I’ve been there. You’ve had your Citi card for a while, you pay it on time, and now you’re eyeing a better one with richer rewards. But you don’t want to close your account or take a credit score hit just to get there. The good news? A Citi credit card upgrade lets you switch cards without applying for a new one.

The fastest way to upgrade is to call Citi at 1-800-950-5114 and request a product change to a card within your eligible family.

Below, you’ll find every step, every catch, and every smart move to make this work in your favor.

Key Takeaways

This guide explains how to upgrade a Citi credit card through a product change, covering how to call and request one, eligibility requirements, what carries over to the new card, how rewards and annual fees are handled, and when applying for a new card makes more sense.

Core Facts:

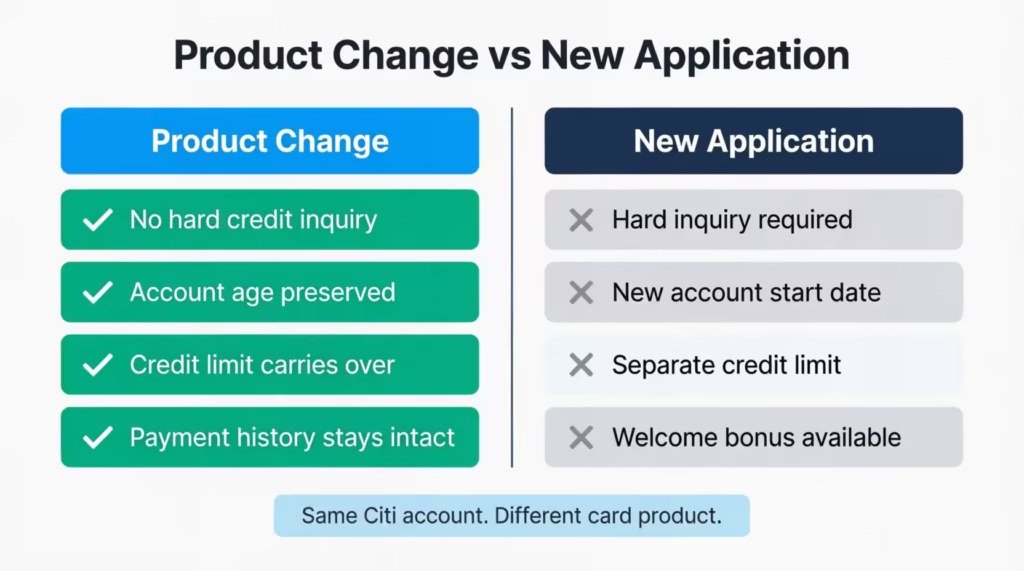

- A Citi product change switches your existing account to a different card without closing it or opening a new one, meaning no hard credit inquiry and no reset to your account age or payment history.

- The primary method is calling Citi customer service at 1-800-950-5114 and asking a rep to move your account to a specific card; online upgrades are not generally available.

- Most accounts must be open for at least 12 months before a product change is approved, though some reps may approve requests after 6 to 9 months.

- Product changes do not include the welcome bonus offered to new applicants, which can represent significant value on premium cards.

- Your credit limit, account opening date, and payment history all carry over; your card number may change if the new card runs on a different payment network.

- Annual fees are typically prorated when upgrading mid-year, with unused portions returned as a statement credit; timing and amounts should be confirmed with the rep before accepting.

Best for:

- Citi cardholders who want better rewards or benefits but prefer to avoid a hard credit inquiry or losing established account history.

- People who are ineligible for a welcome bonus due to Citi’s 48-month rule and have little to gain from a fresh application.

- Cardholders moving between cards in the same rewards family who want their existing points balance to transfer automatically.

What It Means to Upgrade a Citi Credit Card

A Citi credit card upgrade is officially called a product change. It’s when you swap your current card for a different one inside the same issuer’s lineup, while keeping the same account open. You’re not applying for a new card. You’re not closing the old one. You’re simply changing the product attached to your existing account.

This matters for two big reasons. First, a product change does not trigger a hard credit inquiry. A new application would. That means your credit score is safe from the small dip that comes with a fresh pull. Second, your account history stays intact. The age of your account, your on-time payment record, and your credit limit all carry over to the new card.

Think of it like changing the engine in a car you already own. The car is the same, the title is the same, but what’s under the hood is different. Your credit profile sees one account, not two, and the open date doesn’t reset.

This is the core reason people choose this path. You get the perks of a newer or better card without giving up the credit history you’ve already built.

📌 Did You Know: Because a product change keeps the same account number internally, your average age of accounts is preserved, which is a factor that makes up 15% of your FICO score.

How to Upgrade Your Citi Credit Card

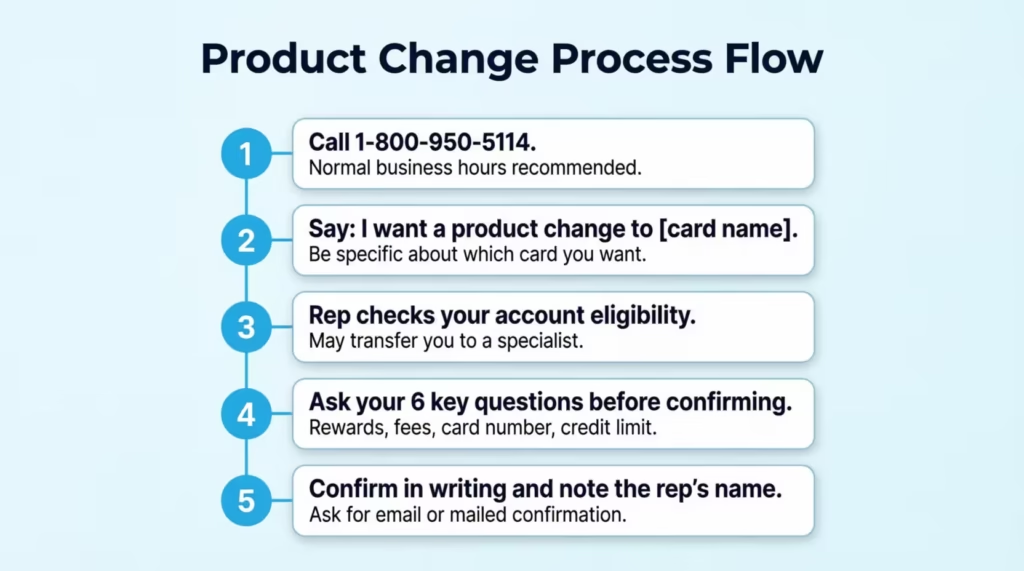

The most reliable way to request a product change is by phone. Citi’s main customer service line is 1-800-950-5114. You can also find a direct number on the back of your card. Call during normal business hours for the smoothest experience.

When the agent picks up, say something simple and clear, like: “I’d like to request a product change on my current Citi card. I’d like to switch to the [name of the card you want].” That’s it. The rep will pull up your account, check if you qualify, and walk you through the options.

Most calls take 15 to 25 minutes. The rep may need to transfer you to a specialist who handles product changes. That’s normal. Stay on the line and have your card details ready.

If the first rep says no, politely thank them and call back later. Different agents sometimes give different answers based on what offers are loaded into the system for your account.

Can You Upgrade a Citi Card Online or Through the App?

For most cardholders, online product changes are not available. Citi does not offer a general “upgrade” button inside your online dashboard, the way some other issuers do. The phone is still the main route.

That said, you may sometimes see a banner inside your online account or the Citi mobile app inviting you to switch to a specific card. If you see one of these offers, you can usually accept it right there with a few clicks. But these are limited and only show up for select accounts.

If you don’t see an offer, don’t waste time hunting through menus. Just call.

Responding to a Targeted Upgrade Offer

Citi sometimes sends targeted upgrade invitations by mail, email, or as a notice inside your online account. These offers are pre-approved for your specific account. They often come with a small bonus, like extra ThankYou Points or a statement credit, if you accept within a deadline.

These targeted offers are worth grabbing when they line up with the card you actually want. The link in the email or the banner inside your account takes you straight to a short confirmation page. No phone call needed.

Before you click accept, read the fine print. Check the new card’s annual fee, the rewards structure, and the offer’s expiration date. Targeted offers usually lock you into specific terms, so make sure they match what you’d ask for on a phone call.

Questions to Ask the Rep Before Confirming the Upgrade

Before you say yes on the phone, ask these questions. They protect your rewards, your wallet, and your peace of mind.

- Will my existing ThankYou Points or miles transfer to the new card? This is the most important question if you’re moving between card families.

- Will my card number stay the same, or will I get a new one? This affects any auto-pay setups you have linked.

- Is the annual fee being prorated, refunded, or charged again? Timing matters here.

- Does this upgrade come with any welcome bonus or statement credit? Targeted offers sometimes include one.

- Will my credit limit stay the same? It usually does, but confirm.

- When will the new card arrive, and when does my old card stop working?

Write down the rep’s name and the time of the call. If anything goes sideways later, having that record helps fix it fast.

💡 Pro Tip: Ask the rep to email or mail you a written confirmation of the change. Verbal promises about fee proration or bonus offers are easier to dispute when you have something in writing.

Which Citi Cards You Can Upgrade To

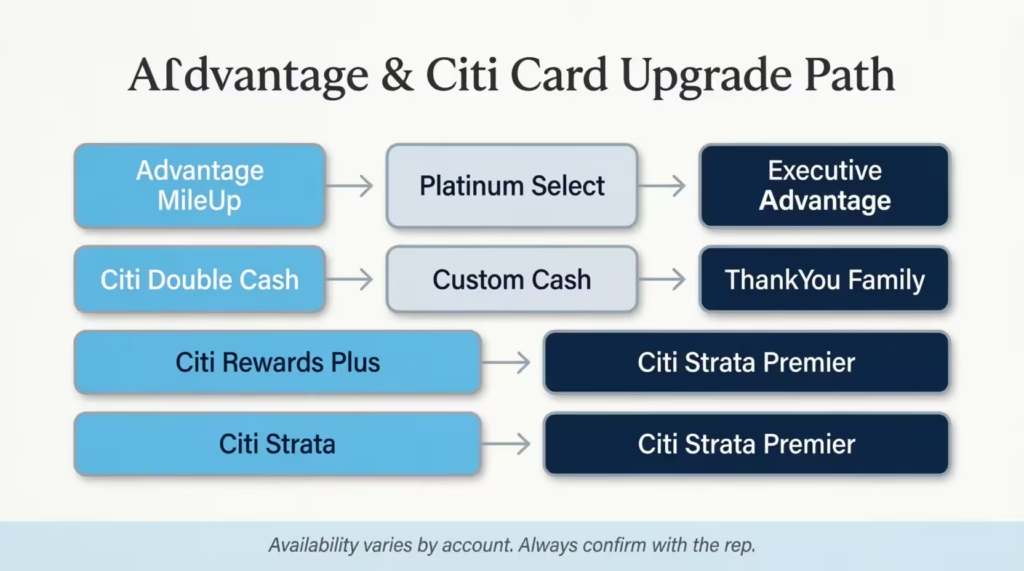

Citi groups its cards into a few families. The card you can move into depends on the family your current card belongs to and what’s available for product changes at the time of your call.

Common upgrade paths include:

- Citi AAdvantage MileUp to the Citi AAdvantage Platinum Select, then to higher-tier AAdvantage cards like the Executive.

- Citi Double Cash to the Citi Custom Cash, or sometimes into the ThankYou family.

- Citi Rewards+ to the Citi Strata Premier for richer travel rewards.

- Citi Strata to the Citi Strata Premier for travelers who want bigger bonus categories.

Not every card is open as an upgrade target. Some premium cards, like the Citi Strata Elite, may require a fresh application instead. Always ask the rep which products are available for your account before deciding.

Citi’s Cross-Family Flexibility vs. Other Issuers

Here’s where Citi stands out. Unlike Chase, which keeps tight rules about moving between Sapphire and Freedom cards, Citi is sometimes willing to move you across card families. For example, you may be able to switch from an AAdvantage co-branded card to a ThankYou Points card.

This kind of cross-family move is not guaranteed. It depends on the rep, the offers loaded for your account, and the current Citi policy. But it’s worth asking. American Express, by contrast, rarely allows you to leave a co-branded card (like Hilton or Delta) for a Membership Rewards card through a product change.

If you want to switch loyalty currencies, Citi gives you the most flexibility of any major issuer. Just be ready to redeem your existing rewards first, because they may not convert.

Eligibility Requirements for a Citi Card Upgrade

Before Citi approves a product change, your account needs to meet a few baseline checks. These are not as strict as a new card application, but they still matter.

The basics include:

- Your account must be open and active.

- You must be current on payments, with no late fees in recent months.

- Your account must be in good standing, meaning no over-limit balances or recent disputes.

- You must have held the card long enough to qualify (more on that below).

Citi also looks at your overall relationship. If you have other Citi accounts, that history factors in. A cardholder with a steady payment record and low utilization is far more likely to get approved than someone who’s been bouncing near their credit limit.

How Long You Need to Have the Card Before Upgrading

The standard waiting period is at least 12 months from the date you opened the card. This isn’t a random rule. It traces back to the Credit CARD Act of 2009, which requires issuers to honor the terms of a card for at least the first year before changing them in ways that affect the customer.

Some Citi reps may approve a product change after just 6 to 9 months, especially if it doesn’t involve a major fee jump. But planning for the full 12-month wait is the safer bet. If you call too early, you’ll likely be told to try again later.

Credit Score and Account Standing Requirements

Citi typically looks for a FICO score around 700 or higher for most mainstream product changes. Premium upgrades, like moving into the Strata Premier or Executive AAdvantage, may need a score closer to 740.

Beyond the number, your account standing matters more than people think. A clean record of on-time payments over the last 6 to 12 months carries real weight. If you’ve missed a payment recently, fix the issue first, then wait a few cycles before calling.

Low credit utilization also helps. Keeping your balance under 30% of your credit limit signals to Citi that you handle credit responsibly.

⚠️ Mistake to Avoid: Don’t apply for several new credit cards in the weeks before requesting an upgrade. Even though the upgrade itself has no hard pull, recent inquiries can make Citi cautious about approving the change.

What Stays the Same After a Citi Card Upgrade

This is the part most people care about. A product change preserves the parts of your account that protect your credit profile. Here’s what carries over:

- Your account opening date. The age of your account does not reset.

- Your credit limit. It stays at the same amount, unless you ask for an increase.

- Your payment history. Every on-time payment you’ve made stays on the account.

- Your account number (in most cases). If you’re staying within the same network, like Mastercard to Mastercard, the number often stays.

This is huge for your credit score. The length of your credit history and your credit utilization ratio both stay stable. You don’t lose ground just because you switched products.

For someone who’s had the same card for five or seven years, a product change is the only way to get a better card without sacrificing that valuable account age.

What May Change After the Upgrade

Not everything stays put. A few things may shift when you switch products:

- Your card number may change if you’re moving to a different network. For example, if your current Citi card runs on Mastercard and the new one runs on Visa, you’ll get a new number. That means updating any auto-pay or subscription services linked to the old card.

- Your APR may change to match the new card’s terms.

- Your reward-earning rates will reflect the new card’s structure.

- The card benefits, like purchase protection, travel insurance, or extended warranty, may differ.

- The annual fee may increase or decrease depending on which card you switch to.

The rep can confirm exactly what changes for your specific upgrade. Always ask.

What Happens to Your Citi Rewards Points When You Upgrade

If you’re upgrading inside the same rewards family, your points transfer automatically. ThankYou Points stay as ThankYou Points. AAdvantage miles stay as AAdvantage miles. Cash back balances move over as cash back.

The transfer usually happens within one to two billing cycles. You don’t need to take any action. Just keep an eye on your account during the switch to confirm the balance shows up correctly.

Upgrading from a basic ThankYou card to a premium one, like the Strata Premier, can actually boost the value of those points. Premium cards often unlock transfer partners and better redemption rates that weren’t available on the entry-level card. Your existing balance suddenly becomes worth more, without you doing anything extra.

The Risk of Switching to a Different Rewards Currency

Here’s where things get tricky. If you’re moving between card families with different rewards currencies, your existing points or miles may not transfer.

For example, switching from a Citi AAdvantage card (which earns American Airlines miles) to a Citi Double Cash (which earns ThankYou Points or cash back) means your AAdvantage miles stay tied to your AAdvantage account, but the card earning them is gone.

The miles themselves usually survive in your AAdvantage frequent flyer account, but you’ll lose the card-linked benefits, like priority boarding or free checked bags.

The safest move is to redeem or use your existing rewards before you upgrade, especially when crossing currencies. Book the flight, transfer the points, or cash out the balance. Then make the switch with a clean slate.

Ask the rep directly: “Will my current rewards balance survive this product change, or do I need to use it first?” Their answer should match what you find in the card’s terms.

How the Annual Fee Is Handled During an Upgrade

The annual fee is one of the most confusing parts of any upgrade. Here’s how it usually works.

If you’ve already paid the annual fee on your current card and you upgrade mid-year, Citi typically prorates the refund. You get back the unused portion of the fee, often as a statement credit. The new card’s annual fee then gets charged based on its own schedule.

For example, say you paid a $95 fee in March on your old card, and you upgrade in September. You’d get back roughly six months’ worth of that fee, about $47, as a credit. Then the new card’s fee, say $99, may be charged at the time of upgrade or at your next anniversary, depending on the rep and the card.

This proration practice is shaped by the Credit CARD Act, which requires fair treatment of annual fees when account terms change. Always confirm the exact timing and amount before you say yes. Ask: “When will the new fee post, and will I get a refund for the unused portion of my current fee?”

If the upgrade lowers your annual fee or removes it entirely, the math gets simpler. You just stop paying it going forward, and any unused portion comes back as a credit.

The Sign-Up Bonus Tradeoff

This is the biggest catch of a product change. When you upgrade, you do not get the welcome bonus that new applicants for that card receive.

Welcome bonuses are often the most valuable part of a credit card. A card like the Strata Premier may offer 70,000 or more ThankYou Points to brand-new customers who hit a spending requirement. If you upgrade to that card, you skip the bonus entirely.

That’s a real cost. Those points could be worth $700 to $1,400 in travel rewards, depending on how you redeem them.

There’s also Citi’s 48-month rule to keep in mind. For many Citi cards, you can only earn the welcome bonus once every 48 months on the same card family. If you upgrade now and then close the new card later to reapply, you may still be locked out of the bonus.

This is why the upgrade-versus-apply question is so important. Sometimes the smarter move is to apply fresh, even with the hard inquiry, just to capture the welcome offer.

Upgrade vs. Apply for a New Card: Which Makes More Sense

This is the final decision, and it comes down to a simple tradeoff. Choose upgrade if any of these apply to you:

- You want to keep your account age and avoid a hard credit inquiry.

- You’re not eligible for the welcome bonus (you’ve had the card or family recently).

- You’re happy skipping the bonus in exchange for a clean, fast switch.

- Your credit score recently took a hit, and you don’t want another inquiry.

- You’re moving between similar cards where the bonus isn’t huge.

Choose to apply for a new card if any of these apply:

- The welcome bonus is large, and you qualify for it.

- You can absorb a small, short-term dip in your credit score from a hard pull.

- You want to keep your old card open for its credit limit and history, while adding the new one.

- The new card is in a family, Citi won’t let you cross into it through a product change.

For most people who already have a Citi card and just want better rewards without the bonus, the product change wins. For people chasing maximum value, especially on a premium card with a rich welcome offer, a fresh application is usually the better play.

Run the math. If the welcome bonus is worth more than the temporary credit score impact and the loss of one account, apply for a new. If not, upgrade.

Frequently Asked Questions (FAQs)

Can I upgrade my Citibank credit card?

Yes, Citi allows you to switch to a different card within its lineup through a process called a product change. The fastest way to request one is by calling Citi customer service at 1-800-950-5114 and asking the rep to move your account to a specific card.

How does upgrading a credit card work?

A Citi card upgrade, called a product change, switches your existing account to a different card in the lineup without closing the account or opening a new one. Your credit history and limit carry over, but the rewards structure and annual fee shift to match the new card’s terms.

Does upgrading a credit card cause a hard inquiry?

No, a Citi product change does not trigger a hard credit inquiry, unlike applying for a new card. Your account stays open under the same terms, so your credit score is not affected by the switch itself.

Can I upgrade my credit card without affecting my credit score?

A Citi product change keeps the same account open, preserving your account age, payment history, and credit limit, so your score is not impacted. The only scenario that could affect your score is if the upgrade involves a network change that requires a new card number, and you miss updating auto-pay.

What can I upgrade my Citi Double Cash card to?

The Citi Double Cash can typically be upgraded to the Citi Custom Cash or into the ThankYou Points card family, depending on what is available for your account at the time. Ask the rep which products are loaded for your specific account when you call.

What is the Citibank 48-month rule?

Citi restricts welcome bonus eligibility so that you can only earn a bonus on the same card family once every 48 months. If you upgrade rather than apply fresh, you skip the bonus entirely, and the 48-month clock still applies if you later close and reapply.

What is the hardest Citi credit card to get?

Premium Citi cards like the Strata Elite typically require a fresh application rather than a product change, which suggests stricter approval standards than standard upgrade paths. A FICO score closer to 740 or higher is generally needed for top-tier Citi cards.

What happens to my card number when I upgrade a Citi card?

Your card number typically stays the same when you stay on the same network, such as Mastercard to Mastercard, but changes if you move to a different network. Updating auto-pay and subscription services is necessary any time a new card number is issued.

Bottom Line

Switching to a better Citi card doesn’t have to mean a new application or a credit score hit. A product change lets you keep your account history, your credit limit, and most of your rewards, while unlocking better perks. We’ve covered how to call, what to ask, who qualifies, what stays the same, and where the real tradeoffs live, like the missed welcome bonus and the rewards currency risk.

Based on the math, the most effective approach is to upgrade when you’d skip the bonus anyway, and apply new when a rich welcome offer beats the small credit dip.

If you know someone holding an entry-level Citi card and wondering if they’re leaving rewards on the table, share this guide. It could save them hours on the phone and hundreds in lost value.