Carrying $30,000 in credit card balances feels heavy. The interest keeps growing. The minimum payments barely move the needle. Generic “just budget better” advice starts to feel useless when the balance is this large.

Most people also worry that consolidation loans, settlement, or bankruptcy could make things worse. That’s a fair concern, and it’s exactly why picking the right method matters so much when you want to know how to get rid of 30k in credit card debt for good.

The fastest, safest fix is to match one payoff method (DIY, balance transfer, consolidation loan, debt management plan, settlement, or bankruptcy) to your actual credit score, monthly surplus, and creditors.

In this guide, we’ll explore all options with real numbers and clear timelines. You’ll get a simple framework to help you choose the plan that suits your needs.

Key Takeaways

This guide explains how to get rid of 30k in credit card debt, covering DIY payoff methods, balance transfers, consolidation loans, debt management plans, settlement, and bankruptcy, with real timelines and costs.

Core Facts:

- At 21% APR, a $30,000 balance generates about $525 in monthly interest, or roughly $6,300 per year, before any principal is paid down.

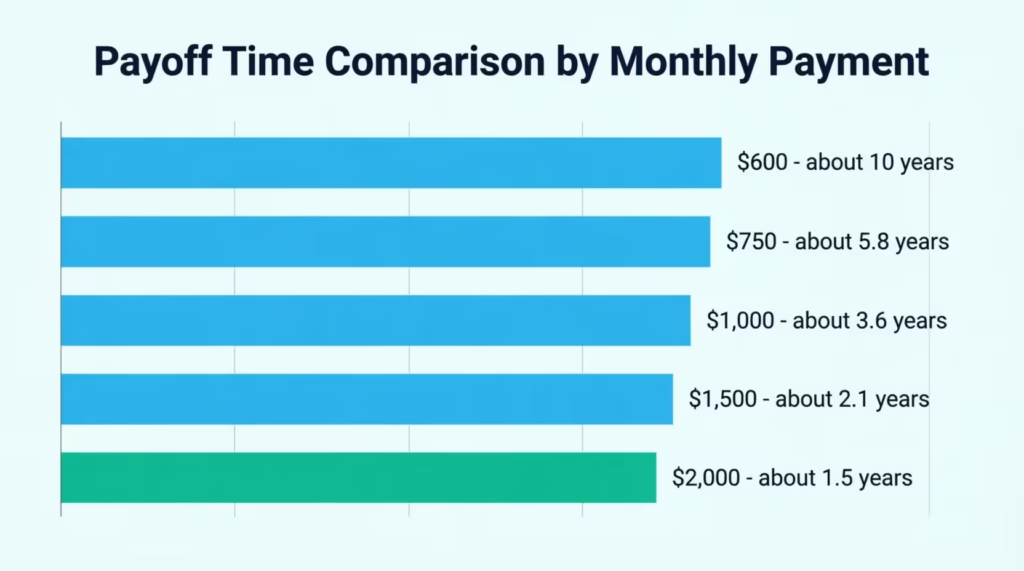

- Monthly payment amount determines payoff speed dramatically: $600 a month takes about 10 years, while $1,500 a month takes about 2 years and 1 month.

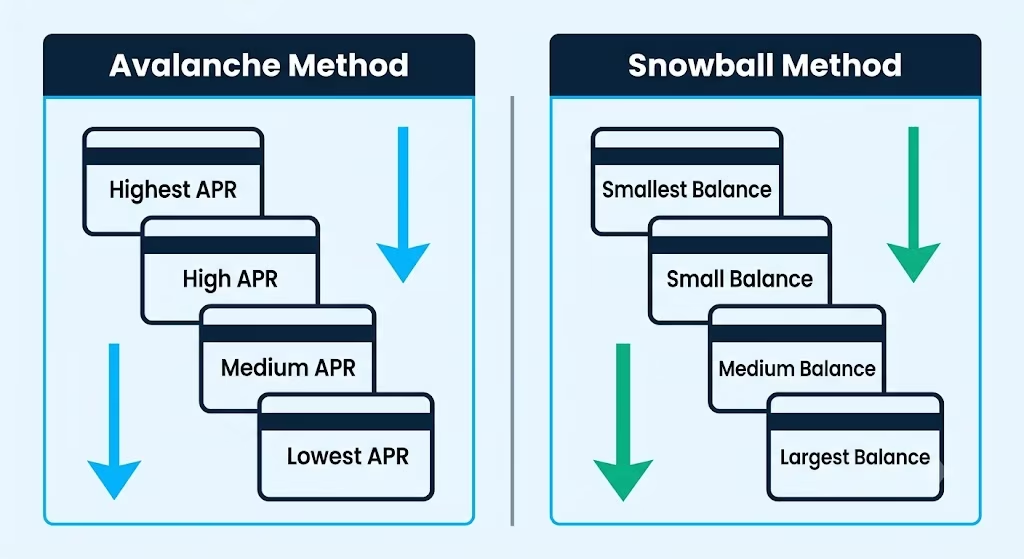

- The debt avalanche method targets the highest APR card first, while the debt snowball method targets the smallest balance first regardless of rate.

- Balance transfer cards can offer 0% APR for up to 21 months but typically charge a 3% to 5% transfer fee and usually require a credit score of 690 or higher.

- Nonprofit debt management plans can lower APRs into the 6% to 10% range and typically pay off debt in three to five years, usually requiring cards to be closed.

- Debt settlement companies typically charge 15% to 25% of enrolled debt and can drop credit scores by 100 or more points since payments are stopped during negotiation.

Best for:

- Readers carrying a $30,000 credit card balance who want to compare DIY, balance transfer, consolidation loan, and structured payoff options.

- People trying to decide between the avalanche and snowball payoff methods based on their APR spread and motivation style.

- Readers with high debt relative to income who need to evaluate whether debt management, settlement, or bankruptcy fits their situation.

What $30,000 in Credit Card Debt Really Costs You

A $30,000 balance is not just a big number. It is an interest machine. At today’s rates, it drains hundreds of dollars from your budget every month before you pay down a single cent of principal.

LendingTree, using Federal Reserve data, reports the average APR on credit card accounts that were assessed interest was 21.00% in Q1 2026. Plug that into a $30,000 balance, and the math is brutal.

Here is what you are actually paying:

- Monthly interest at 21% APR: about $525 per month

- That’s more than $6,300 in interest per year before principal

- Daily interest: about $17 per day

Now compare that to typical U.S. cardholders. The average American carries roughly $6,500 to $7,900 in credit card debt. A $30,000 balance is more than four times the national average. That means the interest hit lands four times harder too.

The minimum payment trap makes this worse. Most cards set the minimum at about 2% of the balance or interest plus 1%. On $30,000, that starts at around $600 a month. Since only $75 of that goes to principal in month one, paying only the minimum can stretch payoff to over 30 years and cost more than $50,000 in interest. You could pay back your debt almost three times over and still owe money.

That is why a plan matters. Every extra dollar above the minimum works incredibly hard for you because it skips the interest line and goes straight at principal accrual.

📌 Did You Know: If you have a $30,000 balance at 21% APR, paying just $10 more each day (about what you’d spend on lunch) can cut years off your payoff. Plus, you’ll save thousands in interest since that extra money skips the interest charge.

Getting Started: Know Your Real Numbers

Before picking a method, you need one thing: a clear, honest picture of what you owe and what you can pay. Most people guess. Guessing is why the debt grew in the first place.

List and Organize Every Balance

Pull up every credit card statement or log in to each issuer’s app. Write down these five things for every card:

- Card name (Chase Freedom, Citi Double Cash, Discover, etc.)

- Current balance

- APR (find this in the “rates and fees” section of your statement)

- Minimum payment

- Statement closing date

Put it all in a simple spreadsheet or on paper. That’s it. Do not skip a card because it feels small. A $900 store card at 29.99% APR often hurts more than a $9,000 bank card at 18%.

Here is a sample layout for a typical reader with $30,000 spread across four cards:

| Card | Balance | APR | Minimum |

|---|---|---|---|

| Card A | $12,500 | 24.99% | $260 |

| Card B | $9,800 | 22.49% | $200 |

| Card C | $5,200 | 19.99% | $110 |

| Card D | $2,500 | 27.99% | $60 |

| Total | $30,000 | $630 |

Now you can see the real shape of your debt in one glance.

How to Get Out of $30,000 in Credit Card Debt: Building Your Starting Point

Once every balance is listed, calculate two more numbers:

- Total monthly income (after tax, take-home pay)

- Total monthly expenses (rent, food, utilities, transport, insurance, subscriptions, minimum debt payments)

Subtract expenses from income. That leftover number is your monthly surplus. This is the money you actually have to attack debt with. If your surplus is $200, you cannot promise yourself $1,000 a month. Aggressive plans built on fantasy numbers fail in month two.

Your debt-to-income ratio also matters here. Divide your total monthly minimum debt payments by your gross monthly income. If your minimum payments exceed 20% of your gross income, DIY methods might not work. Instead, a debt management plan or settlement could be better options. We will get to those.

Find Extra Money to Put Toward Debt

Small, boring cuts add up faster than you expect. Look at last month’s checking account statement and mark every recurring charge. Cancel or pause what you don’t actually use. A quick real example:

Jennifer, a 41-year-old operations coordinator with $31,400 in credit card debt across three cards, went through her statements over one weekend. She canceled two streaming services ($22), a barely-used meal kit ($64), a duplicate cloud storage plan ($10), and an unused gym membership ($45). She also switched her phone plan to a $30 prepaid option, saving $55. Total found: $196 per month, or $2,352 per year, added straight to her card payments.

Then check for one-time boosts. Redirect a tax refund. Sell items you don’t use. Ask about overtime shifts. Even a temporary side income of $200 a month makes a real dent on top of extra payments.

DIY Payoff Methods: Avalanche vs. Snowball

If your credit is decent and you have a real monthly surplus, doing it yourself is usually the cheapest path. Two methods dominate. Both work. They just aim at different goals.

Debt Avalanche Method

The debt avalanche method targets the highest APR first. You pay minimums on every card except the one with the worst rate, and you throw every extra dollar at that card. Once it’s gone, you attack the card with the next highest rate.

Using our earlier example ($30,000 across four cards), the payoff order would be:

- Card D ($2,500 at 27.99%)

- Card A ($12,500 at 24.99%)

- Card B ($9,800 at 22.49%)

- Card C ($5,200 at 19.99%)

This order minimizes total interest paid. Mathematically, it is always the cheapest way to erase debt on your own.

Debt Snowball Method

The debt snowball method targets the smallest balance first, regardless of APR. You pay minimums on the rest and pile every extra dollar on the smallest card. When it’s paid off, you roll that payment onto the next smallest card.

For the same four cards, snowball order would be:

- Card D ($2,500)

- Card C ($5,200)

- Card B ($9,800)

- Card A ($12,500)

You’ll pay a bit more in interest overall. What you gain is speed of wins. Killing a card in a few months feels amazing, and that motivation keeps many people going when the total balance is scary.

How Can I Pay Off $30,000 in Credit Card Debt? Choosing Avalanche or Snowball

Pick avalanche if:

- Your APRs vary a lot (say, 15% to 29%)

- You are motivated by saving money

- You are not likely to quit if wins take a while

Pick snowball if:

- Your APRs are close (all within a few points)

- You’ve tried and quit payoff plans before

- You need quick wins to stay committed

There is no “correct” answer here. Both methods finish the same job. The best one is the one you’ll actually stick with for two to five years. You can use any free payoff calculator, which many banks and credit unions provide. It will show you the month-by-month differences for your numbers.

💡 Pro Tip: If you can’t decide, run avalanche for the first three months. If your motivation is dropping, switch to snowball. The math loss over three months is small, and finishing the plan is worth far more than saving a few hundred dollars in interest.

Realistic Payoff Timelines for $30,000

Honest timelines are where most articles get vague. So here are the real numbers, calculated at the 21% average APR, assuming no new charges.

How to Get Rid of 30000 Credit Card Debt: Timeline by Monthly Payment

| Monthly Payment | Time to Payoff | Total Interest Paid | Total Paid |

|---|---|---|---|

| $600 (near minimum) | About 10 years | ≈ $42,000 | ≈ $72,000 |

| $750 | About 5 years, 10 months | ≈ $22,050 | ≈ $52,050 |

| $1,000 | About 3 years, 7 months | ≈ $12,900 | ≈ $42,900 |

| $1,500 | About 2 years, 1 month | ≈ $7,200 | ≈ $37,200 |

| $2,000 | About 1 year, 6 months | ≈ $5,050 | ≈ $35,050 |

Read that table twice. The jump from $750 to $1,500 a month cuts your payoff time by nearly four years and saves about $15,000 in interest. That is the power of every extra dollar.

If you can’t hit $750 a month on your own, DIY alone likely won’t be enough. That is a signal to consider a lower-rate option like a balance transfer or a debt management plan (both coming up next).

How to Get Out of 30k Credit Card Debt Faster With Extra Payments

Two tactics squeeze extra progress out of any budget:

Pay twice a month, not once. Credit card interest is calculated daily on your average balance. If you break your monthly payment into two, like $500 on the 1st and $500 on the 15th, your average balance stays lower. This means you pay less in daily interest. On $30,000, this trick alone can save $150 to $300 a year.

Throw every windfall at the principal. Tax refunds, bonuses, birthday cash, insurance rebates, a gift card you sold. Every dollar that lands outside your normal budget should go straight to the card you’re currently attacking. A single $2,000 tax refund applied to a 24.99% card saves about $500 a year in interest and shortens your timeline by nearly two months.

⚠️ Mistake to Avoid: Do not close paid-off cards during payoff. Closing accounts reduces your available credit. This increases your credit utilization ratio, which can hurt your FICO score. This is especially important if you need a balance transfer or a consolidation loan.

Lowering Your Interest Rate: Balance Transfers and Consolidation Loans

If your credit score is at least around 670, you can often cut your APR sharply. Lower APR means more of your payment attacks the principal. That is usually the single biggest lever for a $30,000 balance.

Balance Transfer Cards

A 0% intro APR balance transfer card lets you shift your debt to a new card. This card charges no interest for a set period, which can be up to 21 months on top-tier options. During that window, every dollar you pay goes to principal.

The catch is fees. Most cards charge a balance transfer fee of 3% to 5% of the amount transferred. On $30,000, that’s $900 to $1,500 upfront. There are also two hard limits on the strategy:

- You usually need a credit score of 690 or higher to be approved for the best offers.

- Most cards have a credit limit lower than $30,000, so you may only move part of your debt.

Realistic plan: transfer as much as you can (say, $12,000 to $18,000), then use avalanche on whatever stays on your old cards.

Two of the longest 0% intro offers as of 2026 are the Wells Fargo Reflect Card and the Citi Diamond Preferred Card, both currently offering 21 months at 0% for qualifying transfers.

Check the transfer fee and the ongoing APR before applying. If you can’t pay off the balance before the intro period ends, the regular APR usually rises to 17% to 28%.

How to Pay Off 30000 in Credit Card Debt With a Consolidation Loan

A debt consolidation loan is a fixed-rate personal loan that pays off all your cards at once. You then repay the loan in equal monthly installments, usually over three to seven years.

Why it works: personal loan APRs for good credit borrowers are often 8% to 15%, versus 21% on cards. Your rate is locked, and your payment is predictable.

Watch for these three costs:

- Origination fee of 1% to 8% (some lenders take it from the loan proceeds, so a $30,000 loan may deposit $28,000 in your account).

- Higher APR if your credit score is below 670, sometimes above your card rate.

- Prepayment penalties on some lenders (avoid these).

Do the math before signing. If your loan APR plus fees costs more than what you’d pay on your cards using avalanche, the loan isn’t helping. A quick check: multiply the loan payment by the number of months, then compare that total to the interest you’d pay staying on cards. Whichever total is lower wins.

Negotiating Directly With Your Card Issuer

This step is free, takes 15 minutes, and works more often than people expect. Card issuers would rather cut your rate than lose you to a competitor or to charge off.

How to Get Rid of $30k in Credit Card Debt Without a Loan or Card

Call the number on the back of your card. Ask for the “hardship” or “customer retention” department.

Then use a simple script:

“Hi, my name is [name]. I have been a customer since [year]. I am carrying a balance of $[amount] at [current APR], and I am trying to pay it off responsibly.

I have received offers from other issuers at lower rates. Can you reduce my APR so I can stay with you and finish paying this down?”

Stay calm and polite. If the first agent says no, thank them, hang up, and try again in a few days with a different agent. Results vary, but many customers report drops of 3 to 8 percentage points on at least one card. On $30,000, a 5-point APR cut saves about $1,500 in interest per year.

Even better if you can honestly say you have on-time payment history for the last 12 months. That single line moves outcomes more than anything else.

Combine this call with credit counseling later if the issuer says no. The counseling agency can often get rate concessions the individual customer cannot.

Structured Help: Credit Counseling and Debt Management Plans

If DIY isn’t working and you can’t get a good balance transfer or consolidation loan, your next step is to contact a nonprofit credit counseling agency. This is the middle ground: more structure than DIY, far less damage than settlement or bankruptcy.

How to Get Rid of $30 000 Credit Card Debt Through a Debt Management Plan

A nonprofit counselor first reviews your budget for free. If it makes sense, they set up a debt management plan (DMP). Here is how a DMP actually works:

- The counselor negotiates with your card issuers to lower APRs, often into the 6% to 10% range.

- You make one monthly payment to the agency. They pay each creditor.

- Most DMPs are structured to pay off your debt in three to five years.

- Your cards are usually closed as part of the plan.

The National Foundation for Credit Counseling (NFCC) is the largest network of accredited nonprofit agencies. Fees are modest, typically a small setup fee and a monthly fee capped at about $25 to $50 total. There is no interest charged on top of your card interest.

Credit impact is real but manageable. Closing older cards can drop your score by 20 to 50 points at first because your credit utilization ratio goes up. Since you’re making on-time payments through the plan, most people see their score recover and grow within a year.

A DMP is a strong fit if:

- Your APRs are high, and issuers won’t budge

- Your surplus is enough to cover a 3 to 5 year payoff but not much faster

- You want structure and support, not just a spreadsheet

It is not the right fit if your income truly can’t cover the DMP payment. In that case, keep reading.

Debt Settlement: How It Works and What It Really Costs

Debt settlement is often marketed as the “cut your debt in half” option. The truth is more complicated. It can work, but the costs go far beyond what most ads mention.

Here is the process:

- You stop paying your cards (this is required for most for-profit settlement companies to negotiate).

- You deposit money into a savings account they control, usually for 24 to 48 months.

- Once enough cash is built up, the company negotiates with each creditor to accept a lump sum of 40% to 60% of what you owe.

On $30,000, that might mean settling for $12,000 to $18,000. Sounds great. Now the real costs:

- Fees: Settlement companies typically charge 15% to 25% of the enrolled debt, so $4,500 to $7,500 on your $30,000.

- Credit score damage: Because you stop paying, each account gets marked late, then charged off. Investopedia reports scores can drop 100+ points, and the negative marks stay on your report for seven years.

- Taxes: If a creditor forgives more than $600, they file a 1099-C with the IRS. The forgiven amount is generally treated as taxable income. The IRS explains in Publication 4681 that you may exclude some or all of that income if you were legally insolvent (your total debts exceeded your total assets) at the time of forgiveness. That exclusion can save thousands, but it requires paperwork and often a tax professional.

- Lawsuits: While you are not paying, creditors can sue. A default judgment can lead to wage garnishment in many states.

Settlement can still be the right call if you truly cannot pay, your credit is already damaged, and bankruptcy isn’t a fit. If you go this route, working with a licensed attorney or a nonprofit counselor (not a for-profit settlement chain) usually protects you better.

When Bankruptcy Makes Sense for $30,000 in Credit Card Debt

Bankruptcy carries stigma, but it is a legal tool. For some people carrying $30,000 in unsecured credit card debt, it is the fastest, cleanest path to a fresh start. U.S. Courts data shows over 574,000 bankruptcy cases were filed in 2025, so it is far from rare.

Two chapters matter for consumers:

Chapter 7 wipes out most unsecured debt (including credit cards) in about three to six months. To qualify, your income must be below your state’s median, or you must pass the means test administered by the U.S. Trustee Program. You might need to give up some non-exempt assets. However, most filers keep their car, retirement accounts, and household goods because of state exemptions.

Chapter 13 is a court-supervised repayment plan lasting three to five years. You keep your assets and pay creditors a portion of what you owe based on your income. This route fits people who have steady income but too much of it to pass Chapter 7, or who want to catch up on a mortgage or car loan.

Credit impact and recovery:

- Chapter 7 stays on your credit report for 10 years; Chapter 13 for 7 years.

- Most filers can qualify for a mortgage 2 to 4 years after discharge with FHA loans, sometimes sooner.

- FICO scores often start recovering within 12 to 18 months of discharge as new positive tradelines are added.

Signals that bankruptcy deserves a serious look:

- Total unsecured debt is more than half your annual gross income

- Even a strict DMP would not finish in 5 years

- You are facing lawsuits, garnishment, or account levies

- You are drawing down retirement funds to pay cards (this is almost always a mistake)

A one-time consultation with a bankruptcy attorney is often free. Even if you don’t file, the meeting tells you where you truly stand.

Choosing the Right Strategy for Your Situation

Now put it all together. Every method above works, but only one fits your combination of credit score, monthly surplus, and total debt load.

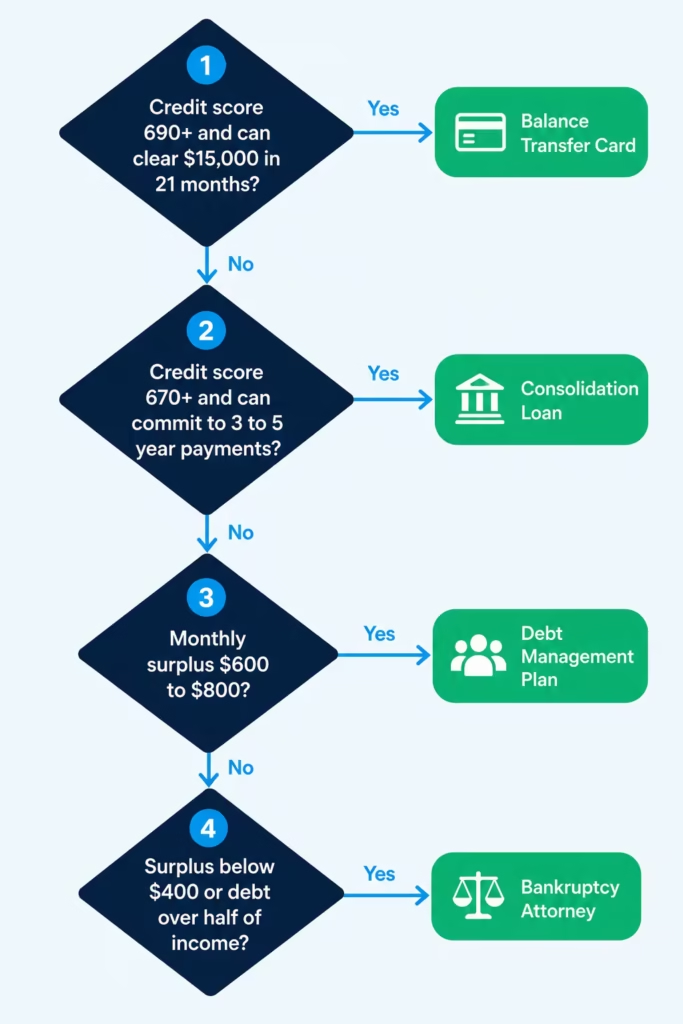

How to Get Rid of 30k in Credit Card Debt: A Quick Decision Guide

Answer these four questions in order. The first “yes” points you to your best starting move.

- Is your credit score 690+ and can you clear at least $15,000 in 21 months? → Start with a balance transfer card. Move as much as your limit allows, and put the rest on avalanche.

- Is your credit score 670+ and can you commit to a fixed 3 to 5 year payment? → Look at a debt consolidation loan with a rate at least 5 points below your card APR. Lock it in.

- Is your monthly surplus at least $600 to $800, but your credit isn’t strong enough for options 1 or 2? → Start with a call to a nonprofit counselor and consider a debt management plan through the NFCC.

- Is your surplus below $400, or is your total debt more than half your annual income? → Talk to a bankruptcy attorney first. If bankruptcy isn’t a fit, then explore debt settlement with a qualified professional (not a mass-market settlement company).

No matter which path you choose, pick one payoff method (avalanche or snowball). Then, set a monthly payment you can stick to and put it on autopay.

Avoiding the Relapse: Staying Out of Debt After Payoff

Consolidation loans and balance transfers can make your credit cards $0. However, they don’t fix the spending habits that led to the debt. Studies of consolidation loan borrowers repeatedly show a large share end up with new card debt within two to three years. That is called consolidation relapse, and it is the real reason people cycle through debt for a decade.

Three habits stop it cold:

Keep spending on one boring card, not the ones you just paid off. Keep paid-off cards open to maintain a low credit utilization ratio and a healthy score. However, store them in a drawer or lock them in your issuer’s app. Use one card, ideally a debit card or a low-limit card, for daily spending.

Automate an emergency fund on payoff day. As soon as your last card balance reaches $0, send that same payment to a high-yield savings account. Start by saving enough for one full month of expenses. After that, aim for three months. Cards fill back up because there is no cushion for surprises. Build the cushion first.

Set a hard rule: no new balance you can’t pay in full by the statement date. If a purchase can’t be paid off from the current month’s income, don’t put it on the card. That single rule keeps your credit utilization ratio low and protects everything you just accomplished.

Frequently Asked Questions (FAQs)

Is $30,000 in credit card debt a lot?

Yes, it’s more than four times the typical American’s balance of $6,500 to $7,900. At 21% APR, that size balance generates around $525 in monthly interest before any principal gets paid down.

How long does it take to pay off $30,000 credit card debt?

At $600 a month, it takes about 10 years and costs roughly $42,000 in interest. At $1,500 a month, that drops to about 2 years and 1 month with only $7,200 in interest.

How to clear 30k debt fast?

Combine a rate-reduction tool, like a 0% balance transfer or consolidation loan, with the avalanche method on any remaining balance. Paying $1,500 to $2,000 monthly can clear $30,000 in 18 to 25 months.

What to do if you have $30,000 in credit card debt?

List every balance, APR, and minimum payment, then calculate your monthly surplus. Use that surplus to choose between DIY payoff, a balance transfer, a consolidation loan, a debt management plan, or bankruptcy based on your credit score and income.

How many Americans have $20,000 in credit card debt?

The article doesn’t give a specific count for Americans at the $20,000 mark, but it notes the average U.S. cardholder carries $6,500 to $7,900. A $20,000 balance would be roughly three times that national average.

What is the average credit card debt total for a US citizen?

The average American carries roughly $6,500 to $7,900 in credit card debt. A $30,000 balance is more than four times that typical amount.

How can I get out of $30,000 credit card debt?

Start with a decision guide based on your credit score and surplus: balance transfer if your score is 690+, a consolidation loan if it’s 670+, a debt management plan if your surplus is $600 to $800, or bankruptcy if your surplus is below $400.

Will closing cards hurt my credit score?

Yes, closing paid-off cards reduces your available credit and raises your utilization ratio, which can hurt your FICO score. Through a debt management plan specifically, closing cards can drop your score by 20 to 50 points initially, though it typically recovers within a year.

How long does it take to pay off $25,000 in debt?

The article gives timelines for $30,000, not $25,000 specifically, but a smaller balance at the same payment would pay off somewhat faster. At $1,000 a month on $30,000, it takes about 3 years and 7 months, so $25,000 would land under that mark.

What debt doesn’t go away?

Certain debts like most federal student loans, child support, and some tax debts typically survive bankruptcy, unlike unsecured credit card debt. Credit card debt itself can be eliminated through Chapter 7 bankruptcy in about three to six months.

Wrapping Up

Getting out from under a $30,000 balance is possible, but only with a plan that fits your actual numbers. This guide covers the real cost of debt, how to organize your balances, and DIY methods. It explains honest payoff timelines, rate-reduction tools, structured plans, and last-resort options like settlement and bankruptcy.

The best strategy for most readers is simple: first, lower the interest rate using a balance transfer, consolidation loan, or DMP. Then, use the avalanche method for the remaining balance. That combination cuts years and thousands in interest off any payoff plan.

If you know someone quietly carrying a large card balance, share this guide with them. It could save them a decade and tens of thousands of dollars.