the fix is usually clear.

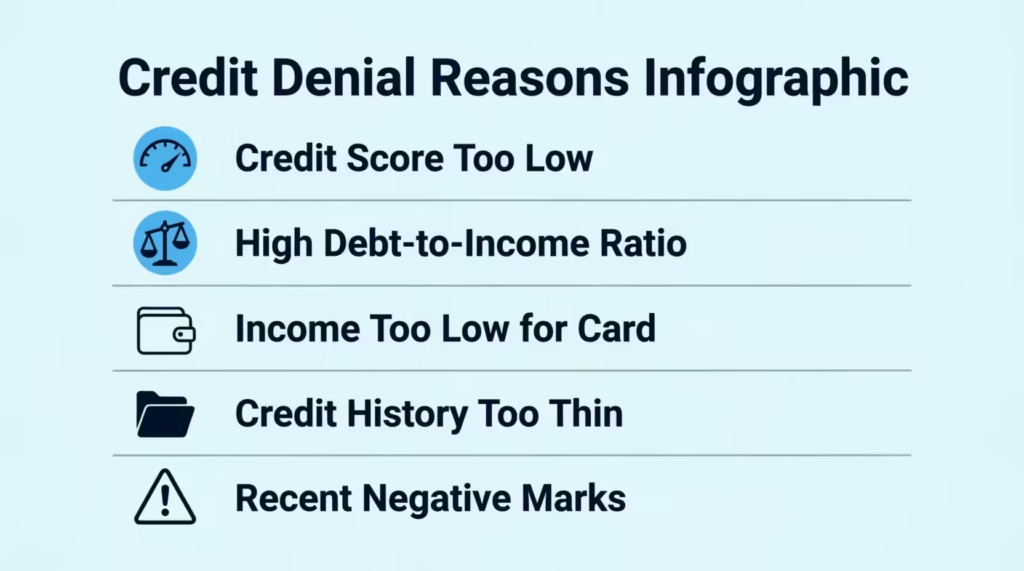

Your credit score falls below the card’s floor

Most Citi rewards cards, like the Citi Double Cash or Citi Strata Premier, target scores in the “good” to “excellent” range. That usually means a FICO score of 690 or higher. Store cards and secured options accept lower scores. If your score sits below the target, the system may auto-decline before a human ever sees your file.

Your debt-to-income ratio is too high

Lenders look at how much of your monthly income already goes to debt payments. When that number climbs past 40% to 45%, banks worry you can’t take on more. Citi doesn’t publish a hard cutoff, but a high debt-to-income ratio is one of the top silent killers of an application. Pay down a credit card or two before you apply next time.

Your reported income is too low for the card

Premium cards need enough income to justify the credit line. If you list $22,000 in gross income and ask for a card that usually carries a $10,000 limit, the math doesn’t work.

Your credit history is too thin

A thin file means you have fewer than three or four active accounts, or your oldest account is less than two years old. Citi’s models want to see a track record. First-time applicants often hit this wall.

You have recent negative marks

Late payments in the last 12 months, a collection account, a charge-off, or a public record like a bankruptcy can trigger an instant denial. Even one 30-day late payment from six months ago can be enough on a strong card.

⚠️ Mistake to Avoid: Don’t guess which of these caused your denial and start “fixing” things blindly. The adverse action letter names the exact reason. Wait for it before you pay down cards or dispute anything.

Citibank-Specific Denial Triggers Most People Miss

Generic denial articles stop at “low score” or “high utilization.” Citi has its own quirks, and if you have strong credit but still got denied, one of these is usually the culprit.

Recent inquiry sensitivity

Citi is famously strict about new inquiries on your credit report. Reports from applicants on r/CreditCards and myFICO forums show that even one hard pull in the last 30 days can trigger a denial on a Citi card, and applicants with 4 to 6 inquiries in the last six months are often auto-declined regardless of score. This is stricter than most other major issuers. If you just opened a car loan or another card, wait 60 to 90 days before applying to Citi.

Internal risk models look past FICO

Banks build their own scoring models on top of FICO. Citi’s model weighs things like how quickly you’ve opened new accounts, whether your balances are climbing, and how you use your current Citi products. You can have a 780 FICO and still fail Citi’s internal scorecard if the pattern looks risky.

Existing Citi credit exposure

Citi caps how much total credit it will extend to one person. If you already hold two or three Citi cards with high limits, the bank may deny a new application simply because you’re at their internal exposure ceiling. This has nothing to do with your creditworthiness.

Product family overlap

Some Citi cards live in the same “family” and can’t be held together. For example, holding both a Citi Double Cash and a Citi Custom Cash may trigger restrictions on getting a third cash-back Citi card. The same applies to certain co-branded travel cards.

48-month bonus rules on co-branded cards

For cards like the Citi/AAdvantage lineup, you cannot earn the welcome bonus if you received one on that same card within the last 48 months. The application itself may go through, but the bonus, and sometimes the approval, will not.

💡 Pro Tip: If you’re already a Citi customer, check your total Citi credit exposure before applying. Add up the limits on every Citi card you hold. If the number feels large compared to your income, ask the reconsideration line to move part of an existing limit to the new card instead of extending fresh credit.

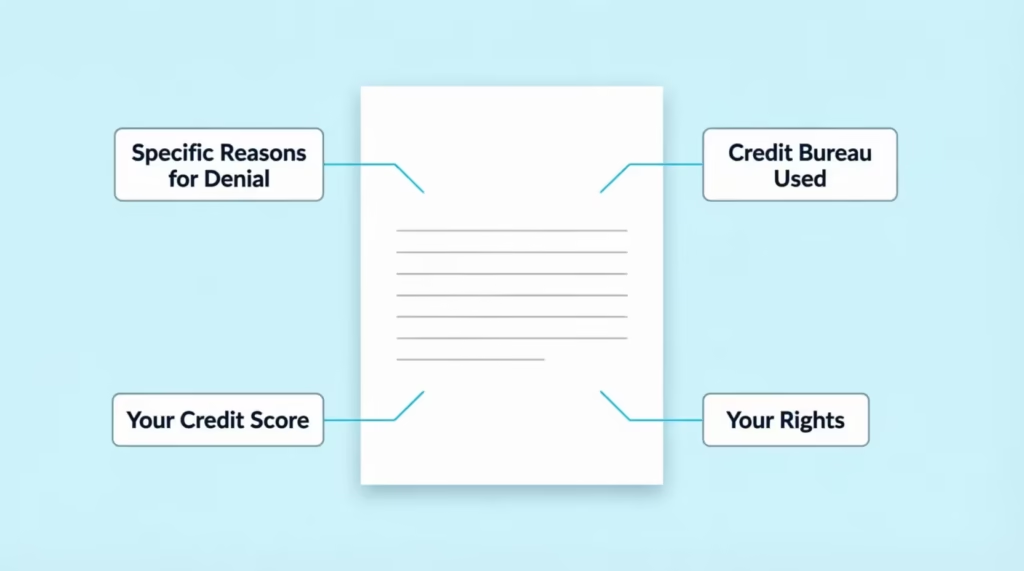

What the Adverse Action Letter Tells You

You don’t have to guess why Citi said no. Federal law forces the bank to tell you in writing. This document, called the adverse action letter, is the single most useful piece of paper in this whole process.

Under the Equal Credit Opportunity Act, Regulation B, creditors must send a notice with the specific reasons for the denial within 30 days of receiving a completed application. The rule appears in 12 CFR 1002.9 on the CFPB website. The letter must either list the main reasons for the denial or tell you how to request them within 30 more days.

The letter typically includes four key pieces of information:

- The specific reasons for denial. Common lines include “too many recent inquiries,” “insufficient credit history,” or “high balances on revolving accounts.” These are the reasons Citi’s system flagged.

- The credit bureau used. Citi usually pulls Equifax or Experian, though this varies by state and card. Knowing the bureau helps you check the right report.

- Your credit score at the time of application. The Fair Credit Reporting Act (FCRA) requires the bank to disclose the score used if it played a role in the decision. This is the score Citi actually saw, which may differ from the one you see on Credit Karma or a free app.

- Your rights. The notice must explain your right to a free copy of the credit report used, if you request it within 60 days.

If your letter feels vague, call Citi and ask for the “statement of specific reasons.” You’re legally entitled to it.

Application Errors That Look Like Credit Denials

Not every denial is about your credit. Sometimes the system rejects you for a clerical reason, and fixing it takes minutes.

Mismatched personal information.

Your name, address, Social Security number, or date of birth on the application must match what’s on your credit report. A typo in your SSN, a maiden name on one record but a married name on another, or an old address from three moves ago can all trigger an “unable to verify identity” denial. Log in to your account, review the application, and correct any mismatches.

A frozen credit report

If you froze your credit at Equifax, Experian, or TransUnion after a data breach, Citi cannot pull your file. The application will deny automatically with a message like “unable to obtain credit report.” Thaw the freeze at all three bureaus before you reapply. You can do this online in a few minutes:

Incomplete or wrong fields

Leaving housing payment blank, entering gross income instead of net when the field asks for net, or under-reporting household income can all trigger issues. Double-check every field before you submit.

A recent fraud alert

A fraud alert on your file forces the bank to take extra verification steps. If Citi can’t reach you at the phone number on file, they may deny the application by default. Update your phone number with each bureau before you apply.

📌 Did You Know: Data breach victims are advised by the FTC to freeze credit at all three bureaus, but many forget to thaw before applying for new credit. This is one of the most common reasons a “creditworthy” applicant gets an instant denial.

How to Check Your Citibank Application Status

Before you assume the worst, confirm what Citi actually decided. A “pending” status is different from a denial, and it changes what you should do next.

Check status online using the Citi Application Status page. You’ll need either your application reference number (from the confirmation email) or your Social Security number plus ZIP code. The tool shows one of three outcomes:

- Approved. Your card is on the way. No action needed.

- Pending review. Citi needs more time or more information. This usually resolves within 7 to 10 business days.

- Not approved. The formal denial. Your adverse action letter is on its way by mail or secure message.

If your status is “pending,” don’t panic and don’t reapply. Pending often means a human is reviewing your file, and calling in can actually help. If it’s “not approved,” move on to the reconsideration steps below.

You can also call Citi’s application status line at 1-888-201-4523. The line runs 24/7. Have your reference number ready.

Pulling Your Own Credit Report First

Before you call anyone at Citi, look at what they saw. Pull your full credit report from AnnualCreditReport.com, the only site authorized by federal law. All three bureaus, Equifax, Experian, and TransUnion, now offer free reports every week.

Focus on three things when you read your report:

- Recent hard inquiries. Count every hard pull in the last 6 months and the last 12 months. If you see 4 or more in the last 6 months, that’s likely your denial reason on Citi.

- Credit utilization. Add up your credit card balances and divide by total credit limits. If the ratio is above 30%, that’s a warning sign. Above 50%, it’s a major red flag.

- Errors. Look for accounts that aren’t yours, late payments you actually paid on time, or balances that look wrong. Errors get disputed for free, and they can move your score fast.

Knowing these numbers before you call reconsideration gives you specific facts to work with instead of vague hopes.

What to Do Immediately After a Citibank Denial

The first hour after a denial matters more than most people realize. Follow this order, and you’ll keep every option open.

- Step 1: Read the online denial message carefully. Screenshot it. The wording often hints at the main reason, even before the letter arrives. Phrases like “too many recent applications for credit” or “insufficient income” point you toward the fix.

- Step 2: Do not reapply immediately. A second application triggers a second hard inquiry, and it almost always ends the same way. Worse, back-to-back inquiries hurt your score more than a single one.

- Step 3: Call the reconsideration line within 24 to 48 hours. This is the single highest-leverage action. Reconsideration works best while your application is fresh in the system and the denial reason is easy to address. Wait too long, and the file may be closed.

- Step 4: Wait for the adverse action letter. It arrives by mail within 7 to 10 business days, or sooner in your Citi secure message center. Read it carefully. The exact reasons listed there tell you whether to reapply in weeks or months.

- Step 5: Decide between reconsideration, correction, or reapplication. Reconsideration works when the denial reason is fixable on the phone, like unverified income or an old address. Correction works for frozen credit or a typo. Reapplication is for score or history issues that need real time to improve.

How the Citibank Reconsideration Line Works

The reconsideration line is a small internal team at Citi that reviews denied applications by hand. They can override the automated denial without triggering a new hard inquiry, which makes this the single most valuable phone call in the whole process.

Call the personal card reconsideration line at 1-800-695-5171. The line runs from 8 a.m. to midnight ET, every day. For business cards, use 1-800-763-9795.

Timing matters. Call within 48 hours of the denial for the best odds. After 30 days, the file may be too old to reopen without a new application.

Before you dial, have this info ready:

- Your application reference number

- Your annual income and any side income you didn’t list

- Your monthly housing payment

- Your employer name, position, and how long you’ve worked there

- The credit limits and balances on your other Citi cards, if any

- Your explanation for anything unusual, like a recent inquiry or a paid-off collection

Keep the tone polite and confident. The agent has full authority to reverse the denial, but only if you give them a reason.

What to Say on the Call

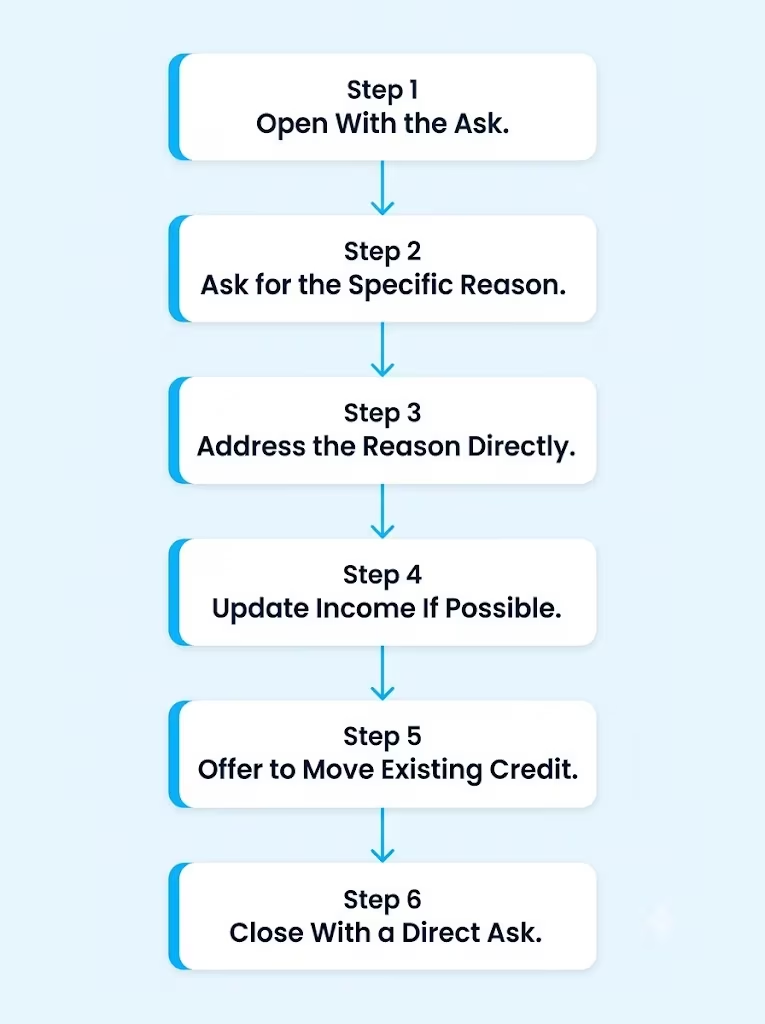

You don’t need a script word for word, but you do need to hit the right points. Here’s the flow that works best:

Open with the ask. “Hi, my name is [name]. I applied for the Citi Double Cash on [date] and received a denial. I’d like to request reconsideration.”

Ask for the specific reason. “Can you tell me the primary reason the application was declined?” Let the agent read it back. Now you know what to address.

Address the reason directly. If the reason is “too many recent inquiries,” explain what those inquiries were for. Something like “Two of those were for a car loan I was rate-shopping in the same week, and one was for an apartment application. None of them resulted in new credit card debt.”

Update income if possible. If you have side income, bonus income, or a raise you didn’t list, share it now. Citi counts household income for personal cards, so a spouse’s income also qualifies if you have reasonable access to it.

Offer to move existing credit. This is the strongest lever. Say: “If total exposure is the concern, I’m happy to move $5,000 of my limit from my existing Citi card to open room for this new one.” Agents can do this on the spot.

Close with a direct ask. “Based on what we discussed, would you be able to approve the application today?”

If the first agent says no, thank them politely and hang up. Wait a day, then call again. A different agent may see the file differently. This is a common tactic churners use, and it works.

When Reconsideration Is Unlikely to Succeed

Not every denial can be reversed on the phone. Save your time if any of these apply to your file.

Recent bankruptcy. A Chapter 7 discharge less than 24 months old, or a Chapter 13 still in repayment, will almost always block approval. Citi’s hard eligibility rules override the reconsideration team.

Serious derogatory marks in the last 12 months. A recent charge-off, an active collection, or a 60-day-plus late payment tells the bank the risk is present tense. No script fixes this.

Hard eligibility failures. Under 18, no valid SSN or ITIN, or a mismatched identity that can’t be verified. These are legal or system-level blocks, not credit judgments.

Score far below the card’s floor. If you applied for a premium card with a 620 score, no agent will approve it. The gap is too wide. Downgrade your target to a card that matches your score, or wait and rebuild first.

In these cases, spend your energy on fixing the underlying issue instead of calling reconsideration. The next section covers timing.

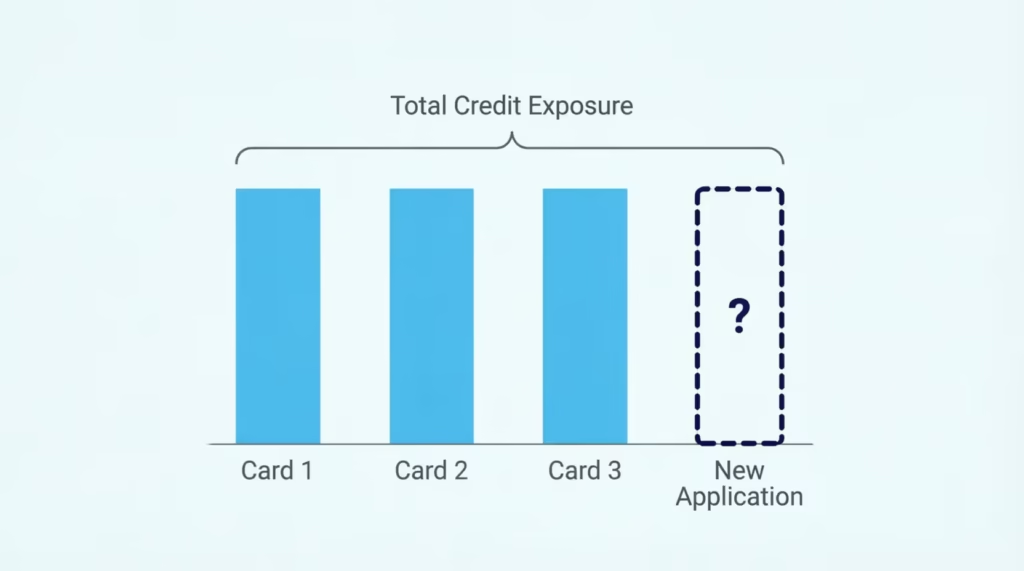

How Existing Citibank Cards Affect a New Application

If you already hold a Citi card, the calculation changes. Some of these factors help you, others hurt you.

Total credit exposure matters.

Citi looks at how much credit it has already extended to you across all products. If you hold three cards with $15,000 limits each, your exposure is $45,000. Adding a fourth card with a $10,000 limit pushes it to $55,000.

If your income is $60,000, the bank may see that as too much. Ask on the reconsideration call to shift $5,000 or $10,000 from an existing card to the new one. This keeps total exposure flat and often unlocks approval.

Product overlap can trigger denials

Citi restricts certain combinations, especially in the ThankYou Rewards family and the AAdvantage family. Holding two ThankYou cards may block you from a third. Holding the AAdvantage Platinum Select may block you from the AAdvantage Executive, at least for the welcome bonus. Check the specific card’s terms before applying.

Moving credit limits is Citi’s specialty

Citi is more flexible than most banks about shifting limits between your own cards. You can call anytime, not just after a denial, and ask to move a portion of a limit from one card to another. This is useful when you want to close an unused card without losing total credit, or when you want to make room for a new application.

Length of relationship helps.

If you’ve been a Citi customer for 5-plus years with clean payment history, the reconsideration team gives you real weight. Mention it on the call.

How Long to Wait Before Reapplying

There is no universal waiting period. The right wait depends on why you were denied. Use this framework to decide.

Short wait: 1 to 2 weeks

Use this window when the denial was clerical. A frozen credit report, a typo in your SSN, or an outdated address falls here. Fix the issue, wait until any new information settles into your credit file, and apply again.

Medium wait: 60 to 90 days

This range fits denials tied to recent inquiries or a temporarily high credit utilization. Inquiries lose most of their impact after 90 days on Citi’s model, and utilization drops as soon as you pay down balances and the statement closes. Also use this window if income was the issue and you got a raise or started a documented side income.

Long wait: 6 to 12 months

Use this timeline when the denial was about score, thin credit history, or a recent negative mark. Scores move slowly, and building history takes time. Applying too soon just burns another inquiry.

Very long wait: 24 months or more

After a bankruptcy or a series of charge-offs, plan for a two-year rebuild. Start with a secured card or a credit-builder loan, then step up to unsecured cards after 12 to 18 months of clean history.

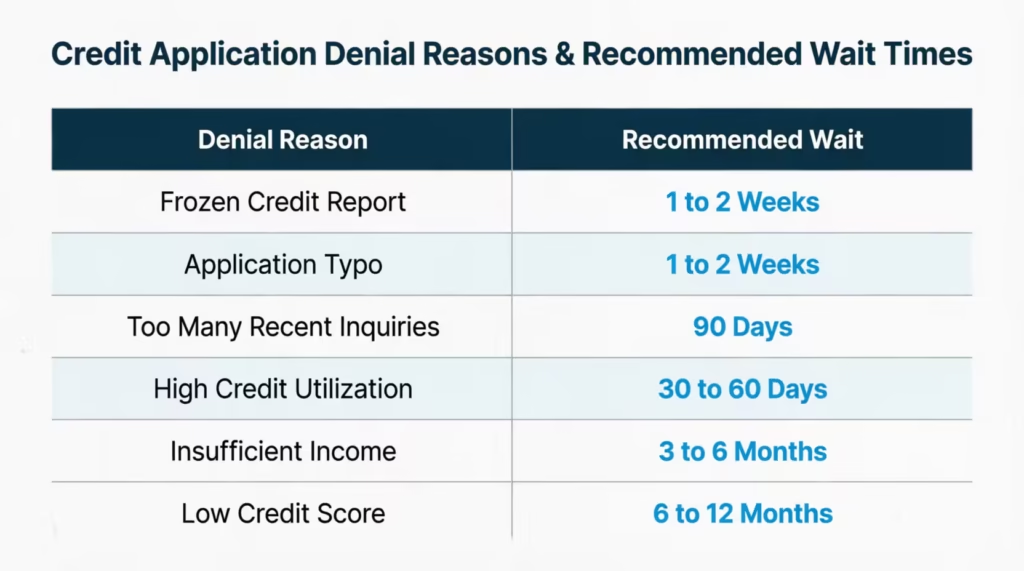

Here’s a quick reference:

| Denial reason | Recommended wait | What to do during the wait |

|---|---|---|

| Frozen credit report | 1 to 2 weeks | Thaw all three bureaus |

| Application typo | 1 to 2 weeks | Fix personal info |

| Too many recent inquiries | 90 days | Avoid all new applications |

| High credit utilization | 30 to 60 days | Pay balances below 10% |

| Insufficient income | 3 to 6 months | Document raise or side income |

| Low credit score | 6 to 12 months | Pay on time, lower utilization |

| Recent late payment | 12 months | Build clean payment history |

| Bankruptcy | 24 months plus | Rebuild with secured card |

How to Strengthen Your Application Before You Reapply

Waiting alone doesn’t fix the underlying reason for a denial. Use the wait window to actively improve the parts of your profile Citi flagged.

Pay balances down to below 10% utilization

Utilization is the second-largest factor in your FICO score, and it changes fast. If your total credit card balances are $6,000 and your total limits are $20,000, your utilization is 30%. Pay it down to $2,000, and utilization drops to 10%.

Do this before your statement closes, because the balance on the statement date is what gets reported. Lower credit utilization is often the single fastest score booster available.

Dispute credit report errors.

Pull your reports from AnnualCreditReport.com and flag anything wrong. Common errors include accounts that aren’t yours, late payments already corrected, and outdated balances.

File disputes directly with the bureau online. The bureau has 30 days to investigate under the Fair Credit Reporting Act. A single removed late payment can raise your score by 40 to 100 points.

Match your credit profile to the right card

If your score is 660, don’t apply for the Citi Strata Premier. Start with a card that matches your profile, like the Citi Double Cash or a Citi Rewards+, and step up later. Every card has a target credit range, and applying above your range wastes an inquiry.

Add positive payment history. If your file is thin, add accounts that report on-time payments. Options include:

- Becoming an authorized user on a family member’s clean, aged credit card

- Opening a secured card from a bank that graduates to unsecured, like the Discover it Secured or Capital One Platinum Secured

- Using Experian Boost to add utility and phone payments to your Experian file

Fix the specific reason on your adverse action letter

This is the most important step. If the letter says “insufficient income,” add documented income before you reapply. If it says “delinquent past or present obligations,” get any late accounts current and let 6 months of clean history report. Don’t work on the wrong problem.

Give the file time to reflect changes

Score improvements take one or two full statement cycles to appear on your credit report. Pay down balances now, wait 45 to 60 days, then pull a fresh report and confirm the changes before you reapply.

Frequently Asked Questions (FAQs)

Why did Citibank reject my application?

Citi denials usually trace back to your credit score, recent inquiries, income, debt-to-income ratio, or Citi’s own internal exposure rules. Your adverse action letter names the exact reason within 30 days of the decision.

What is the minimum credit score for Citibank?

Most Citi rewards cards, like the Citi Double Cash or Citi Strata Premier, target a FICO score of 690 or higher. Store cards and secured options accept lower scores.

Can I get a Citi credit card with a 600 credit score?

A 600 score sits well below the 690-plus range most Citi rewards cards target, so approval is unlikely. Consider a secured card or a card designed for building credit instead, then reapply once your score improves.

What bureau does Citibank pull from?

Citi usually pulls Equifax or Experian, though this varies by state and card. Your adverse action letter will confirm which bureau was used for your specific application.

What is the most common cause for a credit application being rejected?

Recent hard inquiries are one of Citi’s most common denial triggers, with 4 to 6 inquiries in the last six months often leading to an automatic decline regardless of score. High debt-to-income ratio and low credit scores are the other frequent causes.

Can I apply again if my credit card application is rejected?

Yes, but the right wait depends on the denial reason. Clerical issues need just 1 to 2 weeks, recent inquiries need 60 to 90 days, and low score or recent late payments need 6 to 12 months.

Is a rejected credit card application bad for my credit?

A denial itself doesn’t directly hurt your score, but the hard inquiry from applying does cause a small, temporary dip.

Is Citibank hard to get approved for?

Citi is stricter than most major issuers about recent inquiries, sometimes denying applicants over even one hard pull in the last 30 days. Citi also weighs its own internal risk model on top of your FICO score, so strong credit doesn’t guarantee approval.

How does the Citi reconsideration line work?

The reconsideration line is a Citi team that manually reviews denied applications and can override an automatic denial without a new hard inquiry. Call 1-800-695-5171 for personal cards within 48 hours of the denial for the best odds.

How long does Citibank take to approve an application?

A pending review usually resolves within 7 to 10 business days. You can check your status anytime at the Citi Application Status page or by calling 1-888-201-4523.

Wrapping Up

A Citi denial isn’t the end of the road. It’s a data point that tells you exactly what to fix. The adverse action letter names the reason, the reconsideration line offers a fast reversal path, and the right waiting period lets your credit profile heal without wasting another inquiry.

For most readers, the most effective approach is to call reconsideration within 48 hours, then use the adverse action letter to guide a focused 90-day fix. That combination reverses more denials than any single tactic alone.

If you know someone who just got a “sorry, we couldn’t approve” email from Citi, share this guide with them. It could save them from a second denial and a wasted hard inquiry.