I get it. You’ve decided you’re done with your Discover card, and now you just want a clear, no-nonsense way to close it without losing your rewards or tanking your credit score. Maybe the Capital One merger has you rethinking things, or you’re just simplifying your wallet. Either way, figuring out how to cancel a Discover credit card isn’t as obvious as it should be, especially since Discover doesn’t offer an online closure option.

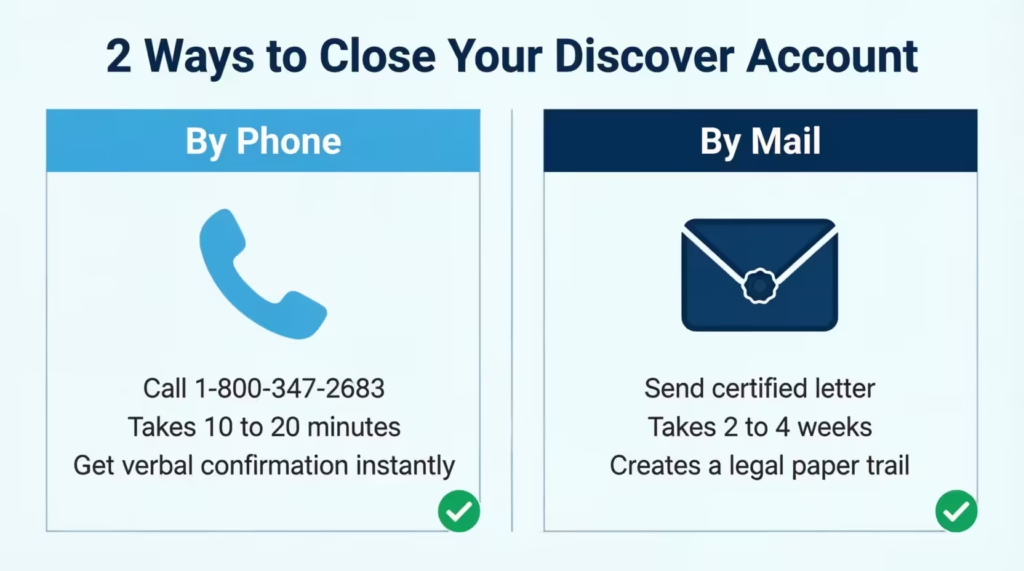

Here’s the short answer: you can only close a Discover card by calling 1-800-347-2683 or by sending a certified letter.

Below, I’ll walk you through every step, from the prep work that protects your credit score to what Discover’s retention team will say when they try to talk you out of it.

Key Takeaways

This guide explains how to cancel a Discover credit card, including the available cancellation methods, steps to protect your credit score and rewards, how account closure affects credit utilization and account age, and how to verify the account was closed correctly.

Core Facts:

- Discover does not offer online or mobile app account closure; cardholders must cancel by phone at 1-800-347-2683 or by sending a signed written request by mail.

- Before canceling a Discover card, redeem all Cashback Bonus rewards, move recurring charges, notify authorized users, and download important account statements.

- Closing a Discover account with a remaining balance is allowed, but interest continues to accrue and monthly payments remain required until the balance reaches zero.

- Credit utilization can increase immediately after closure because the card’s available credit is removed from your total credit limit calculation.

- A closed Discover account in good standing typically remains on a credit report for about 10 years and continues contributing to account age during that period.

- After cancellation, verify that credit reports show the account status as “closed at consumer’s request” and confirm the reported balance is $0.

Best for:

- People considering whether to cancel a Discover credit card and wanting to understand the potential credit score impact before making a decision.

- Cardholders preparing to close a Discover account while protecting rewards, avoiding missed recurring payments, and maintaining accurate records.

- Consumers who recently canceled a Discover card and need to verify proper account closure and credit report reporting.

Can You Cancel Your Discover Card Online?

No, you can’t cancel your Discover credit card online or through the mobile app. This surprises a lot of cardholders. You can do nearly everything else with your Discover account. You can pay bills, redeem Cashback Bonus, or freeze your card. But you can’t close the account this way.

Discover requires you to speak with a representative or send a written request. There are only two valid ways to close a Discover credit card account:

- By phone: Call 1-800-DISCOVER (1-800-347-2683). This number is printed on the back of your card and listed on Discover’s contact page.

- By mail: Send a signed letter to Discover’s customer service address, ideally as certified mail with a return receipt.

The phone option is faster. Most calls take 10 to 20 minutes, and you get verbal confirmation on the spot. The mail option creates a paper trail, which some people prefer for legal or record-keeping reasons. There’s no email form, no chat option, and no button hidden deep in account settings. If a website tells you otherwise, it’s outdated.

📌 Did You Know: Discover keeps phone-only cancellation on purpose. It gives their retention team one final chance to offer you a statement credit, a lower APR, or a product change before you close the account. Knowing this in advance helps you stay calm during the call.

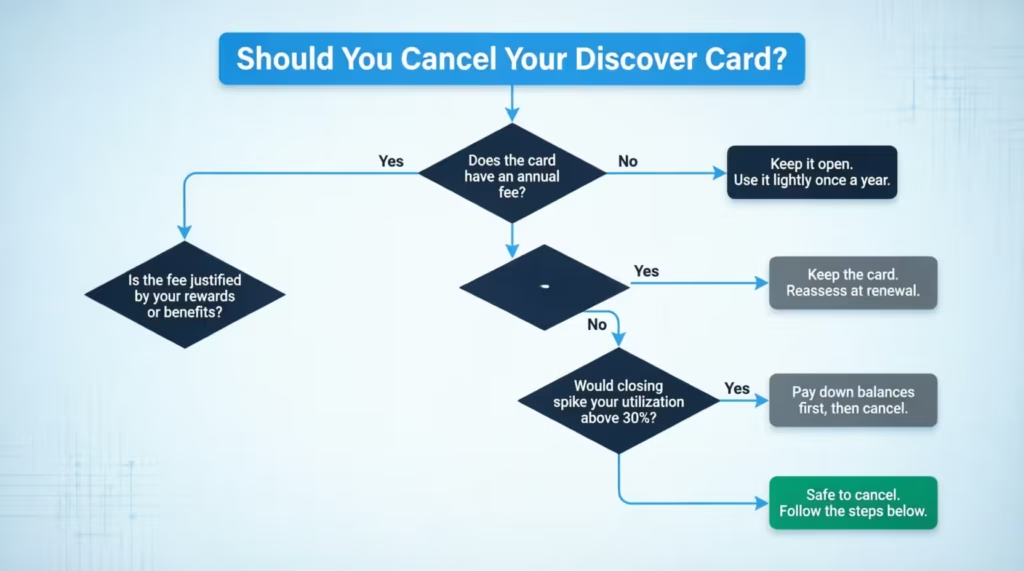

Should You Cancel Your Discover Card? A Decision Framework

Before you pick up the phone, take a minute to make sure closing the card is actually the right move. Some situations clearly call for cancellation. Others don’t, and closing the wrong account can quietly damage your credit profile for years.

Cancel the card when:

- You’re splitting finances after a divorce or ending a joint account, and keeping it open creates legal or financial risk.

- The card has a high annual fee that no longer matches how you use it.

- You’re struggling with overspending, and removing the temptation matters more than the credit score impact.

- You’re consolidating to a different rewards setup that better fits your spending.

- Fraud or repeated security issues have made the account a headache.

Keep the card when:

- It has no annual fee. There’s almost no downside to letting it sit.

- It’s your oldest credit account. Closing it can shorten your average age of accounts, which makes up 15% of your FICO score.

- Your credit utilization ratio would jump above 30% on your remaining cards after closure.

- You plan to apply for a mortgage, auto loan, or new card in the next 6 to 12 months.

The general rule: if there’s no annual fee and no behavioral reason to cut the card up, keeping it open and using it lightly once or twice a year is almost always the safer choice.

When Keeping Your Discover Card Is the Smarter Move

Think of Jennifer, a marketing manager in her early 30s who’s had her Discover it Cash Back card for seven years. It’s her oldest credit line, and it has no annual fee. She rarely uses it, but it gives her a $6,000 credit limit on top of her newer Chase and Capital One cards.

If she closes it, her total available credit drops, her utilization ratio climbs, and the clock starts ticking on her average account age (closed accounts in good standing stay on your report for about 10 years, but the protective effect fades).

For someone in Jennifer’s spot, a smarter move is to set one small recurring charge on the card, like a $9.99 streaming subscription, and pay it off automatically each month. The account stays active, her credit profile stays strong, and she avoids the headache of cancellation entirely.

If you mostly want the card “out of your face,” ask Discover to lower the credit limit, remove it from your digital wallet, or freeze it through the app. You get the behavioral benefit without the credit score risk.

What the Capital One Merger Means for Your Discover Account

Capital One officially completed its acquisition of Discover on May 18, 2025, forming the sixth-largest bank in the United States. If you’re wondering whether the merger changes anything for your current account, here’s the honest answer: not much, at least not yet.

For now, your Discover card works the same way. Your account number, rewards program, Cashback Bonus structure, APR, credit limit, and customer service phone numbers all stay the same. You’ll still log in through Discover.com and use the Discover mobile app. According to Capital One’s official Discover FAQ page, customers “shouldn’t expect any immediate changes” to their accounts.

The migration of Discover credit card accounts onto Capital One’s systems is expected to begin in the second half of 2026 and continue into later phases. Debit card migration is already underway. When credit card migration happens, Capital One has said it will notify customers well in advance.

So, should the merger change your decision to cancel? Probably not on its own. If you liked your Discover card before the merger, the product itself hasn’t changed. If you didn’t, the merger doesn’t fix the reasons you wanted to leave. Make the decision based on the card, not the corporate news.

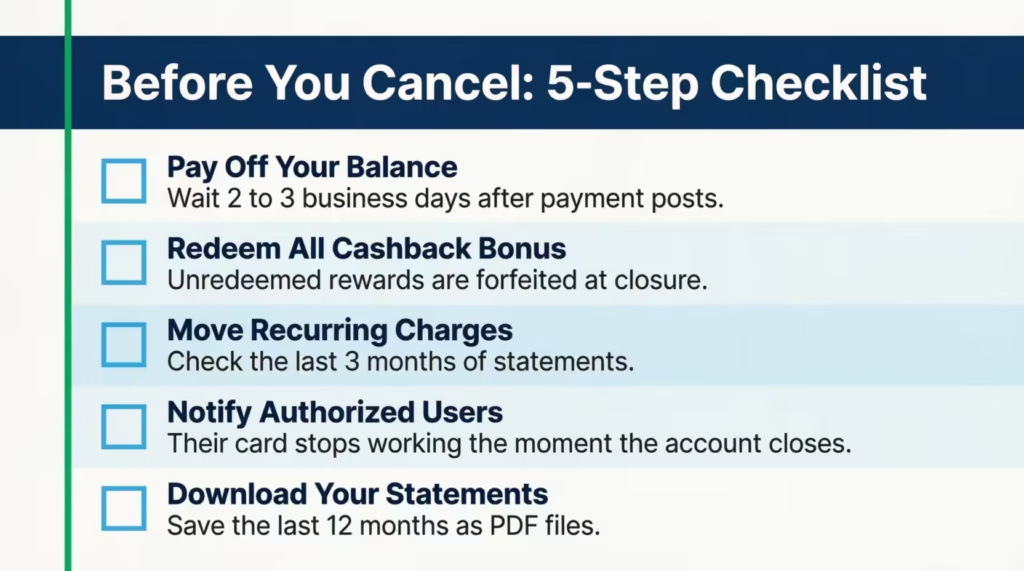

What to Do Before You Call Discover

This is the part most articles skim over, and it’s the part that protects your money. Once your account closes, certain things become much harder or impossible to recover. Work through this checklist in order before you pick up the phone.

Pay Off Your Balance Before You Cancel

Aim to close the card with a zero balance. While Discover does allow you to close an account with a remaining balance, doing so creates avoidable friction. Interest still accrues. You still have to make monthly payments. And a “closed” card with a balance can look messier on your credit report than a paid-off, open one.

The best way is to wait until your statement closes. Then, pay the full balance. After that, wait 2 to 3 business days for the payment to post before calling. This way, the representative confirms a $0 balance on the call itself.

What to Do If You Can’t Pay the Full Balance First

Life happens. If you carry a balance you can’t pay off right now, you still have good options:

- Close the account anyway. Discover will keep sending you monthly statements until the balance hits zero. Your APR stays the same, but you can no longer make new purchases. This stops further spending while you pay it down.

- Transfer the balance to a 0% APR card. If your credit is strong, a balance transfer card with a long 0% intro period can save hundreds in interest. Just account for the typical 3% to 5% balance transfer fee.

- Set up an aggressive payoff plan first, then cancel. Pay it down over 2 to 6 months, then close once it hits zero.

⚠️ Mistake to Avoid: Don’t close the account and then forget about the remaining balance. Missed payments on a closed Discover account hurt your credit score just as much as missed payments on an active one, and the account stays open in the credit reporting sense until the debt is fully paid.

Redeem Your Cashback Bonus

This is the single biggest avoidable loss when cardholders cancel. Any unredeemed Cashback Bonus is forfeited when your account closes. There’s no grace period, no mailed check, no “we’ll send you a final statement with your balance.” It’s gone.

Log in to your Discover account, go to the rewards section, and redeem every dollar. You can:

- Get it as a statement credit (fastest and simplest)

- Deposit it into a linked checking or savings account

- Use it at checkout with Amazon or PayPal

- Convert it to a gift card (some categories offer a small bonus)

Even if you have just $4 or $5 sitting there, redeem it. After cancellation, it’s not recoverable.

Move Your Recurring Charges to Another Card

This step saves more headaches than any other. Make a list of every subscription or autopay tied to your Discover card. Common ones include:

- Streaming services (Netflix, Spotify, Disney+, Hulu)

- Utility bills (electric, gas, internet)

- Insurance premiums (auto, renters, life)

- Gym or fitness app memberships

- Cloud storage (iCloud, Google One, Dropbox)

- Phone bill or wireless plan

- Software subscriptions (Adobe, Microsoft 365)

Pull up your last 3 statements and scan every recurring charge. Update the payment method on each provider’s website before you cancel, not after. Once the card closes, those payments fail. A missed utility or insurance payment can lead to late fees, service interruptions, or even policy cancellation.

💡 Pro Tip: Don’t trust your memory. Look at the last 3 months of statements together, because some charges (like annual subscriptions for AAA, antivirus software, or domain renewals) bill only once a year and won’t show up in a single month.

Notify Authorized Users

If you’ve added a spouse, partner, child, or family member as an authorized user on the card, give them a heads-up before you cancel. Their card stops working the moment the account closes, even if they don’t know it. This avoids embarrassing declined-card moments at checkout.

Closing the account also removes the Discover tradeline from the authorized user’s credit report. For a young adult building credit through a parent’s account, this can briefly affect their credit profile. It’s not always a reason to keep the account open, but it’s worth a quick conversation.

Download Your Statements

Once the account closes, you can usually still access your transaction history online for about 7 years. But access policies can change, especially during the Capital One migration. To be safe, download your last 12 months of statements (or more if you’re self-employed and need records for taxes). Save them as PDFs in a folder on your computer or in cloud storage.

You’ll thank yourself the next time tax season comes around and you need to verify a deductible business purchase.

How to Cancel Your Discover Card by Phone (Step-by-Step)

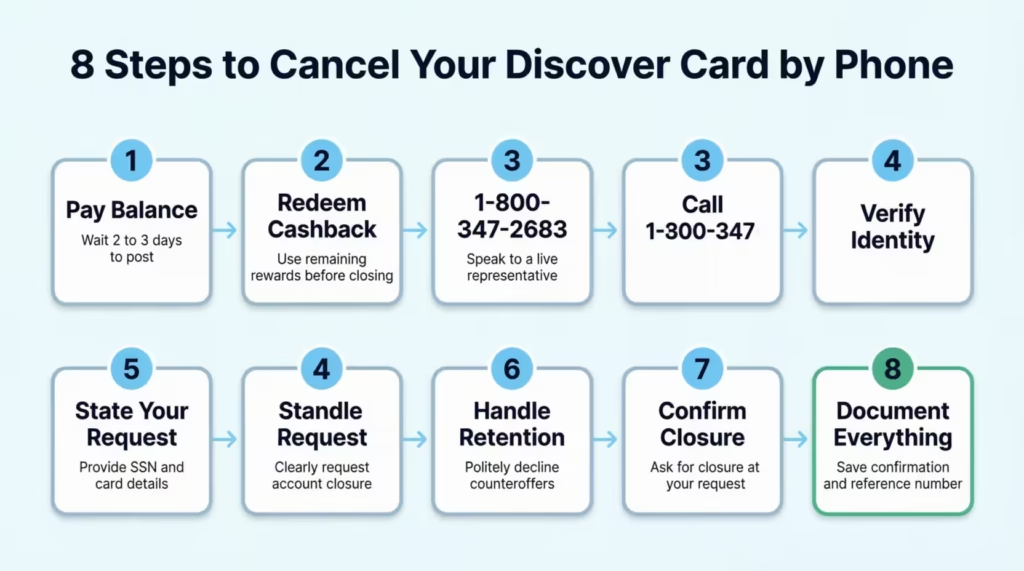

Calling is the fastest path. Plan for a 15-minute call. Here’s exactly how it goes:

- Pay off your balance first and wait 2 to 3 business days for the payment to post fully.

- Redeem all Cashback Bonus and confirm the balance is zero in your rewards center.

- Call 1-800-DISCOVER (1-800-347-2683). This is the main customer service line and handles closure requests.

- Verify your identity. You’ll be asked for the card number, your full name, date of birth, and possibly the last four of your Social Security number. Have these ready.

- State your request clearly. Say something direct like, “I’d like to close my Discover credit card account permanently.”

- Handle the retention offers calmly. The representative will almost certainly try to keep you (more on this below). You can listen politely and still say no.

- Confirm the closure. Ask the representative to confirm out loud that the account is now closed and that the closure reason is recorded as “at customer’s request” or “at consumer’s request.” This phrasing matters for your credit report.

- Document everything. Write down the date, time, the representative’s name or employee ID, and any confirmation number they provide. Keep this somewhere safe for at least 12 months.

After the call, you’ll typically receive a written confirmation by mail within 7 to 10 business days. If it doesn’t arrive within 2 weeks, call back and request it.

What Discover’s Retention Team Will Say and How to Respond

Discover trains its retention team well. They are not aggressive, but they are persistent. Here’s what to expect:

“Can I ask why you’re closing the account today?” A short, honest answer is fine. “I’m simplifying my wallet” or “I’m switching to a different rewards card” works. You don’t owe a long explanation.

“What if I could waive the annual fee for the next year?” If your card has an annual fee and the fee is the only reason you’re leaving, take it. If you’ve decided to leave for other reasons, politely decline.

“How about a statement credit or a lower APR?” These offers are real and sometimes substantial ($50 to $200 statement credits aren’t unusual). Take them if they change your math. Decline if they don’t.

“Would you consider downgrading instead of closing?” A product change to a no-annual-fee card lets you keep the account open and protect your credit history without paying a fee. This is genuinely worth considering if your main concern is the fee.

“Are you sure? This account has been open for X years.” They’re not guilting you. They’re flagging a real credit score consideration. If your decision is firm, just say, “Yes, please close it.”

The polite, firm phrase that ends the conversation: “I understand, but I’d like to go ahead and close the account today.” Repeat it as needed.

How to Cancel Your Discover Card by Mail

If you want a paper trail or you’d rather avoid the retention conversation, mailing a written request works. It takes longer (plan for 2 to 4 weeks), but it’s just as valid.

Write a short letter that includes:

- Your full name as it appears on the card

- Your full Discover account number

- Your mailing address and phone number

- The last four digits of your Social Security number (for identity verification)

- A clear statement: “I am requesting that you close this credit card account effective immediately at my request.”

- Your signature and the date

Send the letter as certified mail with a return receipt requested through USPS. This costs about $9 to $10 total, but it’s worth every penny. You get a stamped receipt proving the date you mailed it and a signed card proving Discover received it. If there’s ever a dispute about whether you actually requested closure, this is your proof.

Mail it to the customer service address on the back of your most recent statement. Then expect a written closure confirmation within 30 days. If you haven’t received confirmation by day 30, call 1-800-347-2683 to follow up.

Keep a copy of the letter, the certified mail receipt, and the return receipt card together in a folder. Save them for at least 12 months in case any billing or reporting issues come up later.

How Canceling Your Discover Card Affects Your Credit Score

This is where many cardholders get tripped up. Closing a credit card can lower your credit score, but the size of the drop depends on two specific FICO factors. According to FICO’s scoring breakdown, amounts owed (which includes credit utilization) make up 30% of your score, and length of credit history accounts for another 15%. Closing a card touches both.

The good news: a closed account in good standing stays on your credit report for about 10 years, so the history effect is slow to fade. The not-so-good news: your credit utilization can jump overnight.

How Closing a Discover Card Affects Your Credit Utilization

Your credit utilization ratio is the percentage of your total available credit that you’re currently using. Lower is better. Most credit experts suggest keeping it under 30%, and ideally under 10% if you’re optimizing your score.

Here’s the math that matters. Suppose you have:

- Discover card: $8,000 limit, $0 balance

- Chase card: $5,000 limit, $1,500 balance

- Capital One card: $4,000 limit, $500 balance

Total credit: $17,000. Total balance: $2,000. Utilization: about 12%. Healthy.

Now close the Discover card.

Total credit drops to $9,000. Total balance stays at $2,000. New utilization: about 22%. Still okay, but you’ve nearly doubled your ratio in one phone call.

If your other cards already carry higher balances, the jump can be much worse. A utilization spike from 15% to 45% can drop a FICO score by 20 to 40 points or more, often within a single billing cycle.

To soften the blow: pay down balances on your other cards before you close the Discover account. If you can get total balances near zero first, the utilization spike won’t matter much.

How Closing a Discover Card Affects Your Credit History Length

FICO looks at two things here: the age of your oldest account and the average age of all your accounts. Closing a credit card doesn’t immediately erase its history. The closed account keeps reporting for around 10 years, and it continues to count toward your average age during that time.

The real risk comes later. Once that closed account drops off your report (typically 10 years after closure), your average account age can drop sharply, and so can your score. This matters most if the Discover card is one of your oldest cards.

A simple check: log in to a free credit monitoring tool (Credit Karma, Experian, or your bank’s built-in score tracker) and look at the “age of oldest account” or “average account age” field. If your Discover card is the oldest, think twice before closing it. If it’s one of your newer cards, the long-term impact is small.

How to Verify Your Discover Account Is Fully Closed

Don’t assume “closed on the phone” means “closed on your credit report.” Verifying the closure protects you from billing surprises and reporting errors. Here’s how to confirm everything is wrapped up cleanly.

Within 7 to 14 days after canceling:

- Check that you’ve received a written closure confirmation from Discover. If not, call 1-800-347-2683 and request one.

- Try logging into your Discover account. You should still be able to view past statements, but the account should be marked as closed.

At 30 to 45 days after canceling:

- Pull a free copy of your credit report from AnnualCreditReport.com. This is the only federally authorized source for free credit reports from all three major credit reporting agencies (Equifax, Experian, and TransUnion). You’re entitled to a free report from each one every week.

- Find the Discover account on each report. The status should read “closed at consumer’s request” or “closed by consumer.” This wording matters. If it says “closed by creditor” or “closed by grantor” by mistake, that can signal something negative to future lenders, like the account was closed due to risk. Dispute the wording with the credit bureau immediately if you see this.

- Confirm the balance shows $0, and there are no surprise charges, fees, or interest.

At 60 days after canceling:

- Watch your bank and email for any final statement showing a $0 balance.

- Check that no recurring charges you thought you’d moved are still hitting the closed card. If any are, contact that merchant directly to update the payment method.

Final step: dispose of the physical card. Cut it through the chip, the magnetic stripe, and the account number, then split the pieces between two trash bags taken out on different days. For metal cards, send them back to Discover or take them to a secure shredding service. This protects you from dumpster-diving identity theft long after the account is closed.

When your credit report says “closed at consumer’s request” with a $0 balance, and there are no ongoing charges, plus you’ve destroyed the card, you’re finished. Truly done.

Frequently Asked Questions (FAQs)

How much will my credit score drop if I close a credit card?

The drop depends mostly on how much your credit utilization rises after losing that card’s available credit. A utilization spike from 15% to 45% can lower a FICO score by 20 to 40 points or more within a single billing cycle.

What is the biggest killer of credit scores?

A sudden spike in credit utilization is the fastest way to damage your score, since amounts owed make up 30% of your FICO score. Closing a card that carries a large credit limit can nearly double your utilization ratio overnight, even if your balances haven’t changed.

Will my Discover credit card close if I don’t use it?

Discover can close an inactive account at its discretion, though the timeline varies. Using the card for one small recurring charge each month, like a streaming subscription set to autopay, keeps the account active and protects your credit history without any effort.

What’s the best reason to cancel a credit card?

The clearest reasons to cancel are a high annual fee that no longer justifies itself, a joint account you need to sever after a divorce, or a card that’s driving overspending you can’t otherwise control. Cards with no annual fee are almost always worth keeping open, even if unused.

Is it better to cancel a credit card or let it cancel itself?

Letting the issuer close the account for inactivity is worse for your credit than canceling it yourself. When a creditor closes an account, it can appear on your credit report as “closed by grantor” rather than “closed at consumer’s request,” which signals risk to future lenders.

Can I close a credit card if it is all paid off without damaging my credit score?

Paying off the balance before closing is the right move, but it doesn’t eliminate the credit score impact. A zero balance protects you from ongoing interest, but your credit utilization ratio can still rise sharply the moment the card’s available credit is removed from your profile.

What happens if I cancel a credit card I never use?

The account’s available credit disappears from your profile immediately, which raises your credit utilization ratio and can lower your score. If the card is your oldest account, losing it will also eventually shorten your average credit history once it falls off your report in about 10 years.

What number is 1-800-347-2683?

That is Discover’s main customer service line, also written as 1-800-DISCOVER. It is the only phone number you can use to close a Discover credit card account, since Discover does not offer an online or in-app cancellation option.

Can I reopen a Discover card after closing it?

Discover does not reopen closed accounts. If you want a Discover card again after canceling, you would need to submit a new application, which means a hard inquiry on your credit report and no guarantee of approval or the same terms.

How does the Capital One merger affect canceling a Discover card?

The cancellation process is unchanged as of mid-2026. You still call 1-800-347-2683, your rewards and account terms remain the same, and Capital One has stated that credit card account migration onto its systems is not expected to begin until the second half of 2026 at the earliest.

Bottom Line

Closing a Discover card isn’t hard, but it does reward people who prepare. The best approach is to pay off the balance. Next, redeem every cent of Cashback. Move your recurring charges, then call 1-800-347-2683 with a clear plan.

FICO’s scoring weights show that a spike in utilization is the biggest risk. So, paying down other balances first can better protect your score than anything else. Verify the closure on your credit report at 30 days, dispose of the card securely, and you’re set.

If you know someone weighing whether to cancel a credit card, share this guide so they don’t lose rewards or hurt their credit by accident.