I know the feeling. You’ve spent weeks scrolling through listings, and you’ve finally found the camper that fits your life, whether it’s a weekend travel trailer or a full-time home on wheels. But before you sign anything, one question keeps stopping you cold: is your credit score good enough to actually get approved, and at a rate you can live with? Getting clear answers on the credit score needed to buy a camper shouldn’t require guesswork or a wasted hard credit pull.

Most mainstream lenders require a FICO score between 660 and 680 for camper financing. However, some specialty lenders may approve scores as low as 550, but there are tradeoffs.

Here are the score tiers, rate ranges, loan-size effects, and steps to boost your application before you apply.

Key Takeaways

This guide explains what credit score is needed to buy a camper, including score tiers, how loan amount and camper type affect requirements, APR ranges by credit tier, and steps to strengthen a loan application.

Core Facts:

- Most mainstream lenders require a FICO score between 660 and 680 for camper financing, while some specialty lenders approve scores as low as 550.

- Loan size affects the score floor: loans under $25,000 typically need 600 to 640, while loans of $150,000 and above typically need 720 to 740 or higher.

- Camper loans generally require a credit score 20 to 40 points higher than an auto loan of the same amount because lenders view campers as discretionary purchases.

- Excellent credit (750+) can see APRs around 6.5% to 8.5%, while subprime borrowers (below 620) may face APRs of 20% to 30% or more.

- On a $50,000 camper over 15 years, a 7% APR costs about $30,900 in total interest, compared to about $69,800 at 14% APR on the same loan.

- Most RV lenders prefer a debt-to-income ratio at or below 36%, though some stretch to 43% for strong applicants.

Best for:

- Prospective camper or RV buyers trying to determine which credit tier they fall into before applying for financing.

- Buyers comparing loan amounts or camper sizes to understand how the purchase price affects their required credit score.

- Borrowers with fair or below-average credit weighing whether to apply now or rebuild credit first to reduce total loan cost.

Credit Score Tiers for Camper Financing

RV and camper lenders sort borrowers into four broad credit tiers. Each tier signals how risky a lender thinks you are, and that risk shapes your approval odds, your interest rate, and how much cash you’ll need up front. The average approval score for a camper loan sits around 660 to 680, but the picture changes a lot depending on which tier you fall into.

Here is how lenders typically group applicants when they review a credit score for RV loan requests. This is the section most buyers scan first, so the numbers matter.

| FICO Score Range | Tier | Approval Likelihood | What to Expect |

|---|---|---|---|

| 750 and above | Excellent | Very high | Best APRs, lowest down payment, longest terms |

| 700 to 749 | Good | High | Strong rates, standard down payment, most lenders open |

| 640 to 699 | Fair | Moderate | Approval possible, higher APR, larger down payment |

| Below 640 | Subprime | Low to limited | Specialty lenders only, high APR, short terms |

The FICO score model most lenders check is FICO 8, and some use FICO 9 or FICO Auto scores for RV underwriting. Experian data shows the average U.S. FICO score reached 715 as of 2025, which sits solidly in the “Good” tier for camper approval.

Where your score falls in this credit score range decides not just if you get approved, but how much your camper truly costs over the life of the loan. A borrower at 760 and a borrower at 640 buying the same $40,000 trailer can pay thousands more or less in total interest.

💡 Pro Tip: Pull your own credit report from all three bureaus before you shop. A soft pull won’t hurt your score, and it lets you fix errors that might drop you a full tier before a lender ever sees your file.

What’s the Minimum Credit Score to Qualify?

Most mainstream banks and credit unions set their floor for camper loans between 600 and 660. Below that, you move into specialty and subprime territory, where a few lenders will go as low as 550 for smaller camper loan amounts.

But here’s the part many buyers miss. Qualifying for a loan and qualifying for a loan with fair terms are two different things.

A 600 FICO might get you a “yes,” but the APR could be double what someone with a 720 pays. The term might be shorter, cutting your monthly cushion. The down payment could jump from 10% to 20% or more. So when you look at RV loan credit score requirements, look past the raw approval number and study the full offer.

The realistic buckets for camper financing credit score requirements break down like this:

- 660 and above: Standard approval at most banks, credit unions, and RV lenders.

- 620 to 659: Approval possible, but rates rise sharply and down payment demands grow.

- 580 to 619: Subprime territory. A few lenders will work with you on smaller loan amounts.

- 550 to 579: Very limited. Usually specialty RV lenders or buy-here-pay-here dealers only.

- Below 550: Traditional financing is off the table. Consider rebuilding credit first.

The minimum credit score to finance a camper also shifts by lender type. Credit unions often accept lower scores than big banks. They look at your membership history and overall financial picture. Specialty RV lenders may accept lower scores but usually require larger down payments to protect themselves.

Why There’s No Single Universal Number

You’ll see one blog say “you need 680” and another say “700 is the floor.” Both can be right, and neither is the full answer.

Each lender sets its own risk appetite. A national bank funding thousands of RV loans a month may cap at 660. A niche RV lender that specializes in luxury motorhomes may want 720 or higher. A local credit union with a member you’ve banked with for 15 years might approve you at 620 based on relationship.

FICO models add another layer. Auto lenders sometimes pull FICO Auto Score 8 or 9, which weighs auto and vehicle loan history more heavily. Your regular FICO 8 might read 690, but your FICO Auto 9 could come back as 705 or 675 depending on your file. That’s why the same person can get two different “your credit score” numbers on the same day.

Loan program rules also change the floor. A lender might publish a 660 minimum but require 700 for used campers over 10 years old. So the “minimum” always comes with fine print.

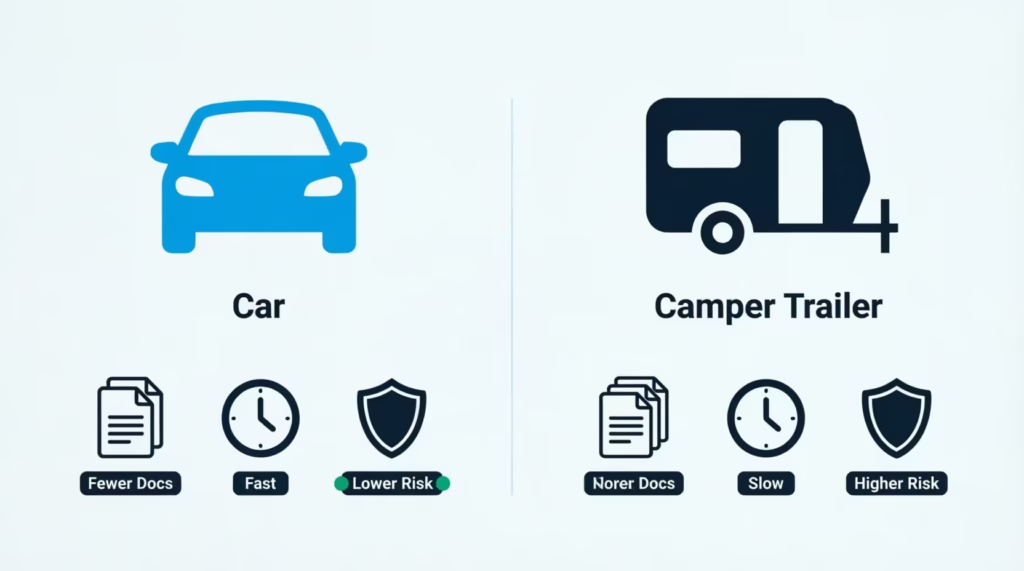

How the Loan Amount Changes the Score You’ll Need

The size of your RV loan shifts the credit bar in a very real way. Lenders take more risk on bigger balances, so they demand stronger credit as the ticket price climbs. This is one of the biggest gaps in most online guides, and it matters a lot when you’re choosing between a $15,000 pop-up and a $95,000 Class C.

Here’s how the loan-to-value ratio and loan size typically shape score expectations:

| Loan Amount | Camper Type Example | Typical Score Floor | Notes |

|---|---|---|---|

| Under $25,000 | Pop-up, small used travel trailer | 600 to 640 | Most lenient; some lenders treat like an auto loan |

| $25,000 to $75,000 | New travel trailer, mid-size fifth wheel | 660 to 680 | Standard camper loan tier |

| $75,000 to $150,000 | Class C motorhome, luxury fifth wheel | 700 to 720 | Stricter underwriting, more documentation |

| $150,000 and above | Class A motorhome, diesel pusher | 720 to 740+ | Jumbo RV underwriting, sometimes tax returns required |

The reason is straightforward. If you default on a $20,000 travel trailer, the lender can resell it fast and recover most of the balance. If you default on a $180,000 Class A motorhome that lost 20% of its value the day you drove it off the lot, the lender is looking at a big loss. Higher balances mean higher risk, and higher risk means the lender wants stronger credit.

The credit score needed to buy an RV also changes with the age of the camper. Many lenders add stricter score rules for units older than 10 years, because used campers depreciate faster and are harder to resell. So a 660 score might sail through on a new $45,000 travel trailer but stall on a 12-year-old $45,000 rig.

If your score sits at the edge of a tier, you can sometimes drop to a smaller unit or a slightly newer used model to slide into an easier approval bracket. Small choice, big effect.

RV and Camper Loans vs. Auto Loans, Why the Bar Is Higher

Many buyers walk in expecting camper financing to feel like an auto loan. It doesn’t. The credit score needed for RV loan approval is often 20 to 40 points higher than for a car loan of the same amount. This difference comes from how lenders view the purchase.

Lenders treat cars as necessities. You need one to get to work, so borrowers fight hard to keep car payments current, even in tough times. Default rates on auto loans stay lower because of that behavior pattern.

Lenders treat campers, motorhomes, and travel trailers as lifestyle or discretionary purchases. When budgets tighten, the RV payment is one of the first things people drop. Default risk is higher, so camper financing credit score requirements are stricter to offset that risk.

This classification changes three things for the borrower:

- Higher score expectations. A 640 gets you approved on a car loan almost anywhere. A 640 for an RV puts you in fair or subprime territory with fewer lender options.

- More documentation. Expect pay stubs, tax returns for self-employed buyers, and sometimes proof of storage or insurance before funding.

- Longer approval timeline. Auto loans often close same-day. RV loans can take three to seven business days for underwriting to review your file.

So the answer to “is it easy to finance an RV” is honestly no, not compared to a car. The bar is higher, the review is deeper, and the fine print matters more. But knowing this ahead of time lets you prep your file properly instead of getting blindsided by a denial after weeks of shopping.

What Your Credit Score Gets You (Rates by Tier)

Approval is just step one. The interest rate you get based on your score decides how much the camper actually costs. On a 15-year RV loan, even a 2% APR difference can add tens of thousands to the total paid.

Current RV loan rates in 2026 vary. Buyers with excellent credit can expect rates around 6.49%. For those in the subprime category, rates can go as high as 35.99%. Average new RV loan APRs run about 7.53%, and used RV loans average 7.69% based on LendingTree’s borrower data.

Here’s what different credit tiers can expect for APR ranges and down payment percentages on a standard camper loan:

| Credit Tier | Typical APR Range | Typical Down Payment | Typical Term |

|---|---|---|---|

| 750 and above | 6.5% to 8.5% | 10% | Up to 20 years |

| 700 to 749 | 8% to 11% | 10% to 15% | 15 to 20 years |

| 660 to 699 | 11% to 15% | 15% to 20% | 12 to 15 years |

| 620 to 659 | 15% to 20% | 20% to 25% | 10 to 12 years |

| Below 620 | 20% to 30%+ | 25%+ or specialty | 7 to 10 years |

To see why this matters, look at a $50,000 camper financed over 15 years. At 7% APR, the monthly payment lands near $449 and total interest paid is about $30,900. At 14% APR on the same camper, the monthly payment climbs to $666 and total interest hits $69,800. Same trailer. Nearly $39,000 more paid over the life of the loan, all because of the credit tier.

A lower credit score for RV loan approval often triggers three things at once: a higher APR, a bigger required down payment, and a shorter term. Lenders use these levers together to reduce their risk. Instead of denying you outright, they price the loan so they’re protected either way.

📌 Did You Know: RV loan terms can stretch to 20 years for larger motorhomes, much longer than a standard 5 to 7 year auto loan. That long term is why even small APR differences balloon into massive dollar amounts by the end.

What Lenders Look at Besides Your Credit Score

Your score opens the door, but it doesn’t finish the deal. Lenders review your full financial picture before they say yes, and a great score with weak other factors can still get denied.

The main pieces they weigh:

Debt-to-income ratio (DTI). This is the percentage of your gross monthly income that already goes to debt payments. Most RV lenders prefer a debt-to-income ratio at or below 36%, and many will stretch to 43% for strong applicants. Fannie Mae’s standard for total DTI on qualifying mortgages is 36%, with allowances up to 45% for borrowers with strong compensating factors, and most RV lenders follow a similar framework. If your DTI runs above 45%, expect a denial even with a 740 score.

Income stability and employment history. Two years in the same job or the same field carry weight. Job hoppers and 1099 contractors face more paperwork, including two years of tax returns instead of just recent pay stubs.

Length of credit history. Someone with 15 years of accounts in good standing beats someone with the same score but only three years of history. Lenders want to see how you’ve handled credit across time and across different economic conditions.

Credit utilization. This is how much of your available revolving credit you’re actively using. High credit utilization (above 30% on cards) signals financial stress even if your score still looks decent. Pay balances down before you apply.

The camper itself as collateral. RV loans are secured loans, meaning the camper secures the debt. Lenders look at the unit’s age, mileage, condition, and resale value. A 15-year-old rig with 90,000 miles is much harder to finance than a new one, because the collateral loses value faster than the loan pays down.

Walk through each of these before you submit an application. If your DTI is 48%, work on paying down a credit card first. If your utilization is 60%, drop it under 30% two months before applying. Small changes here can beat trying to raise your credit score by 20 points.

Buying a Camper with Bad or Below-Average Credit

Yes, you can finance a camper with a lower score. The tradeoffs just get steeper.

Most subprime lender programs for RVs will look at scores from 550 to 619, with a few going as low as 500 for very small loan amounts. The typical floor for RV financing with bad credit is about 550. Some dealer in-house programs may go lower, but they have strict conditions.

Here’s what to expect if you’re asking “can I finance a camper with bad credit“:

- Higher APR. Expect 18% to 30% or higher, sometimes matching credit card rates. On a 10-year loan, that adds tens of thousands in interest.

- Larger down payment. Plan for 20% to 30% down, sometimes more. The lender wants immediate equity to protect against default.

- Shorter term. Instead of 15 or 20 years, you’re looking at 7 to 10 years. That raises the monthly payment even with a smaller loan balance.

- Smaller loan cap. Many bad-credit RV programs cap out around $30,000 to $50,000. Luxury motorhomes are usually off the table.

- Age limits on the camper. Expect the lender to require newer units, often under 10 years old, since old campers lose value fast.

Buy here pay here financing and dealer in-house financing are two other options that come up. Both can approve you when banks won’t, but proceed carefully. APRs for buy-here-pay-here deals usually go over 20% to 25%.

Also, these loans often get reported to just one credit bureau or not at all. This means you won’t build any credit history by paying it off. Some dealers also add tracking devices and quick-repo terms that make default extra painful.

⚠️ Mistake to Avoid: Don’t sign a bad-credit RV deal without running the math on total cost paid. A $35,000 camper at 24% APR over 8 years costs you about $77,000 total. Sometimes waiting six months to rebuild credit saves you $30,000 or more.

If your score is under 580, seriously consider spending 6 to 12 months rebuilding before you buy. Pay down credit cards, dispute errors on your report, avoid new inquiries, and let time do some of the work. The dollar savings on the loan usually beat the delay by a large margin.

How to Strengthen Your Application Before You Apply

You have more control over your approval odds than most buyers realize. A few concrete moves before you submit can lift you into a better tier, cut your APR, and save real money. Focus on these levers.

Put down more cash. Aim for a 10% to 20% down payment at minimum, and 25% if your score sits in the fair tier. A bigger down payment lowers the loan-to-value ratio. This reduces lender risk and can lead to better terms, even for average credit. On a $50,000 camper, moving from 10% down to 20% down is another $5,000 out of pocket but can drop your APR by 1% to 3%.

Add a qualified co-signer. A co-signer with strong credit (720+) and low DTI can pull your application into a better approval tier. The co-signer takes on full legal responsibility for the debt, so this only works if both of you understand the stakes. Family members are the most common option, and the arrangement can be worth thousands in interest savings.

Downsize the unit. Consider a smaller camper or a slightly older used model to bring the loan amount into a more lenient tier. Switching from a $90,000 fifth wheel to a $45,000 travel trailer can shift you from luxury underwriting to standard approval. This can happen without altering your score at all.

Get pre-qualified with a soft pull first. Most credit unions and online RV lenders offer pre-approval with a soft credit check that doesn’t hurt your score. This lets you see actual rate offers before committing to a hard credit inquiry. Get soft quotes from three to five lenders, then apply formally only to the best match.

Shop credit unions and specialty RV lenders. A credit union often beats bank rates by half a point to a full point for members, and they weigh your full relationship, not just the raw score.

Specialty RV lenders like Good Sam Finance, My Financing USA, and Trident Funding target RV buyers. They often approve applications that banks might reject. Consider a soft-pull quote at your existing credit union first; you can start with the National Credit Union Administration’s credit union locator to find one you’re eligible to join.

Time your inquiries. Multiple RV loan inquiries made within 14 to 45 days typically count as one on your credit report. So, feel free to shop around with several lenders quickly. What hurts your score is a hard inquiry every few weeks across many unrelated products.

Fix your credit report before you apply. Pull your free reports from all three bureaus at AnnualCreditReport.com and dispute any errors. One in five consumer credit reports has a real error. Fixing one incorrect late payment can boost your score by 20 to 40 points in just one billing cycle.

Stack two or three of these together, and a borrower who would’ve been offered 14% APR often lands 9% instead. That’s the practical difference between “approved but expensive” and “approved and affordable.”

Frequently Asked Questions (FAQs)

Can I buy a camper with a 500 credit score?

Yes, but your options are very limited. Most traditional lenders require at least a 550 to 600 credit score, so a 500 score usually means working with specialty or dealer financing that charges much higher interest rates and often requires a large down payment.

What credit score is needed for RV financing?

Most RV lenders look for a FICO score between 660 and 680 for standard approval. Borrowers with scores above 720 usually qualify for the best rates, while some specialty lenders accept scores as low as 550 with stricter loan terms.

How much of a down payment do I need to buy an RV?

A 10% to 20% down payment is common for borrowers with good credit. Buyers with lower credit scores may need to put down 20% to 30% or more to improve their approval chances and reduce lender risk.

What is a good RV loan rate right now?

Borrowers with excellent credit can qualify for RV loan rates starting around 6.5%, while average rates are roughly 7.5% for new RVs. Lower credit scores can push rates above 20%, with some subprime loans reaching 35.99%.

How easy is it to qualify for a camper?

Camper loans are generally harder to qualify for than auto loans because lenders consider them discretionary purchases. Besides your credit score, they’ll also review your debt-to-income ratio, income stability, down payment, and the camper’s age and value.

What are the common RV loan mistakes to avoid?

Avoid accepting the first loan offer, skipping pre-qualification, or focusing only on monthly payments instead of total loan cost. Buying with poor credit without comparing lenders can add tens of thousands of dollars in extra interest.

What is the lowest credit score you can have to buy a camper?

Some specialty lenders may approve applicants with credit scores as low as 550, and a few dealer programs may go lower for small loan amounts. Below 550, traditional camper financing is rarely available.

Is it financially smart to buy an RV?

Buying an RV is most affordable when you qualify for a low interest rate and can comfortably manage the payments. Improving your credit score before applying can save thousands of dollars over the life of a long-term RV loan.

Why is the 10-year RV rule?

Many lenders apply stricter financing standards to RVs that are more than 10 years old because older campers depreciate faster and are harder to resell. As a result, borrowers may need higher credit scores or larger down payments for older units.

Does applying with multiple RV lenders hurt your credit score?

Multiple RV loan applications made within 14 to 45 days are typically treated as a single hard inquiry for credit scoring purposes. Shopping several lenders during that window helps you compare rates with little impact on your credit.

Wrapping Up

Buying a camper is a big decision, and your credit score shapes almost every part of it, from approval odds to APR to down payment size. The typical score for camper financing is about 660. Buyers with scores over 720 get the best rates. Specialty options start around 550 but come with tradeoffs. Because RV loans cost more and stretch longer than auto loans, even small score improvements pay back in a big way over the loan’s life.

For most buyers, the best step is to pull your report. Fix any errors. Then, get a soft-pull pre-qualification. Only after that should you start negotiating on a specific camper.

If you know someone ready to buy their first RV or travel trailer, share this guide. It could save them thousands in interest and help them avoid bad subprime deals.