If you’ve ever needed cash fast and wondered whether your American Express card could help, you’re not alone. Many Amex cardholders don’t know how to get cash from their Amex credit card, or worse, they try it without knowing the true cost.

The good news is that most Amex revolving credit cards do allow cash access. But the process has a few steps you’ll want to know before you start.

In this guide, we’ll walk through every method, every fee, and every smart alternative so you can make the best choice for your situation.

Key Takeaways

This guide explains how to get cash from an Amex credit card, covering ATM and bank branch methods, PIN setup requirements (7-10 business days), the 5% transaction fee structure, immediate interest accrual with no grace period, and cheaper alternatives to consider first.

Core Facts:

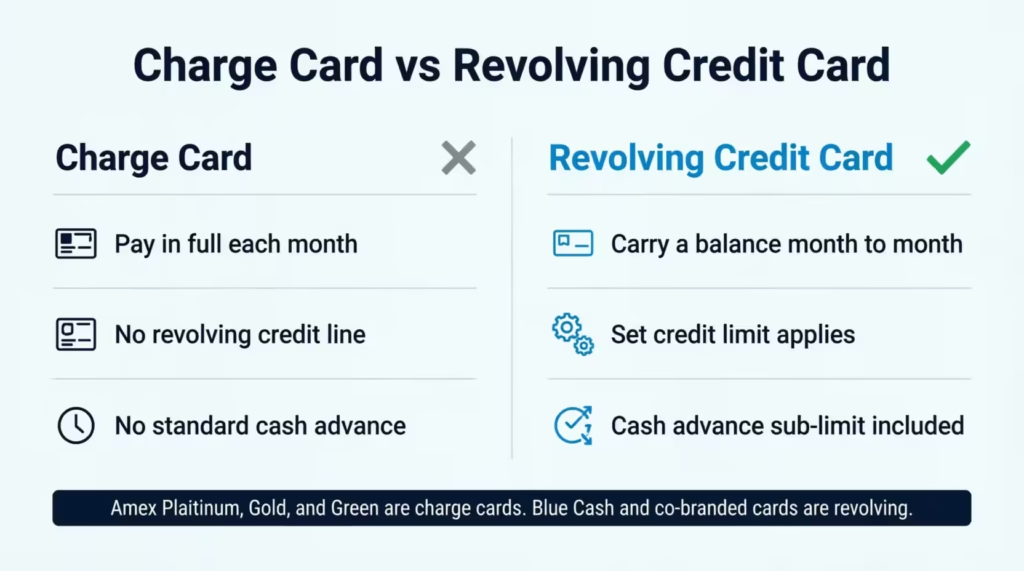

- Only revolving Amex credit cards (Blue Cash, co-branded cards) support standard cash advances; charge cards (Platinum, Gold, Green) do not have a traditional cash advance feature.

- Your cash advance limit is a separate sub-limit, typically 20-30% of your total credit limit, and decreases as your purchase balance rises.

- A cash advance PIN must be requested separately online or by phone and arrives by mail in 7-10 business days; bank branch teller withdrawals do not require a PIN.

- Amex charges a cash advance fee of 5% of the transaction amount or $10, whichever is greater, applied immediately on the transaction date.

- Interest accrues from Day 1 with no grace period; a $300 cash advance at 29.99% APR costs approximately $25.80 in total fees and interest within the first 30 days.

- International cash advances add a 2.7% foreign transaction fee on most standard Amex cards on top of the standard 5% cash advance fee.

Best for:

- Amex cardholders facing a genuine short-term cash emergency who can repay the full balance within one billing cycle.

- Travelers who need local currency abroad and have confirmed their card’s foreign transaction fee policy in advance.

- Cardholders researching costs before deciding between a cash advance and a personal loan or credit union emergency loan.

Does Your Amex Card Allow Cash Advances?

Before you head to the nearest ATM, there’s one thing you need to check first: not every American Express card supports a traditional cash advance.

Amex issues two different types of cards, and they work very differently when it comes to cash access. Knowing which one you hold takes less than a minute and can save you a frustrating trip.

How Charge Cards and Credit Cards Handle Cash Differently

A revolving credit card lets you carry a balance from one month to the next. You have a set credit limit, and your monthly statement shows a “minimum payment due.” These cards come with a built-in cash advance sub-limit. That means cash access is part of the account by design.

A charge card works differently. It requires you to pay your balance in full every month. Because there’s no revolving credit line, there’s no traditional cash advance credit pool to draw from. The Amex Platinum, Amex Gold, and Amex Green cards all fall into this category.

Some charge cards do offer a limited cash access program called Amex Express Cash, but this is not the same as a revolving card cash advance. It works through a separate enrollment process, and the terms are different.

Co-branded cards, such as the Delta SkyMiles cards, Hilton Honors cards, and Marriott Bonvoy cards issued by American Express, are revolving credit cards. So are the Blue Cash Everyday and Blue Cash Preferred cards. These cards do support standard cash advances.

How to Confirm Which Type of Card You Have

You can figure this out in about 60 seconds using one of these methods:

- Check your monthly statement. If it shows a “minimum payment due,” your card is a revolving credit card that supports cash advances. If it only shows a “payment due in full” requirement, it’s a charge card.

- Log in to your Amex account online. Go to your card’s details page. The account type is listed under your card information.

- Check your cardholder agreement. It will clearly state whether a cash advance feature applies to your account.

If you have a charge card and still want cash access, call the number on the back of your card and ask specifically about the Amex Express Cash program. The eligibility and terms vary by account.

What Is Your Amex Cash Advance Limit?

Once you’ve confirmed your card supports cash advances, there’s a second number you need to know before you do anything else: your cash advance limit.

This is not the same as your total credit limit, and many cardholders get surprised by this. Your total credit limit covers purchases. Your cash advance limit is a separate, smaller sub-limit that sits within that total.

For example, if your credit limit is $10,000, your cash advance limit might be $1,500 or $2,000. You can’t withdraw $5,000 just because $5,000 is available for purchases. The cash advance sub-limit is its own ceiling, and it applies only to cash transactions.

There’s one more thing to keep in mind. Your available cash advance balance goes down as your overall card balance goes up. If you’ve already charged $8,000 in purchases on a $10,000 card with a $2,000 cash advance limit, your available cash advance might be zero, even though you haven’t taken a single dollar of cash.

To find your specific cash advance limit, log in to your Amex account. Look under your card details or account summary. The limit is listed there. You can also find it on your monthly statement or in your cardholder agreement.

Why Your Cash Advance Limit Is Lower Than Your Credit Limit

Amex sets the cash advance sub-limit as a separate risk control. Cash advances are considered higher risk than purchases because they carry no grace period and are harder to reverse. As a result, Amex caps the amount you can access in cash at a fraction of your total credit line.

This limit is set when the account is opened and is disclosed in your cardholder agreement. In most cases, you can’t raise it simply by requesting a change. A full credit review would typically be required, and even then, the outcome isn’t guaranteed.

How to Get a Cash Advance PIN for Your Amex Card

Here’s something that catches a lot of people off guard. To withdraw cash from an ATM using your Amex card, you need a separate PIN, specifically for cash advances. This is not the same PIN you might use for chip-and-PIN purchases in some countries.

If you’ve never set one up, you won’t be able to complete an ATM transaction, no matter how much available cash advance credit you have.

⚠️ Mistake to Avoid: Many cardholders assume their existing Amex account PIN works at ATMs for cash. It doesn’t. Your cash advance PIN must be requested separately. If you need cash today and haven’t set one up yet, the ATM method is not available to you on the same day. Plan ahead or use the bank branch method instead.

There are two ways to get your PIN set up.

Requesting Your Amex PIN Online

- Go to americanexpress.com and log in to your account.

- Navigate to the “Account Services” or “Card Management” section.

- Look for a “PIN Management” option and select it.

- Follow the steps to set or update your cash advance PIN.

- For security, Amex will typically mail your PIN separately rather than display it on screen. Standard delivery takes 7 to 10 business days.

This method works well if you’re planning ahead. It won’t help you if you need cash today.

Requesting Your Amex PIN by Phone

- Call the customer service number printed on the back of your Amex card.

- When connected, ask specifically to set up or update your ATM PIN for cash access. Be clear that you mean a cash advance PIN, not a general account PIN.

- Have your account number, Social Security number, or other verification details ready before you call.

- Ask the representative to confirm when the PIN will arrive and how it will be delivered.

Phone requests follow the same delivery timeline as online requests: expect 7 to 10 business days for the PIN to arrive by mail.

How to Get Cash from Your Amex Card at an ATM

With your PIN in hand and your cash advance limit confirmed, you’re ready to complete the transaction. Here’s exactly what to do.

Before you approach the ATM, have these three things ready:

- Your Amex card

- Your cash advance PIN

- Your available cash advance balance (so you don’t attempt more than the limit allows)

Step-by-step ATM process:

- Find an ATM that accepts Amex (see the subsection below for help locating one).

- Insert your Amex card.

- Enter your cash advance PIN when prompted.

- On the main menu, look for “Credit” or “Cash Advance” as an account type. Do not select “Debit,” “Checking,” or “Savings.” Selecting the wrong account type will result in a declined transaction.

- Enter the amount you want to withdraw. Keep it at or below your available cash advance balance.

- Confirm the transaction. The ATM screen will show any ATM operator fee before you finalize. You can cancel here if the fee is too high.

- Collect your cash and your receipt. Keep the receipt. It confirms the transaction amount and any fees charged at the ATM.

If the transaction is declined, check three things: confirm your cash advance limit is sufficient, confirm the PIN was entered correctly, and confirm the ATM displays the correct network logo (see below).

💡 Pro Tip: Some ATMs have a separate daily withdrawal limit that’s lower than your card’s cash advance limit. If your card has a $2,000 cash advance limit but the ATM caps daily withdrawals at $500, you can only take $500 per day from that machine. Check the ATM’s on-screen limit before you start the transaction.

Which ATMs Accept Amex for Cash Advances

Not every ATM accepts Amex, and not every ATM that accepts Amex for purchases will also process cash advances.

- Look for ATMs that display the Amex logo, or the logo of the network printed on the back of your specific card (Visa or Mastercard for co-branded Amex cards).

- Citibank ATMs are among the most commonly cited partners for Amex Express Cash transactions in the United States.

- Use the Amex ATM locator at americanexpress.com to find nearby participating machines before you leave home.

- If you’re at an ATM that shows your card’s network logo but the cash advance still declines, try a different machine. Some ATMs accept the card for purchases, but are not enrolled for credit card cash advance transactions.

What Amex Express Cash Is

If you see the phrase “Express Cash” in your Amex account or on ATM signage, this is Amex’s branded name for its ATM cash access program. It’s not a separate product. It’s simply what Amex calls a cash advance accessed at an ATM.

To use Express Cash, your card must be enrolled, and you must have a PIN set up. Both are handled through the same account portal or phone process described above. The same fee structure that applies to any Amex cash advance also applies to Express Cash transactions.

How to Get Cash from Amex Without an ATM

Don’t have your PIN yet? Can’t find a compatible ATM? Or do you need a larger amount than the daily ATM limit allows? There are two other ways to access cash through your Amex account.

Getting a Cash Advance at a Bank Branch

This is the most accessible non-ATM option, and it doesn’t require a PIN.

- Walk into any bank that processes transactions on the Amex network. Most major U.S. banks can handle this.

- Bring your Amex card and a valid government-issued photo ID (driver’s license or passport).

- Tell the teller you’d like a cash advance on your credit card and specify the amount.

- The teller processes the transaction on the Amex network and gives you the cash.

No PIN is needed for in-person teller advances in most cases because the teller verifies your identity directly. Your Amex transaction fee still applies. The bank may also charge its own teller service fee for processing a credit card cash advance. Ask about this before the transaction is finalized.

Using Amex Convenience Checks

Amex occasionally mails convenience checks to eligible cardholders. These look like personal checks but draw from your card’s credit line rather than a bank account.

You can deposit one just like a regular check. The funds will appear in your bank account within the standard bank processing window.

The important thing to know: convenience checks are treated as cash advances. The same fee applies, and interest starts accruing from the date the check is deposited. In some cases, the fee on convenience checks is even higher than on standard ATM withdrawals.

If you haven’t received convenience checks and think your account might qualify, you can call Amex to ask. They’re not available to all cardholders.

Amex Cash Advance Fees: What You Will Pay

A cash advance is not a free transaction. Before you complete one, you need to know exactly what you’ll be charged.

There are two separate fees. They apply simultaneously to ATM withdrawals, and both appear on your next statement as separate line items.

The Amex Transaction Fee for Cash Advances

Amex charges a cash advance transaction fee on every cash withdrawal. According to American Express, the current rate on most cards is 5% of the transaction amount or $10, whichever is greater.

Here’s what that means in real terms:

| Withdrawal Amount | Amex Transaction Fee (5%) |

|---|---|

| $100 | $10.00 (minimum applies) |

| $200 | $10.00 (minimum applies) |

| $300 | $15.00 |

| $500 | $25.00 |

| $1,000 | $50.00 |

For smaller withdrawals under $200, the $10 flat minimum kicks in. For anything over $200, the 5% rate applies.

This fee is charged on the transaction date, not at the end of the billing cycle. It shows up immediately.

Always verify your specific card’s fee in your cardholder agreement before making a withdrawal. Rates can vary by card product, and Amex may update terms over time.

ATM Operator Fees on Amex Cash Advances

On top of the Amex transaction fee, the ATM operator often charges its own surcharge. This is the fee from whoever owns the ATM machine, not from Amex. It’s separate and completely outside Amex’s control.

ATM operator fees typically range from $2 to $5 per transaction, though some machines charge more.

The good news: the ATM screen will display this fee before you confirm the transaction. You have the option to cancel at that point if the surcharge seems too high. If you cancel, no transaction takes place, and no fee is charged.

Using an ATM through the Amex Express Cash partner network (such as certain Citibank ATMs) may reduce or eliminate the operator surcharge. It’s worth checking the ATM locator to find a partner machine if surcharge cost is a concern.

How Cash Advance Interest Works on Amex

The fees above are just the upfront cost. The interest is where cash advances can become genuinely expensive, especially if you don’t repay the balance quickly.

The most important rule to understand is this: there is no grace period on cash advances.

Why Cash Advances Have No Grace Period

Standard credit card purchases come with a grace period. If you pay your balance in full by the due date, you pay zero interest on those purchases. That grace period typically runs 21 to 25 days from the statement closing date.

Cash advances are different. Interest starts on the day you take the cash, not on the statement date, not on the due date. There is no window where the balance is interest-free.

This rule applies to all credit card cash advances, not just Amex. The Consumer Financial Protection Bureau notes that cash advances typically gain interest immediately, which is a key distinction borrowers often miss.

The rule is required to be disclosed in your cardholder agreement under Regulation Z, which governs credit card disclosures in the United States.

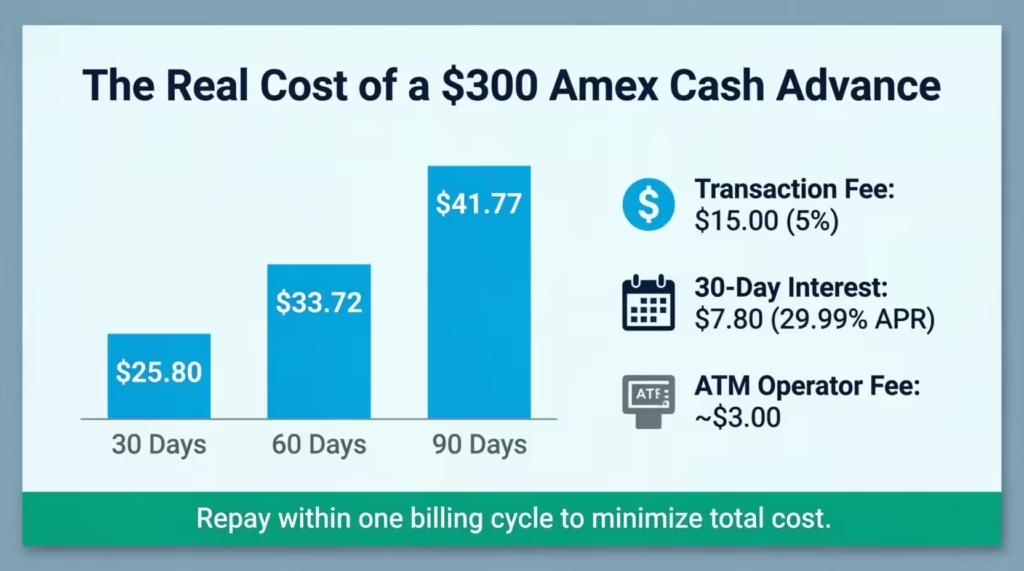

What a Cash Advance Actually Costs: A Worked Example

Let’s put real numbers to this.

Say you take a $300 cash advance on an Amex card with a 29.99% cash advance APR and the standard 5% transaction fee.

Day 1 – Transaction date:

- Cash advance fee (5%): $15.00

- Amount withdrawn: $300.00

- Total charged to account on Day 1: $315.00

Interest calculation for 30 days:

To find the daily periodic rate, divide the APR by 365:

29.99% / 365 = 0.0821% per day

Daily interest on $315: $315 x 0.000821 = $0.26 per day

Over 30 days: $0.26 x 30 = $7.80 in interest

Total cost of a $300 cash advance carried for 30 days:

- Transaction fee: $15.00

- 30 days of interest: $7.80

- ATM operator fee (estimate): $3.00

- Total cost: $25.80 on a $300 withdrawal

That’s 8.6% of the amount withdrawn, paid in the first month alone.

If the balance is carried longer, the cost compounds:

| Time Carried | Total Interest Accrued | Total Cost (incl. fees) |

|---|---|---|

| 30 days | $7.80 | $25.80 |

| 60 days | $15.72 | $33.72 |

| 90 days | $23.77 | $41.77 |

These numbers use a 29.99% APR and 5% transaction fee for illustration. Verify your specific card’s rate before calculating your own scenario.

📌 Did You Know: Payments you make to your Amex account are typically applied to the lowest-APR balance first. This means if you carry a purchase balance at a lower rate alongside a cash advance balance, your payment reduces the purchase balance first, leaving the higher-rate cash advance accruing interest the longest.

How a Cash Advance Affects Your Credit Score

Taking a cash advance can affect your credit score, but not in the way many people expect.

A cash advance does not appear on your credit report as a separate negative item. It doesn’t show up labeled as a cash advance, and it doesn’t trigger a hard inquiry. Credit bureaus don’t distinguish between a cash advance balance and a purchase balance within the same account. From their perspective, it all looks like a credit card balance.

What does affect your score is credit utilization. Credit utilization is the ratio of your current card balance to your total credit limit. It’s one of the most important factors in your FICO Score calculation.

If your Amex card has a $10,000 credit limit and you take a $2,000 cash advance, your card balance rises by $2,000. If your pre-existing purchase balance was already $3,000, your total balance is now $5,000 on a $10,000 limit. That’s 50% utilization, which is high. Financial experts generally recommend keeping utilization below 30%.

The impact on your score depends on the size of the withdrawal relative to your credit limit and your existing balance. A small cash advance that you repay within the same billing cycle will have minimal lasting effect. Your next statement will show the lower balance, and your reported utilization will drop back down.

If you’re preparing to apply for a mortgage, car loan, or any other credit product, timing matters. A cash advance that raises your utilization significantly could temporarily lower your score, even if only for one billing cycle. Consider repaying it before your statement closes if you’re in that situation.

Cheaper Alternatives to an Amex Cash Advance

A cash advance is a fast way to access cash, but it’s rarely the cheapest. Before you confirm the transaction, it’s worth spending 60 seconds considering whether one of these options fits your situation better.

Personal Loan or Credit Union Loan

If you can wait 24 to 48 hours, a personal loan is almost always cheaper than a cash advance.

Personal loan APRs typically range from 7% to 20% for borrowers with good credit, compared to the 25% to 29.99% cash advance APR on many Amex cards, plus the upfront fee. That difference compounds fast if you carry the balance for more than a few weeks.

Credit union emergency loans are especially competitive. Existing members often qualify quickly, and some credit unions process approvals the same day. Online personal loan lenders like Marcus or LightStream can fund within one business day for approved applicants.

Best suited for: readers who need $500 or more, don’t need the cash within the next few hours, and can qualify for a personal loan.

Using a Debit Card or Direct Bank Withdrawal

This one sounds obvious, but it’s worth stating directly: if you have funds in a checking or savings account, a debit card, an ATM withdrawal, or a bank teller withdrawal costs nothing or very little.

Some readers searching for ways to access cash from a credit card haven’t stopped to check whether a simpler option is already available to them. A bank ATM withdrawal from your own account typically costs $0 at in-network ATMs and $2 to $5 at out-of-network machines, which is still far less than a credit card cash advance.

Check your account balance before proceeding with a cash advance.

Why Payment Apps Are Usually Not a Cheaper Alternative

This is a common workaround that often backfires. If you use Venmo, PayPal, Cash App, or a similar platform to send money to yourself or another person, and you fund that transaction with your Amex credit card, the issuer typically classifies it as a cash advance.

That means the same 5% transaction fee and the same immediate interest rate kick in, the same as if you had gone to an ATM.

The exception: if you fund the payment app from your bank account or debit card, it’s not a cash advance. The classification depends entirely on the funding source, not the app itself.

Before using a payment app as a workaround, check how the app handles credit card funding. Most major apps list this in their terms, and some explicitly warn that credit card transactions may be treated as cash advances by the card issuer.

Using Your Amex to Get Cash While Traveling Internationally

Using your Amex card for a cash advance abroad is possible, but the cost structure is different from domestic withdrawals. There are also practical access considerations that don’t apply at home.

The standard Amex cash advance fee still applies. On top of that, most non-travel-oriented Amex cards charge a foreign transaction fee on international transactions.

Foreign Transaction Fees on Amex Cash Advances

The foreign transaction fee on most standard Amex cards is 2.7% of the transaction amount. This applies on top of the regular 5% cash advance fee.

So on a $300 international cash advance, your fees look like this:

- Cash advance fee (5%): $15.00

- Foreign transaction fee (2.7%): $8.10

- ATM operator surcharge (varies): $3.00 to $7.00

- Total fees before interest: $26.10 to $30.10

Then interest starts accruing from Day 1, as it does on all cash advances.

Premium Amex travel cards, including some versions of the Amex Platinum, waive the foreign transaction fee entirely. Check your specific card’s fee schedule before traveling. This information is in your cardholder agreement and on the Amex website under your account.

Finding ATMs That Accept Amex Overseas

Amex is accepted at fewer international ATMs than Visa or Mastercard. In major cities and tourist areas, you’ll generally find ATMs that work. In smaller towns or rural regions, the options narrow quickly.

Use the Amex ATM locator on americanexpress.com before you travel to identify which ATM locations in your destination accept Amex cash advances. This is worth doing in advance, not when you’re standing on a street corner at 9 PM.

One more warning for international ATM withdrawals: decline dynamic currency conversion (DCC) if offered.

Dynamic currency conversion is when an ATM asks whether you want to complete the transaction in U.S. dollars instead of local currency. It sounds convenient, but the exchange rate the ATM applies is almost always worse than the rate Amex uses. Choosing local currency lets Amex handle the conversion, which typically gives you a better rate.

Always choose the local currency option when traveling internationally.

When an Amex Cash Advance Is Worth It (and When It Is Not)

After looking at the fees, interest, and alternatives, here’s a simple framework for making the final decision.

A cash advance is a defensible choice when:

- You have a genuine, immediate need for physical cash with no realistic alternative available right now

- You’re confident you can repay the full amount within 7 to 14 days

- The total fee and interest cost are acceptable, given the urgency of your situation

- No personal loan, debit account, or other lower-cost option is accessible in time

A cash advance is a poor choice when:

- You expect to carry the balance for more than one billing cycle

- A personal loan or credit union loan is accessible within your timeframe

- You have available funds in a bank account you haven’t checked

- The need isn’t urgent enough to justify the immediate 5% fee plus accruing interest

The simplest repayment test: if you can pay the full cash advance balance before or on your next statement due date, the total cost is the transaction fee plus a few days of interest, which may be manageable for a real emergency. If you can’t pay it off that quickly, the interest compounds at a high daily rate, and cheaper borrowing options will almost always serve you better.

A cash advance exists for genuine emergencies. It’s not a cost-effective way to access cash regularly, and the fee and interest structure make it one of the more expensive short-term borrowing options available on a credit card.

Frequently Asked Questions (FAQs)

How much is a cash advance fee for $1,000?

On most Amex cards, the cash advance fee is 5% of the transaction amount, so a $1,000 withdrawal costs $50 in transaction fees alone. Add the ATM operator surcharge and immediate interest accrual from Day 1, and the true cost climbs higher before your next statement arrives.

Can I withdraw $2,000 from my credit card?

Whether you can withdraw $2,000 depends on your card’s cash advance sub-limit, which is a separate ceiling from your total credit limit and is often set between 20% and 30% of it. Log in to your Amex account and check your cash advance limit before attempting the withdrawal, since many cardholders find that this number is lower than expected.

Can you withdraw $5,000 cash from a credit card?

A $5,000 cash advance is only possible if your card’s cash advance sub-limit is at or above that amount, which is uncommon on most standard Amex revolving credit cards. Even if your total credit limit is high, most cash advance limits are set far below $5,000, and daily ATM withdrawal caps add another restriction on top.

Can I transfer money from my Amex credit card to my bank account?

Amex doesn’t offer a direct credit-to-bank transfer feature, but you can deposit an Amex convenience check into your bank account if your card is eligible for them. Contact Amex to ask whether your account qualifies, since convenience checks aren’t available to all cardholders and are treated as cash advances with fees and immediate interest.

What ATMs accept American Express cards?

ATMs displaying the American Express logo or the Visa or Mastercard network logo on co-branded Amex cards will typically process cash advances. Citibank ATMs are among the most widely cited U.S. partners, and the Amex ATM locator at americanexpress.com can identify participating machines near you.

How much can I borrow with a cash advance?

Your borrowing limit for a cash advance is set by your card’s cash advance sub-limit, not your total credit limit, and it’s typically 20% to 30% of the total. Your available amount also decreases as your purchase balance rises, so check the specific number in your Amex account before planning a withdrawal.

Is it a good idea to get a cash advance on a credit card?

A cash advance makes sense only for genuine emergencies where no cheaper option is available, and you can repay the full balance within one billing cycle. The combination of a 5% upfront fee and immediate high-APR interest with no grace period makes cash advances one of the more expensive short-term borrowing options available on a credit card.

How long does it take to get an Amex cash advance PIN?

After requesting a cash advance PIN online or by phone, Amex mails it separately for security, which typically takes 7 to 10 business days. If you need cash today and don’t have a PIN, the bank branch teller method is your best same-day option since it doesn’t require a PIN.

Can Amex convenience checks be deposited at any bank?

Yes, Amex convenience checks can be deposited at any bank just like a personal check, but they draw from your card’s credit line rather than a bank account. They’re treated as cash advances, so the same transaction fee applies, and interest begins accruing from the deposit date.

Does taking a cash advance reduce my available credit for purchases?

Yes. A cash advance draws from your total credit line, so the amount you withdraw is no longer available for purchases until you repay it. If your purchase balance is already high, your available cash advance amount may be lower than your stated cash advance limit for the same reason.

Bottom Line

Getting cash from your Amex card is straightforward once you know the steps. First, confirm your card is a revolving credit card that supports cash advances. Find your cash advance sub-limit before you approach an ATM. Set up your PIN at least 7 to 10 days before you need it.

Then choose the method that fits your situation, whether that’s an ATM, a bank branch, or a convenience check. Based on the fee and interest structure, repaying the balance within one billing cycle keeps the total cost manageable. If you can access a personal loan or your own bank account instead, those options are almost always cheaper.

If this guide helped you avoid a costly surprise, consider sharing it with a friend who uses Amex regularly. They may not know these rules yet, and a quick share could save them real money.