If you’re behind on credit card bills, the fear of losing your home can feel overwhelming. Maybe a collector called with a threat, or maybe you just got served with court papers, and now you’re wondering if the answer to ” Can credit card debt take your house is really “yes.” That worry is normal, and it deserves a straight answer.

Here’s the short truth: credit card companies cannot take your home just because you missed payments, but ignoring the debt can put your equity at risk over time.

We’ll walk you through the exact legal steps, your state protections, and the smart moves to make this week.

Key Takeaways

This guide explains whether credit card debt can lead to losing a home, covering the legal steps from missed payments to judgment liens, homestead exemption protections by state, and what to do if you’ve already been sued.

Core Facts:

- Credit card debt is unsecured, so a creditor must sue you, win a judgment, and record a lien before it has any legal claim on your home.

- After about 180 days of missed payments, the account is charged off, then sold or sent to in-house collections before any lawsuit begins.

- Once served, you typically have 20 to 30 days to file a written answer before the creditor can seek a default judgment.

- A judgment lien clouds your property title and must be paid, settled, or released before you can sell or refinance the home.

- Homestead exemption laws vary by state, with Texas, Florida, Iowa, Kansas, Oklahoma, and South Dakota offering unlimited or near-unlimited home equity protection.

- A forced sale of a home over credit card debt is legally possible but rare, since homestead exemptions and sale costs often leave nothing for the creditor.

Best for:

- Homeowners who have received a debt collection notice or lawsuit and want to understand their actual risk level.

- People trying to decide whether to respond to a credit card lawsuit or negotiate a settlement before a judgment is entered.

- Anyone managing an estate or surviving spouse situation who wants to know whether credit card debt can affect an inherited or shared home.

Can Credit Card Debt Take Your House? The Direct Answer

The short answer is NO, not directly and not right away. A credit card company cannot show up, change your locks, or grab your house because you missed a few payments. Credit cards are unsecured debt, which means no piece of property was pledged as collateral when you signed up. That’s very different from a mortgage or car loan.

For a card issuer to reach your home at all, it must first sue you in civil court, win, and get a judgment lien recorded against your property. Even then, a forced sale of a primary residence is uncommon in most states because of homestead laws and the cost of the process.

In real life, most credit card lawsuits lead to wage garnishment, bank levies, or a lien on your property. This lien stays until you sell or refinance. It rarely results in someone taking your house.

So the true answer is layered: your home is not in danger the moment you fall behind, but it can become part of the fight if a judgment creditor wins in court and you have non-exempt equity in your state. The rest of this guide shows you exactly how that path works, and where it usually stops.

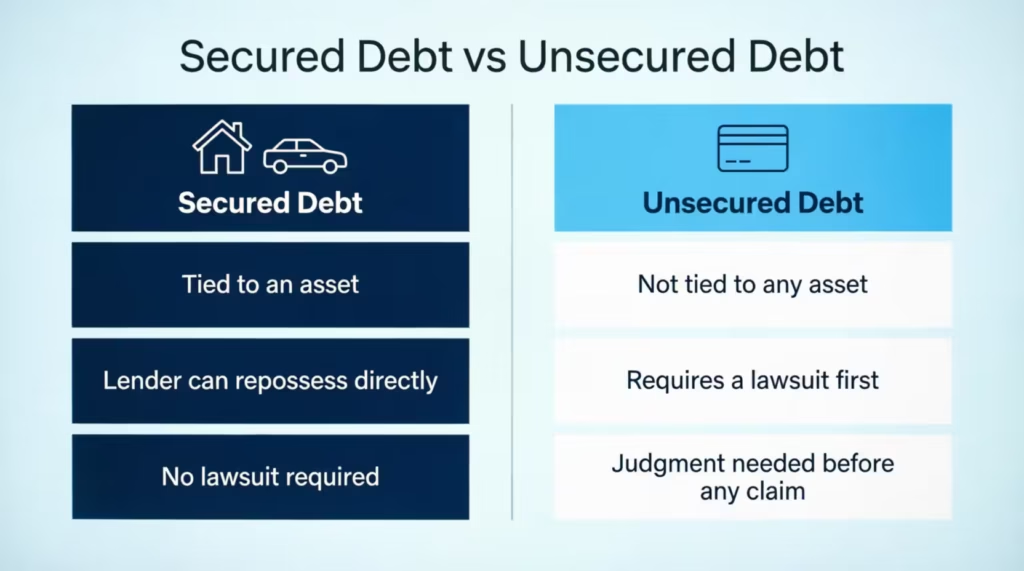

Secured vs. Unsecured Debt (Why the Answer Isn’t Simple)

The reason this question causes so much panic is that many people mix up two very different kinds of debt.

Secured debt is tied to a specific asset. A mortgage is secured by your house. An auto loan is secured by your car. If you stop paying, the lender has a legal right, written into the loan contract, to take that exact asset back. No lawsuit is needed to start foreclosure or repossession in most cases, just the process your state requires.

Credit cards, medical bills, and personal loans are unsecured. Nothing was pledged, so the card issuer has no direct claim on any item you own. To reach your assets at all, the issuer has to go to court and prove you owe the money.

Only after a judgment can the creditor try to attach that debt to your property. That extra legal layer is what protects most homeowners from a fast, quiet loss of their home over card balances.

Can Credit Card Debt Collectors Take Your House?

Third-party collectors sound scarier than the original bank, but they don’t have more power. When a card company writes off your account, it often sells the debt to a collection agency for pennies on the dollar. That agency now owns the right to collect, but not the right to seize anything you own.

A debt collector must follow the same legal path as the original issuer. It has to sue you, serve you properly, win a judgment, and then record that judgment as a lien if it wants any claim on your home. It cannot skip court. It cannot put a lien on your house just by mailing threatening letters or leaving voicemails.

Federal law gives you real protection here. The Fair Debt Collection Practices Act (FDCPA) bans collectors from lying about what they can do, threatening actions they don’t intend to take, or claiming they can take your home when they legally cannot.

The Consumer Financial Protection Bureau explains that collectors also can’t call at odd hours, contact you at work after you’ve told them to stop, or use abusive language.

You also have the right to debt validation. You can send a written request within 30 days of the collector’s first contact. This request should ask them to prove the debt is yours and that they have the legal right to collect it.

If they can’t, they must stop collection activity. Many buyers of old card debt lose paperwork over the years, so this simple letter often shuts the case down before it ever reaches a courtroom.

💡 Pro Tip: Always send a debt validation request by certified mail with a return receipt. That paper trail proves you asked in time, which becomes powerful evidence if the collector later sues you without proper documentation.

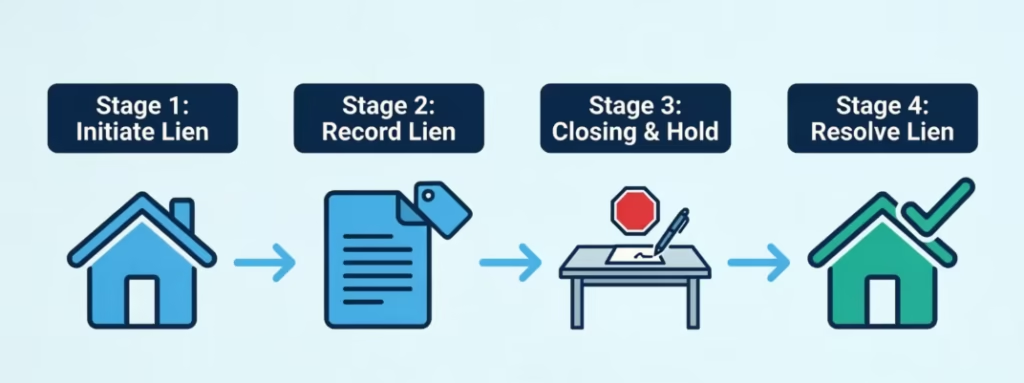

The Legal Process a Creditor Must Follow Before Any Lien

The path from a missed payment to a lien on your home is long, and each step gives you a chance to respond. Understanding this timeline removes a lot of the fear because it shows how many exits exist along the way.

Step 1: Default and charge-off. After you miss payments for about 180 days, the card issuer usually charges off the account. This is an internal accounting move, not a legal one. Your account is closed, and the balance is reported as a loss. Late fees stop building at this point, but interest often keeps growing.

Step 2: Sale or in-house collection. The issuer either turns your file over to its own collection team or sells the debt to a buyer. You’ll start getting letters and calls from a new name.

Step 3: The lawsuit. If the balance is worth chasing, the creditor files a complaint in civil court. You must be served with a civil court summons in a way your state allows, usually in person or by certified mail. This is the single most important moment. From the day you’re served, you typically have 20 to 30 days to file a written answer with the court.

Step 4: Your response, or silence. If you file an answer, the case moves toward mediation, settlement talks, or trial. You can raise defenses, such as the statute of limitations or lack of proof. If you ignore the summons, the creditor will ask the judge for a default judgment. This is usually granted, so you lose without getting to share your side.

Step 5: The judgment. Once the court enters a judgment, the creditor becomes a judgment creditor with new collection tools. It can request wage garnishment, freeze bank accounts, or turn its focus to your home.

Step 6: Recording the lien. To attach the judgment to your house, the creditor files an abstract of judgment with the county recorder or clerk where you own property. That filing places the lien on the public record and clouds your title until it’s paid, settled, or removed.

⚠️ Mistake to Avoid: Skipping the court date because you “know” you owe the money is the single fastest way to lose. Showing up forces the creditor to prove the debt, which they often cannot do with old, resold accounts.

What Is a Judgment Lien, Exactly?

A judgment lien is a legal claim recorded against your real property because a court decided you owe money. It does not transfer ownership.

The creditor does not become a co-owner of your house, cannot move in, and cannot rent it out. The lien simply attaches to the property, like a note stapled to the title, that says a debt must be paid before the property can change hands cleanly.

The practical effect shows up when you sell or refinance. Title companies check public records before any closing. If a lien appears, the sale cannot go through until the lien is paid off, negotiated down, or released by the creditor.

In most states, the lien also earns interest at a set rate, so a balance can grow while it sits there. Judgment liens typically last 5 to 20 years depending on the state and can often be renewed, so waiting them out is rarely a real plan.

Judgment Lien vs. Foreclosure: Can Credit Card Debt Foreclose on a House?

This is where most homeowners get confused, and the confusion causes real panic. Foreclosure and a judgment lien are not the same thing, and credit card debt rarely leads to foreclosure.

Foreclosure is the specific legal process a secured lender uses to take back the collateral for a loan. A mortgage lender can foreclose because you gave the lender a lien on the house as part of the mortgage. If you stop paying, the lender uses that pre-agreed right to sell the home and recover its money. No new lawsuit about ownership is needed.

A card issuer has no such pre-agreed right. Even after winning a lawsuit, it can’t just start a foreclosure. What it holds is a judgment lien. To turn that lien into cash by selling your home, the creditor would need to file a separate court action asking a judge to order a forced sale of your home. Judges rarely grant this for unsecured debt. Two big reasons stand in the way.

First, homestead exemption laws protect a chunk of your home equity, sometimes all of it. Second, the sale costs, real estate fees, senior mortgage payoff, and the exempt amount often leave nothing for the judgment creditor. If there’s no money in it, no lawyer will spend months pushing for a sale.

The result: a lien can sit on your title for years, but it doesn’t push you out of your home, doesn’t cancel your mortgage, and doesn’t lead to eviction on its own. Losing your house to card debt is legally possible but practically rare.

Homestead Exemptions: The Main Reason Your House Is Usually Safe

The homestead exemption is the legal shield that keeps most homeowners in their homes even when they lose a debt lawsuit. It’s a state law that sets aside a portion of your home’s equity and puts it out of reach of most judgment creditors.

Here’s the mechanism in plain terms. Say your house is worth $300,000 and you owe $220,000 on the mortgage. Your equity is $80,000. If your state’s homestead exemption is $100,000, that entire $80,000 is protected.

A judgment creditor cannot force a sale because there’s nothing left to collect after paying the mortgage and honoring the exemption. Even if the exemption were $50,000, a forced sale would only net $30,000 for the creditor, minus court and sale costs, so it usually isn’t worth trying.

The exemption is not a free pass for every debt. It does not block your mortgage lender from foreclosing if you stop paying the mortgage, because you signed away that protection when you took the loan.

It does not stop the IRS from collecting federal tax debt. It usually doesn’t block child support or spousal support liens. Mechanic’s liens for work done on the property may also break through. But for standard credit card judgments, homestead protection is powerful and, in some states, absolute.

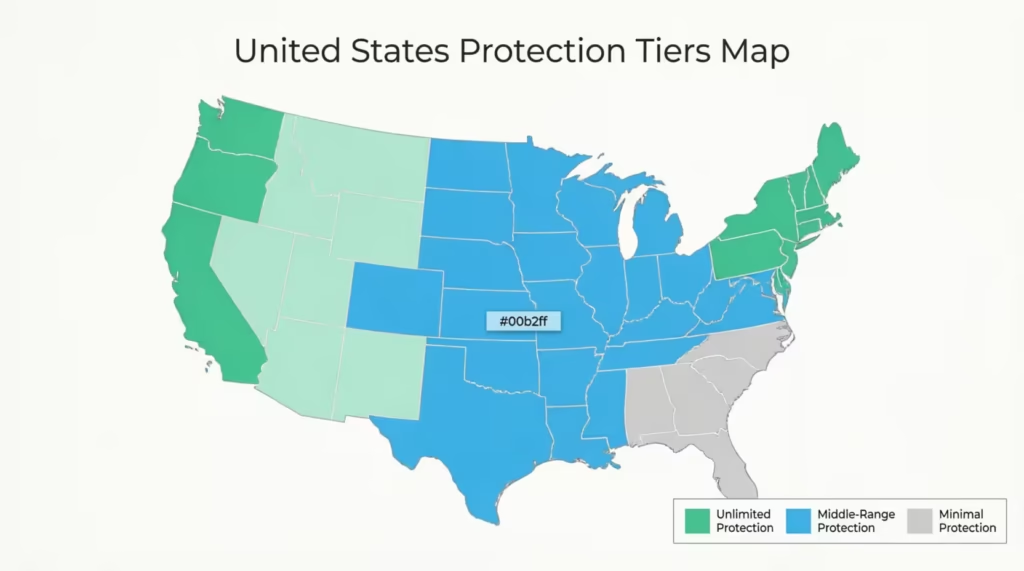

How Much Protection Depends Heavily on Your State

Homestead exemption amounts differ greatly across the country. This means the same card debt can lead to different results based on your location.

Unlimited or near-unlimited protection. A small group of states protects the full value of a primary residence with almost no dollar cap. Texas, Florida, Iowa, Kansas, Oklahoma, and South Dakota fall in this group. In Texas, up to 10 acres of an urban homestead and up to 200 acres of a rural homestead are shielded from most creditor claims, with no cap on the home’s value. If you live in one of these states, a credit card judgment lien rarely leads to a forced sale.

Middle-range caps. Many states protect a set dollar amount of equity, often between $25,000 and $600,000. California, Massachusetts, New York, and Nevada sit at the higher end. States like Ohio and Illinois offer more modest amounts.

Near-zero protection. A few states, including New Jersey and Pennsylvania, offer very small or no state homestead exemption. Homeowners there rely more on federal bankruptcy exemptions if debt trouble grows.

Marital protection. In some states, if the home is owned by both spouses as “tenants by the entirety,” a creditor of only one spouse cannot force a sale at all. Check with a local consumer attorney if this applies to you.

📌 Did You Know: A handful of states require you to formally file a homestead declaration with the county to lock in the protection. In most states, the exemption happens automatically. But if you need to file and skip the form, your home could be at risk, even if the law would normally protect it.

Can Credit Card Debt Affect Your Home if You Try to Sell or Refinance?

Yes, and this is the moment most homeowners actually feel the weight of a judgment lien. Even if no one ever tries to force a sale, an unresolved lien can freeze a deal you badly want to close.

When you sell, the buyer’s title company runs a title search. Any recorded lien shows up. Because clean title is required to transfer ownership, the lien must be handled before closing. In practice, three things can happen.

You pay the full amount from your sale proceeds at closing. You negotiate a lower payoff with the creditor, sometimes 30 to 60 cents on the dollar, in exchange for a lien release. Or the deal falls apart if there isn’t enough equity to cover the lien plus the mortgage and closing costs.

Refinancing is similar. A refinance lender needs to be sure it will hold the first-priority lien on the property. If a judgment lien is already recorded, the new lender will require it to be paid off or released as a condition of closing. That can shrink or wipe out the cash you were hoping to pull from the home. Home equity lines and home equity loans face the same rule.

There’s a quieter effect too. Judgment liens appear on your credit report and stay for years. Even if you’re not selling, that record can push mortgage rates higher, make insurance more expensive, and complicate any application for new credit.

Can a Lien Force the Sale of Your House?

Technically yes, practically rare. A creditor with a recorded judgment lien can ask the court to order a sale of the property to satisfy the debt. Judges have discretion and generally won’t approve one unless a few conditions line up.

There must be significant non-exempt equity in the home. If the homestead exemption and mortgage balance cover most of the home’s value, there’s not much left for the creditor.

So, the court has no reason to disrupt a family’s housing for a small return. The creditor must also cover the cost of the forced sale process, which is expensive. And the debt has to be large enough to justify all of it.

In most states, this path is rarely used for credit card debt. Creditors prefer wage garnishment and bank levies because they’re cheaper and faster. The lien usually just waits on your title until you sell, refinance, or resolve it on your own terms.

Can Credit Card Debt Take Your House After Death? What Happens to a Parent’s or Spouse’s Home

Losing a loved one is hard enough without a debt collector calling about their old credit cards. The good news is that credit card debt does not automatically transfer to family members. You don’t get your parent’s Visa balance just by inheriting their house. Also, creditors usually can’t make you pay from your own money.

Here’s how it actually works. When someone dies, their estate is opened, usually through probate. The executor collects the person’s assets, pays valid debts in a set order, and then distributes what’s left to the heirs. Credit card debt sits near the bottom of that priority list, below funeral costs, taxes, and secured debt like a mortgage.

If the estate has enough cash and non-real-estate assets to pay the card debt, the house is safe and passes to heirs clean. If the estate is short, the executor may have to sell assets, including real estate, to satisfy creditors. That’s not the credit card company “taking” the house; it’s the estate paying its bills before heirs receive anything.

Several exceptions can pull a survivor into the debt directly. If you were a co-signer or joint account holder on the credit card, the debt is yours too. If you were only an authorized user, you are not legally responsible for the balance.

In one of the nine community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), debts taken on during the marriage are often treated as shared, which can make a surviving spouse responsible for card balances even without co-signing. The rules vary by state, so a local probate attorney is worth the small fee.

The executor should never pay a card debt out of personal funds and should ask every collector to send written proof of the claim. Creditors have a limited window, often 3 to 6 months after probate opens, to file claims against the estate. Late claims are usually barred.

What Happens If You Ignore a Credit Card Debt Lawsuit

Ignoring the lawsuit is the single most damaging move a homeowner can make, and it’s also the most common one. Fear and confusion push people to hope the papers will go away. They don’t.

When you don’t respond to a properly served summons within the deadline, usually 20 to 30 days, the creditor files for a default judgment. The judge grants it almost automatically because your silence is treated as agreement that the debt is valid and the amount is correct. You lose the case without a hearing.

That default judgment gives the creditor the full toolkit. It can garnish your wages, often up to 25% of your take-home pay under federal rules and less in some states. It can freeze your bank accounts.

It can record a judgment lien on your home. And it locks in the debt amount, plus court costs, plus interest, sometimes at 8% to 12% per year depending on the state, for the entire life of the judgment.

You also lose the chance to raise defenses that could have wiped the case out. Old debts often violate the statute of limitations, which is 3 to 6 years for card debt in most states. Buyers of resold debt frequently lack the paperwork to prove they own the account.

Some balances include improper fees or charges you didn’t make. None of that matters if you never file an answer, because the court won’t consider it after the deadline.

If a default judgment has already been entered, all is not lost. Many states let you file a motion to vacate the default judgment if you act quickly and show a valid reason, such as improper service or a strong defense. A consumer law attorney or legal aid office can move fast on this.

What to Do If You’ve Been Sued or Already Have a Lien

Now for the action layer. If a card debt has reached this point, you have real options, and the sooner you use them, the more of your home equity you keep.

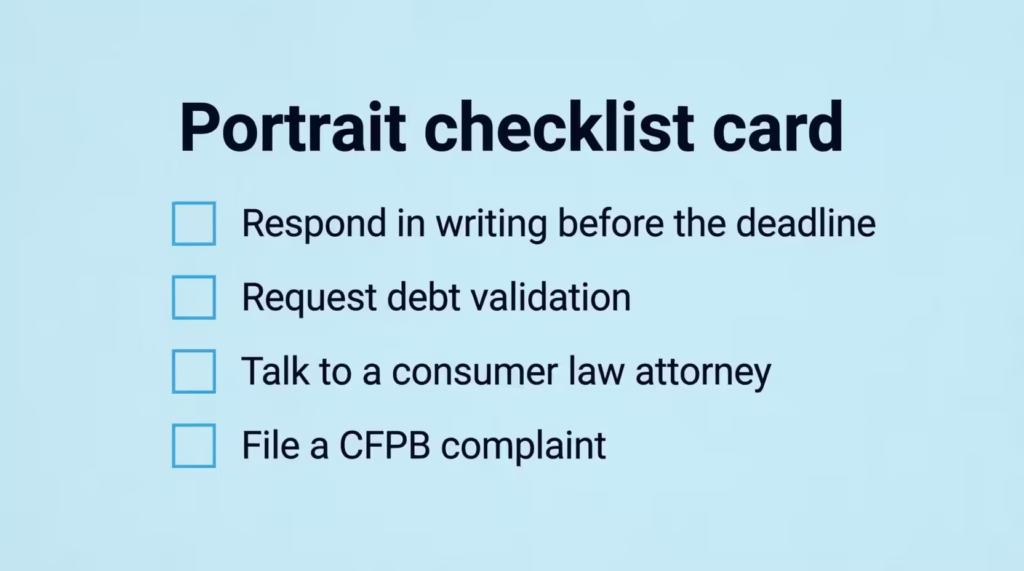

Respond to the lawsuit in writing before the deadline. Even a simple, one-page answer denying the claim buys you time, forces the creditor to prove its case, and often triggers settlement talks. Most courts have free answer forms on their websites. Never miss this step.

Send a debt validation request. If a collector is chasing you and you haven’t been sued yet, mail a validation letter within 30 days of first contact. Ask for the original creditor’s name, the account number, the full balance breakdown, and proof that the current collector owns the debt. If they can’t produce it, they must stop collecting.

Talk to a consumer law attorney. Many offer free 30-minute consultations, and some take cases on contingency for FDCPA violations, meaning you pay nothing unless they win. Legal aid societies help lower-income homeowners for free. The National Association of Consumer Advocates keeps a searchable directory of attorneys who focus on this area.

File a complaint with the CFPB. The Consumer Financial Protection Bureau forwards complaints directly to the company, which must respond within 15 days. This often speeds up resolution, especially when the collector has broken FDCPA rules.

Pick a removal path if a lien is already recorded. Three main options exist:

- Pay the full lien amount from savings or from sale proceeds.

- Settle for less. Judgment creditors often accept 30 to 60 cents on the dollar in a lump sum because collecting the full amount is uncertain. Always get the lien release in writing before you pay.

- File for bankruptcy. Chapter 7 can wipe out unsecured card debt and, in many states, allow you to strip judgment liens that impair your homestead exemption. Chapter 13 creates a 3-to-5-year repayment plan that stops collection actions and can also remove qualifying liens. Bankruptcy is a serious step, but for homeowners with multiple judgments and shrinking equity, it can protect the house.

How to Prevent a Lien Before It Happens

The best defense is early action, before any lawsuit is filed.

Answer the phone or open the letters. Silence is what turns a $4,000 balance into a lawsuit. Even one honest conversation with the creditor can slow things down.

Ask about hardship programs. Most major card issuers, like Chase, Citi, Bank of America, Capital One, and Discover, have hardship plans. These plans can lower your interest rate, waive fees, or allow smaller payments for 6 to 12 months. You must ask, because they rarely offer these plans upfront.

Negotiate a settlement before a lawsuit. Once a debt is 90 to 180 days late, many issuers will settle for 40 to 60% of the balance to avoid legal costs. Get any agreement in writing, and confirm how the settlement will be reported to the credit bureaus.

Use a nonprofit credit counselor. Agencies certified by the National Foundation for Credit Counseling can set up a debt management plan, which consolidates card payments into one lower monthly amount, often with reduced interest.

File a homestead declaration if your state requires it. In states like Massachusetts and California, filing a simple declaration with the county recorder locks in the maximum homestead protection. The fee is small, usually under $50, and the paperwork takes minutes.

Frequently Asked Questions (FAQs)

Can a credit card company really take my house?

Not directly. A credit card issuer must sue you, win a judgment, and record a lien before it has any claim on your home. Even then, a forced sale is rare because of homestead exemptions and the cost of the court process. Most people never lose their home to card debt.

What is a judgment lien and how does it work?

A judgment lien is a legal claim recorded against your property after a court rules you owe money. It doesn’t transfer ownership, but it clouds your title. You must pay, settle, or release the lien before selling or refinancing. Many liens also grow with interest until resolved.

Does my state protect my home from credit card debt?

Every state offers some homestead exemption, but the amounts differ hugely. Texas, Florida, Iowa, and Kansas protect unlimited equity. Others protect a set dollar amount. A few offer almost nothing. Check your state’s current exemption or ask a local consumer attorney to confirm.

What happens if I ignore a debt collection lawsuit?

The creditor gets a default judgment, and you lose the case without a hearing. That judgment lets them garnish wages, freeze bank accounts, and record a lien on your home. You also lose the chance to raise defenses that might have wiped the debt out.

Do I inherit my parents’ credit card debt if I inherit their house?

No. Credit card debt belongs to the estate, not the heirs. The executor pays valid debts before distributing assets. You only owe if you co-signed the card, were a joint account holder, or live in a community property state and are the surviving spouse.

Can a lien force me to sell my house?

Rarely. A creditor can request a court to order a forced sale. However, judges often deny these requests. They do this when homestead protections and mortgage balances leave little equity for the creditor. Wage garnishment and bank levies are far more common than forced home sales.

How do I stop a lien from being placed on my home?

Respond to the lawsuit on time, request debt validation, negotiate a settlement, or file for bankruptcy if debts have piled up. If your state requires a homestead declaration, file it now, before any judgment is entered. Speed matters more than any single tactic.

Wrapping Up

Credit card trouble is stressful, but the path from a missed payment to actually losing a home is long and full of exits. Unsecured card debt requires a lawsuit, a judgment, and often a forced-sale motion before it touches your house, and homestead exemptions block most of those endings.

Based on how these cases usually play out, the most effective move is responding to any lawsuit in writing before the deadline and asking for debt validation right away. That single action preserves nearly every option you have.

If you know a friend or family member juggling credit card debt and homeowner worries, share this guide with them. It could save them from a default judgment that would haunt their equity for years.