Closing a credit card sounds simple until you actually try it. You worry about losing your points, hurting your credit score, or getting stuck with a surprise fee. When it comes to figuring out how to cancel a Citibank credit card, most guides skip the details that actually matter, like the strict 60-day points deadline or what to say when the agent tries to change your mind.

The safest way to cancel a Citi card is to redeem your points, pay off your balance, then call 1-800-950-5114 and ask for account closure in writing.

We’ll walk you through every step below, from the pre-cancel checklist to the exact phone script, credit score math, and how to confirm your account is truly closed.

Key Takeaways

This guide explains how to cancel a Citibank credit card, including the correct order of steps, the phone script for closure, the 60-day ThankYou points deadline, and the credit score effects of closing an account.

Core Facts:

- ThankYou points expire 60 days after a Citi account closes, so points should be redeemed or transferred before calling to cancel.

- The recommended cancellation method is calling 1-800-950-5114 and requesting account closure along with written confirmation.

- Closing a card does not erase an existing balance; interest continues accruing until the balance is paid to zero.

- Closing an account can raise credit utilization, since one example showed utilization rising from about 12% to about 22% after a card closed.

- Closed accounts in good standing remain on a credit report for up to 10 years and continue counting toward average account age.

- Confirming closure requires checking the online account after 3 to 5 business days and reviewing the credit report within 30 to 60 days.

Best for:

- Cardholders who want to close a Citi card without losing ThankYou points or triggering unexpected fees.

- People concerned about how closing a card will affect their credit utilization or credit score.

- Anyone who wants the exact phone script and questions to ask before ending a cancellation call.

Before You Cancel: A Quick Checklist

Rushing to cancel a Citi credit card is where most people lose money. The account closure process is not just one phone call. It is a sequence, and doing it in the wrong order can cost you rewards, trigger interest charges, or break your auto-pay on important bills.

Work through the three steps below in this exact order. Redeem first, settle the balance second, move recurring payments third. Only then should you close the card. This order protects your money, your credit, and your peace of mind.

💡 Pro Tip: Do not cancel on a Friday afternoon. If something goes wrong with your final statement or a pending charge, you want banking hours the next day to fix it, not a two-day wait.

Redeem or Transfer Your ThankYou Points First

Your Citi ThankYou points do not stick around after you close the card. Once the account is closed, you have only 60 days to use them before they expire for good. This is not the 90-day window many blogs still quote. According to Citi’s own ThankYou Rewards FAQs, points from a closed account expire after 60 days, and this applies even if you still hold another Citi ThankYou card.

Before you make the cancellation call, log in to ThankYou.com and check your balance. You have a few solid options:

- Transfer points to another Citi card you keep open. If you have a Citi Double Cash Card, Citi Premier, or Citi Strata Premier, move the points over. They keep their full value, and no clock starts ticking.

- Transfer to a Citi airline or hotel partner if you hold a card that allows it. Popular partners include Choice Hotels, Wyndham, JetBlue, and Turkish Airlines. Transfers are usually instant or complete within a day.

- Redeem for statement credit, gift cards, or travel through the ThankYou portal. Cash back is worth 1 cent per point, and gift cards sometimes offer small bonuses.

If you live in New York, a state law called General Business Law § 520-e gives cardholders a grace period to use rewards after account changes. As Troutman Pepper reports, this law went into effect on December 10, 2023, and it requires issuers to give New York residents advance notice before rewards are canceled or forfeited. Still, do not rely on this as your safety net. Redeem before you cancel.

Confirm Your Remaining Balance and Payment Obligations

A common myth is that closing a credit card wipes out what you owe. It does not. Closing the account stops new spending, but any outstanding balance stays with you, and interest keeps building until it is paid off.

Before you call:

- Check your current balance in the Citi Mobile App or online at citi.com.

- Look at your last statement date and next due date.

- Note any pending transactions that have not yet posted.

You have two paths here. If you can pay the balance in full, do it before the cancellation call. That way, your final statement is clean, and there is nothing to argue about later. If you cannot pay it off, that is okay too. You can still close the card. Citi will keep sending you monthly statements, and you will keep making minimum payments at the same interest rate until the balance hits zero.

Watch out for the annual fee. If your card has one and the fee posted within the last 30 days, Citi may prorate a refund when you close the account. If it posted more than 30 days ago, you might not get anything back. Ask the agent about annual fee proration during the call.

Move Recurring Charges and Auto-Pay Elsewhere

This is the step people forget, and it causes real headaches later. If your Citi card is set up for auto-pay on Netflix, your gym, your car insurance, or Amazon, those charges will start failing the moment the card is closed. Some services will send a warning email. Others will just suspend your account without notice.

Take 15 minutes to make a list. Check your last three statements for anything that looks like a recurring charge. Then update each one with a new payment method before you cancel. Common ones to check:

- Streaming services (Netflix, Hulu, Spotify, Disney Plus)

- Utilities and phone bills

- Insurance premiums

- Subscription boxes and app subscriptions

- Charity donations

- Gym or fitness memberships

- Cloud storage (iCloud, Google One, Dropbox)

If you use a digital wallet like Apple Pay or Google Pay, remove the Citi card there too so it does not accidentally get charged.

How to Contact Citibank to Cancel Your Card

Now the real work starts. Knowing how to cancel Citibank credit card requests through the right channel saves time. Not every method works for every card, and some methods are faster than others. You have three main paths: phone, online or app messaging, and mail. Only one of them gets the job done in a single call.

Canceling by Phone

Phone is the fastest and most reliable way. Citi customer service is available 24/7 for most card types, and a live agent can close the account, confirm your final balance, and email you confirmation before you hang up.

Call the number on the back of your card. If you already cut it up, dial 1-800-950-5114 for general Citi credit card support. For Spanish, call 1-800-947-9100.

Have this ready before you dial:

- Your card number or account number

- The last four digits of your Social Security number

- Your billing ZIP code

- A pen and paper to write down the agent’s name, employee ID, and the closure reference number

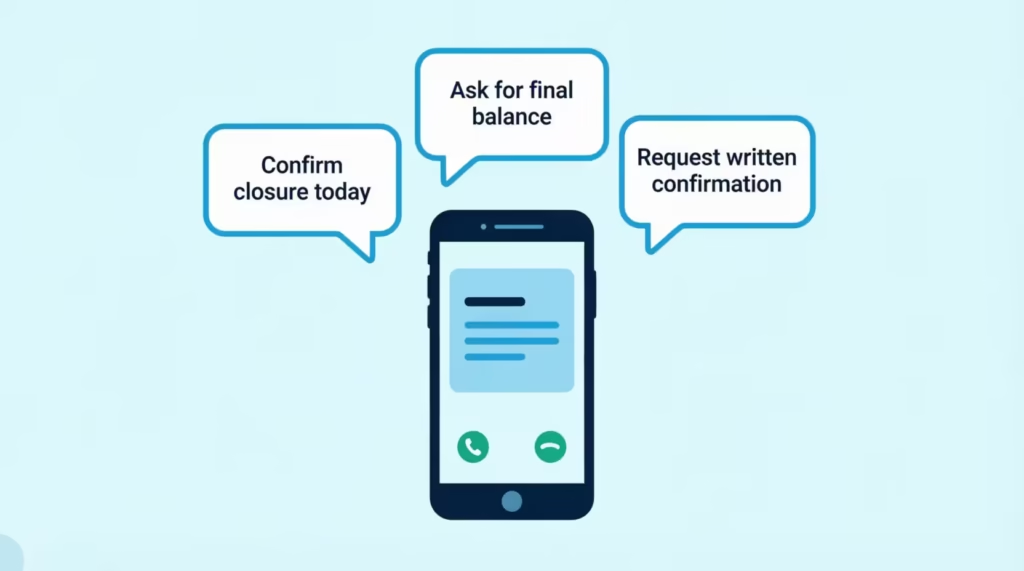

When the agent picks up, be direct. Say something like: “I want to close my Citi credit card account today. Please process the closure and send me written confirmation.” Do not leave room for confusion. The agent will verify your identity, ask a few questions, and then likely offer a retention deal (more on that below). Politely decline and repeat your request.

Ask these three questions before you end the call:

- Is my account officially closed as of today?

- What is my final balance, and when is it due?

- Will I get written confirmation by mail or email?

Write down the answers. If the agent will not close the account or keeps stalling, ask to speak with a supervisor.

Canceling Through Online Account or Mobile App

Citi’s online portal and mobile app do not always let you close a card with a single click. For some accounts, you can send a secure message through your online account requesting closure.

This works, but it is slower. You may wait one to three business days for a response, and Citi may still call you to verify identity before processing.

To try this route:

- Log in at citi.com or open the Citi Mobile App (iOS or Android).

- Go to “Services” or “Help & Contact Us.”

- Choose “Send a Secure Message” and select a category like “Account Services” or “Close Account.”

- Type a clear message: “I request that the account ending in [last 4 digits] be closed. Please confirm closure in writing.”

If the app shows a “Close Account” button in your account settings, use it. Not all cards have this option. If nothing works within a few days, call instead. Do not assume silence means the account is closed.

Canceling by Mail or In Person

Mail is the slowest option, but some people prefer it because it creates a paper trail. Write a short, dated letter that includes your full name, account number, mailing address, phone number, and a clear request to close the card. Sign it. Send it certified mail with a return receipt to:

Citibank Customer Service P.O. Box 6500 Sioux Falls, SD 57117

Keep a copy for yourself. Expect the process to take two to four weeks.

You can only close your account in person at a Citi branch if your card is linked to a Citi bank account. Even then, the branch typically just calls the credit card line for you. It rarely saves time.

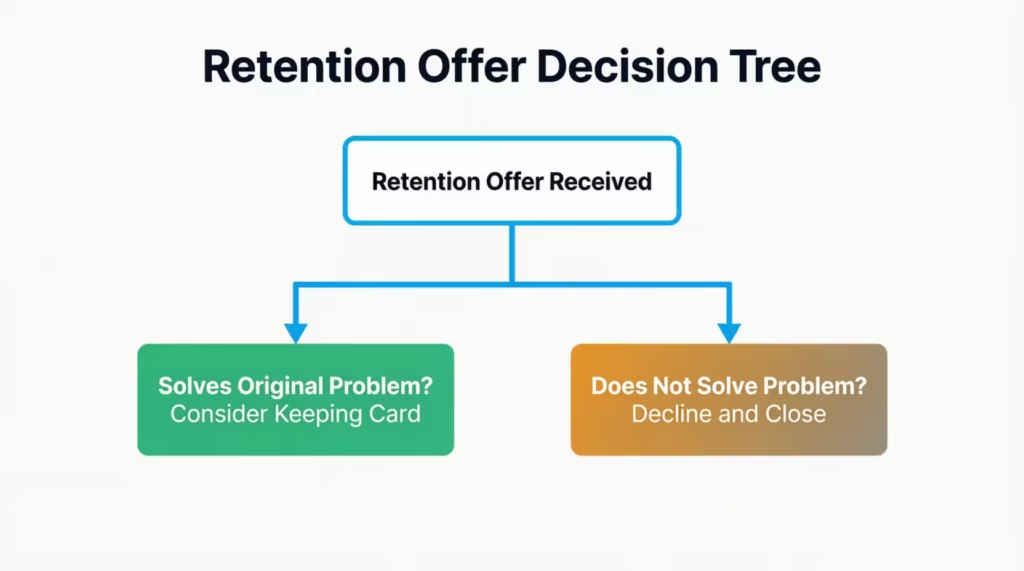

Handling a Retention Offer

When you ask to cancel, the agent may pause and offer you something to stay. This is called a retention offer, and it is a normal part of the account closure process. Citi trains its agents to keep customers, so expect it.

Common retention offers include:

- A statement credit of $50 to $200

- Bonus ThankYou points, often 5,000 to 20,000

- A waived or partially refunded annual fee for the current year

- A lower interest rate for a set period

Whether to accept is your call. Ask yourself two questions. First, does the offer solve the reason you were canceling in the first place? If you were closing because the annual fee stopped being worth it, a one-year fee waiver may make sense, but only if you plan to use the card. Second, will you actually use the card enough to earn back the value? If not, the offer is a distraction.

To firmly decline, say: “Thank you, but I’ve decided to close the account. Please process the closure now.” Do not explain, apologize, or negotiate. If the agent keeps pushing, repeat the sentence word for word. You are not being rude. You are being clear.

⚠️ Mistake to Avoid: Do not accept a retention offer without reading the fine print. Some fee waivers come with spending requirements, like $1,000 in 90 days, or they only apply if you keep the card open for another 12 months.

What Happens to Authorized Users

If you added a spouse, child, or family member as an authorized user on your Citi card, closing the account cancels their access too. Their card stops working the same day yours does. Citi does not send them a heads-up, so the responsibility to warn them falls on you.

Before you cancel:

- Tell each authorized user the exact day you plan to close the card.

- Remind them to move any auto-pay or recurring charges off the card.

- Return or shred their physical card once it is deactivated.

If the authorized user relied on this card for their own credit history, closing it may cause a small dip in their credit score too.

This depends on how long the account was open and how much of their total credit limit came from your card. If they want to keep building credit, help them apply for a starter card or become an authorized user on a different account before you close yours.

If you only want to remove the authorized user without closing your account, that is a separate request. Call the same customer service number and ask to remove the authorized user only. The main account stays open.

Canceling a Pending Application (Not Yet an Open Account)

There is an important difference between canceling a Citi credit card application and closing an open Citi account. If you applied for a card but changed your mind, and the card has not arrived yet or you have not activated it, the steps are different.

If Citi has not yet approved the application, call 1-800-763-9795, the Citi application status line, and ask them to cancel your pending application. If you catch it before final approval, you may avoid the hard inquiry showing up as a permanent negative mark. Once the hard pull has already hit your credit report, canceling the application will not remove it, though its impact on your score usually fades within a few months.

If the card has been approved but you have not activated it, you can still close the account. Just call the main number and say the card was approved but you no longer want it. The account will show as opened and closed on your credit report, which is a smaller footprint than a full year of activity.

If the card is already activated, even if you never used it, you must go through the full account closure process described earlier.

How Closing a Citi Card Affects Your Credit Score

The credit score impact is the number one reason people hesitate to cancel. The truth is, the effect is usually smaller than people fear, but it depends on two factors: credit utilization ratio and length of credit history.

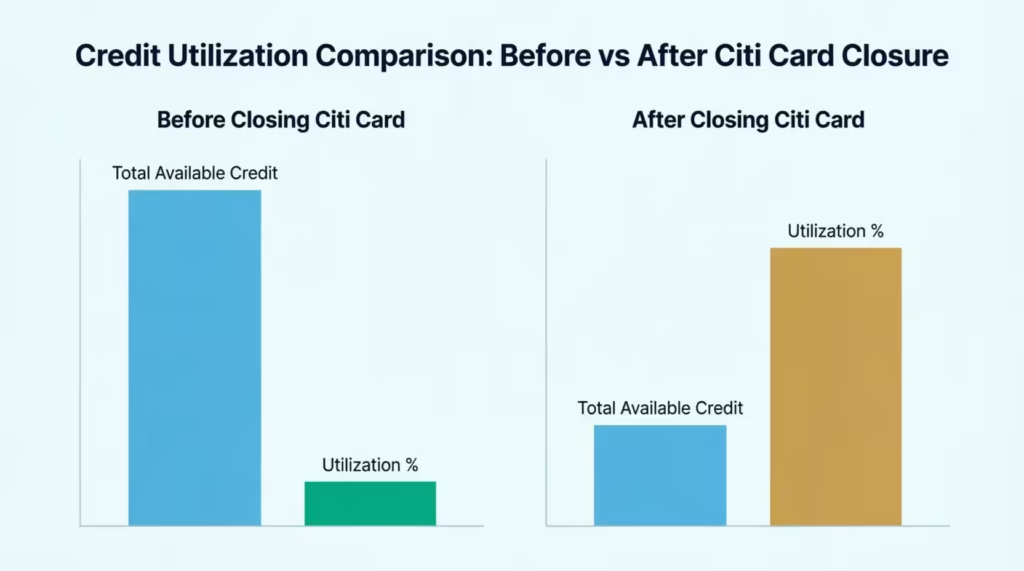

Credit utilization ratio is the percentage of your available credit that you are actually using. Lenders like to see this below 30 percent, and under 10 percent is even better. When you close a Citi card, that card’s credit limit disappears from your total available credit. If you still carry balances on other cards, your utilization ratio jumps up.

Here is a concrete example. Sarah, a 34-year-old marketing manager, has three credit cards:

- Citi Double Cash: $8,000 limit, $0 balance

- Chase Freedom: $5,000 limit, $1,500 balance

- Capital One: $4,000 limit, $500 balance

Her total credit limit is $17,000, and her total balance is $2,000. Her utilization is 2,000 divided by 17,000, which is about 12 percent. Now she closes the Citi card.

Her available credit drops to $9,000, but her balance stays at $2,000. Her new utilization jumps to about 22 percent. Her credit score could dip by 10 to 30 points until she pays down those balances or the ratio recovers.

Length of credit history matters too, but less than most people think. Closed accounts in good standing stay on your credit report for up to 10 years, and they keep counting toward your average account age during that time. So the real hit to your account age does not show up for a decade, and by then, your other accounts have aged too.

To soften the impact, do these three things before closing:

- Pay down balances on other cards so your utilization stays low even after the Citi limit is gone.

- Do not apply for new credit in the same 30-day window. Multiple changes at once make the dip look bigger.

- If the card has been open for many years, consider keeping it open with zero balance and canceling a newer card instead.

If you plan to apply for a mortgage, car loan, or new credit line in the next 6 to 12 months, wait to cancel. A small dip now could raise your interest rate on a much bigger loan later.

Confirming Your Account Is Actually Closed

Getting a verbal “yes, it’s closed” on the phone is not enough. Accounts sometimes stay technically open due to a pending charge, a system delay, or a simple error. You need to verify closure yourself.

Do these three checks:

- Log in to your Citi online account after 3 to 5 business days. The card should show as “Closed” in your account list. If it still shows “Active” after a week, call back and ask why.

- Request written confirmation. Ask the agent during the closure call to email or mail you a confirmation letter. Save it. This is your proof if the account ever reappears or if a billing dispute pops up.

- Check your credit report within 30 to 60 days. Pull a free report from AnnualCreditReport.com, the only federally authorized site under the Fair Credit Reporting Act. The Citi card should be marked as “Closed by consumer” or “Account closed at consumer’s request.” If it still shows open, or if it is marked “Closed by credit grantor,” dispute it with the credit bureau and Citi.

Watch your next billing cycle too. If Citi accidentally lets a recurring charge through, you may see a small balance appear on a card you thought was dead. Pay it and call Citi again to confirm closure.

📌 Did You Know: Even after your account is closed, Citi keeps your account data for at least seven years to comply with federal recordkeeping rules. That means you can still request past statements or a formal closure letter years later if you need it for a tax audit or loan application.

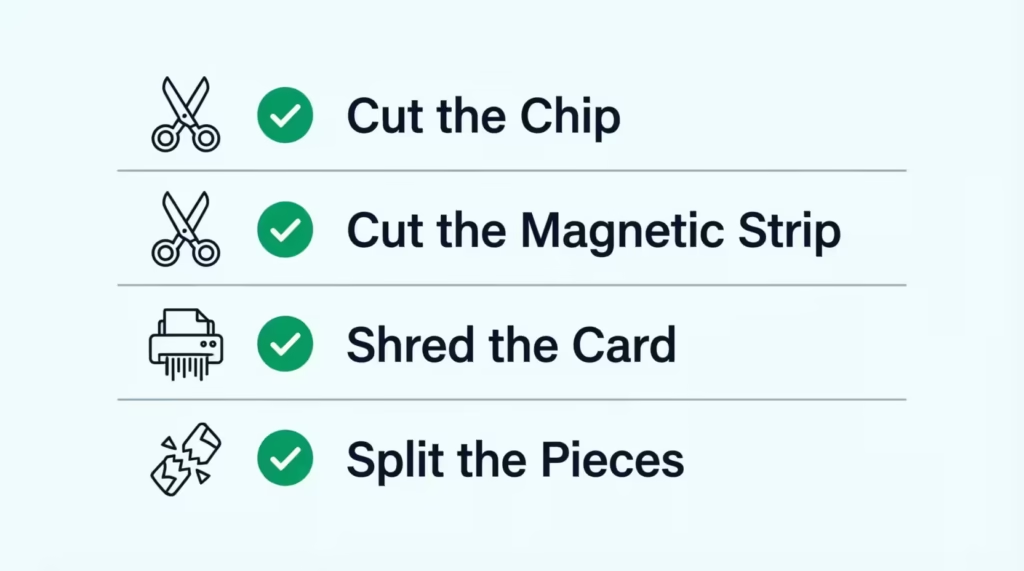

Disposing of the Physical Card

Once you have confirmation the account is closed, destroy the physical card. Do not just toss it in the trash. Credit cards have chips, magnetic strips, and printed numbers that can all be used for fraud.

The safest way to dispose of a Citi credit card:

- Cut through the chip. The EMV chip on the front is the main target for skimmers. Cut it into at least two pieces with scissors.

- Cut across the magnetic strip on the back. Two or three cuts across the strip make it unreadable.

- Shred the card if you have a cross-cut shredder. Most home shredders rated for credit cards do the job in seconds.

- Split the pieces between two trash bags. Put half in this week’s trash and half in next week’s. It sounds paranoid, but it removes any chance of someone piecing it back together.

If you have a metal Citi card, such as an older Citi Prestige, you cannot cut it with scissors. Mail it back to Citi in the return envelope they provide, or drop it off at a branch for secure disposal.

Citibank Customer Service Numbers by Card Type

Different Citi cards use different customer service lines. Calling the right one gets you a specialized agent who can process closure faster. All numbers below are current for U.S. cardholders as of 2026, based on the official Citi contact page.

| Card Type | Phone Number | Hours |

|---|---|---|

| General Citi credit cards | 1-800-950-5114 | 24/7 |

| Spanish customer service | 1-800-947-9100 | 24/7 |

| Costco Anywhere Visa by Citi | 1-855-378-6467 | 24/7 |

| Citi AAdvantage cards | 1-800-950-5114 | 24/7 |

| Citi Custom Cash, Double Cash, Diamond Preferred | 1-800-950-5114 | 24/7 |

| Application status or pending application | 1-800-763-9795 | 8 a.m. to 10 p.m. ET |

| TTY (hearing impaired) | 711 or other Relay Service | 24/7 |

| Citi Retail Services (store cards like Best Buy, Home Depot) | Number on card back | Varies |

If you have a store-branded Citi card, like Home Depot or Best Buy, the number on the back is usually a Citi Retail Services line. This number is different from your main Citi credit card number. Use the number on the card for the fastest routing.

For international travel, Citi accepts collect calls at 1-605-335-2222 for U.S. cardholders calling from abroad.

Frequently Asked Questions

How can I cancel my credit card online?

Log in to citi.com or the Citi Mobile App, go to Services or Help & Contact Us, and send a secure message requesting closure. Expect this to take one to three business days, and Citi may still call to verify your identity before processing it.

Does canceling a credit card hurt your credit?

It can cause a temporary dip, usually 5 to 20 points, mainly from a higher credit utilization ratio once that card’s limit disappears. The account still counts toward your credit history for up to 10 years, so the score recovers for most people within a few months.

What is the downside to canceling a credit card?

Your total available credit drops, which raises your utilization ratio if you carry balances elsewhere, for example, jumping from 12% to 22% after closing an $8,000 limit card. You also lose any ThankYou points not redeemed within 60 days and must move any auto-pay charges tied to the card.

Is it better to cancel a credit card or let it close for inactivity?

Canceling on your own terms is better because you control the timing, redeem your points first, and move auto-pay charges before the card stops working. Letting Citi close it for inactivity gives you no warning and can leave subscriptions failing without notice.

How much will my credit score drop if I cancel a card?

Most people see a drop of 5 to 20 points, mainly driven by utilization. In one example, closing an $8,000 limit card pushed a $2,000 balance from 12% to about 22% utilization, which can cost 10 to 30 points until balances are paid down.

Can I cancel a credit card without calling?

Yes, you can send a secure message through the Citi online account or app, or mail a signed letter to Citibank Customer Service, P.O. Box 6500, Sioux Falls, SD 57117. Both are slower than phone, taking one to three days online or two to four weeks by mail.

How long does it take to close a Citi credit card?

Closure happens the same day when you call 1-800-950-5114, with written confirmation arriving by mail in 7 to 14 business days. Your credit report may take 30 to 60 days to show the change since Citi reports to bureaus monthly.

What is the 7-year rule on credit cards?

The article doesn’t address a 7-year rule, but it does note that Citi keeps account data for at least seven years for federal recordkeeping. This means you can still request past statements or a closure letter years later for a tax audit or loan application.

Can Citi refuse to close my account?

Citi cannot legally refuse to close your account once you’ve paid off the balance and made a clear request. If you still owe money, they’ll freeze new charges but won’t officially close it until the balance hits zero, and you can ask for a supervisor or file a complaint with the CFPB at consumerfinance.gov if an agent stalls.

Wrapping Up

Closing a Citi credit card the right way comes down to sequence and confirmation. Redeem your ThankYou points before the 60-day clock starts, pay down what you owe, move your auto-pays, then call 1-800-950-5114 and ask for closure in writing. Watch your credit report over the next two months to make sure the account is marked “Closed by consumer.”

Based on the account closure process details above, the most effective approach is phone closure with written follow-up, because it gives you same-day action and a paper trail.

If you know someone stuck with a Citi card they no longer need, share this guide. It could save them from losing thousands of points or taking an avoidable credit hit.