You’re about to tap “Borrow” or “Pay in 4,” and a small voice asks, “Wait, will this show up on my credit report?” That worry is fair. Cash App wears many hats now, and each one plays by different rules. So we wrote this guide to give you a clear answer for every part of Cash App that could affect your credit score, without the guesswork.

Basic Cash App use does not affect your credit score, but borrowing features can, if payments go unpaid.

Below, we walk you through each feature, what it reports, when it hurts, and how to protect yourself before a problem shows up on your credit file.

Key Takeaways

This guide explains whether Cash App affects your credit score, covering everyday transfers, Cash App Borrow, Afterpay, the Cash App Card, and overdrafts, along with the 30-day threshold that can trigger collections reporting and score damage.

Core Facts:

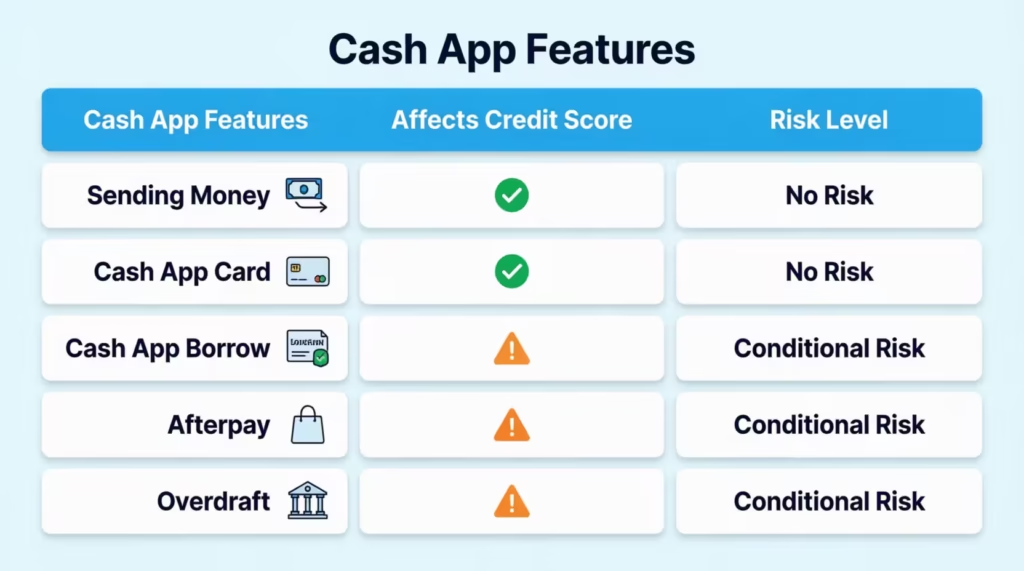

- Regular Cash App activity, including transfers, direct deposits, and using the Cash App Card, is never reported to Equifax, Experian, or TransUnion and does not affect your credit score.

- Cash App Borrow does not report on-time payments, but an unpaid balance can be sent to collections and reported once it passes roughly the 30-day delinquency mark.

- Afterpay Pay-in-4 purchases do not currently report on-time payments to U.S. credit bureaus, but a defaulted balance sent to collections can appear on your credit report.

- Cash App does not run a hard credit inquiry for Borrow applications; it uses a soft check based on account activity, which does not affect your credit score.

- A negative Cash App balance from overdraft is not automatically reported to credit bureaus, but it can affect your credit if left unpaid and sent to a collections agency.

- Collection accounts from Cash App debt can remain on a credit report for up to seven years from the original missed payment date, the same as any other collection.

Best for:

- Cash App users deciding whether to use Borrow, Afterpay, or overdraft and wanting to understand the credit risk before opting in.

- Anyone who missed a Cash App Borrow or Afterpay payment and wants to know the timeline before it becomes a credit issue.

- Readers who already have a Cash App related collection entry and want to understand how it behaves on their credit report.

Does using Cash App normally affect your credit score

Regular Cash App activity does not touch your credit score. Sending money to a friend is not reported to any credit bureau. Getting your paycheck by direct deposit doesn’t get reported either. Splitting a dinner bill or paying your roommate rent through Cash App also isn’t reported. None of that activity shows up on your credit report at Equifax, Experian, or TransUnion.

Here is why. Credit bureaus only receive data about credit accounts, meaning loans, credit cards, and other lines of borrowing. A peer-to-peer payment app is not a lender. When you send $40 to a friend, no one is loaning you anything. There is no account to report, no balance owed, and no payment history to track.

Your Cash App balance is also not a credit account. It behaves more like a digital wallet or a checking balance. Because you are moving your own money, credit reporting agencies never see it.

That means someone can use Cash App for years without ever affecting their credit score, in either direction. Sending, receiving, direct depositing, or holding money in Cash App will not help you build credit, and it will not hurt you. Only certain Cash App features that involve actual borrowing can change that, and we cover each of those next.

Does Cash App Borrow affect your credit score?

Cash App Borrow is where the credit picture starts to change. Borrow is a small short-term loan, usually between $20 and $200, that you repay in about four weeks. Unlike a peer-to-peer transfer, Borrow is real credit. That means it can affect your credit score, but only in specific situations.

Cash App Borrow does not report positive activity to the credit bureaus. Paying it back on time will not help you build credit. What it can do is hurt your credit if you fall behind. If a Borrow balance goes unpaid, Cash App may report the delinquency to the major credit bureaus or hand the debt to a collections agency, and that entry can lower your score.

This makes Cash App Borrow very different from a cash advance app that never reports anything. It is also different from a traditional personal loan, which usually reports both good and bad behavior. Borrow only reports the bad, so you get downside risk without the upside of building credit history.

The math also matters. Because Borrow is such a small-dollar loan, many users assume it is too small to affect credit. That is a mistake. A collections entry as small as $50 can appear on your credit file and pull your score down. What triggers reporting is the missed payment, not the size of the loan.

Does Cash App run a credit check for Borrow?

Cash App does not run a hard credit inquiry when you apply for Borrow. That is one of the reasons the product is popular with users who have thin or subprime credit files. In fact, Block has publicly shared that more than 70% of active Cash App Borrow customers have FICO scores below 580, yet they maintain a 97% repayment rate, according to the Cash App Score pilot announcement.

Instead of a hard pull, Cash App checks your account behavior. It looks at things like how often you receive direct deposits, how you use your balance, and your repayment history inside the app. This is a soft check, not a credit bureau inquiry, so it will not appear on your credit report and will not shave points off your score.

The difference between hard and soft inquiries is worth knowing. A hard inquiry happens when a lender pulls your file to make a lending decision, like when you apply for a credit card or car loan.

It can drop your score by a few points and stays on your report for up to two years. A soft inquiry does not affect your score at all and is often invisible to other lenders. Cash App’s Borrow check falls into that soft category.

💡 Pro Tip: Even though there is no hard pull to apply for Borrow, the loan itself is still real debt. Treat it like any other short-term loan and pay it back on time to avoid the reporting risk.

What happens if you miss a Cash App Borrow payment

Missing a Borrow payment follows a predictable timeline, and knowing it can save your credit score.

On the due date, if the money is not there, Cash App tries to pull the funds from your linked balance or debit card. If that fails, a late fee is added. Your account is now past due, but nothing has been reported yet.

Between day 1 and roughly day 30, Cash App will keep trying to collect and may pause your ability to use Borrow again. Your credit is still safe during this window in most cases, but the clock is ticking.

Once you cross the 30-day mark, the risk jumps sharply. Delinquencies of 30 days or more are the industry-standard threshold for credit bureau reporting. At this point, Cash App may send the debt to a third-party collections agency. This agency can then report the collection to the credit bureaus: Equifax, Experian, and TransUnion.

A new collection entry on your credit report is one of the most damaging items possible. Payment history makes up about 35% of your FICO Score, the single largest factor, as myFICO explains in its credit score breakdown. A fresh collection can drop a healthy score by 50 to 100 points, and even more if your file is thin. On top of that, you will lose access to Cash App Borrow in the future.

Does Cash App Afterpay affect your credit score?

Cash App Afterpay is the Buy Now, Pay Later feature built into Cash App. It lets you split purchases into four interest-free payments. Because Afterpay is now owned by Block, the same company that owns Cash App, the two products are tightly linked. But the credit rules for Afterpay are still their own.

For standard Afterpay Pay-in-4 purchases in the U.S., on-time payments do not affect your credit score in either direction. Afterpay confirms on its help page that Pay-in-4 payments do not impact your credit score. It also specifies that it currently does not report Pay-in-4 activity to U.S. credit bureaus, as noted in the Afterpay credit check FAQ. Afterpay may run a soft check when you sign up or make a purchase, but that soft check is invisible to lenders and does not change your score.

Defaults, however, are treated differently. If you stop paying an Afterpay balance, the account can be closed, sent to collections, and reported. When a collections agency takes on your debt, a public collection entry shows up on your credit file. This can lower your score, just like any unpaid debt.

The bigger shift is coming from the credit scoring industry itself. FICO has now built new scoring models designed to include BNPL data. According to the official FICO announcement about FICO Score 10 BNPL, FICO Score 10 BNPL and FICO Score 10 T BNPL became available in the fall of 2025, alongside the standard versions. Experian has also launched a specialty BNPL bureau, described on the Experian Buy Now Pay Later solutions page, which gives lenders visibility into BNPL activity without adding it to traditional credit reports for most consumers yet.

For now, if you use Afterpay through Cash App and pay on time, your traditional score is not affected. But the industry is moving toward including BNPL data more broadly, so long-term you should not assume BNPL will stay invisible forever.

📌 Did You Know: Cash App Afterpay Pay-in-4 doesn’t report on-time payments now, but a default can still appear on your credit report if it goes to collections. The “no reporting” rule protects good behavior, not missed payments.

Does the Cash App Card affect your credit score?

The Cash App Card is a prepaid debit card, not a credit card. It draws from your Cash App balance, which is your own money. Because you are not borrowing anything to use it, the Cash App Card does not affect your credit score.

Cash App does not run a credit check when you order the card, does not open a credit line for you, and does not report the card to Equifax, Experian, or TransUnion. There is no monthly payment to make and no balance for a lender to review.

This is very different from a secured credit card, which is often confused with a prepaid card. A secured card looks similar because you fund it with your own money as a deposit, but it is still a real credit account. Secured cards report to the bureaus every month and can help build credit history over time. The Cash App Card does not do this.

If your goal is to build credit, the Cash App Card is not the right tool. It is a convenient way to spend the money already in your Cash App balance, nothing more. To build credit, you would need a product designed for that purpose, such as a secured credit card or a credit-builder loan from a bank or credit union.

Does overdrawing Cash App affect your credit score

Cash App now offers a small overdraft feature for eligible users with direct deposit. If a purchase pushes your balance below zero, the app can temporarily cover the shortfall. This raises a real question, because bank overdrafts do sometimes lead to credit damage.

For Cash App specifically, a negative balance by itself is not reported to the credit bureaus. It is treated as a short-term shortfall on the app, not as a debt on your credit file. There is no immediate credit score impact when your account first dips below zero.

What can happen instead is a fee, plus a deadline. Cash App expects the negative balance to be cleared quickly, usually with your next direct deposit or a manual reload. If it is not, the app may pause certain features, block your Borrow eligibility, and eventually escalate the shortfall.

The risk to your credit begins if that unpaid negative balance is treated as debt and sent to a collections agency. Once a collector holds the account, they can report it to the credit bureaus, and that entry can drop your score in the same way a missed loan payment would.

To stay safe, treat any overdraft as urgent. Reload your balance or receive your next paycheck as soon as possible. Overdrafts that are cleared within a few days rarely lead to credit issues.

What happens if you owe Cash App money

“Owing Cash App money” can mean three very different things, and each one has its own credit outcome. Sorting out which situation you are in is the first step.

Scenario 1: You owe on Cash App Borrow. This is a real loan. If it goes unpaid past about 30 days, Cash App can send it to collections and the debt can be reported. Your credit score can drop.

Scenario 2: You owe on Cash App Afterpay. Missed installments start with late notices and account holds. If the balance is written off and sent to collections, that collection entry can appear on your credit report and lower your score.

Scenario 3: You owe due to a negative Cash App balance. This is usually an overdraft. It is not automatically reported. It only becomes a credit issue if it is escalated to a third-party collector.

In every case, Cash App usually starts with in-app reminders and notifications. If you keep ignoring them, the account can be closed, and the debt handed off to a collections partner. From that point, the collections agency, not Cash App, decides whether to report the debt to Equifax, Experian, and TransUnion.

If you are behind on any Cash App product, the safest move is to log into the app, check the exact balance, and pay it down before the 30-day mark. That single step prevents the vast majority of Cash App credit damage.

Is Cash App debt treated the same as other unpaid debt on your credit report

Yes. Once a Cash App debt is on your credit report through a collections agency, it behaves like any other collection account. There is no special leniency because it started inside a payment app.

Collection accounts can stay on your credit report for up to seven years from the date of the original missed payment. Paying off a collection does not automatically erase it, though some newer scoring models weigh paid collections less heavily.

A $75 unpaid Borrow balance from Cash App can stay on your credit report for years. This means any future lender, landlord, or utility company can see it. Small debts have long shadows once they hit collections.

Does repaying Cash App on time help your credit score

This is one of the most common myths around Cash App, and the honest answer is no. Paying Cash App Borrow or Afterpay on time does not directly build your credit score. Cash App does not report positive payment history to Equifax, Experian, or TransUnion.

The reason is mechanical, not personal. Credit scores are built from data that lenders send to the credit bureaus. Traditional credit cards, auto loans, mortgages, and student loans all report monthly payment activity, both good and bad. Cash App does not currently send monthly on-time reports for Borrow or Afterpay in the same way.

That is why users who “responsibly use Cash App” for years often see no change in their credit score. There is nothing wrong with their behavior. There is simply no data flow feeding it into the credit bureaus. Good behavior that never gets reported cannot help your score.

This is a key difference between Cash App and true credit-builder products. A credit-builder loan or secured credit card reports on-time payments to at least one bureau. This helps build a positive payment history, which is the biggest factor in your FICO Score.

⚠️ Mistake to Avoid: Do not rely on Cash App as your credit-building tool. Users often assume that “using it responsibly for a year” will lift their score. It will not, because on-time Cash App payments are not reported to the credit bureaus.

Can Cash App build your credit at all

Cash App, as it works today, cannot build your credit on its own. The mechanism just is not there. To build credit, you need an account that reports on-time payments to at least one of the three major credit bureaus every month. Cash App does not do that for Borrow, Afterpay, or the Cash App Card.

If your goal is to build credit from scratch or repair a thin file, better tools exist:

- A secured credit card requires a refundable deposit but reports to all three bureaus monthly. This is the fastest and most reliable way to establish credit history.

- A credit-builder loan from a credit union or online lender holds the loan amount in a savings account while you make monthly payments. Every payment gets reported.

- Becoming an authorized user on a family member’s well-managed credit card can also import positive history onto your file.

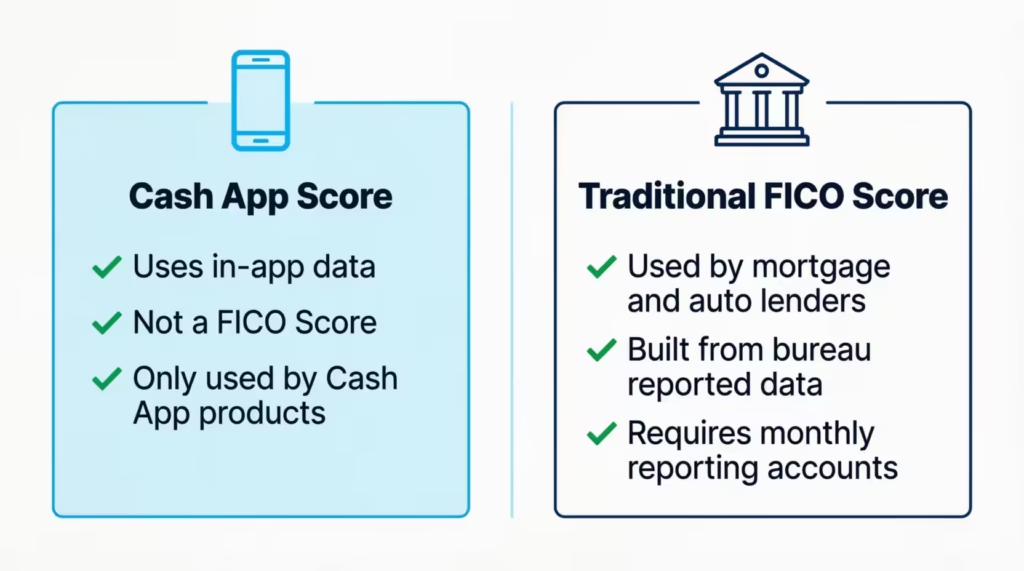

Cash App is now piloting its own separate score, called the Cash App Score, which uses first-party data like paycheck deposits and repayment behavior. It is not a FICO Score and is not currently used by outside lenders, so it will not help you qualify for a mortgage or auto loan today. It is a tool for Cash App-owned products only.

Set your expectations here. If you want a higher FICO Score in six months, Cash App is not the path. Combining a small secured card with on-time bill payments will move the needle much faster.

How to protect your credit score while using Cash App

You can use Cash App confidently without hurting your credit if you follow a few clear rules. Each one is tied to a specific risk we walked through above.

Pay any Borrow or Afterpay balance well before 30 days late. The 30-day mark is the industry standard trigger for collections and credit reporting. If you keep every payment within that window, the risk of a credit hit drops to nearly zero.

Avoid stacking multiple balances. If you have an open Borrow loan, an active Afterpay plan, and a negative Cash App balance, you increase the risk of missing a payment. Handle one obligation at a time.

Keep your Cash App balance positive, or reload fast. If you use the overdraft feature, treat the negative balance like a bill due today. Reload from your bank or wait for your direct deposit and clear it immediately.

Turn on payment reminders and low-balance alerts inside the Cash App settings. Most missed payments happen simply because someone forgot the due date, not because they could not pay.

Check your credit report at least once a year. You can pull all three reports for free at AnnualCreditReport.com, the official site authorized under federal law. Look for any collection entries you do not recognize, especially small dollar amounts, which are a sign of a forgotten Cash App or BNPL balance.

Following these five habits keeps Cash App in its safe lane, useful for payments and small credit needs, without ever creating a surprise on your credit file.

What to do if Cash App already affected your credit

If a collection entry from a Cash App debt is already sitting on your credit report, you still have real options. Recovery is possible, and the sooner you start, the faster your score can bounce back.

Step 1: Confirm the entry. Pull your three credit reports at AnnualCreditReport.com and locate the exact account. Note the original creditor, the collections agency, the amount, and the date the account went delinquent. You need these details before contacting anyone.

Step 2: Pay or settle the outstanding balance. If the debt is truly yours, paying it off stops further damage and, under many newer FICO and VantageScore models, reduces the score impact of the collection. In some cases you can negotiate a “pay for delete” with the collections agency, where they remove the entry in exchange for payment. Get any agreement in writing before you pay.

Step 3: Dispute inaccurate entries. If any detail is wrong, the amount, the date, or you do not recognize the debt at all, you have the right under the FCRA to dispute it. File the dispute with both the credit bureau and the company that furnished the information. The bureau generally has 30 days to investigate.

Step 4: Rebuild deliberately. Once the collection is handled, focus on adding positive data. Open a secured credit card, keep utilization under 30%, and pay every bill on time. Payment history is 35% of your FICO Score, so a clean stretch of on-time payments does more to lift your score than almost anything else.

Step 5: Monitor progress. Free monitoring tools from Experian, Credit Karma, or your existing bank can flag any new activity. Watch your score every month. Many people notice real improvement within six to twelve months after paying off collections and adding new positive accounts.

A single Cash App collection does not have to define your credit for seven years. Handling it directly, disputing anything inaccurate, and adding real credit-building accounts on top will move you forward.

Frequently Asked Questions (FAQs)

Can Cash App mess with your credit score?

Yes, but only through Cash App Borrow or Afterpay. Missing payments for 30 days or more can send the debt to collections, which drops your score, while normal transfers never touch it.

Does Cash App show up on credit reports?

Regular transfers, deposits, and card use never appear on your credit report. A Borrow or Afterpay debt only shows up if it becomes a collections account after 30 days unpaid.

What is the biggest killer of credit scores?

Payment history is the single largest factor, making up about 35% of your FICO Score. A new collections entry, even from a small Cash App debt, can drop a healthy score by 50 to 100 points.

Is it possible to be in debt on Cash App?

Yes, through an unpaid Borrow loan, a defaulted Afterpay balance, or an uncleared negative balance from overdraft. Any of these can become real debt if ignored past 30 days.

Does owning Cash App affect your credit?

Simply having a Cash App account does not affect your credit score at all. Only borrowing features like Cash App Borrow or Afterpay carry any credit risk, and only when payments are missed.

Does Cash App go on your credit report?

Cash App itself does not report to Equifax, Experian, or TransUnion for on-time payments. A collections agency can report an unpaid Borrow or Afterpay balance if it goes 30 days or more without payment.

What is the downside to using Cash App?

The main downside is that Cash App Borrow and Afterpay only report missed payments, not on-time ones. This means you get the risk of credit damage without any credit-building benefit for responsible use.

How fast can I build my credit from a 500 to a 700?

The article does not give a timeline for raising a score from 500 to 700. It does note that a secured credit card or credit-builder loan reports monthly, which is a faster path than relying on Cash App.

Why shouldn’t you use Cash App?

Cash App is safe for everyday transfers, deposits, and card use, so there is no credit reason to avoid it for those. The real caution is treating Borrow or Afterpay balances casually, since unpaid debt past 30 days can lead to a damaging collections entry.

Wrapping Up

Cash App itself is safe for your credit for the everyday stuff: sending money, receiving deposits, and using the Cash App Card. The credit risk only appears with Cash App Borrow, Afterpay defaults, and unpaid overdrafts, and only after 30 days of delinquency. Good behavior does not build your score, but bad behavior can absolutely hurt it

To improve your credit, treat any Borrow or Afterpay balance like a real bill. Pay it within 30 days. Also, use a secured card to help build your credit.

If you know someone using Cash App Borrow or Afterpay for the first time, share this guide; one clear read now could save their credit score later.