I remember opening my statement one month and just staring at the minimum payment line. It looked way bigger than last month, but I hadn’t gone on a shopping spree. If you’re feeling that same mix of confusion and worry, you’re not alone. A rising credit card minimum payment almost always has a specific, traceable cause hiding inside your statement.

The short answer: your minimum went up because your balance grew, your interest charges climbed, a fee was added, or a one-time event (like a cash advance or expired promo APR) changed the math.

Below, we’ll walk through every likely cause, show you how the numbers actually work, and help you decide what to do next.

Key Takeaways

This guide explains why a credit card minimum payment suddenly increases, covering balance growth, interest rate changes, added fees, past-due rollovers, and one-time events like cash advances, plus how to lower it and whether it affects your credit score.

Core Facts:

- Minimum payments are calculated using one of three formulas: a percentage of balance (typically 1% to 3%), a flat fee floor (often $25 or $35), or interest plus 1% of the principal.

- A balance increase directly raises a percentage-based minimum; for example, a balance rising from $3,000 to $4,500 on a 2% formula raises the minimum from $60 to $90.

- Late fees can run up to $41 for repeat offenses, and a penalty APR of 29.99% or higher can apply for at least six months after a late payment.

- The size of a minimum payment itself is not reported to credit bureaus, but missing it triggers 30-day delinquency reporting that can drop a score by 60 to 100 points.

- On a $5,000 balance at 22% APR, minimum-only payments can take over 20 years to pay off according to CFPB payoff estimates.

- Consequences after a missed payment follow a timeline: a late fee posts on day 1, delinquency reports to bureaus on day 30, a penalty APR may apply by day 60, and charge-off to collections can occur between day 90 and 180.

Best for:

- Cardholders who noticed their minimum payment jump and want to identify the exact cause using their own statement.

- People deciding whether to pay only the minimum or more, based on how it affects long-term interest costs.

- Anyone who missed a payment or is at risk of missing one and wants to understand the exact consequence timeline before it escalates.

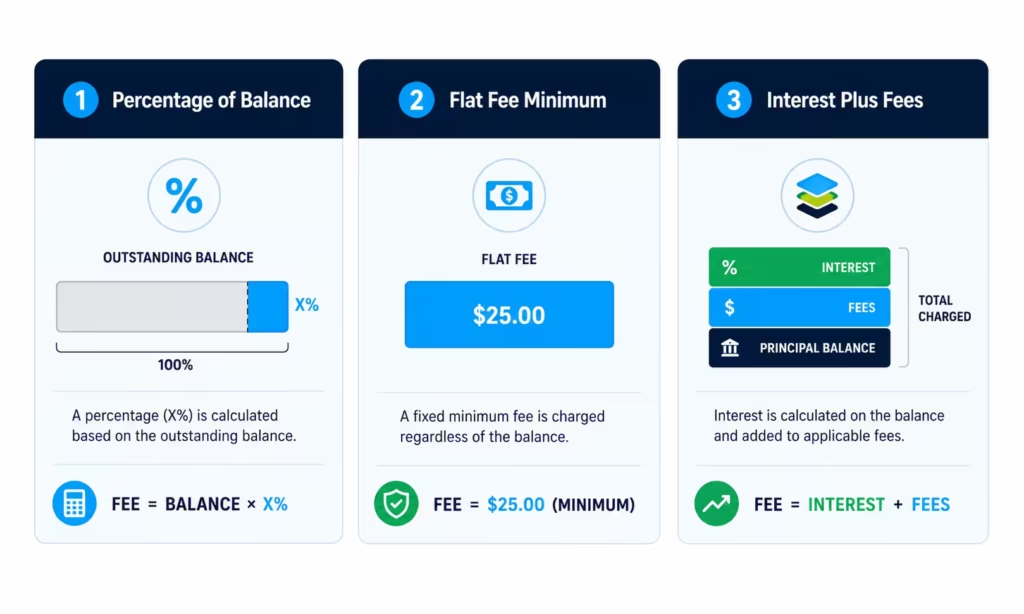

How Your Minimum Payment Is Actually Calculated

Before you can figure out why the number jumped, you need to know how the number is built in the first place. Card issuers don’t all use the same formula. Most use one of three approaches, and the one your card uses is written in your cardmember agreement.

The first approach is the percentage of balance method. The issuer takes a small slice of what you owe, usually between 1% and 3%, and that’s your minimum. If your balance rises, your smallest percent payment rises with it, dollar for dollar.

The second approach is the flat fee minimum. The issuer sets a floor, often $25 or $35. You pay that amount as long as your balance stays above it. If your balance drops below the floor, you just pay the full balance.

The third approach is the interest plus fees method. The issuer charges all the finance charges for the cycle, then adds 1% of the principal on top. This method reacts strongly to interest rate changes, since interest is baked right into the payment.

Why the Formula Differs by Issuer

Each bank picks its own formula based on risk rules and federal guidance. Under Credit CARD Act rules, the minimum must be big enough to pay off some principal each month, not just interest. That’s why you rarely see a pure “interest only” minimum today.

To find your formula, open your card’s statement and flip to the section titled “How We Calculate Your Minimum Payment,” or check the pricing terms in your online account. Chase, Capital One, Citi, and Discover all publish these terms clearly. Reading this one page saves hours of guessing.

Your Balance Went Up (The Most Common Reason)

If your issuer uses a percentage-based formula, this is the number one reason your minimum grew. Even a small statement balance change can push the number up more than you’d expect.

Say your card uses a 2% minimum. Last month your balance was $3,000, so your minimum was $60. This month, a few small purchases plus a car repair pushed your balance to $4,500. Your new minimum is now $90. That’s a 50% jump in the minimum from a 50% jump in the balance.

Here’s the tricky part. The balance the issuer uses isn’t just what you spent this month. It’s the closing balance at the end of the billing cycle, which includes any old balance you carried over, plus new purchases, plus interest, plus fees. So even a “quiet” month can still show a bigger balance if you didn’t fully pay off the last one.

Check your statement for the “Previous Balance” and “New Balance” lines side by side. If the new balance climbed even a little, and your card uses the percentage of balance method, your minimum will climb right along with it.

Interest Charges Are Quietly Inflating Your Minimum

Interest doesn’t just cost you money. It grows the very balance your minimum is calculated from. That means high interest can push your minimum higher every single month, even without new spending.

Your interest is figured using your APR and your average daily balance. The card adds up your balance for each day of the cycle, divides by the number of days, then applies the daily rate. If you carried $4,000 for most of the month at a 24% APR, that’s roughly $80 in interest added to your balance in one cycle.

Once that $80 gets added, next month’s minimum is calculated on the bigger number. This is compounding interest in action. Small charges snowball fast.

💡 Pro Tip: If your minimum climbed but your spending didn’t, pull up your APR for the last three statements. A rate change of even 2% can add real dollars to your balance and quietly bump your minimum higher.

Two events cause a sudden APR change. The first is introductory APR expiration. Many cards offer 0% for 12 to 21 months. When that ends, the rate can jump to 20% or more overnight, and interest starts stacking on the balance. The second is a variable interest rate shift. Most credit card APRs move with the prime rate. When the Federal Reserve raises rates, your APR usually follows within a cycle or two.

Confirm the rate on your latest statement matches what you expect. If it doesn’t, that alone can explain the whole increase.

Fees and Late Payments Added to the Balance

Fees don’t just sting once. They join your balance and stay there until paid, which means they keep influencing your minimum for months. This is a common reason people feel their credit card minimum payment got worse “for no reason.”

The most common trigger is a late payment fee. Under CFPB rules, first-time late fees are typically capped, but repeat late fees can be up to $41. That fee posts to your account, joins your balance, and gets pulled into next month’s minimum calculation.

An over-limit fee works the same way. If you opted into over-limit coverage and went past your credit line, the issuer can charge a fee, which then rides on your balance.

The most painful trigger is the past-due amount rollover. If you missed last month’s minimum, that unpaid amount gets tacked onto this month’s minimum, often as a separate line. So this month you’re being asked to pay two minimums at once, plus a late fee, plus interest on all of it.

There’s also the penalty APR. If you paid late, some issuers raise your APR to 29.99% or higher for at least six months. That higher rate means more interest, which means a bigger balance, which means a bigger minimum.

⚠️ Mistake to Avoid: Paying just the “current” minimum when a past-due amount is also showing. If you don’t pay both, the past-due keeps aging, and once it hits 30 days, it can be reported to the credit bureaus.

A One-Time Account Event May Be the Real Cause

If nothing above matches your situation, a specific one-time event probably changed the math. These are the sneaky ones because your spending really didn’t change, but your account did.

A cash advance fee is the first thing to check. Cash advances often carry a 3%-5% upfront fee, no grace period, and a higher APR (often 25%-29%). All three factors hit your minimum together. Even a small ATM withdrawal can noticeably lift the minimum for months.

An introductory APR expiration is the second big one. If your 0% offer ended between last statement and this one, any balance you were carrying is now generating interest for the first time. That interest gets added to your balance, and the minimum grows.

A variable interest rate shift is the third. If your APR is tied to the prime rate and the Fed hiked rates, your APR moved up. Interest charges rose, balance rose, minimum rose.

Issuer-driven credit limit reductions can also matter. If your issuer cut your credit limit and part of your balance now sits above the new limit, some cards require you to pay the over-limit portion as part of your minimum until you’re back under the limit.

Match Your Situation to the Exact Cause

Use this quick diagnostic to zero in on why your minimum payment increased suddenly. Match the symptom on the left to the most likely cause on the right, then head to that section for the fix.

| What You’re Seeing | Most Likely Cause |

|---|---|

| Bigger balance than last month | Percentage-based minimum reacting to a higher balance |

| Same balance, higher minimum | Interest rate went up or intro APR ended |

| New fee showing on statement | Late fee, over-limit fee, or cash advance fee added |

| Two minimums stacked on one bill | Past-due rollover from a missed payment |

| Cash withdrawal recently taken | Cash advance interest and fees |

| Nothing obvious changed | Variable APR shift tied to prime rate |

If two symptoms match, both causes are probably in play. That’s very common when a missed payment triggers both a late fee and a penalty APR at the same time.

Where Your Minimum Payment Money Actually Goes

Here’s the part most people don’t see. When you pay only the minimum, most of that money isn’t actually chipping away at your debt. It’s paying interest.

Say you owe $5,000 at 22% APR, and your minimum is $110 (about 2% of the balance plus interest). The interest charge that month, based on your average daily balance, is roughly $92. That means only $18 of your $110 payment goes to principal. Your $5,000 debt only drops to $4,982.

Next month, the balance is barely lower, so the interest is still around $91. Again, only about $19 goes to principal. This is compounding interest working against you.

The Minimum Payment Trap

This slow grind has a name: the credit card minimum payment trap. On a $5,000 balance at 22% APR with minimum-only payments, the CFPB’s payoff estimates show it can take over 20 years to clear the debt, and you’d pay several thousand dollars in interest along the way.

The trap gets worse, not better, as your balance drops. Once your balance is small, the percentage-based minimum drops with it, which stretches your payoff timeline even longer. Paying anything extra above the minimum, even $25 or $50, breaks the cycle fast.

Does a Higher Minimum Payment Hurt Your Credit Score?

This is the fear that keeps people awake at night. The good news: the size of your minimum payment, by itself, isn’t reported to the credit bureaus and doesn’t directly hurt your score.

Card issuers don’t send “minimum payment amount” to Experian, Equifax, or TransUnion. They send four main things: your balance, your credit limit, your payment status (on time or late), and your account age.

What the credit bureaus care about is whether you paid at least the minimum on time. If you did, your credit bureau reporting stays clean. Payment history is roughly 35% of your FICO score, so on-time payments protect the biggest part of your score.

Two indirect effects still matter. First, if your balance is high enough to push a big minimum, your credit utilization ratio is probably high too. FICO tracks the FICO utilization factor, and utilization above 30% starts to drag your score.

Second, if you can’t pay the new minimum and miss it, delinquency reporting kicks in at 30 days past due. That single 30-day late mark can drop a good score by 60 to 100 points.

📌 Did You Know: The specific minimum payment number never appears on your credit report. Only the balance, the limit, and whether you paid on time show up.

What Happens If You Can’t Afford the New Minimum

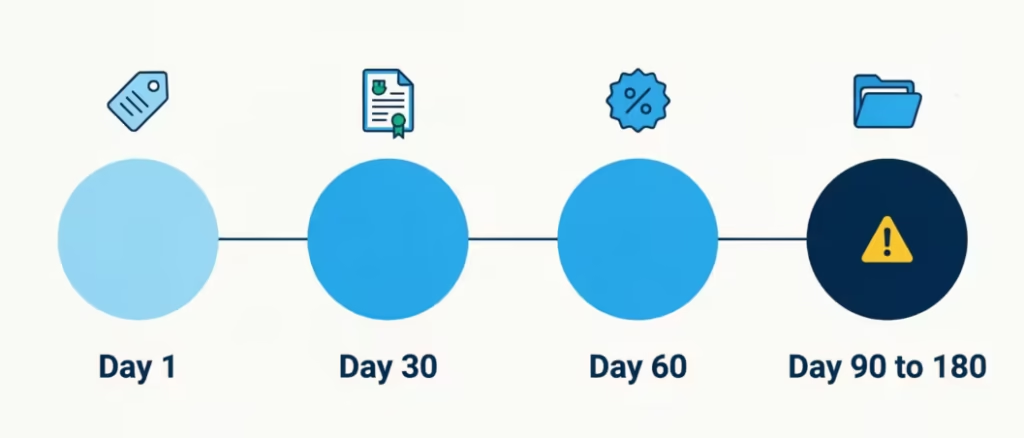

If the new minimum is out of reach this month, you have a short window to act before the situation gets worse. The consequence timeline is predictable, which means it’s also fixable.

Day 1 past due: A late payment fee posts to your account, often $30 to $41. Your account is marked past due internally, but not yet to the credit bureaus.

Day 30 past due: This is the big one. Issuers report the account as 30 days late to Experian, Equifax, and TransUnion. This is when delinquency reporting hits your credit file, and your score can drop sharply.

Day 60 past due: A penalty APR may kick in, raising your rate to as high as 29.99%. Your minimum grows further because interest just spiked.

Day 90 to 180 past due: The account can be charged off and sent to collections, which stays on your credit report for seven years.

To stop this timeline, call your issuer before the due date, not after. Ask about a hardship program. Most major issuers, including Chase, Bank of America, Citi, and Capital One, offer short-term reduced-payment plans, temporary APR reductions, or fee waivers for cardholders who reach out early. These programs aren’t advertised, but they’re real, and asking doesn’t hurt your credit.

How to Stop Your Minimum Payment From Climbing Further

You now know the cause. The decision path to keep the number from growing next month.

Start with the biggest driver from the diagnostic table above. If it’s balance growth, focus on paying more than the minimum this cycle to shrink the base the next minimum is calculated from. If it’s interest, focus on lowering the rate. If it’s a fee, focus on getting it reversed or making sure it doesn’t repeat.

Verify Your Issuer Calculated It Correctly

Open your latest statement and find the minimum payment breakdown. Match it against the formula in your cardmember agreement. Confirm these four numbers:

- Your statement balance matches your online account.

- The interest charge matches your APR times your average daily balance.

- Any fees are legitimate (not duplicates or errors).

- Your minimum percent payment matches the percentage in your agreement.

If any number looks off, call the issuer and ask them to walk through the calculation with you. Issuers make errors, and they’ll correct them when shown.

Can You Negotiate a Lower Minimum Payment?

Yes, but not through casual bargaining. The two proven paths are a hardship program or an APR reduction request. Both can lower the minimum indirectly by lowering what’s driving it up.

For a hardship program, call and say clearly: “I’m having trouble making the current minimum. What hardship options do you offer?” Ask about reduced payments, temporary APR reductions, or fee waivers. Programs usually last 3 to 12 months.

For an APR reduction, call and say: “I’ve been a customer for X years. Can you review my APR?” Success rates are higher if you’ve made on-time payments for at least six months. Even a 3% APR drop shrinks your interest charge and slows the balance climb.

If neither option works and you find yourself in the credit card minimum payment trap, consider a balance transfer card. With a 0% intro APR, it can pause interest for 12 to 21 months. This gives your payments a better chance to reduce the principal. Just watch the transfer fee, usually 3% to 5%, and have a payoff plan before the intro period ends.

Frequently Asked Questions (FAQs)

How do I lower my minimum payment on my credit card?

Pay more than the minimum each cycle to shrink the balance the percentage is calculated from, or call your issuer to ask about a hardship program or APR reduction. A 0% balance transfer card can also pause interest for 12 to 21 months while you pay down principal.

What is the minimum payment on a $5,000 credit card balance?

With a common 2% formula, the minimum would be around $100, though your issuer’s exact method (percentage, flat fee, or interest plus fees) changes the math. On a $5,000 balance at 22% APR, roughly $92 of a $110 payment can go to interest alone, leaving only about $18 toward principal.

Is it better to pay the minimum or more than the minimum?

Paying more than the minimum is always better, since minimum-only payments mostly cover interest rather than reducing your debt. On a $5,000 balance at 22% APR, minimum-only payments can take over 20 years to pay off according to CFPB estimates.

Does a higher minimum payment hurt your credit score?

No, the size of your minimum payment isn’t reported to the credit bureaus and doesn’t directly affect your score. What matters is whether you pay at least the minimum on time, since payment history makes up roughly 35% of your FICO score.

What happens if I can’t afford my new minimum payment?

A late fee posts on day 1, often $30 to $41, and by day 30 past due your issuer reports the account as late to all three credit bureaus. By day 60, a penalty APR as high as 29.99% may kick in, so calling your issuer before the due date to ask about a hardship program is the best first step.

How long will it take to pay off $15,000 in credit card debt?

The payoff time depends heavily on your APR and payment amount, since minimum-only payments are calculated to stretch balances out for years. Using the same logic as a $5,000 balance at 22% APR, which can take over 20 years on minimum payments alone, a $15,000 balance would take even longer without extra payments.

Can a cash advance increase my minimum payment?

Yes, cash advances typically carry a 3% to 5% upfront fee, no grace period, and a higher APR, often between 25% and 29%. All three factors add to your balance immediately, which raises your minimum payment for months afterward.

What triggers a penalty APR on a credit card?

A late payment can trigger a penalty APR, raising your rate to 29.99% or higher for at least six months. This higher rate increases your interest charges, which grow your balance and push your minimum payment up.

Can I negotiate a lower minimum payment with my credit card issuer?

Yes, through a hardship program or an APR reduction request, both of which lower your minimum indirectly. Hardship programs typically last 3 to 12 months, while APR reduction requests have higher success rates if you’ve paid on time for at least six months.

What’s the difference between a percentage-based minimum and a flat fee minimum?

A percentage-based minimum charges 1% to 3% of your balance, so it rises and falls as your balance changes. A flat fee minimum sets a fixed floor, often $25 or $35, and you pay that amount as long as your balance stays above it.

Bottom Line

A rising minimum payment seldom comes out of nowhere. The number goes up due to a bigger balance, higher interest, a new fee, a past-due rollover, or a one-time event like a cash advance or an expired promo APR. To stop the increase quickly, match your symptom to its cause using the diagnostic table above.

For most readers, the best way is to check the calculation. Then, tackle the biggest factor: balance, rate, or fee.

If you know someone stuck watching their minimum creep up every month, share this guide; it could save them years of interest and real stress.