Closing an American Express credit card feels like it should be simple. But many cardholders discover too late that they lost their Membership Rewards points, missed a full fee refund, or took a surprise credit score hit because they skipped a few key steps.

The process of canceling an Amex credit card involves more than a single phone call. Done in the right order, it is clean and painless. Done out of order, it gets expensive fast.

In this guide, we walk you through every step, from protecting your points to timing your cancellation around the fee refund window, and getting confirmation in writing.

Key Takeaways

This guide explains how to cancel an Amex credit card the right way, covering pre-cancellation steps to protect Membership Rewards points, the 30-day annual fee refund window, retention offer evaluation, credit score impact, and the product change alternative.

Core Facts:

- Amex refunds the annual fee in full only if you cancel within 30 days of the fee posting; no prorated refund applies after that window closes.

- Membership Rewards points are forfeited immediately upon closure if the canceled card is the only one linked to your rewards account; a 30-day redemption window applies for most U.S. cardholders.

- Co-branded Amex cards (Delta SkyMiles, Hilton Honors, Marriott Bonvoy) do not protect your Membership Rewards balance; only cards that earn Membership Rewards directly qualify.

- Canceling a card reduces your total available credit, which raises your credit utilization ratio and can lower your credit score if you carry balances on other accounts.

- A closed Amex account in good standing remains on your credit report for up to 10 years, so payment history and account age continue benefiting your score after closure.

- A product change (downgrade to a no-fee Amex card) keeps the account open, preserves your credit limit and account history, and protects your Membership Rewards balance.

Best for:

- Amex cardholders approaching or within their 30-day annual fee refund window who are weighing whether to cancel or downgrade.

- Cardholders with a large Membership Rewards balance who need to confirm whether their points are protected before calling to cancel.

- Anyone considering full cancellation who wants to understand the credit score impact and explore retention offers or downgrade options first.

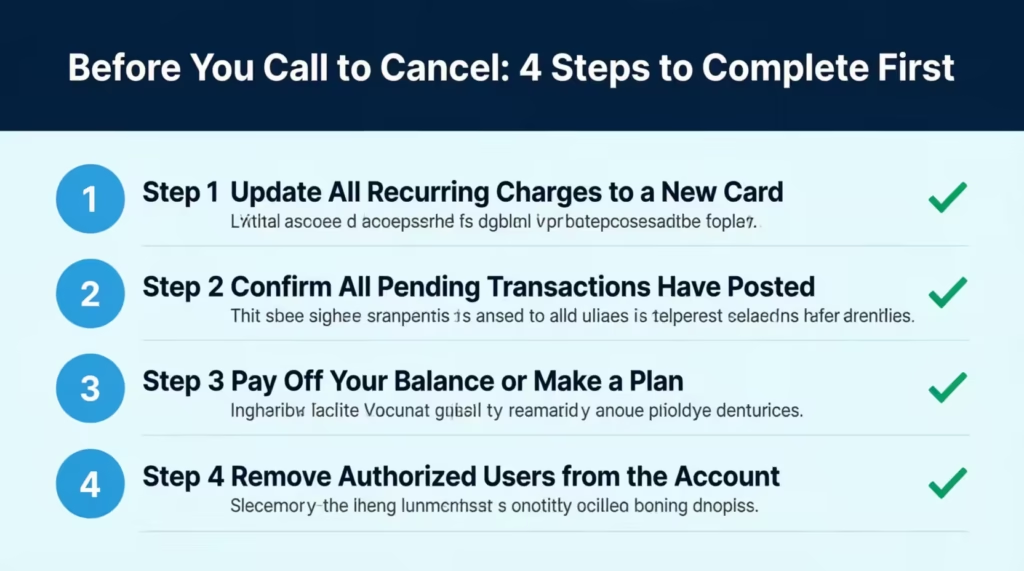

What to Do Before You Call to Cancel Your Amex Card

The order you follow matters just as much as the call itself. Most cardholders dial customer service first and think about everything else later. That is when the problems start. A gym membership keeps billing a closed card. Points disappear because no one thought to move them. A pending hotel hold creates a disputed charge weeks after the account is supposedly gone.

Before you pick up the phone, complete these four tasks in order. Each one prevents a specific problem that is very hard to fix after the fact.

Update Every Recurring Charge Tied to This Card

Go through your last two or three statements. Find every subscription or recurring payment billed to this card. Think broadly: streaming services, gym memberships, insurance premiums, software subscriptions, cloud storage, and any utility on autopay.

Write them down, then update each one to a different payment method before you cancel. Do not assume a merchant will decline the charge and send you a polite notification. Many merchants retry failed payments multiple times. Some will send your account to a collections agency after repeated failures.

Give yourself at least one full billing cycle before canceling. Some merchants take 10 to 14 days to process a payment method change on their end. If your next billing date is coming up soon for any of these services, update the payment method now and wait to confirm that the next charge hits your new card successfully. Then cancel.

Missing even one recurring charge can mean a surprise collections notice or an unexpected service interruption weeks after you thought the card was fully closed.

Confirm All Pending Transactions Have Posted

Log in to your AmericanExpress.com account and review your transaction list before calling. Look for any transactions labeled as pending. These are purchases that have been authorized but have not yet been fully settled into your account.

Closing the account does not cancel pending transactions. They will still process and appear on your final statement. But if you cancel before they post, it can create billing confusion and sometimes a small dispute to sort out afterward.

Wait until the account shows no pending activity. For most everyday purchases, this takes two to five business days. Hotel authorization holds, and gas station charges can sometimes take a bit longer to clear.

Once everything looks settled, you are ready for the next step.

Pay Off Your Balance or Make a Plan for It

Closing your Amex card does not erase any balance you owe. The debt remains. Interest continues to accrue at the same rate. Minimum payment requirements do not stop.

If possible, pay the balance to zero before canceling. This keeps everything clean and removes any ambiguity about what is still owed after the account closes.

If a full payoff is not possible right now, that is fine. You can still cancel the account. Just know that your minimum payment is still due each billing cycle. Amex will send you a final statement with any remaining balance. Set a reminder so you do not miss that payment.

Remove Authorized Users Before You Close the Account

If anyone else is listed as an authorized user on your account, they will lose card access when the account closes. It is cleaner to remove them ahead of time rather than letting the closure cut off access without warning.

You can remove authorized users by calling the number on the back of your card or by using the Amex online chat tool. The process takes just a few minutes.

Once the removal is confirmed, collect their physical card if possible. Set it aside to destroy when you destroy your own card after the account is fully closed.

How to Protect Your Amex Membership Rewards Points Before Canceling

Membership Rewards points are not automatically safe when your Amex account closes. In some situations, those points disappear the moment the account is shut down immediately and permanently. In others, they survive without you needing to do anything.

The key is knowing which situation you are in before you make the call. Getting this wrong is one of the most costly mistakes a cardholder can make during the cancellation process. Points that took months or years to earn can be gone in seconds.

Here is what happens in each scenario.

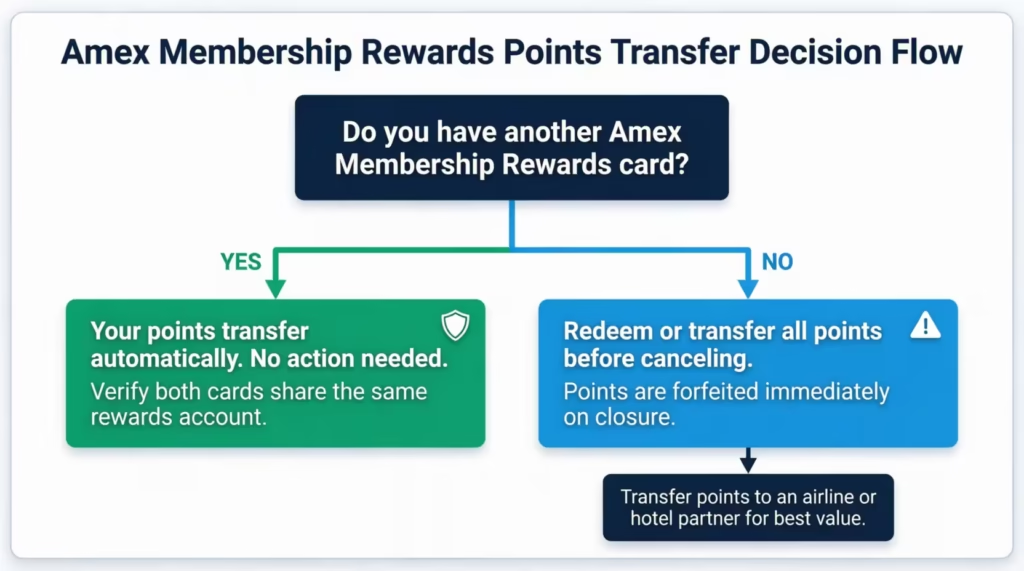

If You Have Another American Express Membership Rewards Card

If you hold at least one other American Express card that earns Membership Rewards points, your points are safe. They do not disappear when you close one card in the program. They transfer automatically to your remaining Membership Rewards account.

There is one thing to verify before you cancel. Make sure both cards are linked under the same Membership Rewards account. Log in to AmericanExpress.com and confirm that your rewards balance appears under a shared program account. If they share the same account, your points carry over without any action needed on your part.

One important note: co-branded Amex cards do not count toward this protection. If your other Amex card is a Delta SkyMiles card, a Hilton Honors card, or a Marriott Bonvoy card, it earns points in a separate loyalty program. It will not protect your Membership Rewards balance. Only cards that earn Membership Rewards points directly, such as the Amex Platinum, Amex Gold, Amex Green, or Amex EveryDay, will keep those points safe.

If This Is Your Only American Express Membership Rewards Card

If the card you are canceling is the only card linked to your Membership Rewards account, your points will be forfeited immediately upon closure. Per American Express’s Membership Rewards terms, unredeemed points are forfeited immediately when the last linked card account closes, and no other enrolled card exists.

There is a limited exception. As of December 2023, New York cardmembers may have up to 90 days after account closure to redeem any remaining points. For all other cardmembers in the United States, a 30-day redemption window applies after the account closing date. After that window ends, the points are gone for good.

Do not call to cancel until you have redeemed or transferred all of your points. Redemption options include travel bookings through Amex Travel, statement credits, gift cards, and transfers to airline or hotel partners. The transfer option typically delivers the strongest value per point and is covered in detail in the next section.

⚠️ Mistake to Avoid: Do not assume that having another Amex card automatically protects your Membership Rewards balance. Delta SkyMiles, Hilton Honors, and Marriott Bonvoy cards operate under separate loyalty programs. Only cards enrolled directly in Membership Rewards will keep your points alive.

Transferring Points to Airline or Hotel Partners Before You Cancel

Transferring your Membership Rewards points to an airline or hotel partner before canceling is the safest way to protect a large balance. Once transferred, those points belong to the partner program. They are completely independent of your Amex account and cannot be lost through account closure.

American Express allows transfers to more than 20 airline and hotel partners. Popular options include Delta SkyMiles, Air Canada Aeroplan, British Airways Executive Club, and Marriott Bonvoy. Most transfers are completed within 24 to 48 hours. Some are instant.

This strategy works best if you already have a frequent flyer or hotel loyalty account set up. If you do not have one, create it before you initiate the transfer. You will need an active account number to receive the points.

In general, transferring to airline partners delivers significantly more value than redeeming points for statement credits or gift cards. If your balance is substantial, the transfer route is worth the extra step.

How to Cancel Your Amex Card by Phone

Calling American Express is the most direct way to close your account. It also gives you the best chance of receiving a retention offer before the account is finalized.

Have the following ready before you dial:

- Your card number

- Your billing address and ZIP code

- A clear, simple statement of your intent to cancel

The main number for American Express customer service is 1-800-528-4800. You can also call the number printed on the back of your card. If you are calling from outside the United States, use the international collect number 1-336-393-1111.

When the agent answers, state your request clearly: “I’d like to close my American Express credit card account.” You do not need to provide a detailed explanation.

At some point during the call, the agent may offer you a retention deal to encourage you to keep the account open. The next major section of this guide covers exactly what to do at that moment and how to evaluate whether the offer is worth accepting.

If you decide to go forward with the cancellation, confirm the following before you hang up:

- The official account closure date

- Whether any remaining balance is still your responsibility (it is)

- A confirmation number for the closure

- Whether a written confirmation will be sent to you, and through what channel

If the agent does not offer to send written confirmation, ask for it directly. A confirmation email or letter protects you if there is ever a question about whether the account was properly closed.

How to Cancel Your Amex Card by Mail

Canceling by mail is an option for cardholders who prefer written documentation from the start. It is the slowest method and is not a good fit if you are trying to cancel within the 30-day annual fee refund window, since that deadline is time-sensitive.

Your cancellation letter should include:

- Your full legal name and mailing address

- Your credit card account number

- The date you are requesting the account to be closed

- A clear request for written confirmation of the account closure

Send the letter to the address listed on your most recent Amex monthly statement. Send it via certified mail so you have proof of delivery and a timestamped record. Keep a copy of the letter for your own files.

How to Cancel Your Amex Card Online Using the Chat Tool

American Express allows cardholders to close accounts through its online chat feature. This option works well if you want to cancel without making a phone call.

Here is how to cancel through the chat tool:

- Log in to your account at AmericanExpress.com.

- Find the “Chat” icon in the bottom-right corner of the screen.

- Open the chat and tell the representative you want to close your account.

- Follow the representative’s prompts to confirm the closure.

- Before ending the chat, ask for written confirmation of the account closure. Request that a confirmation be sent to your email address on file, or screenshot the chat conversation yourself before closing the window.

One important distinction: the chat tool can fully close your account. But if you are hoping to receive a retention offer, calling by phone is the better route. Retention offers are more consistently presented through live phone conversations with a retention specialist. The chat channel is better suited for cardholders who have already made their decision and are not interested in any counter-offers.

💡 Pro Tip: Before starting the chat session, have your Amex account open in a separate browser tab. You may be asked to verify your card number, billing address, or other account details mid-conversation, and having them visible saves time.

What to Do When Amex Offers You a Retention Deal

When you call to close your account, there is a good chance the agent will offer you a deal to keep the card open. This is called a retention offer. American Express uses these offers because keeping an existing cardholder costs the company far less than acquiring a new one.

Retention offers take several forms:

- A discounted or fully waived annual fee for the upcoming card year

- A statement credit is applied directly to your account

- A bonus points offer, typically tied to a minimum spending requirement over the next 60 to 90 days

Not every cardholder receives an offer. Some agents will tell you no offer is available for your account. But you can always ask proactively instead of waiting to see if one comes up. When the agent answers, you can say: “Before I close my account, I’d like to know whether any retention offers are available.”

If the agent says no offer exists, proceed with the cancellation. If they present an offer, you are not obligated to accept it on the spot. Ask them to give you a moment to think it through.

One practical note: chat representatives are less likely to surface retention offers than phone agents who are connected directly to a retention team. If exploring a deal is a priority before you cancel, calling is the better choice.

How to Evaluate Whether the Retention Offer Is Worth Accepting

When an offer comes through, the math is simple. Calculate the net value of the offer and compare it to the annual fee you would be paying for another year.

Work through it like this. Say you hold the Amex Gold Card with a $325 annual fee. The agent offers you 20,000 Membership Rewards points if you spend $2,000 in the next 90 days. At a conservative estimate of 1 cent per point in travel value, those 20,000 points are worth about $200.

The net cost of keeping the card for another year would be $125, the $325 annual fee minus $200 in point value. The real question is: does the Amex Gold Card deliver at least $125 in value to you over the next 12 months beyond what you just earned? If yes, the offer makes sense. If no, decline and cancel.

Now consider a second scenario. The agent offers to reduce the annual fee by $150. That drops your cost from $325 to $175 for the year. The same question applies: is the card worth $175, given the benefits you actually use?

If the offer involves a spending requirement, check honestly whether you can hit that threshold naturally in the next 90 days without stretching your budget. Never take on unnecessary spending just to qualify for a retention bonus.

If the offer does not meaningfully close the gap between the fee and the value you get, decline politely and proceed with the cancellation. The agent will not push back, and the closure process continues the same way.

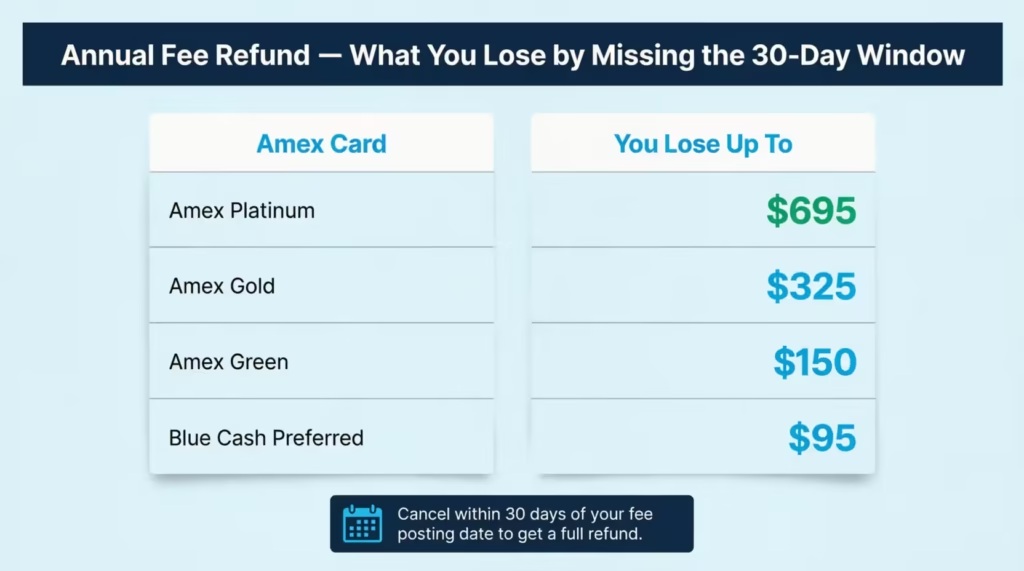

The 30-Day Annual Fee Refund Rule – And How to Time Your Cancellation

American Express will refund your annual fee in full if you cancel within 30 days of the date the fee was charged. After that 30-day window closes, no prorated refund is issued. The full annual fee stays with American Express regardless of how many months remain in your card year.

This is one of the most financially significant rules in the entire cancellation process. Missing the window by even one day can cost you hundreds of dollars.

Here is what the refund looks like in dollar terms across the most common Amex cards:

| Amex Card | Annual Fee | What You Lose by Missing the 30-Day Window |

|---|---|---|

| Amex Platinum | $695 | Up to $695 |

| Amex Gold | $325 | Up to $325 |

| Amex Green | $150 | Up to $150 |

| Blue Cash Preferred | $95 | Up to $95 |

To find when your fee was charged, log in to AmericanExpress.com and check your transaction history. Search for a line item labeled “Annual Membership Fee” and note the exact date it posted.

If you are within 30 days of that date, cancel now. You will receive the full refund.

If you are well past the 30-day window, consider a different timing strategy. Wait until a few days before your next annual fee is scheduled to post, then cancel. That way, the fee never hits your account in the first place. Annual fees typically post around the same date each year. Check your statements from the prior year to identify the pattern.

📌 Did You Know: If you are inside the 30-day window and considering a product change (downgrade) instead of full cancellation, prorated fee adjustments may also apply. Ask the Amex agent specifically whether you are eligible for a partial fee refund on a downgrade requested within this window.

How Canceling Your Amex Card Affects Your Credit Score

Closing an Amex account has a real impact on your credit score. But the effect is often smaller than most cardholders expect, and in most cases it is temporary. Understanding exactly which factors are affected helps you make a smarter decision.

Two components of your FICO Score are directly affected by closing a credit card. The first is your credit utilization ratio, which myFICO identifies as making up 30% of your total FICO score. The second is the average age of your credit accounts, which accounts for 15%. Neither impact is immediate and permanent. Both depend on the rest of your credit profile.

How It Affects Your Credit Utilization Ratio

Credit utilization measures how much of your total available credit you are currently using. When you close a credit card, that card’s credit limit is removed from your total available credit. If you carry any balances on other cards, your utilization ratio rises right away.

Here is a clear example. Say you have three credit cards with a combined credit limit of $20,000. You carry $4,000 in balances across those three cards. Your utilization is 20%, which is within the healthy range that most lenders prefer.

Now you close your Amex card, which had a $5,000 credit limit. Your total available credit drops to $15,000. Your $4,000 in balances now represent 26.7% utilization. That 6.7-point jump could meaningfully affect your score, depending on your full credit profile.

If you carry zero balances on your other cards, this effect is minimal. The ratio stays low no matter how much total credit you have available.

One option worth exploring: ask Amex at the time of cancellation whether the credit line from the closing card can be transferred to another Amex card you hold. Not every situation qualifies, but it is worth a quick ask. Transferring the line keeps your total available credit intact.

How It Affects the Average Age of Your Credit Accounts

Closing an Amex card does not immediately reduce your average account age. This is a common misconception. Closed accounts in good standing remain on your credit report for up to 10 years. During that entire time, they still factor into the average age calculation.

The impact on account age is gradual, not a sudden drop the moment the card closes. If your Amex card is 10 years old and you close it today, you will not notice the score effect for many years, not until the account eventually falls off your report.

If the card you are closing is relatively new, the impact on your average account age is minimal. If it is one of your oldest accounts, the long-term effect on your credit history is a factor worth weighing before you decide to cancel rather than downgrade.

How Long a Closed Amex Account Stays on Your Credit Report

A closed Amex account in good standing stays on your credit report for approximately 10 years. During that entire period, the positive payment history, the long account age, and the responsible use record all remain visible to lenders.

Negative information tied to the account, such as late payments, remains for 7 years.

This is genuinely good news for most cardholders. Closing the account does not erase your credit history. The record of responsible use continues working in your favor for years after the card is gone from your wallet.

Should You Downgrade Instead of Cancel? The Amex Product Change Option

Before you finalize a cancellation decision, it is worth knowing that a third option exists. American Express allows cardholders to do a product change, which means switching your current card to a different Amex card with a lower annual fee or no annual fee at all.

When you do a product change, the account does not close. Your credit limit stays open. Your account history continues. Your average account age is unaffected. And your Membership Rewards balance, if applicable, remains fully intact. A product change preserves almost all of the credit score benefits of keeping the card open, while eliminating the annual fee burden.

There are two key restrictions to understand.

First, Amex generally requires you to stay within the same card family. You can switch one personal consumer card to another personal card, but you typically cannot cross between personal and business products. Co-branded cards, such as Delta or Hilton, are usually limited to downgrade options within that same brand family.

Second, Amex’s one-bonus-per-lifetime rule still applies after a product change. If you downgrade a card and later want to reapply for the same or a higher version of it, you will not be eligible for a welcome bonus again. For cardholders who are simply looking to reduce fees without closing the account entirely, this is rarely a concern.

Which Amex Cards Can Be Downgraded and to What

The specific downgrade options depend on which card you currently hold. Here are the most common paths:

These paths are not guaranteed for every account. Eligibility depends on your account history, how long you have held the card, and your current standing with American Express.

Always ask the agent directly: “What product change options are available for my account?” This ensures you hear all eligible options rather than just the first one the agent mentions.

How to Request a Product Change Instead of Cancellation

The process for requesting a product change is almost identical to calling to cancel. Use the same number: 1-800-528-4800, or the number printed on the back of your card.

When the agent answers, say this: “I’m considering canceling my card, but I’d like to explore downgrading to a different Amex card instead. What product change options are available for my account?”

The agent will review your account and present eligible options. If you find one that fits, the agent processes the change on the spot. You will receive a new physical card in the mail within 7 to 10 business days. Your account number, history, and credit limit all stay the same. Only the card product itself changes.

You can also request a product change through the Amex chat tool at AmericanExpress.com. Follow the same steps used for cancellation via chat, but tell the representative you want to explore a downgrade rather than a full closure.

After You Cancel: Confirming Closure and Closing the Loop

Once the cancellation is confirmed, a few final steps remain. Skipping them can lead to billing issues and credit reporting problems later.

Before you end the call or close the chat session, ask for written confirmation of the account closure. Specifically, request:

- The official date the account was closed

- Confirmation that the balance is zero (or a clear note of any remaining balance owed)

- A confirmation number for the closure

Ask Amex to send this confirmation to the email address on file. If you prefer, you can also request a written letter mailed to your address. Save this document for at least two to three years. If a dispute ever arises about whether the account was properly closed, this confirmation is the document that resolves it.

After the call or chat, monitor your email for the confirmation message. If it does not arrive within three to five business days, follow up.

One more thing to expect: a final statement will likely arrive after the account is closed. This is normal. Any transactions that were still processing at the time of closure will appear here. You are still responsible for paying anything shown on that final statement.

What to Do With Your Physical Amex Card

Once you receive written confirmation that the account is closed, destroy the physical card. Cut through the chip and through the card number with scissors. If you have access to a shredder, that works even better.

This applies to all cards associated with the account. If authorized users had physical cards issued under your account, collect and destroy those as well.

Even after account closure, a card with a visible number can be misused if it falls into the wrong hands before the system has fully deactivated it. Destroying the card removes that risk entirely.

What to Do If Amex Charges You After Cancellation

Not every charge that appears after cancellation is an error. Recurring transactions that were still in process at the time of closure may still post to your account in the days following cancellation. You are responsible for these charges, even if the account is now closed.

If you see a charge you do not recognize and cannot link to any transaction you authorized before cancellation, act quickly. Call American Express at 1-800-528-4800 and reference your account closure confirmation date. Explain that the charge appeared after the confirmed closure date. Amex will investigate, and if the charge is erroneous, it will be removed.

Keep your closure confirmation document accessible when you make this call. The confirmed closure date is the key piece of information that allows Amex to distinguish a legitimate trailing charge from a billing error.

Frequently Asked Questions (FAQs)

Is there a cancellation fee for American Express?

American Express does not charge a separate fee to close your account. The only real cost to consider is missing the 30-day window after your annual fee posts, which means no refund on that fee is issued.

How long does it take to cancel an AmEx account?

The cancellation call or chat typically takes 10 to 20 minutes from start to finish. Your account is generally closed immediately once the representative confirms the request, though your final statement may take a few additional business days to generate.

Is it hard to cancel an AmEx card?

Canceling an Amex card is a simple process by phone or online chat. The more involved part is completing the pre-cancellation tasks beforehand, such as redeeming your Membership Rewards points and updating recurring charges to a different card.

Is it better to cancel a credit card or just stop using it?

Leaving the card open with a zero balance is almost always better for your credit. A card with no balance keeps your total available credit higher, which lowers your utilization ratio and preserves the account’s age on your credit report.

How much will my credit score drop if I cancel a card?

The drop depends on your credit utilization ratio and how old the account is. Cardholders with zero balances on other cards may see little to no impact, while those carrying balances across multiple accounts could see a more noticeable change.

How much are 50,000 Amex Membership Rewards points worth?

At a conservative estimate of 1 cent per point, which is a standard benchmark for travel redemptions, 50,000 Membership Rewards points are worth roughly $500. Transferring to airline or hotel partners can push that value higher, depending on how you redeem them.

Can I cancel an American Express credit card online?

Yes, you can cancel through the chat tool at AmericanExpress.com by logging into your account and clicking the Chat icon at the bottom right. If you also want to ask about a retention offer, calling 1-800-528-4800 is more likely to surface one.

Does canceling one Amex card affect my other Amex cards?

Canceling one card does not affect the standing, credit limit, or benefits of any other Amex cards you hold. The one exception involves Membership Rewards points: if the canceled card was the last one linked to your rewards account, those points are forfeited unless redeemed first.

How long after canceling does a closed Amex account appear on my credit report?

Amex reports account updates to the credit bureaus on a monthly cycle, so a closed account typically appears as closed within 30 to 60 days after cancellation. Once reported, the account stays on your credit report in good standing for up to 10 years.

Bottom Line

Closing an Amex account cleanly takes a bit more planning than a single phone call, but none of it is complicated. The highest-priority steps are protecting your Membership Rewards points and timing your cancellation around the 30-day annual fee refund window. From there, asking about retention offers and downgrade options gives you the full picture before you commit to a final closure.

Based on the credit score factors at play, a product change is the better move for most cardholders who can find a no-fee Amex option that fits their needs. Get written confirmation when it is done and keep it on file.

If this guide helped you, share it with someone else thinking about their Amex options. A friend facing the same choice will find every step useful.