Getting a sudden preset spending limit on your American Express card feels frustrating. One day, your charge card has the flexible spending you signed up for. The next day, you see a hard cap on what you can buy. Even worse, this Amex preset spending limit can block credit limit increases on your other Amex cards, too. We get it. This guide breaks down why it happened, what works, and what doesn’t.

To remove an Amex preset spending limit, pay your balance in full before each statement closing date, keep total credit utilization below 10%, and wait for Amex to restore NPSL status during a future soft pull review.

Below, you’ll find the exact steps, real timelines, and the small habits that move the needle fastest.

Key Takeaways

This guide explains how to remove a preset spending limit on an American Express charge card, covering why Amex assigns the cap, which account behaviors trigger monthly review decisions, and how long restoration of NPSL status typically takes across three risk levels.

Core Facts:

- A preset spending limit is a fixed dollar cap Amex places on a charge card originally issued as No Preset Spending Limit (NPSL), meaning the card declines any purchase above the assigned number regardless of your intention to pay in full.

- The most effective way to restore NPSL status is to pay your Amex balance in full before the statement closing date each month, because Amex reports your balance to the credit bureaus on that date, not on the payment due date.

- Amex runs a monthly soft pull review of your full credit report near each statement closing date, checking utilization across all your cards, FICO score trend, new inquiries, and payment history with Amex.

- A preset cap on any one Amex card freezes credit limit increase requests on every other Amex card you hold, including co-branded cards like Delta SkyMiles and Hilton Honors Amex, until the cap is removed.

- Standard risk cases (triggered by high utilization or a minor FICO drop) typically resolve within 3 to 6 months of consistent clean behavior; extended risk cases involving financial reviews can take 6 to 18 months.

- Calling Amex at 1-800-528-4800 to request a supervisor-level manual review can accelerate the process when something has clearly improved in your credit profile, but phone agents cannot directly override the risk model decision.

Best for:

- Amex Platinum, Gold, or Green cardholders who recently received a preset spending limit notice and want to understand what triggered it and how to reverse it.

- Cardholders whose preset cap on one Amex card is blocking credit limit increases or new card approvals across their full Amex portfolio.

- Anyone currently in a monthly soft pull review cycle who wants to know which specific behaviors move the risk model toward restoring flexible NPSL spending.

What It Means When Amex Assigns a Preset Spending Limit

A preset spending limit is a fixed dollar cap set by American Express. This applies to a charge card account that was initially sold as having No Preset Spending Limit (NPSL). Once this cap is in place, your card stops behaving like a flexible charge card. It starts behaving like a traditional credit card with a hard ceiling.

This is a real change to how your account works. With true NPSL, your spending power adjusts based on your purchase history, payment record, and credit profile, as American Express explains in its official NPSL terms.

You may have spent $4,000 one month and $14,000 the next without issue. After a preset limit is assigned, you can only spend up to the assigned number. If your limit is set at $5,000, your card will decline at $5,001. That is a sharp departure from the card’s original design.

American Express must notify you when this change happens. You will usually receive a letter, an email, or a secure message inside your online account. Some users also see an Adverse Action Notice if the limit was triggered by credit risk. The notice usually lists the broad reasons, like high balances or recent credit pulls, but it rarely tells you the exact internal trigger.

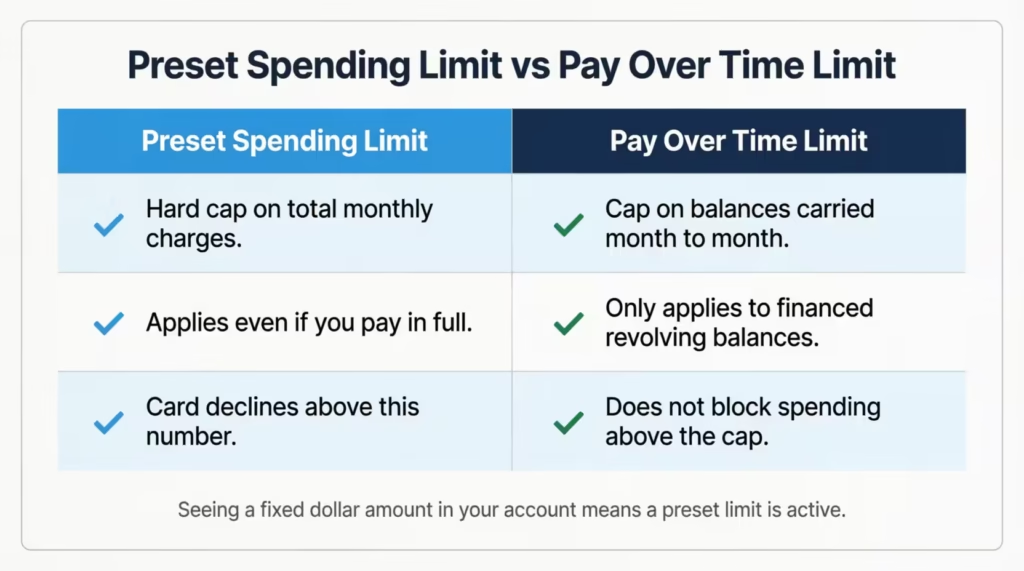

The Difference Between Your Preset Limit and Your Pay Over Time Limit

These two limits look similar in the app but do very different things. Mixing them up leads to the wrong fix.

A Pay Over Time Limit is the maximum balance you can carry from one month to the next on eligible purchases. It only applies if you enrolled in Pay Over Time, which lets you finance charges of $100 or more with interest. This limit affects revolving balances, not your total monthly spending.

A preset spending limit is a hard cap on how much you can charge in a single billing cycle, full stop. It applies even if you plan to pay the bill in full at the end of the month. So a Pay Over Time Limit of $2,000 does not stop you from charging $15,000 if you pay in full. A preset spending limit of $5,000 does stop you, no matter how you plan to pay.

If you see “Available to Spend” with a dollar figure that does not refresh after you pay, you likely have a preset spending limit. If you only see a Pay Over Time cap, your card is still NPSL.

Why American Express Assigns a Preset Spending Limit

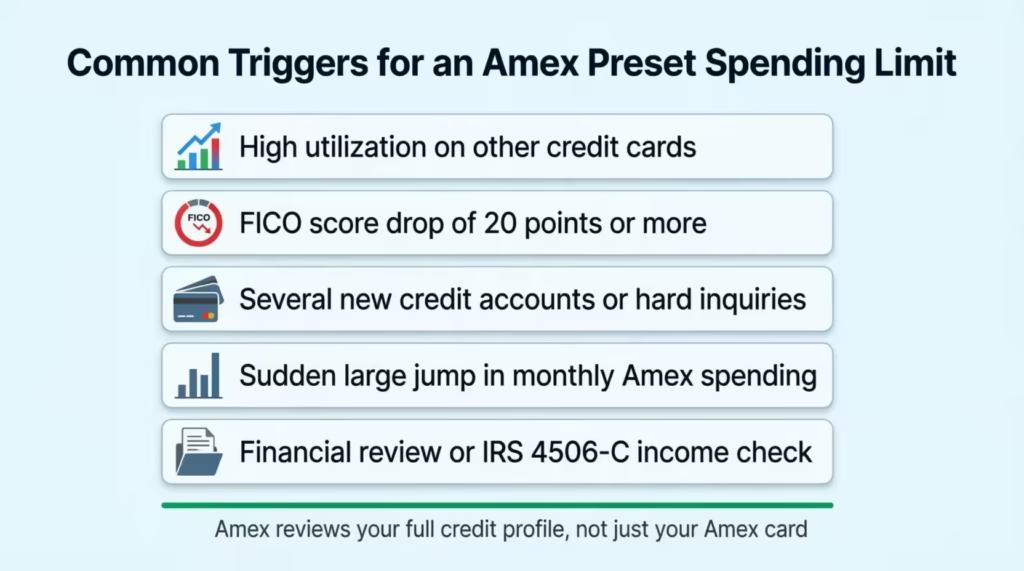

American Express does not assign a preset cap at random. It happens when their risk model flags something in your overall credit profile or your spending behavior. Most triggers fall into a handful of patterns, and many of them have nothing to do with your Amex card itself.

The most common trigger is rising credit utilization on your other credit cards. Experian reports that the average overall credit utilization in the U.S. was 29% in Q3 2024.

If your utilization sits well above that, Amex’s model may treat it as a stress signal, even if you always pay your Amex bill on time. Carrying high balances on a Chase, Citi, or Discover card can pull a preset limit on your Platinum or Gold card.

Other common triggers include:

- A drop in your FICO score, often 20 points or more

- Several new credit accounts or hard inquiries in the past 12 months

- A sudden, large jump in monthly Amex spending without a matching income signal

- Carrying balances month to month on revolving cards

- A flagged financial review where Amex asks for tax returns or bank statements

A financial review (sometimes called the “4506-C” review) is a deeper check. Amex pulls your tax transcript directly from the IRS to verify the income you reported. If you decline the review or your verified income is lower than expected, a preset spending limit often follows. The cap is the system’s way of reducing exposure while you stay on the account.

📌 Did You Know: Amex’s risk model looks at all your credit cards, not just your Amex ones. A maxed-out store card from another bank can quietly trigger a preset cap on your Platinum card, even if your Amex usage is perfect.

Where to See the Preset Limit in Your Amex Account

You can confirm a preset limit in two places. On the web at americanexpress.com, log in and open the affected card. Look at the panel on the right side of the account home page. With true NPSL, you will see “No Preset Spending Limit” listed. With a preset cap, you will see a dollar figure next to “Available to Spend” or “Total Credit Line.”

In the Amex mobile app, tap on the card, then look under the balance summary. The same labels apply. If you tap “View Details” or scroll to the credit limit area and see a hard number with a percentage used, the cap is active.

A quick way to double-check: pay your balance down to zero. With NPSL, the “Available to Spend” amount will not show a fixed cap. With a preset limit, the figure will refresh and clearly show the same number every month.

How a Preset Limit on One Card Affects Your Other Amex Accounts

This is the part most cardholders find out the hard way. A preset spending limit on one Amex card freezes credit limit increases (CLI) on every other Amex card you own. If you have both Gold and Platinum, and Gold has a preset cap, your Platinum CLI requests will be denied for the same risk. This happens even though Platinum is still technically NPSL.

The reason is that Amex treats your entire customer relationship as one risk file. When the underwriting model puts a cap on any account, it tags your customer ID as elevated risk. That tag blocks new credit on any Amex product. It also blocks new card approvals during this window. Many users report that applying for a new Amex card while a preset cap is active leads to instant denial, regardless of credit score.

Co-branded cards feel this, too. Your Delta SkyMiles or Hilton Honors Amex CLI requests will be frozen. This happens even though those cards are issued by another brand. The underwriting still flows through Amex’s risk engine, so the freeze applies.

This blocking effect is what makes the preset limit so painful. It is not just one card with reduced spending power. It is your entire Amex ecosystem stuck in place until the cap comes off.

Whether Calling American Express Can Help Remove the Limit

This is the question almost every cardholder asks first. The short answer: calling can help in specific situations, but it cannot directly reverse the decision. The preset limit was set by Amex’s risk algorithm. Phone agents do not have a button that turns it off.

What a phone agent can do is escalate your case to a supervisor or to the account management team. They can also note the file that you want to submit supporting documents for a manual review. A senior representative can sometimes ask for your account to be re-evaluated before the next monthly review. The Amex customer service line for this is 1-800-528-4800.

The catch: the re-evaluation still runs through the same risk model. If nothing has changed in your credit profile, the answer will be the same. Calling helps most when something has clearly improved. Maybe you paid off a large balance, finished a financial review, or had an inquiry drop off your report. In those cases, asking for a re-review can shave weeks or months off the wait.

⚠️ Mistake to Avoid: Calling repeatedly and asking the same agent to “just remove the limit” wastes your time and can flag your account as high-contact. Call once, ask for the supervisor or backend team review, and then wait.

What to Say When You Call Amex

Keep the call focused and polite. Long arguments do not help. Try this approach:

- Identify yourself and the card affected.

- Say: “I received notice of a preset spending limit on my account. I’d like to request a supervisor or backend review to see if my account can be re-evaluated for restoration of No Preset Spending Limit status.”

- Mention any positive changes since the limit was set. Examples: paid off a large balance, income increased, inquiries aged off, and completed a financial review.

- Ask if there is documentation you can submit to support the review.

- Take the agent’s name and reference number for the case.

Avoid threats to close accounts or aggressive language. Amex agents have wide discretion to push a review forward or hold it back. A calm, prepared cardholder gets more help than an angry one.

Documents Amex May Ask You to Provide

If Amex agrees to a manual review, they may request paperwork to verify your financial picture. The most common documents include:

- The last two or three months of bank statements (checking and savings)

- Recent pay stubs, usually the last two to three pay periods

- Your most recent federal tax return, or IRS Form 4506-C, which lets Amex pull a tax transcript directly

- For self-employed cardholders: profit and loss statements or 1099 forms

- Proof of large assets, like brokerage or retirement account statements, if relevant

Send only what they ask for. Upload through the secure document portal in your Amex account when possible, not by email. Keep copies of everything for your records. Amex usually responds within 30 days, though some reviews take longer.

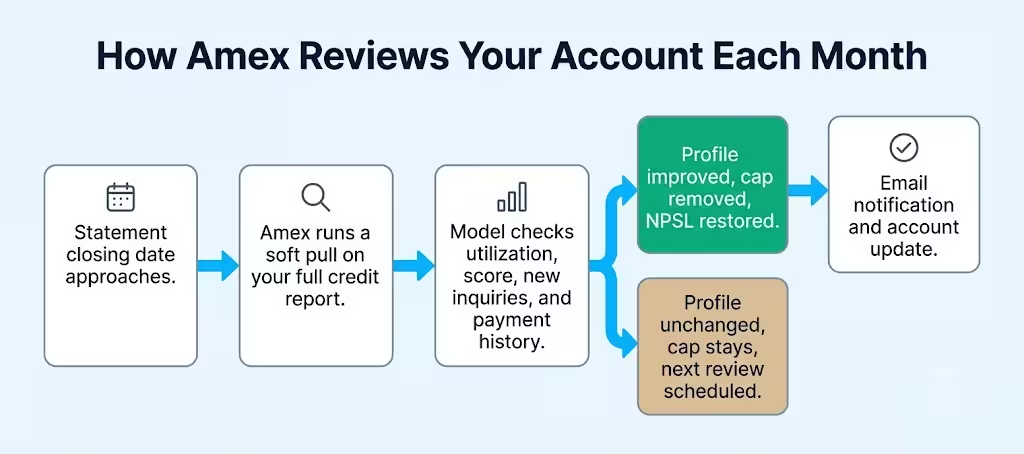

How American Express Reviews Your Account After Assigning a Preset Limit

Once a preset cap is on your account, Amex does not just forget about you. The risk team runs a monthly soft pull on your credit file, usually timed close to your statement closing date. A soft pull does not hurt your credit score, but it pulls a fresh snapshot of your overall credit picture.

During each review, Amex checks several things:

- Your reported balances across all credit cards, not just Amex

- Your total credit utilization

- New credit applications and hard inquiries

- Late payments or collections, even on accounts at other banks

- Your FICO score trend, up or down

- Your payment history with Amex over the last several billing cycles

The model is looking for steady improvement. One good month is not enough. Three to six months of clean behavior is the usual baseline for the algorithm to reconsider. For accounts placed on a cap after a financial review or fraud flag, the wait can be longer.

You will not get a notice every time a soft pull happens. You may only find out when something changes. One day, the dollar figure on your account home page disappears and is replaced with “No Preset Spending Limit.” That is the signal that the most recent review went in your favor.

How to Use the Check Spending Power Tool During This Period

The Check Spending Power tool inside your Amex account lets you enter a planned purchase amount and instantly see whether the charge will be approved. This is useful when you are stuck with a preset cap and want to avoid a declined transaction at the register.

Log in to your account online or in the app. Find the Check Spending Power link on your card’s home page, usually near the payment summary. Enter the dollar amount you plan to spend. The tool returns a yes or no in seconds, with no hard pull and no impact on your credit score.

Use this tool sparingly. Some users on the myFICO forums and the r/amex subreddit report that checking very large amounts repeatedly, especially amounts well above your typical spending, can flag the account for an extra review. A few normal checks per month is fine. Twenty checks in a week for $50,000 each is asking for trouble. Use it for real planned purchases, not as a way to “test” your limit.

What to Do to Get the Preset Limit Removed

This is the part most articles skip over. The fix is not one big action. It is a set of small, repeated behaviors that the risk model rewards over several monthly reviews.

The single most important habit is paying your balance in full before the statement closing date each month. Not just by the due date. Before the statement cuts. Doing this makes your card report a $0 or very low balance to the credit bureaus. Your overall reported utilization drops, which is exactly what the soft pull review wants to see.

Other actions that move the needle:

- Bring your total utilization across all credit cards below 10%. Below 5% is even better.

- Enroll in Amex AutoPay and set it for “Pay in Full” so you never miss a payment.

- Stop applying for new credit cards or loans. Each hard inquiry adds risk in the model’s eyes.

- Pay down any revolving balances at other banks, especially store cards with low limits.

- Keep using your Amex card for normal spending, but stay well below the preset cap. Charging up to 90% of the cap every month signals stress, not strength.

- Avoid returns, disputes, or chargebacks during this window, since they add friction to the file review.

💡 Pro Tip: Set up two AutoPay rules if your bank allows it. One pays your statement balance on the due date as backup. The other pays the current balance two days before your statement closes. This combination lowers reported utilization without ever risking a late payment.

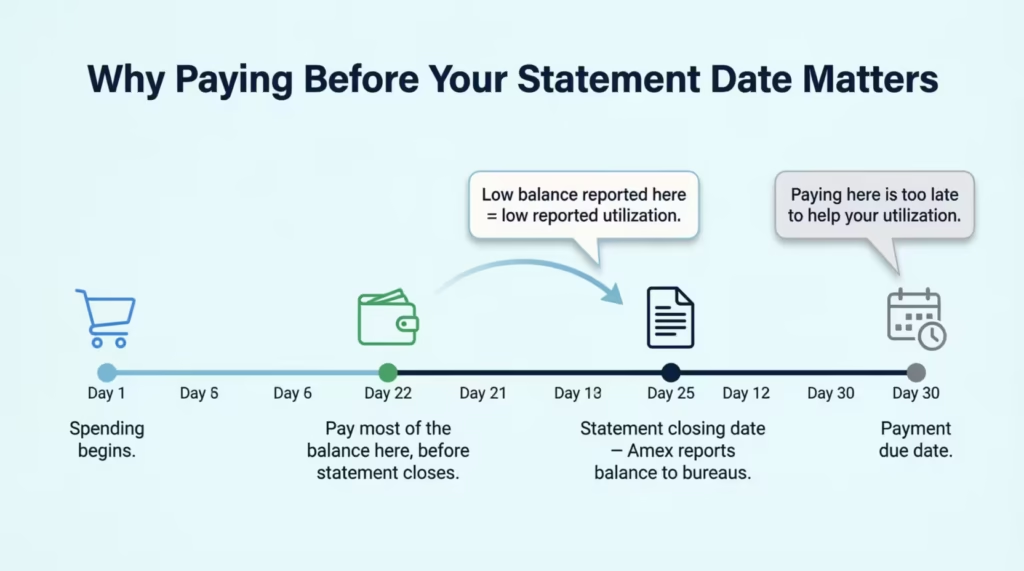

Why Paying Before Your Statement Date Matters More Than Paying by the Due Date

Most cardholders think paying by the due date is enough. For avoiding interest and late fees, yes. For getting a preset limit removed, no.

Here is why. Amex reports your balance to the credit bureaus on your statement closing date. That reported balance is the number that shows up on your credit report and feeds into your utilization calculation.

If you spend $4,000 on your Gold card and pay it off the day after the statement cuts, your credit report still shows a $4,000 balance for that month. Your utilization spikes, and the soft pull review sees a stressed file.

Now reverse it. Spend $4,000 during the cycle, but pay $3,800 of it three days before the statement closes. Amex reports a $200 balance. Your utilization on that card looks tiny. The soft pull review sees a calm, in-control account.

Do this every month for three to six cycles. The risk model starts seeing a pattern of low reported balances and consistent payments. That pattern is exactly what triggers the removal of a preset cap.

Lowering Utilization on All Cards, Not Just Your Amex

This is the step that catches most people off guard. Even if your Amex card reports $0 every month, a maxed-out Chase Freedom or Discover It card can keep the preset cap in place. Amex looks at your entire credit report, not just its own products.

Pull a free copy of your credit report at AnnualCreditReport.com. Check each card’s reported balance and credit limit. Calculate the utilization on each one. If any card is above 30%, that is a problem. If any card is above 50%, that is a bigger problem. Pay those balances down first, even if you have to skip Amex spending for a month to free up cash.

For Sarah, a marketing manager at a Seattle consulting firm, the fix took about four months. Her Amex Gold had a $4,000 preset cap because her Capital One card was sitting at 78% utilization.

She redirected $1,200 a month to the Capital One balance while paying her Gold in full before each statement. After the fourth monthly soft pull, the preset cap dropped off her Gold card. Her overall utilization had gone from 41% to 8% in that window.

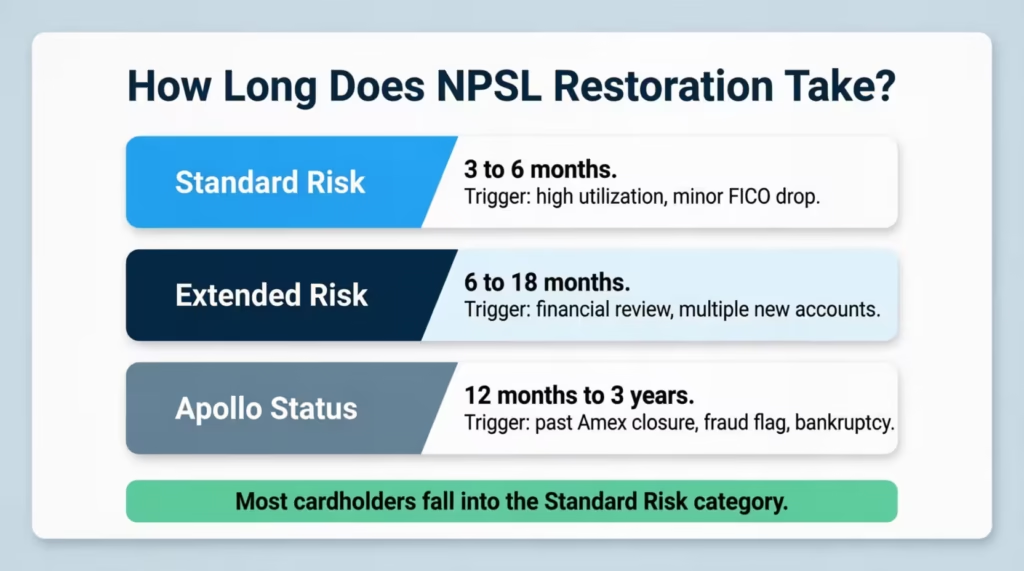

How Long Does It Realistically Take to Get Back to NPSL

There is no published timeline from Amex. But based on patterns reported across the r/amex and myFICO communities, the wait usually falls into three buckets.

| Risk Level | Typical Removal Timeline | Common Triggers |

|---|---|---|

| Standard risk | 3 to 6 months | High utilization, minor FICO drop |

| Extended risk | 6 to 18 months | Financial review, multiple new accounts |

| Apollo / Reinstatement watch | 12 months to 3 years | Past Amex closure, bankruptcy, fraud flag |

Standard risk cases are the most common. If your preset cap appeared after a few months of high utilization, expect three to six monthly reviews of clean behavior before the cap lifts. Some users report removal in as few as two months when their improvement is dramatic.

Extended risk is for cardholders who have gone through a full financial review or who had several risk factors stack up at once. Six to 18 months is normal here. The risk model wants a longer track record before it changes course.

Apollo is Amex’s internal program for cardholders with a tough history. This can happen after a previous closure. These accounts can stay capped for years, even with perfect recent behavior. If you suspect you are in this group, calling customer service rarely helps. Patience and steady payments are the only real path.

Amex Platinum Preset Spending Limit: What Is Different

The Platinum card sits in a special spot. With an annual fee of $695 as of 2025, cardholders expect the full NPSL flexibility from day one. When a preset cap lands on a Platinum account, the impact feels heavier.

Two differences stand out. First, a preset cap on Platinum almost always blocks CLI on the co-branded Amex cards in your wallet, like the Delta SkyMiles Reserve or the Hilton Honors Aspire. The freeze extends to your full Amex relationship, including business cards if you have them under the same customer ID.

Second, Platinum cardholders often get a slightly longer rope. Because the risk model knows you are paying a premium fee, it may give the account a chance to recover before assigning a cap. But once a cap is on a Platinum, removal can take longer than on a Gold or Green card, because Amex treats Platinum accounts with extra scrutiny.

If your Platinum has a preset cap, do this:

- Pay before the statement closes.

- Lower your overall utilization.

- Avoid new credit.

- Wait for the monthly soft pulls.

The annual fee does not buy faster removal.

What Happens When American Express Removes the Preset Limit

When the soft pull review finally goes your way, several things change at once. You will usually receive an email from Amex within a day or two. The subject line often reads something like “Update to your Card account” or “Good news about your American Express account.”

Log in to your account to confirm. The “Available to Spend” box should no longer show a hard dollar figure. Instead, you will see “No Preset Spending Limit” listed again. The card goes back to its flexible spending. Your spending power changes with your payment history and usage.

The other changes that follow:

- Credit limit increase requests on your other Amex cards become available again, usually within a few weeks.

- New Amex card applications may start being approved instead of auto-declined.

- Co-branded card CLI requests reopen.

- The monthly soft pulls do not fully stop, but they shift to a normal account-monitoring frequency rather than the focused review cycle.

Some users see a Membership Rewards bonus offer or a targeted upgrade offer in the months that follow, as Amex tries to rebuild the relationship. Take or ignore them based on your own plans.

One last note. NPSL status restored is not bulletproof. If you push utilization back up or pick up several new inquiries in the next few months, the preset cap can return. Many cardholders who recover from a first cap stay extra cautious for a year afterward. Keep the same habits in place. The same behaviors that earned the removal also keep it from coming back.

Frequently Asked Questions (FAQs)

Why did Amex lower my preset spending limit?

Amex sets a limit when its risk model sees warning signs in your credit profile. These signs include higher use of other cards, a lower FICO score, multiple new credit applications, or a sudden increase in monthly spending without a matching income. The trigger is often from a non-Amex card, not from anything wrong with your Amex account itself.

Can a preset limit on one Amex card affect my other Amex cards?

Yes. A cap on one of your Amex cards stops credit limit increase requests on all your other Amex cards. This includes co-branded cards like Delta SkyMiles and Hilton Honors. Amex treats your entire customer relationship as a single risk file, so the freeze applies to all products under your customer ID.

Why won’t Amex let me increase my limit?

If any card in your Amex portfolio has an active preset spending limit, Amex blocks credit limit increase requests on all of your other Amex cards until that cap is lifted. Restoring NPSL status on the capped card is the only way to reopen CLI eligibility across your accounts.

Does American Express Platinum have a preset spending limit?

The Platinum card is advertised as having no preset spending limit (NPSL). However, Amex can set a spending cap if its risk model raises concerns. This can happen with Gold or Green cards, too. Once a cap is placed on a Platinum, removal can take longer than on other Amex cards because Amex applies extra scrutiny to Platinum accounts.

Is Amex Gold really no limit?

The Amex Gold card is originally issued as NPSL, meaning your spending power adjusts based on your payment history and credit profile. However, Amex can place a fixed preset cap on the Gold account if your overall credit picture triggers their risk model, turning it into a card with a hard monthly ceiling.

Which Amex cards have no preset spending limit?

Amex’s charge cards, including the Platinum, Gold, and Green, are issued as NPSL products. However, NPSL is a feature Amex can remove by assigning a preset cap to any of these accounts if your credit profile raises a risk flag.

Does no preset spending limit affect a credit score?

NPSL itself does not damage your credit score, but how your balance is reported does. Amex reports your balance to the credit bureaus on your statement closing date, and that balance feeds into your utilization calculation. Charging heavily and paying after the statement cuts can still spike your reported utilization and lower your score.

How long does it take for my spending limit to reset?

For standard risk cases triggered by high utilization, three to six months of clean behavior typically leads to NPSL restoration. Accounts that have a financial review or several risk factors can take six to 18 months. Accounts with a history of closure or fraud flags may stay capped for one to three years.

What documents does Amex ask for during a financial review?

Amex usually asks for two to three months of bank statements. They also want recent pay stubs and your latest federal tax return. You can provide IRS Form 4506-C, too. This form lets Amex get your tax transcript straight from the IRS. Self-employed cardholders may also be asked for profit and loss statements or 1099 forms.

Wrapping Up

Removing a preset cap on an Amex card comes down to patience and a few steady habits. The decision sits with Amex’s risk model, not a phone agent, so the goal is to give the model the signals it wants to see.

To manage your Amex accounts effectively, follow these steps:

- Pay your Amex balance in full before the statement closing date.

- Keep your total credit utilization below 10% on all your cards.

- Avoid applying for new credit until your NPSL is restored.

This strategy can help maintain a healthy credit profile.

Most cases are clear within three to six monthly soft pull reviews.

If you know an Amex cardholder feeling stuck with a sudden spending cap blocking their other cards, share this guide. It could save them months of guessing.