If you already have one or two Citi cards in your wallet, you’re probably wondering how many Citi cards you can have before the bank starts saying no. Maybe you want a Custom Cash for groceries, a Strata Premier for travel, or another AAdvantage card before a big trip. The worry is real. Nobody wants to burn a hard inquiry on a denial or trigger an unspoken cap.

Citi does not set a fixed number of cards you can hold. The real limits are total credit exposure and strict application timing.

Below, you’ll get the exact rules, the 8-day and 65-day timing, the 48-month bonus warning, and clear steps to take if you get denied. Everything is laid out so you can plan your next application with confidence.

Key Takeaways

This guide explains how many Citi cards you can hold, covering total credit exposure, the 8-day and 65-day application timing rules, the 48-month bonus eligibility rule, and steps to take after a denial.

Core Facts:

- Citi sets no fixed cap on the number of credit cards a person can hold, unlike American Express, which limits cardholders to five credit cards and ten charge cards.

- Citi approval depends on total credit exposure, the combined credit limit across all Citi cards a person holds, evaluated against income, credit report standing, and payment history with Citi.

- Citi allows only one personal card application every 8 days and no more than two personal card applications within any 65-day window, regardless of approval or denial outcomes.

- A new welcome bonus cannot be earned on a card or its card family within 48 months of receiving a bonus on that same card, even if the earlier card was closed.

- Citi allows a person to hold two of the same card, such as two Custom Cash cards, as long as the 8-day and 65-day timing rules and exposure limits are met.

- Business card applications run on a separate track requiring roughly 95 days between applications and do not count against the personal 8-day or 65-day timing window.

Best for:

- Readers planning to apply for a new Citi card who want to avoid a denial from exceeding exposure limits or breaking timing rules.

- Cardholders who already have one or more Citi cards and are considering a duplicate card or a new card in the same family.

- Anyone recently denied for a Citi card who wants to understand reconsideration and credit line reallocation as alternatives to closing an account.

Does Citi Limit How Many Credit Cards You Can Have?

Citi does not cap the total number of credit cards one person can hold. No published rule says “five cards maximum” or “ten cards maximum.” Someone can hold three Citi cards, seven, or even more, as long as each new application meets the bank’s other requirements.

This is very different from American Express. Amex sets a hard limit of five credit cards per person at one time, plus a separate limit on charge cards. Citi does not work that way.

It also differs from Chase’s well-known 5/24 rule. Chase looks at all your recent card openings across every bank. Citi does not. Citi only cares about your history with Citi itself.

So the real question isn’t “how many cards can I have?” The real question is: “What does Citi actually check before approving another card?” The answer comes down to two things. First, your total credit exposure with Citi. Second, how recently you applied for other Citi products.

The rest of this guide walks through both, plus the timing and bonus rules that can trip up even strong applicants.

How Citi’s Total Credit Exposure Limit Works

Total credit exposure is the combined credit limit across every Citi card you hold. If you have a Citi Double Cash with a $10,000 limit and a Citi Custom Cash with $8,000, your exposure is $18,000. That number, not the card count, is what Citi watches most closely.

Every applicant has a personal ceiling. Citi decides where that ceiling sits using your income, your credit report, your history as a Citi customer, and internal risk scoring. The bank does not publish the exact formula. But once you hit your personal ceiling, new applications tend to get denied even if your credit score is strong.

This is why two people can look almost identical on paper and get very different results. One person earning $80,000 with clean payment history might be approved for a fourth Citi card. Another person with the same income but higher existing exposure might be denied. The card count is the same. The exposure is not.

Understanding this shifts your strategy. Instead of asking “am I at my card limit,” ask “am I near my exposure limit.” That single change in thinking prevents most surprise denials.

💡 Pro Tip: Before applying for another Citi card, add up your current Citi credit limits. If that number is already close to your annual income, expect Citi to want to shift limits from an existing card rather than approve fresh credit.

Income and Creditworthiness Factors

Citi looks at several factors when deciding your exposure ceiling. Each one carries weight, and they work together.

Income relative to existing credit. If your Citi limits already add up to a large portion of your yearly income, the bank sees less room to add more. A person earning $60,000 with $50,000 already extended by Citi has almost no headroom. Someone earning the same $60,000 with only $10,000 extended has plenty.

Credit score and report standing. A higher score signals lower risk. It doesn’t remove the exposure cap, but it can raise where that cap sits. Late payments, collections, or high utilization on other cards can lower it fast.

Payment history with Citi. If you’ve held a Citi card for years and always paid on time, the bank views you as a proven customer. That track record can push your ceiling higher. A new Citi customer with no internal history usually starts with a tighter ceiling, even with strong outside credit.

Citi also verifies your income during the application, so the number you enter should match what you can actually document. According to Citi’s own guidance, applicants must provide proof of income when applying, which includes pay stubs, tax returns, or bank statements.

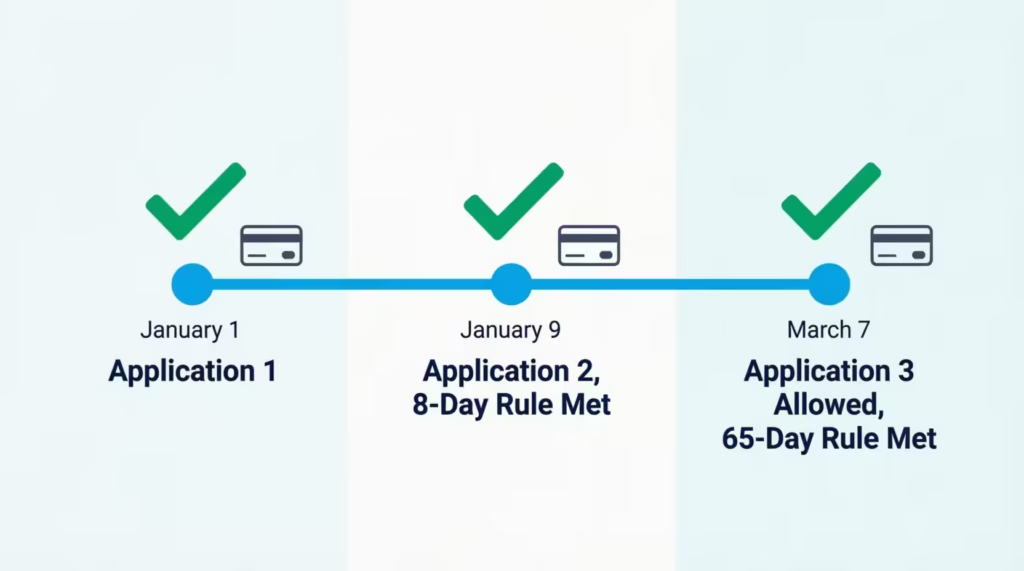

The 8-Day and 65-Day Application Rule

This is the timing rule most Citi applicants get wrong. It’s often called the 1/8/65 rule.

Here’s how it works: You can only submit one Citi personal card application every 8 days. You also cannot submit more than two Citi personal card applications within any 65-day sliding window. Both rules apply at the same time. Both apply whether the earlier application was approved, denied, or is still pending.

That last point matters. Some readers assume a denial “resets” the clock. It doesn’t. The application itself starts the count, not the outcome. Breaking either rule almost always leads to an automatic denial on the newer application.

Here’s a simple timeline to make it concrete:

| Date | Action | Status |

|---|---|---|

| January 1 | Apply for Citi Custom Cash | Application 1 |

| January 9 | Earliest date to apply for card 2 | 8-day rule met |

| January 9 | Apply for Citi Strata Premier | Application 2 |

| March 7 | Earliest date to apply for a third card | 65 days after Jan 1 |

If you apply for a third card before March 7 in that example, Citi will deny it based on the 65-day rule. The clock counts from the earliest of the two prior applications, not the most recent one.

⚠️ Mistake to Avoid: Applying for two Citi cards on the same day. The system usually approves the first and instantly denies the second because it violates the 8-day spacing. That’s a wasted hard inquiry that stays on your credit report for two years.

Can You Have Two of the Same Citi Card?

Yes. Citi is one of the few major issuers that allows a person to hold two of the exact same card. Someone could have two Citi Custom Cash cards, two Citi Double Cash cards, or two of another product.

This surprises many readers because most issuers refuse duplicate cards. Chase, Capital One, and Amex generally block a second copy of a card you already have.

The trick is that duplicate applications still follow the 8-day and 65-day timing. They also still count against your total exposure. So a second Custom Cash is possible, but only if your ceiling has room and your last Citi application is at least 8 days behind you.

People use this option for two reasons. First, to stack the $500-in-spend category bonus on the Custom Cash across two different $500 categories. Second, to run two intro APR periods on separate purchases without mixing them on one statement.

Business Cards vs. Personal Cards: Separate Rules

Citi’s application rules split into two separate tracks. Personal cards follow the 8/65 rule. Business cards run on their own clock. The two do not overlap in the way many readers assume.

A business card application does not count against your personal 8-day or 65-day window. And a personal card application does not push back your ability to apply for a business card. This is helpful if you want a mix of both product types in a short period.

The exposure question is more nuanced. Citi usually keeps business and personal credit separate. However, a large business line can still affect how the bank assesses your overall risk. Your business card’s credit limit usually doesn’t appear on your personal credit report. This is one reason many small business owners like them.

The 95-Day Business Card Rule

Business cards have their own spacing requirement. Citi typically wants at least 95 days between two business card applications. That’s noticeably longer than the personal 65-day window.

This matters if you plan to build out both personal and business accounts. A common plan looks like this. Apply for a personal Citi card on day 1. Apply for a Citi business card on day 30, since it’s on a different clock. Apply for a second personal card on day 66, once the 65-day window resets. Then wait until day 125 before another business card, since the business clock needs 95 days from the last business application.

Following that pattern lets you add four Citi cards in roughly four months without breaking any spacing rule. Just remember that exposure still applies. Every new card still needs room under your ceiling.

The 48-Month Bonus Eligibility Rule

Getting approved for a Citi card is one thing. Earning the welcome bonus is another. The 48-month rule can quietly block the bonus even when your application sails through.

The rule says you cannot earn a new welcome bonus on a card if you received a bonus on the same card, or a card in the same family, within the past 48 months. That’s four years. The clock does not reset if you close the old card. Closing it does not help you re-qualify.

Some readers assume closing a card and reapplying is a shortcut. It isn’t. The 48-month timer runs from the date you earned the earlier bonus, not from when the account was open or closed. This applies whether the earlier card is still active or has been shut down for years.

Card families matter here. The Citi Strata family, for example, groups certain premium travel cards together, so a bonus on one can lock you out of a bonus on another. Analysis from The Points Guy notes that Citi has expanded this family grouping over recent years, making the rule stricter than it once was.

To check whether a specific card is affected, read the fine print in the welcome offer. Look for language like “bonus points are not available if you have received a new account bonus for this card in the past 48 months.” That single sentence tells you whether the rule applies to the specific card you’re considering.

📌 Did You Know: Citi’s 48-month rule is stricter than Chase’s 24-month rule and looser than Amex’s once-per-lifetime rule. Knowing which issuer resets fastest can shape the order in which you apply for new cards.

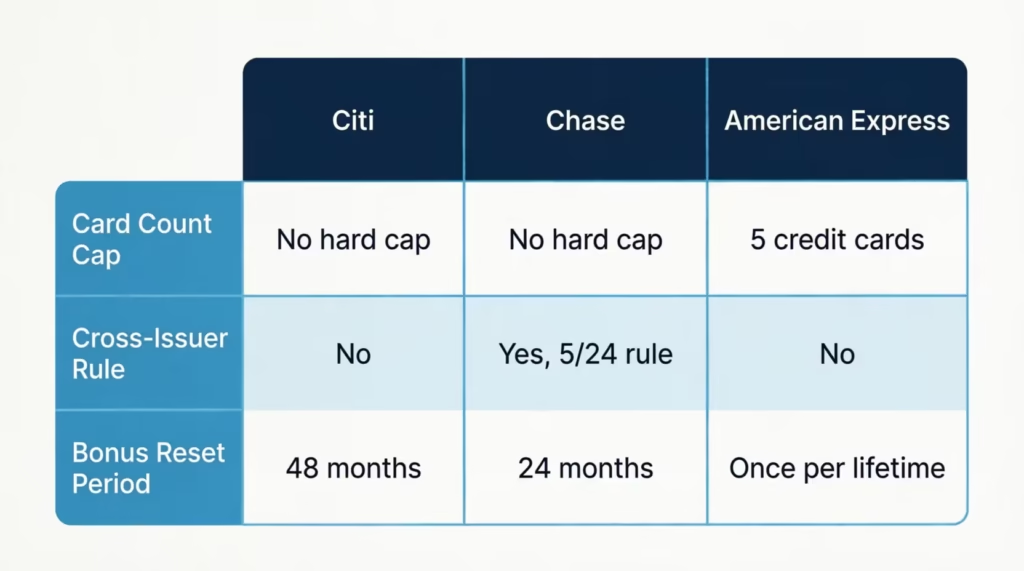

How Citi’s Rules Compare to Other Major Issuers

Citi’s approach makes the most sense when you compare it side by side with the other big issuers. Each bank uses a different strategy to control who gets approved.

| Issuer | Card Count Cap | Cross-Issuer Rule | Bonus Reset Period |

|---|---|---|---|

| Citi | No hard cap | No | 48 months (same/family) |

| Chase | No hard cap | Yes, 5/24 rule | 24 months (most cards) |

| American Express | 5 credit cards, 10 charge cards | No | Once per lifetime (usually) |

The table shows why “how many cards can I have” gets a different answer at every bank. Citi and Chase have no hard number cap but use timing and exposure to limit growth. Amex sets a firm cap. All three use bonus rules to keep you from farming welcome offers.

Does Citi Have a Chase-Style 5/24 Rule?

No. Citi’s timing rules only look at Citi applications. Applications and new accounts from Chase, Bank of America, Capital One, or any other bank do not count against you at Citi.

This is very different from Chase. NerdWallet explains that Chase’s 5/24 rule automatically denies you for many Chase cards if you’ve opened five or more personal cards from any bank in the past 24 months.

For a heavy card user, this difference is useful. You could open several cards at other banks and still apply at Citi without penalty, as long as your Citi-specific timing is clean and your exposure has room.

How Citi’s Card Limit Compares to American Express

Amex takes the opposite approach. It caps most people at five credit cards at once, plus up to ten charge cards. Once you hit five credit cards, a new credit card application usually gets denied even if your credit is strong.

Citi has no such rule. Someone could hold six, seven, or eight Citi cards if their exposure and timing allow it. The philosophies differ. Amex controls total volume with a simple count. Citi controls it with a dollar-based ceiling and timing gates.

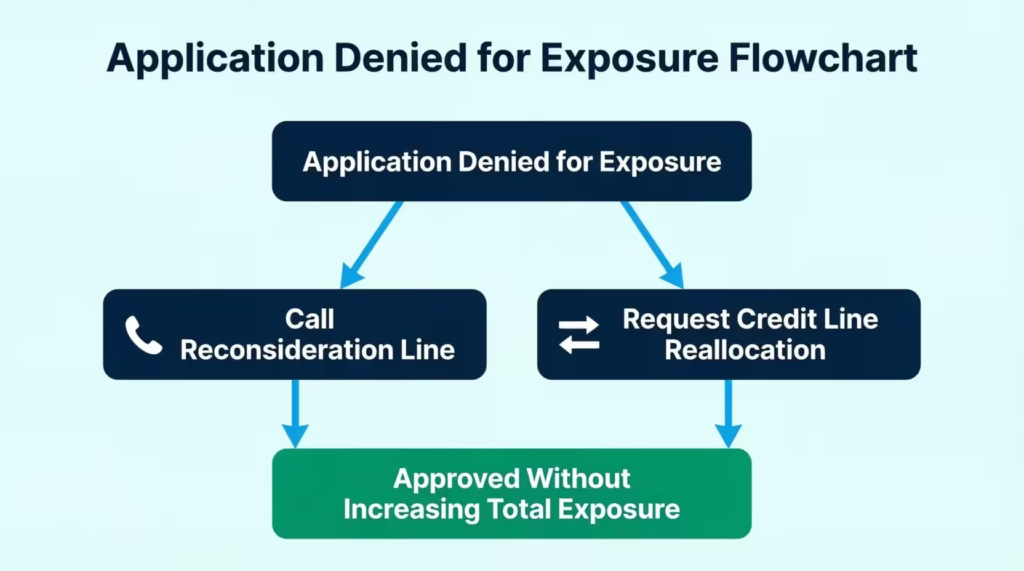

What Happens If Citi Denies You for Too Much Exposure

A denial for high exposure is not the end of the road. It just means Citi has decided not to add more credit right now. There are two clear paths forward, and both are worth trying before you close a card or write off the application.

Calling the Reconsideration Line

The reconsideration line is a phone team at Citi that can review your denied application by hand. A live agent looks at your file, and you can explain your situation directly. Sometimes a denial reverses on the spot.

More often, the agent offers a trade. They approve the new card, but only if you agree to shift some of your existing credit limit to it.

For example, if you already have $15,000 on a Citi Double Cash and Citi doesn’t want to extend more, the agent might approve a new Custom Cash by moving $5,000 from the Double Cash. Your total exposure stays flat. You still get the new card.

To try this route, call Citi’s main credit card customer service line shortly after the denial and ask to be transferred to reconsideration. Have your income, employment, and reasons for wanting the card ready. Be polite and specific. Vague requests tend to get vague denials.

Requesting a Credit Line Reallocation

Reallocation is when you ask Citi to move a limit from one card to another instead of adding new credit. It’s useful even if you didn’t get denied, because it lets you shape your card lineup without expanding total exposure.

A few requirements apply. Both cards usually need to be open for at least six months. The move typically triggers a hard inquiry, so it’s not a free action. And some reallocation requests get routed to a specialized team, especially if the amounts are large or the cards are premium products. Approval is not automatic.

The trade-off is worth thinking about. Reallocation preserves your total available credit, which keeps your utilization ratio steady. Closing a card, by contrast, removes that credit entirely. If your goal is to make room for a new card, reallocation is almost always the safer play.

Should You Close a Card to Get Approved for a New One?

Closing an old Citi card can free up exposure and clear the way for a new approval. It’s a real strategy, and it works. But the tradeoffs matter, and there’s usually a better move.

Closing a card removes its credit limit from your total available credit. That drop can push your utilization ratio up on other cards, which often lowers your credit score. If you carry any balance elsewhere, this hit can be noticeable.

Closing an older account also shortens your average account age over time. FICO and VantageScore both reward longer credit history. A card you’ve held for eight years contributes more to your average age than a card you’ve had for one year. Closing the older card removes that anchor from your report once it eventually drops off (which can take up to ten years).

A better move in most cases is to reallocate the limit first, then close. Move the credit from the card you want to close over to a keeper card. Now Citi’s exposure for you is unchanged, and you preserve the total limit. Then close the original card. Your utilization stays healthy because the limit moved rather than disappeared.

There are exceptions. If the card has an annual fee you don’t want to pay, and Citi refuses to waive it or downgrade the card, closing may be the right call. If the card is very new and you have not built much history on it yet, closing has less impact. In these cases, the tradeoffs are smaller, and the freed exposure can help a new application go through.

Frequently Asked Questions (FAQs)

How many Citi cards can I have?

Citi sets no fixed cap on the number of cards one person can hold. Approval instead depends on your total credit exposure across all Citi cards and how recently you applied for other Citi products.

What is the 8/65 rule for Citi?

You can submit only one Citi personal card application every 8 days, and no more than two within any 65-day window. Both rules run from the date you applied, not the outcome, so a denial does not reset the clock.

What is the 48-month rule for Citi cards?

You cannot earn a new welcome bonus on a card if you got a bonus on that same card or its card family within the past 48 months. The timer starts from when you earned the earlier bonus and does not reset if you close the account.

Does Citi have a 5/24 rule like Chase?

No. Citi reviews your application history only with Citi, so cards opened at Chase, Amex, or any other bank do not affect your Citi approval.

What is the hardest Citi card to get approved for?

Approval odds tighten as your total Citi credit exposure gets closer to your income. A strong applicant can still get denied for a premium card if existing Citi limits already use up most of their exposure ceiling.

Can you have two of the same Citi card?

Yes, Citi allows a person to hold two of the same card, such as two Custom Cash cards. Both applications still must follow the 8-day and 65-day spacing rules and count against your total exposure.

What happens if Citi denies you for too much exposure?

You can call Citi’s reconsideration line, where an agent may approve the card if you agree to shift some credit limit from an existing card. You can also request a credit line reallocation to move a limit to a new card without adding total exposure.

Should you close a Citi card to get approved for a new one?

Closing a card frees up exposure but removes that credit limit from your total available credit, which can raise your utilization ratio and lower your score. Reallocating the limit to a keeper card first, then closing, usually protects your utilization better.

What is the 95-day rule for Citi business cards?

Citi typically requires at least 95 days between two business card applications, separate from the personal 8/65 timing. Business and personal application clocks run independently, so one does not delay the other.

Bottom Line

To get the most from Citi, focus on three key points:

- There’s no limit on the number of cards you can have.

- Total credit exposure is what really matters.

- The 8/65 and 48-month timing rules affect your application options.

Business cards run on a separate 95-day track. If a denial happens, reconsideration and reallocation almost always beat closing an account.

Citi’s rules favor planning applications based on exposure and timing. This approach, rather than focusing on card count, gives most readers the best chance of approval.

If you know someone stacking Citi cards for travel points or bonuses, share this guide. It can help them avoid a hard inquiry and a preventable denial.