Many Discover cardholders reach a point where their current card no longer fits their needs. Maybe you’ve built your credit with a secured card and want your deposit back. Maybe you finished college and aren’t sure what happens next.

If you want to upgrade your Discover credit card, the process varies. Each cardholder follows one of three different paths.

This guide covers all three: what they are, how to request them, and exactly what to do if Discover says no.

Key Takeaways

This guide explains how to upgrade a Discover credit card through three separate paths: secured card graduation, student card transition, and product changes between consumer cards, including what each process involves, how Capital One’s acquisition changed the rules, and what to do if Discover says no.

Core Facts:

- Discover card upgrades follow one of three distinct paths: secured card graduation (deposit returned, account continues unsecured), student card transition (student label removed, account stays open), or a product change between the Discover it Cash Back and Discover it Miles cards.

- The automatic seven-month graduation review for secured cardholders was removed after Capital One completed its acquisition of Discover in May 2025; reviews now happen on an unannounced schedule.

- The Discover it Secured Credit Card stopped accepting new applications in June 2026, but existing cardholders are not affected and the graduation path remains available to them.

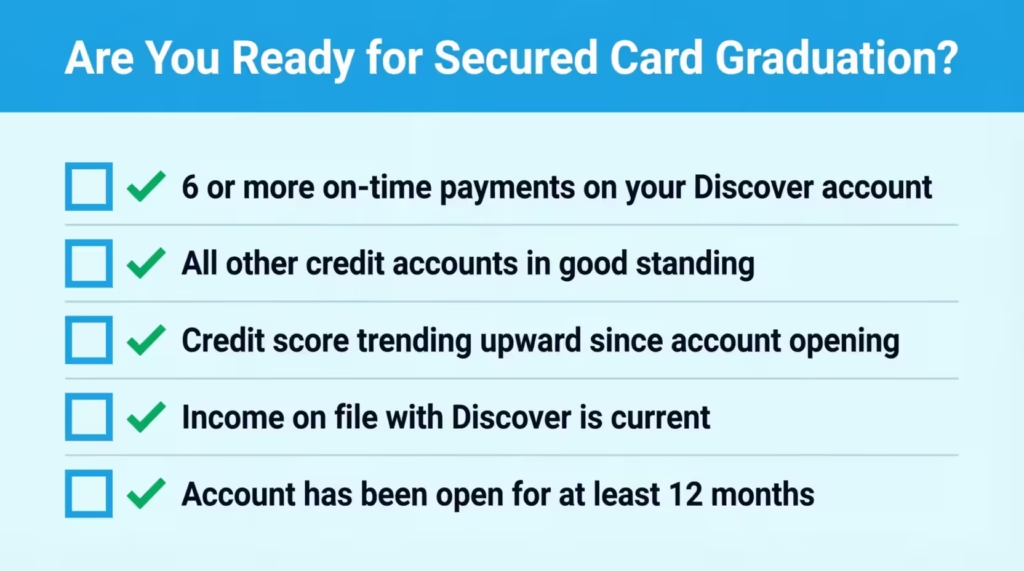

- The most important graduation signal is six or more consecutive on-time payments on the Discover account, combined with good standing across all other credit accounts and an up-to-date income figure on file with Discover.

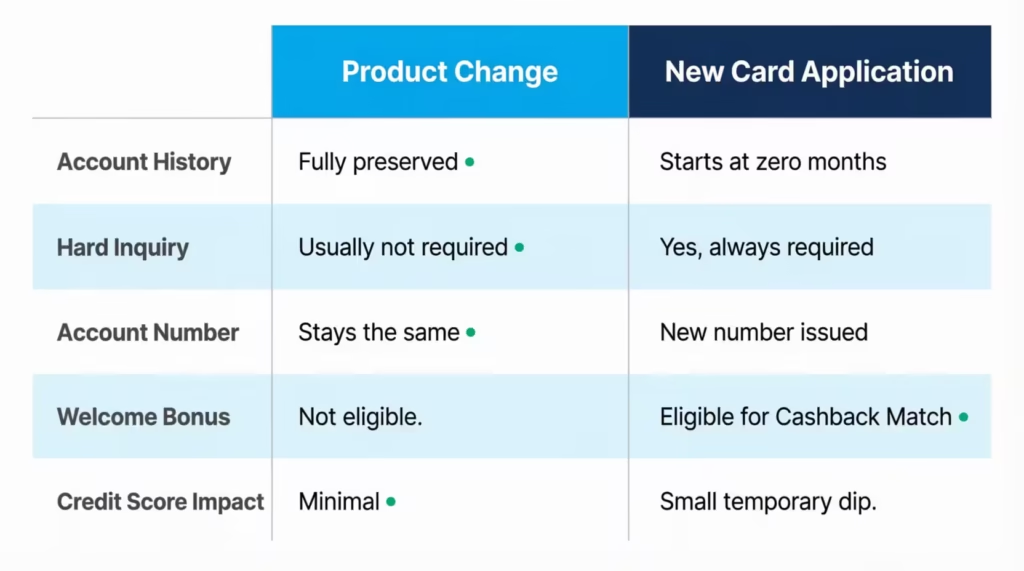

- A product change preserves the full account history, credit limit, and account number, but does not qualify for the first-year Cashback Match welcome bonus, which is available only to new card applicants.

- Product changes and secured card graduation generally do not trigger a hard inquiry, while applying for a new Discover card always does; a new application also starts account history at zero months.

Best for:

- Secured cardholders who have made at least six consecutive on-time payments and want to recover their deposit and continue building credit on an unsecured account.

- Former students who hold the Discover it Student Cash Back card and want to confirm what happens to their account after college or request a switch to a standard consumer card.

- Existing Discover cardholders who want to switch between the Discover it Cash Back and the Discover it Miles card without losing their account history or triggering a hard inquiry.

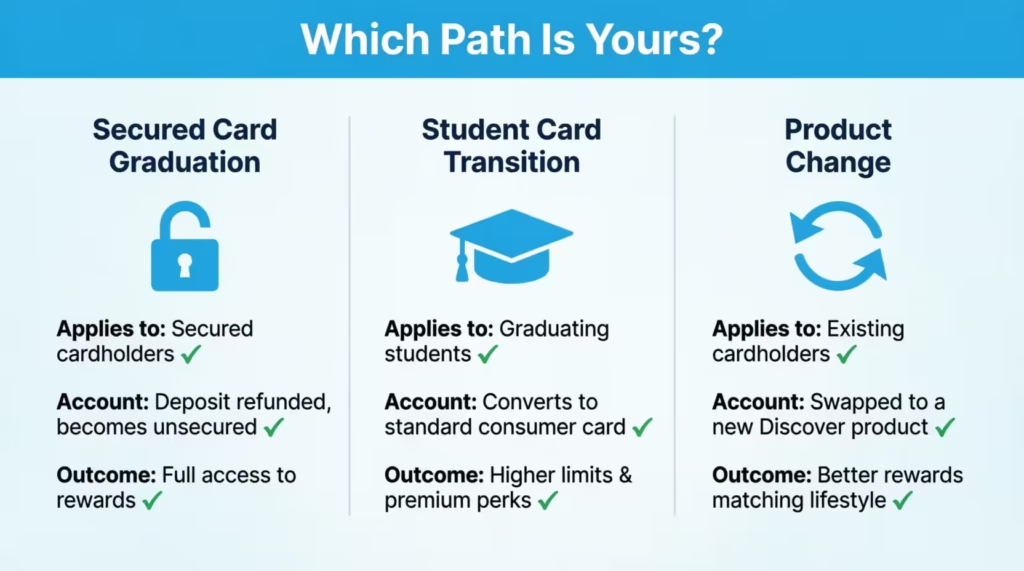

Which Type of Discover Card Upgrade Are You Looking For?

The word “upgrade” means different things at Discover, depending on which card you hold. There are three separate processes under that label. Each has different eligibility requirements, different steps, and a different outcome. Knowing which one applies to you before you call saves a lot of confusion.

Secured card graduation is the first path. This applies if you hold the Discover it® Secured Credit Card. Graduation moves your account from secured (backed by a cash deposit) to unsecured (no deposit required). Your account number stays the same. Your credit history carries over. Your deposit is refunded.

Student card transition is the second path. If you hold the Discover it® Student Cash Back card, you may want a product better suited to a working adult. The student label is removed from your account after college. But your card doesn’t automatically become a different product. Some cardholders get switched to a standard Discover it® Cash Back card, but that isn’t guaranteed.

Product change between consumer cards is the third path. This applies if you already hold a regular Discover card – either the Discover it® Cash Back or the Discover it® Miles – and want to switch between them. A product change keeps your account history, credit limit, and account number intact. No hard inquiry is typically needed.

These three paths aren’t interchangeable. A product change is not the same as applying for a brand-new card. If you call Discover and say “upgrade” without explaining what you need, the representative might give you an answer that doesn’t fit your situation. Know your path before you call.

How the Discover Secured Card Graduation Process Works

Secured card graduation converts your Discover it® Secured account into an unsecured credit card. The account itself doesn’t close. Discover reviews your payment history, credit standing, and account behavior. If you qualify, the security deposit is returned, and the card continues as an unsecured account under the same account number.

When the Discover it® Secured card launched, Discover ran automatic reviews starting at seven months after account opening. That policy no longer works the same way.

Capital One completed its acquisition of Discover in May 2025. Under Capital One’s management, the automatic seven-month review timeline was removed. Discover’s systems regularly check secured accounts, but they don’t have a set schedule for these reviews. Secured cardholders can no longer count on an automatic review at a specific date, the way earlier cardholders could.

The account reports to the three major credit bureaus. These are Equifax, Experian, and TransUnion. This happens during the graduation process. Your credit history doesn’t pause or reset while you wait for a review.

📌 Did You Know: The Discover it® Secured Credit Card stopped accepting new applications in June 2026. If you already hold the card, your account isn’t affected. It stays open, and the graduation path is still available to you.

What Discover Looks for Before Approving Graduation

Discover doesn’t provide a specific checklist. However, the factors it looks at are similar for all successful graduation requests.

The most important signal is six or more consecutive on-time payments on your Discover account. That’s the baseline. Missing even one payment during that window can set the process back.

Beyond your Discover account, Discover also looks at your standing across all your other credit accounts. A missed payment or a collection account on another card can impact your graduation review, even if your Discover account is fine.

Your credit score trajectory matters too. A score that’s been climbing since you opened the account signals responsible behavior over time. Income stability is also a factor. If your income on file with Discover is outdated, update it before you request a review.

Account age is a secondary signal. Most successful graduation requests are from cardholders who have had their account for at least twelve months. However, six on-time payments can happen sooner.

What Changed for Secured Cardholders After Capital One Acquired Discover

Capital One closed its Discover acquisition in May 2025. Two specific changes affect secured cardholders directly.

First, the automatic seven-month review is gone. Before the acquisition, Discover would automatically evaluate secured accounts starting at month seven. That no longer happens on a fixed schedule. Capital One reviews accounts periodically, but doesn’t publish when or how often.

Second, the Discover it® Secured Credit Card stopped accepting new applications in June 2026. If you already hold the card, nothing changes for you. Your account stays active, and the graduation path remains open.

Product change availability has also become less consistent since the acquisition. Some cardholders report being told that certain product changes are no longer available. Others have completed them without issue. If you’re thinking about a specific product change, call Discover first. This way, you can confirm the option is available for your account before you assume anything.

How to Request a Secured Card Graduation From Discover

When you’re ready to request graduation, calling Discover directly is the most reliable method. The number to call is 1-800-347-2683.

When you reach a representative, ask specifically to be reviewed for secured card graduation. Don’t use vague terms like “upgrade.” Be precise. Representatives manage different account changes. Using the right language helps you reach the correct process quickly.

Have these ready when you call:

- Your account number

- Your current annual income (you may be asked to confirm or update it on the call)

- A rough sense of your payment history on the account

The representative will give you one of three responses. First, that an automatic review is already pending, and no action is needed. Second, if your account qualifies, the process will begin right away. Third, that your account doesn’t currently meet the criteria, and they’ll tell you what’s holding it back.

If your account is placed in a review queue rather than graduating immediately, expect the process to take anywhere from a few weeks to a few months. Under Capital One’s current system, it takes six to twelve months from request to account conversion if you need to build more history. If you already meet all the criteria, some cardholders have reported a faster turnaround of two to four weeks.

💡 Pro Tip: Before you call, log into your Discover account and update your income if it hasn’t been updated in the past year. Discover uses the income on file when evaluating graduation eligibility. An outdated or lower figure can slow down the process or lead to an unnecessary denial.

What Happens to Your Security Deposit After Graduation

Once your account graduates, Discover refunds your security deposit. The refund is typically applied as a statement credit to your Discover account. In some cases, it may be returned by check to the address on file.

The timeline for receiving the refund is usually one to two billing cycles after graduation is confirmed.

One key point to remember is that the deposit amount doesn’t turn into your new credit limit. Discover evaluates your creditworthiness separately when setting the unsecured limit. The deposit is simply returned to you.

Some cardholders have added money to their secured account close to graduation in hopes of influencing the new limit. Discover hasn’t confirmed that the strategy works, and the result isn’t guaranteed. What Discover does confirm is that your income, payment history, and credit profile determine the starting limit – not the deposit size.

How Discover Determines Your New Credit Limit After Graduation

Your new unsecured credit limit is set by Discover based on your credit profile at the time of graduation. The deposit you held doesn’t determine the limit.

Discover checks your payment history, income, credit use across all accounts, and your overall credit score. Graduates may receive a limit higher than their original deposit, equal to it, or lower.

If your starting unsecured limit is lower than you expected, you don’t have to accept it as permanent. After graduation, you can request a credit limit increase through Discover’s website or by calling the same number. Many cardholders see their limit increase within six to twelve months of regular use after graduation.

What Happens to Your Discover Student Card When You Graduate From College

The Discover it® Student Cash Back card doesn’t automatically upgrade to a premium rewards product when you leave college. Some online sources suggest otherwise, so it’s worth being direct about what actually happens.

When Discover hears about your graduation, they take action. This can be from you or other signals. Then, they remove the “student” classification. The card and its terms stay the same. Your account stays open, your credit history is fully preserved, and you keep the same account number and credit limit.

Some cardholders say Discover switched their account to a standard Discover it® Cash Back card. This happened after they informed Discover about their graduation. Others report no change at all. Discover’s own documentation doesn’t guarantee an automatic conversion, so experiences vary.

The key point is this: your account doesn’t close, and you don’t have to take action if you want to keep the card as-is. The student card’s terms are nearly identical to the standard Discover it® Cash Back card in most respects.

If you need a different card or want to check what Discover will do with your account, call or chat with Discover directly. This is the best way to get a clear answer.

How to Proactively Request a Product Change on Your Student Card

If you want to switch from the Discover it® Student Cash Back card to the standard Discover it® Cash Back card, you can do so easily. Just request the change directly.

Call 1-800-347-2683 and ask for a product change to the Discover it® Cash Back card. Be specific about which card you want to switch to. Before the representative processes anything, ask whether the product change will trigger a hard inquiry. Most product changes at Discover don’t require one, but confirm this before agreeing to proceed.

If Discover says a product change isn’t available for your account, you can either keep the student card as it is or apply for a new Discover card. Applying for a new card does trigger a hard inquiry and starts your account age at zero. That’s a real trade-off.

Keeping the student card account open, even if you don’t upgrade it, protects the credit history attached to that account. Don’t close it just because you’re no longer a student.

How Discover Product Changes Work Between Consumer Card Types

If you hold a standard Discover card and want to switch to a different Discover product, a product change is the cleanest route. Discover lets you switch between the Discover it® Cash Back and the Discover it® Miles. The Cash Back card earns 5% cash back in rotating categories, up to a quarterly limit. The Miles card earns 1.5x miles on all purchases, with no categories to track.

This is the confirmed consumer-to-consumer product change path at Discover. Discover’s product lineup is limited. Compared to issuers like Chase or Citi, there aren’t many other options available.

A product change keeps everything unchanged. Your account history, credit limit, account number, and standing with credit bureaus all stay the same. One significant trade-off is that a product change doesn’t earn you a new welcome bonus. The first-year Cashback Match offer doubles all cash back or miles you earn in your first year. This offer is for new card applications only, not for product changes.

Product change availability has become less consistent since Capital One acquired Discover. Some cardholders have been told that certain changes are no longer supported. Before building any plans around a specific switch, call Discover to confirm it’s available for your account.

⚠️ Mistake to Avoid: Don’t treat a product change and a new card application as the same thing. A product change keeps your existing account intact and skips the welcome bonus. A new application starts fresh with a new account number, a hard inquiry on your credit report, and full eligibility for the Cashback Match offer. These are two very different outcomes with very different financial implications.

How to Request a Product Change by Phone

Call 1-800-347-2683 and tell the representative you’d like to request a product change. Use that specific phrase – “product change” – not “upgrade” or “new card.”

Before agreeing to anything, ask the representative three specific questions:

- Which cards are currently available as product change options for your account?

- Will this product change require a hard inquiry?

- How does the rewards structure change under the new card?

Discover doesn’t charge annual fees on either the Discover it® Cash Back or the Discover it® Miles, so fee changes aren’t a concern. The main difference is how you earn: rotating categories vs. a flat rate on every purchase.

In some cases, Discover allows product change requests through your online account rather than requiring a phone call. Ask the representative whether this option is available to you.

Once approved, the product change typically takes a few business days to process. Discover will mail a new physical card with the updated branding. Your account number may or may not change, but your account history and credit limit carry over completely.

Will Upgrading or Changing Your Discover Card Hurt Your Credit Score?

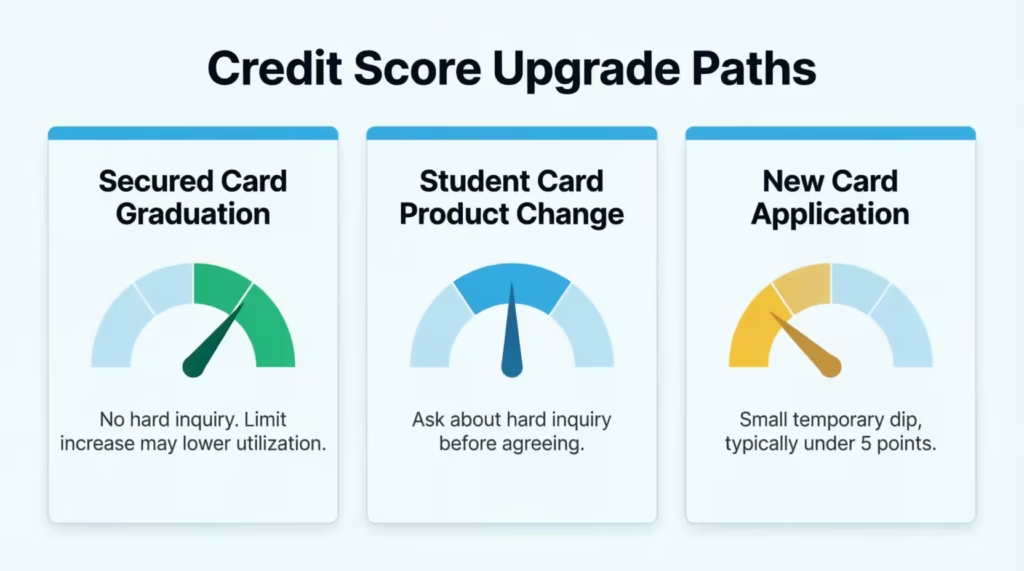

This concern stops a lot of cardholders from taking action. The short answer is that most Discover upgrade paths have little to no negative impact on your credit score. The details depend on which path you’re taking.

Secured card graduation doesn’t typically trigger a hard inquiry. The account keeps reporting under the same account number, so your credit history stays fully intact. If your credit limit goes up after graduation, your credit utilization ratio may improve. This could give your score a small boost over time.

Product changes between consumer cards generally don’t involve a hard inquiry either. Your account history is preserved, and the same account is reported to the credit bureaus before and after the change. Discover may issue a new physical card with new branding, but the underlying account record stays the same.

Student card product changes are less consistent. Ask the representative directly whether the change will trigger a hard inquiry before you agree to anything. That question takes thirty seconds and can prevent an unwanted entry on your credit report.

Applying for a brand-new Discover card works differently from all three scenarios above. A new application does trigger a hard inquiry. According to myFICO, a single hard inquiry typically lowers a credit score by fewer than five points for most people. The inquiry stays on your credit report for two years, but its effect on your score fades within about twelve months.

If your spending stays constant after graduation and your credit limit goes up, your utilization ratio drops. Utilization is one of the most heavily weighted factors in your FICO score. A lower ratio after graduation can help your score recover and grow over the following months.

How to Tell If You’re Ready to Request a Discover Card Upgrade

Calling Discover before you’re ready can lead to a denial. That doesn’t help your odds the next time you try. Running through a quick self-check first takes about five minutes and gives you a much clearer picture of where you stand.

For secured cardholders, check all four of these:

- You have at least six consecutive on-time payments on your Discover account

- All other credit accounts are in good standing – no missed payments, no collections

- Your credit score has improved since you opened the account

- The income on file with Discover reflects what you actually earn now

For student cardholders moving to a regular card:

- You’re approaching or past your college graduation date

- Your income has increased (a new job or full-time employment after school)

- You want better rewards than the student card currently provides

For consumer card product change requests:

- Your account has been open for at least twelve months

- You have no recent late payments on any account

- Your current balance is below 30% of your credit limit

Before you call, take two quick actions. First, log in to your Discover account and update your income if it’s been more than a year since you last did. Second, pull your free credit report at AnnualCreditReport.com and look for any derogatory marks you may have forgotten about.

Marcus, a 24-year-old retail coordinator from Atlanta, called Discover. He wanted to request a secured card graduation after eight months of on-time payments. He was sure he’d qualify. Then the representative pointed out something. His income still showed his old part-time job.

That job was from two years ago, before his promotion. He updated his income on the call and received graduation approval within three weeks. The lesson: your payment record matters, but the income figure Discover has on file matters just as much.

What to Do If Discover Denies Your Upgrade Request

A denial isn’t the end of the road. The steps to take after hearing “no” depend on why Discover gave that answer.

When Discover denies a credit limit increase or a graduation request, they’re required to provide an adverse action notice. This is a written explanation of the reason for the denial. It will arrive by mail or appear in your online account. Read it carefully. It tells you exactly what to address.

If denied for insufficient payment history: Keep paying on time and wait three to six months before requesting again. Avoid calling back every few weeks. Too many requests in a short window can work against you.

If denied for a low credit score: look at what’s dragging the score down. High utilization on another card, a missed payment, or a collection account that doesn’t belong to you can each appear in the explanation. Address the specific issue before trying again. Dispute any errors directly with the credit bureaus.

If denied because the product change isn’t available: Some cardholders have faced this situation since Capital One’s acquisition. In this case, the denial isn’t about your creditworthiness – it’s a policy limitation. Ask the representative when the option might be restored. If no timeline is available, the decision shifts to whether to wait or to apply for a new Discover card instead.

Applying for a new card after a policy-based denial makes more sense than it does after a credit-based denial. A credit-based denial signals your profile isn’t ready. A policy-based denial simply means the product change route is closed right now – and a new application may be the only open door.

When Applying for a New Discover Card Makes More Sense Than a Product Change

Sometimes, applying for a new Discover card is the better choice, even if a product change is possible later.

If the specific Discover card you want isn’t available as a product change option, a new application is the only way to get that product. There’s no workaround for this.

A new application also makes you eligible for the first-year Cashback Match bonus. Discover doubles all the rewards you earn in your first twelve months – cash back or miles – at the end of that year. A product change doesn’t include this offer. For someone who plans to use the card actively, the Cashback Match can add up to a meaningful amount over twelve months.

The trade-off is real, though. A new application adds a hard inquiry to your credit report. The new account also starts with zero months of history, which can temporarily lower your average account age.

A Simple rule: If your credit score is over 700, your income is steady, and you won’t apply for big credit soon, go ahead. Big credit means things like a mortgage or an auto loan. Applying for a new Discover card is likely better than waiting for a product change that might not happen.

Frequently Asked Questions (FAQs)

Does Discover let you upgrade your card?

Yes, but the path depends on which card you currently hold. Discover has three different processes: secured card graduation, student card transition, and product changes between the Discover it Cash Back and Discover it Miles consumer cards.

Can I change my Discover card type?

Yes, Discover allows product changes between the Discover it Cash Back and the Discover it Miles card. Call 1-800-347-2683. Ask for a product change. Confirm if the switch will cause a hard inquiry before agreeing.

Are there downsides to upgrading a card?

The main downside is giving up the welcome bonus. Discover’s first-year Cashback Match doubles all rewards earned in your first twelve months. This offer is only for new card applications and doesn’t apply to product changes.

Will upgrading affect my credit score?

Secured card graduation and consumer product changes typically don’t trigger a hard inquiry, so your score usually isn’t harmed. If your credit limit increases after graduation, your credit utilization ratio may drop, which can give your score a modest lift over time.

What is the downside to the Discover card?

Discover’s product lineup is limited compared to issuers like Chase or Citi, leaving fewer options if you want to switch to a different product. Product changes are currently restricted to two consumer cards: the Discover it Cash Back and the Discover it Miles.

Can I upgrade my Discover card to a Capital One card?

No direct upgrade path exists from a Discover card to a Capital One card. Capital One finished buying Discover in May 2025. However, both brands still run as separate product lines. Cardholders cannot convert between the two brands.

Will all Discover cards move to Capital One?

No migration of existing Discover accounts to Capital One products has been announced. After the May 2025 acquisition, Discover cards still operate under the Discover brand. However, some product policies have changed, like the secured card review timeline.

Can I request a Discover secured card graduation online, or do I need to call?

Calling Discover at 1-800-347-2683 is the most reliable method for requesting secured card graduation. While Discover sometimes allows product change requests online for consumer cards, the graduation process for secured cardholders is best initiated by phone.

Does a Discover product change come with a new card in the mail?

Yes, Discover typically mails a new physical card with updated branding after a product change is approved. Your account number may or may not change, but your full account history, credit limit, and account age carry over completely.

Wrapping Up

Upgrading your Discover card comes down to knowing which path fits your current card and your credit profile. Secured cardholders should aim for six months of on-time payments. Then, call to ask for graduation directly. Student cardholders should reach out to Discover after graduation. This way, they can confirm what will happen to their account.

For consumer card switches, a product change is best. But check availability first because of the changes at Capital One. The most effective approach is to prepare before you call, ask specific questions, and have a clear fallback if the answer is no.

If this guide helped you figure out your next step, share it with a friend who’s trying to make the most of their own Discover card.