You checked your credit card app and saw the words “outstanding balance.” The number felt off. It didn’t match your statement balance or your minimum payment due, and now you’re not sure what you actually owe.

That mix-up can lead to paying the wrong amount, missing your interest-free window, or worrying about a bill you don’t really have. Understanding the meaning of the outstanding balance on a credit card is the fix.

Your outstanding balance is the total amount you currently owe on your credit card, right this moment, including any recent purchases, fees, and interest.

In this guide, I’ll walk you through how it works, how it’s different from other balances, which number to pay, and how it can affect your credit score. Let’s clear it up step by step.

Key Takeaways

This guide explains what an outstanding balance on a credit card means, how it differs from your statement balance and minimum payment, and which balance to pay to avoid interest.

Core Facts:

- Your outstanding balance is the total amount you currently owe your card issuer, including purchases, cash advances, balance transfers, fees, and interest charges.

- Your statement balance is fixed on your billing cycle’s closing date, while your outstanding balance changes in real time as charges and payments post.

- Paying your full statement balance by the due date avoids interest entirely and preserves your grace period for future purchases.

- Available credit is calculated as your credit limit minus your outstanding balance minus any pending charges.

- Most issuers report your outstanding balance to the three credit bureaus (Experian, Equifax, TransUnion) around your statement closing date, and that figure determines your credit utilization ratio.

- A negative outstanding balance means the issuer owes you money, and it typically reports as a $0 balance, which is neutral for utilization.

Best for:

- New cardholders confused about the difference between outstanding balance, statement balance, and minimum payment due.

- Cardholders trying to decide which balance to pay to avoid interest or improve their credit utilization.

- Anyone reviewing daily balance changes in their credit card app and wondering why the number keeps shifting.

What Does Outstanding Balance Mean on a Credit Card?

The outstanding balance on a credit card is the total amount you owe your card issuer at any given moment. It’s a running number. Every time you swipe, tap, or use your card online, this balance goes up. Every time a payment posts, it goes down.

Most card issuers also refer to this as your current balance. The two words mean the same thing on almost every U.S. credit card statement or banking app. So if you see “current balance” in your Chase app and “outstanding balance” on your paper statement, don’t panic. You’re looking at the same number.

Here’s the plain-language definition: your outstanding credit card balance is a snapshot of your live debt. It shows you the full amount you’d need to pay to bring your card balance to zero right now. It includes charges that have already posted, interest that has already been added, and any fees you may owe.

This number is not the same as your statement balance. It’s not the same as your minimum payment. Both of those are fixed on a certain date. Your outstanding balance keeps moving.

What’s Included in Your Outstanding Balance

Your outstanding balance is made up of more than just your last few purchases. It rolls together every dollar you owe your card issuer at that moment. Here’s what typically falls into that total:

- Recent purchases. Anything you bought and that has fully posted to your account. This is the biggest piece for most people.

- Cash advances. If you used your card to pull out cash from an ATM, that amount is included. Cash advances often carry a higher APR and start racking up interest right away.

- Balance transfers. Any debt you moved from another card is counted, including any transfer fees.

- Fees. Late payment fees, annual fees, foreign transaction fees, and over-limit fees all get added in as soon as they’re applied.

- Interest charges. If you carried a balance from last month, the interest that was added to your account is now part of what you owe.

- Pending transactions (sometimes). Some issuers include pending charges in your outstanding balance; others show them separately. Check the fine print in your app to see which method your card uses.

💡 Pro Tip: If your outstanding balance looks higher than you expected, scroll through your recent activity for pending charges and any fees that posted since your last statement. That’s usually where the surprise comes from.

Outstanding Balance vs. Current Balance

These two terms cause a lot of confusion, but here’s the short answer: they mean the exact same thing.

Your outstanding balance and your current balance both refer to the total amount you currently owe on your credit card. Different card issuers just use different labels. Chase and Discover often show “current balance.” Some Citi and Capital One statements use “outstanding balance.” American Express sometimes uses both, depending on where you look.

So if your app shows a current balance of $1,081 and your paper statement calls it an outstanding balance, that’s not a mistake. The number is the same. The label is just different.

The reason this matters: many new cardholders think they owe two separate amounts and try to pay both. You don’t. There’s only one debt on your card at a time, and both labels point to it. Pick whichever term your issuer uses and stick with it in your head.

Outstanding Balance vs. Statement Balance

This is the most important comparison in this whole guide. Getting these two mixed up is what causes people to pay interest they didn’t need to pay.

Your statement balance is a fixed snapshot. It’s the amount you owed on the day your billing cycle closed. That number gets printed on your statement and does not change, no matter how much you spend afterward.

Your outstanding balance is a live number. It keeps moving. It includes your statement balance, plus anything you’ve spent since the statement closed, minus any payments that have posted.

Here’s a real worked example:

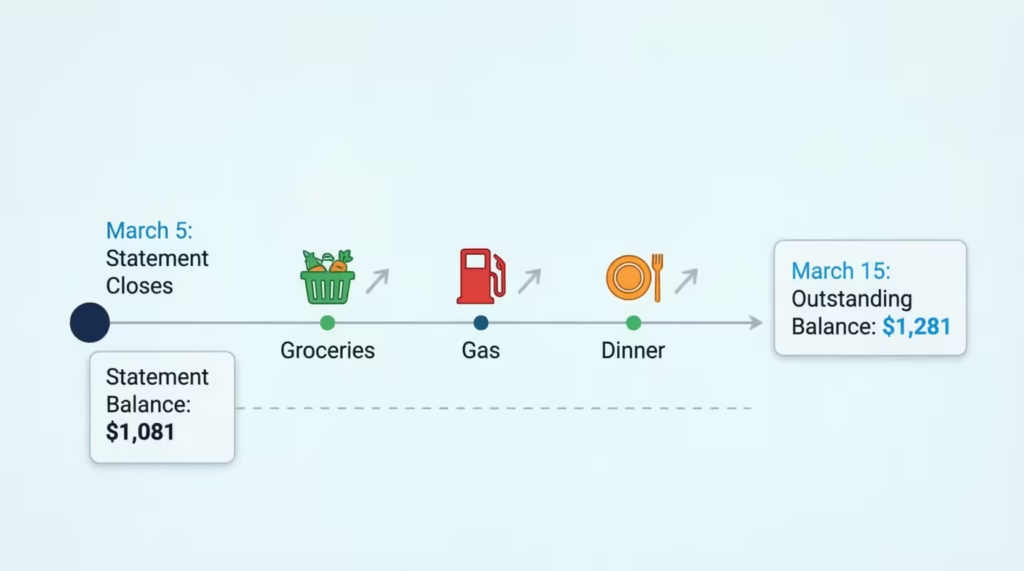

Sarah’s billing cycle closes on the 5th of each month. On March 5, her statement balance is $1,081. That’s what she owes for everything she bought during that cycle. She has until her payment due date (usually about 21 to 25 days later) to pay that $1,081 in full and avoid interest.

Between March 5 and March 15, Sarah buys groceries for $92, fills up her gas tank for $48, and pays for a $60 dinner. Her outstanding balance on March 15 is now $1,281. But her statement balance is still $1,081. Nothing new has been added to the statement balance because the cycle already closed.

If Sarah pays $1,081 (the statement balance) by the due date, she pays zero interest on those March 5 purchases. She can pay the extra $200 later without penalty, as long as she pays it before the next statement’s due date. That gap between the statement close and the payment due date is called the grace period. It only works if you pay the statement balance in full.

📌 Did You Know: If you carry any balance from one month into the next, you lose your grace period. This means new purchases can start earning interest right from the day you make them, until you pay everything off in full for two straight cycles.

Outstanding Balance vs. Minimum Payment Due

Your minimum payment due is the smallest amount your issuer will accept to keep your account in good standing that month. It’s calculated from your statement balance, not your outstanding balance.

Most issuers set the minimum at around 1% to 3% of your statement balance, plus any interest and fees. So if Sarah’s statement balance is $1,081, her minimum payment might be around $35 to $40.

The minimum payment is a bare-bones number. It keeps your account from going late. It does not keep you from paying interest. If you only pay the minimum, the rest of your statement balance starts collecting interest at your card’s APR right away.

Outstanding Balance vs. Available Credit

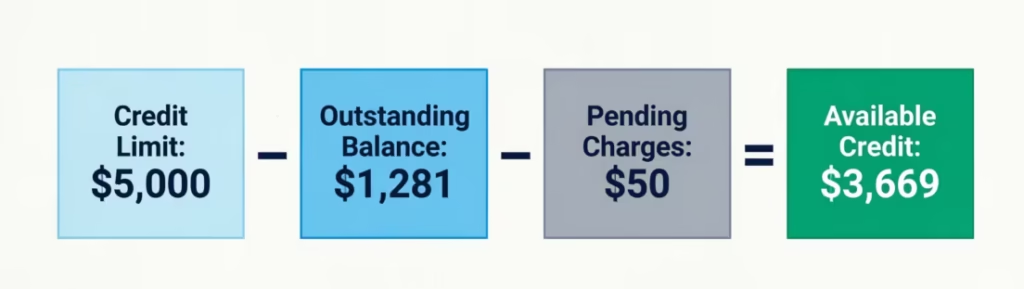

Your available credit is what you have left to spend on your card. It’s a simple formula:

Credit limit → outstanding balance → pending charges = available credit

Here’s an example. Say your credit limit is $5,000. Your outstanding balance is $1,281. You also have $50 in pending charges that haven’t fully posted yet.

$5,000 − $1,281 − $50 = $3,669 in available credit.

That’s the amount you can still charge before you hit your limit. When you make a payment, your available credit goes back up (once the payment posts). When you make a purchase, your available credit drops.

Some cards show your available credit right on the home screen of the app. Others make you tap into an account details page. Either way, the number is always tied to your outstanding balance. As one goes up, the other goes down.

Why Your Outstanding Balance Changes Throughout the Day

If you refreshed your credit card app three times today and saw three different balances, you’re not going crazy. Your outstanding balance really does shift throughout the day. This isn’t a billing error. It’s how the system works.

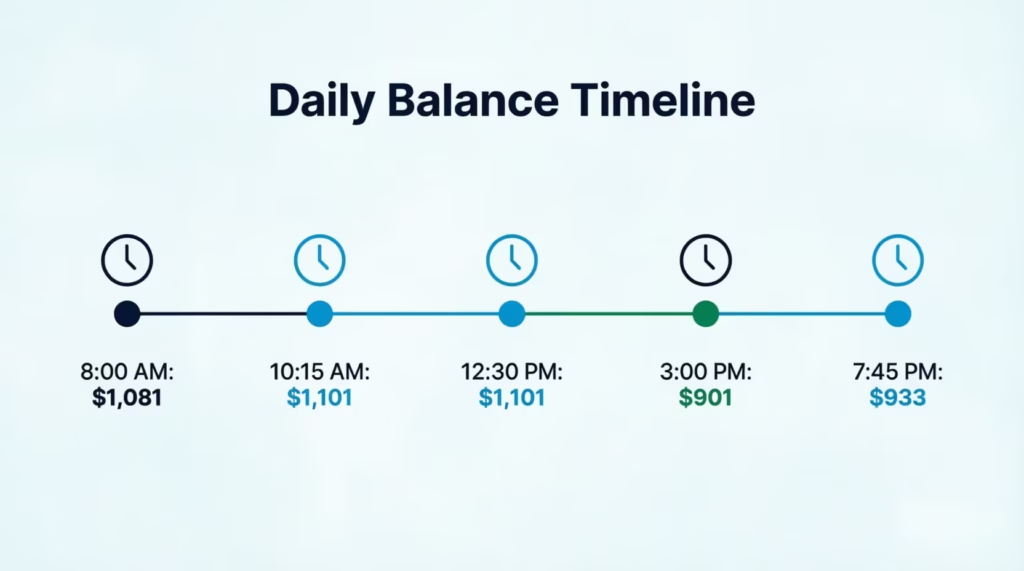

Here’s a typical timeline for a Tuesday:

- 8:00 a.m. You check your app. Balance: $1,081.

- 10:15 a.m. You buy coffee for $6. Pending transactions post to your card. Balance now shows $1,087.

- 12:30 p.m. You grab lunch for $14. Balance: $1,101.

- 3:00 p.m. A payment you made two days ago finally clears. $200 comes off. Balance: $901.

- 7:45 p.m. You order dinner online for $32. Balance: $933.

Every one of those changes is normal. Your outstanding balance moves in real time as purchases, refunds, and payments post to your account. Some transactions show up right away as pending. Others take a day or two to fully clear.

Refunds work the same way in reverse. If you returned a $75 item this morning, the credit might not show up on your outstanding balance until tomorrow or the day after. That’s on the merchant and their bank, not your card issuer.

The takeaway: don’t rely on your outstanding balance to plan a large payment right this second. Instead, use your statement balance if you’re paying to avoid interest, or wait until the end of the day for a more settled number.

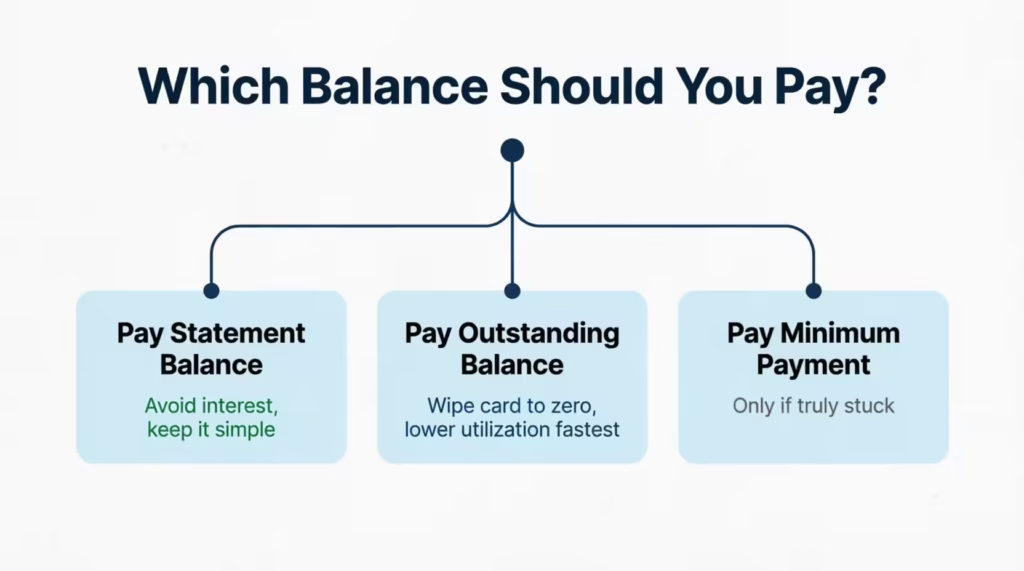

Which Balance Should You Actually Pay?

This is the question that trips up almost every new cardholder. Here’s the straight answer:

Pay your statement balance in full, by the due date, every single month. That’s the rule that keeps you interest-free.

Paying the statement balance triggers your grace period, which means the purchases from that cycle don’t earn interest. Purchases you’ve made since then won’t earn interest. This is true as long as you pay each statement in full every month.

There’s a second option if you want to be even more aggressive: pay your full outstanding balance. This wipes your card back to zero and reduces your credit utilization ratio faster, which can help your credit score if a report is about to be sent to the bureaus.

Here’s the quick decision guide:

- Pay statement balance → avoid interest and keep things simple.

- Pay outstanding balance → wipe the card, lower your utilization, pay debt down fastest.

- Pay minimum payment due → only if you’re truly stuck and can’t cover more.

⚠️ Mistake to Avoid: Paying only the outstanding balance and skipping the statement balance is not a strategy. If your statement balance is $1,081 and you pay $800 (a chunk of your outstanding balance), you still didn’t pay the statement in full. Interest kicks in on the leftover $281 immediately.

Do You Have to Pay the Full Outstanding Balance?

No. You are not required to pay your full outstanding balance to stay in good standing with your credit card issuer. The only amount you must pay to avoid a late fee and account penalties is the minimum payment due by the due date.

That said, paying only the minimum comes with a real cost. Interest keeps building. If you can pay the statement balance in full, you’re getting a short-term loan with no interest cost. That’s the smart play whenever it’s possible.

What Happens If You Only Pay the Minimum

Paying the minimum keeps your account in good standing, but it puts you on a slow, expensive path. The unpaid part of your statement balance starts collecting interest right away, at your card’s APR.

For example, if you owe $1,081 and only pay the $35 minimum, the remaining $1,046 gets charged interest. At a typical APR of around 24%, that’s roughly $21 in interest added the very next month. And it compounds. Interest gets charged on interest.

The CFPB explains that the more you pay each month above the minimum, the less interest you’ll pay over time, and the faster you’ll be debt-free.

You also lose your grace period. Once you carry a balance, any new purchase can start earning interest from day one until you clear the full debt for two straight billing cycles.

How to Find Your Outstanding Balance

Finding your balance takes about 30 seconds if you know where to look. Here are the four easiest ways:

- Mobile app. Open your credit card issuer’s app on your phone. Your outstanding balance (sometimes labeled “current balance”) is almost always shown on the home screen right under your card image. This is the fastest and most up-to-date method. Most major issuers, including Chase, Capital One, Discover, and Citi, offer free apps on the App Store and Google Play.

- Online account. Log in through your issuer’s website using a browser. After logging in, click your credit card account, and the outstanding balance shows up at the top of the account summary.

- Customer service phone line. Call the number on the back of your credit card. Most issuers have an automated menu that reads your current balance to you without needing to speak to an agent. Have your card number and last four of your Social Security number ready.

- Paper statements. If you get statements in the mail, your outstanding balance won’t be printed on them (the statement balance is). Paper statements are best used for checking your statement balance, not your live outstanding balance.

For most people, the mobile app is the simplest choice. It updates in near-real time, shows pending transactions, and often lets you make a payment in the same tap.

Does Your Outstanding Balance Affect Your Credit Score?

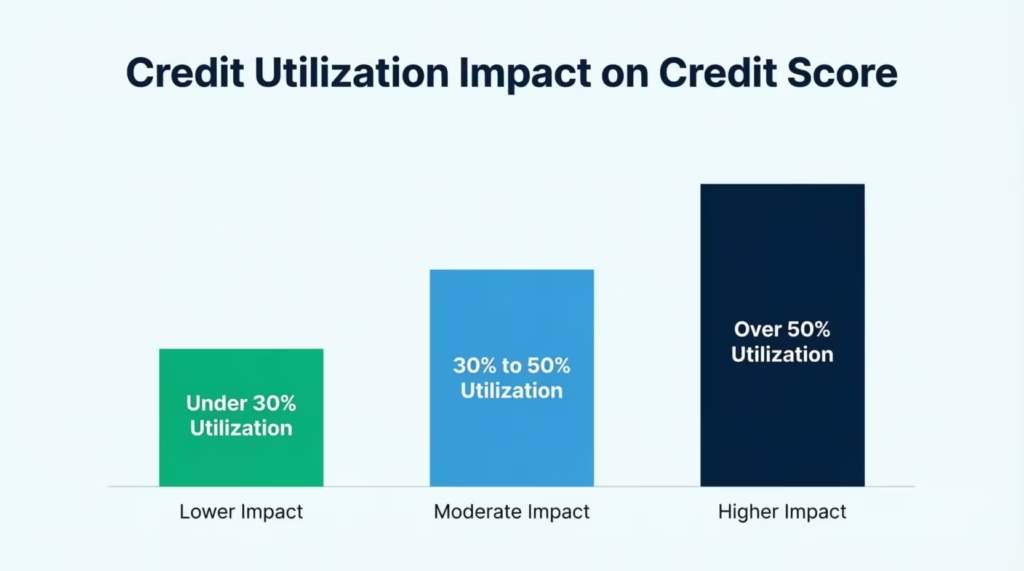

Yes, your outstanding balance directly affects your credit score. It shows up in your credit report as the amount you owe on that card, and that number feeds into your credit utilization ratio. Utilization is one of the biggest pieces of your credit score.

Your credit utilization ratio is the percentage of your total credit limit that you’re using. If your limit is $5,000 and your reported balance is $1,000, your utilization on that card is 20%.

Experian notes that revolving credit utilization is an important scoring factor that can affect around 20% to 30% of your credit score, depending on the scoring model. Broadly, keeping your utilization below 30% helps avoid a bigger negative impact.

The FICO Score is the most widely used model in the U.S. The VantageScore is the other main model, used by many free credit apps. Both look at your outstanding balances across all your cards.

Here’s the key point: it’s not the balance you carry all month that hurts your score. It’s the balance that gets reported to the credit bureaus on a specific day each month. That timing matters a lot.

When Your Balance Gets Reported to Credit Bureaus

Most credit card issuers report your outstanding balance to the three main credit bureaus (Experian, Equifax, and TransUnion) once a month, usually on or around your statement closing date. That means whatever your balance is on that specific day is the number that shows up on your credit report and gets used to calculate your utilization.

Here’s why this trips people up: Imagine you use your card heavily during the month (say, $3,000 on a $5,000 limit) but then pay it in full by the due date. If your statement closes before you pay, the bureaus see a $3,000 balance and a 60% utilization. Your score can drop, even though you never carried a balance and never paid a cent of interest.

There’s a simple workaround. Pay your card down before the statement closing date, not just before the payment due date. This way, the balance that gets reported is lower, and your utilization looks better on your credit report.

You can find your statement closing date in your app or on any recent statement. It’s usually labeled “statement closing date” or “closing date.”

What Does a Negative Outstanding Balance Mean?

A negative outstanding balance means your credit card company owes you money instead of the other way around. It looks weird on your statement, usually shown with a minus sign or in parentheses, like -$45.00 or ($45.00). This is not a mistake. It’s a real credit sitting on your account.

There are a few common reasons this happens:

- You overpaid. You paid $500 when your balance was only $455. The extra $45 sits as a negative balance.

- You got a refund after paying. You paid off your statement balance in full. Then a merchant refunded a $60 return. That $60 comes back as a credit.

- A rewards adjustment. Some cards apply cash back or statement credits that push your balance below zero, especially right after a large redemption.

- A billing correction. Your issuer removed a fee or reversed a fraudulent charge after you’d already paid.

You have three options if you see a negative balance. First, do nothing. The credit will apply automatically to your next purchase. Second, use the card normally, and the negative balance eats into your next few charges.

Third, ask your issuer for a refund by check, direct deposit, or wire. You can request this by calling the number on the back of your card, and by federal law, they must send you the money if you ask.

A negative balance doesn’t hurt your credit score. It usually reports as a $0 balance to the credit bureaus, which is neutral for your utilization ratio.

Frequently Asked Questions (FAQs)

What is an outstanding balance on a credit card?

It’s the total amount you currently owe your card issuer at any given moment, including recent purchases, fees, and interest. It’s a live number that goes up with new charges and down when payments post.

Does an outstanding balance mean I owe money?

Yes, it means you currently owe that exact amount to your card issuer. It includes posted purchases, cash advances, fees, and interest charges added since your last payment.

Is outstanding balance the same as statement balance?

No. Your statement balance is fixed on your billing cycle’s closing date, while your outstanding balance keeps changing as you spend and make payments. Paying your statement balance in full by the due date is what keeps you interest-free.

Should I pay the statement balance or outstanding balance?

Pay your statement balance in full by the due date to avoid interest entirely. Paying your full outstanding balance instead wipes your card to zero and lowers your utilization fastest, which can help your score if a report is due soon.

Is it better to pay the minimum or outstanding balance?

Paying only the minimum keeps your account in good standing but leaves the rest collecting interest at your card’s APR, often around 24%. Paying your full outstanding balance clears the debt completely and stops interest charges right away.

Can my outstanding balance affect my credit score?

Yes, it feeds directly into your credit utilization ratio, which can affect 20% to 30% of your score. Keeping your reported balance below 30% of your credit limit helps protect your score.

Why is my outstanding balance higher than my statement balance?

Your outstanding balance includes purchases made after your billing cycle closed. In contrast, your statement balance only shows charges up to that closing date. For example, if your statement balance is $1,081 and you spend $200 afterward, your outstanding balance becomes $1,281.

What happens if I don’t pay my outstanding balance?

You aren’t required to pay the full outstanding balance, but skipping even your minimum payment risks a late fee and damage to your account standing. Unpaid amounts beyond the minimum continue collecting interest at your card’s APR.

What does a negative outstanding balance mean?

A negative outstanding balance means your card issuer owes you money, usually from an overpayment, a refund after paying in full, or a rewards adjustment. It typically reports as a $0 balance to credit bureaus, which is neutral for your utilization.

How do I lower my outstanding balance?

Pay more than your minimum payment each month. The CFPB says that doing this lowers your total interest and payoff time. Paying your card down before your statement closing date also lowers the balance that gets reported to credit bureaus.

Wrapping Up

Understanding what “outstanding balance” means on a credit card is really about learning to read the different numbers on your statement and knowing which one matters, when. Your outstanding balance is the live total of what you owe. Your statement balance is the amount to pay to skip interest. Your minimum payment is the smallest amount that keeps you out of trouble. And your available credit is what’s left to spend.

The best way to handle interest and grace periods is clear: pay your full statement balance by the due date each month. That single habit keeps you interest-free and steadily builds your credit score.

If you know someone who just got their first credit card and is still figuring out their app, share this guide with them. It could save them from paying interest they never needed to owe.