I’ve been there myself, staring at my Amex account, trying to figure out exactly when my balance will hit the credit bureaus. Maybe you’re prepping for a mortgage, watching your utilization, or timing a new card application. The uncertainty is stressful because one wrong move can drop your score right before you need it.

The good news? Your Amex credit bureau reporting timeline follows a predictable pattern tied to your statement closing date.

This guide walks you through finding that date, understanding what gets sent, and timing your payments to achieve the best score.

Key Takeaways

This guide explains the when does Amex report to credit bureaus, including how statement closing dates trigger monthly updates, the difference between statement and current balance, payment timing strategies, and how late payments and account closures get recorded.

Core Facts:

- American Express reports account data to Equifax, Experian, and TransUnion once per month, triggered by each card’s statement closing date rather than the payment due date.

- Most accounts show updated credit file data within two to seven business days after the statement closing date.

- Amex reports the statement balance from the day the billing cycle closed, not the current balance, which can include charges made after that date.

- Most Amex business charge and credit cards do not report to personal credit bureaus during normal use, while personal cards like Gold, Platinum, Green, and Blue Cash report monthly to all three.

- A late payment is only reported to bureaus once an account is 30 or more days past due, and one 30-day late mark can drop a strong credit score by 60 to 110 points.

- New Amex accounts typically appear on a credit report within 30 to 60 days of approval, and Amex may report to one bureau before the others.

Best for:

- Cardholders who want to lower their reported credit utilization before a major credit application like a mortgage.

- People managing multiple Amex cards with different statement closing dates who need a clean utilization snapshot across all accounts.

- Anyone trying to understand why their credit monitoring app shows different timing than Amex’s actual bureau reporting.

How American Express Reports to Credit Bureaus

American Express shares account data with all three major credit bureaus: Equifax, Experian, and TransUnion. This happens every month. The trigger for this update is your statement closing date, not your payment due date or the first of the month.

When your billing cycle closes, Amex takes a snapshot of your account. That snapshot then travels to the bureaus within a few business days. Most cardholders see their data refreshed on their credit file within two to seven business days after the closing date.

This pattern stays the same whether you carry a balance or pay in full. The bureaus receive your statement balance, your credit limit (when applicable), your payment status, and your account history. Experian explains that most major issuers, including Amex, report monthly on this kind of cycle.

Why There’s No Single “Amex Reporting Day”

A common myth says Amex reports on the same day every month for every cardholder. That’s not true. Each account has its own billing cycle, and that cycle drives the reporting date. Your neighbor’s Amex Gold might close on the 5th. Yours might close on the 22nd. So your data hits the bureaus on different days.

Each Amex card you own can also have its own closing date. If you hold a Gold card and a Platinum card, they often close on separate days. That means two separate reporting events each month, not one.

Does Amex Report Business Cards the Same Way?

Amex handles business cards differently from personal ones. Most Amex business charge cards and business credit cards do not report to the personal credit bureaus during normal use. They only show up on your personal report if the account goes seriously past due. This is a key reason many people use Amex business cards to keep large business spending off their personal utilization ratio.

The Amex Business Platinum and Business Gold follow this rule. Personal cards like the Amex Gold, Platinum, Green, and Blue Cash always report monthly to all three bureaus. If you’re not sure which type of card you hold, check the card art and the cardmember agreement. Business card numbers often begin with various patterns. The agreement outlines the reporting policy.

What Information Amex Sends to the Bureaus

Each month, Amex sends a tidy data file to Equifax, Experian, and TransUnion. The file contains your statement balance as of the closing date. It includes your credit limit for revolving cards or your high balance for charge cards.

You will also see your minimum payment due, your actual payment from the prior cycle, and your account status (open, closed, or past due). Additionally, it shows the date your account was opened and details your payment history for the months.

This data feeds the calculations behind your FICO and VantageScore numbers. The reported balance is what shapes your utilization ratio, which is one of the biggest score factors after payment history.

How Credit Limit Changes Get Reported

If Amex raises or lowers your credit limit, the new number shows up on your next monthly report. A credit limit increase can drop your utilization ratio overnight, which often nudges your score up. A limit cut works the other way, raising your ratio even if your spending hasn’t changed.

Charge cards, like the classic Amex Gold and Platinum, don’t have a preset spending limit (NPSL). For these, Amex reports a “high balance” figure instead of a credit limit. Some scoring models treat that high balance as a stand-in limit. Others ignore it. This is why charge cards can have an unpredictable effect on your utilization math.

💡 Pro Tip: If your score model treats your charge card’s high balance as the limit, a single large purchase can briefly inflate the “limit” and lower your utilization. Spreading spend across cycles keeps things steady.

How to Find Your Exact Amex Statement Closing Date

Knowing your exact closing date is the single most useful piece of information for managing your credit timing. You can find it in three quick ways.

Through the Amex website:

- Sign in at americanexpress.com.

- Choose the card you want to check from the account dashboard.

- Click “Statements & Activity” in the top menu.

- Look for “Closing Date” next to your most recent statement. The next closing date follows the same day each month, give or take a day for weekends or holidays.

Through the Amex mobile app:

- Open the Amex app (App Store or Google Play).

- Tap the card you want to view.

- Tap “Statements.”

- The closing date sits at the top of the most recent statement.

Through a paper or PDF statement: The closing date prints in the header. It will say something like “Closing Date 06/22/26.” Add about 30 days to get the next one.

If you want to be extra sure, call the number on the back of your card and ask the rep to confirm your closing date and your typical reporting day to each bureau.

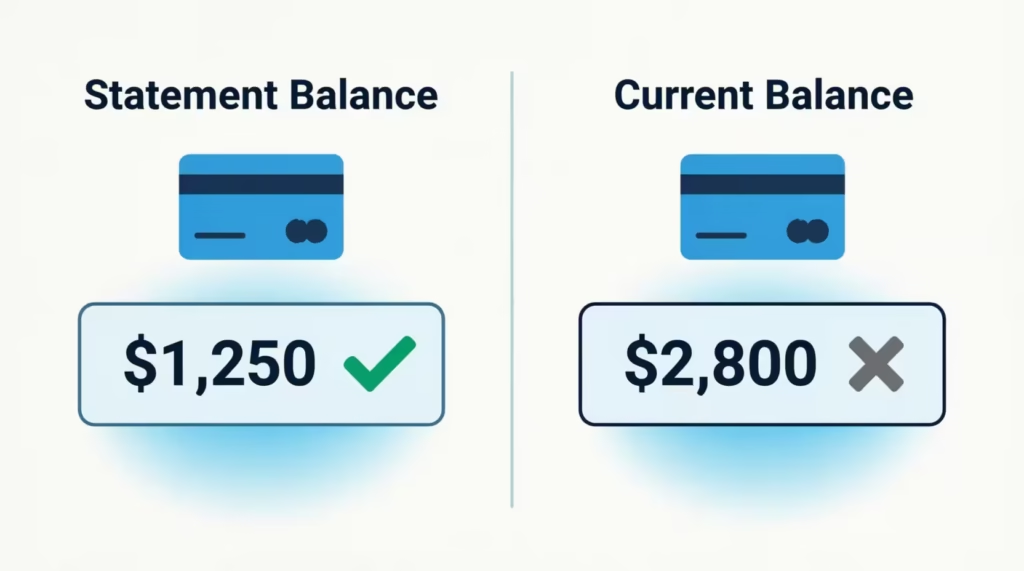

Statement Balance vs. Current Balance: What Actually Gets Reported

This is where many cardholders get tripped up. Amex reports your statement balance, not your current balance. The statement balance is the total you owed on the day your billing cycle closed. The current balance is whatever you owe right now, including new charges after the close.

Here’s a clean example: Sarah, a marketing manager at a tech startup, has a $10,000 limit on her Amex Everyday card. Her cycle closes on the 18th. On the 18th, her statement balance is $3,000. The next day, she charges $2,000 for a work trip. Her current balance is now $5,000, but the bureaus still see $3,000 for that cycle. Her reported utilization on this card is 30%, not 50%.

This is great news if you plan. You can pay your card down right before the closing date and force a lower number onto your credit file, even if you keep spending after.

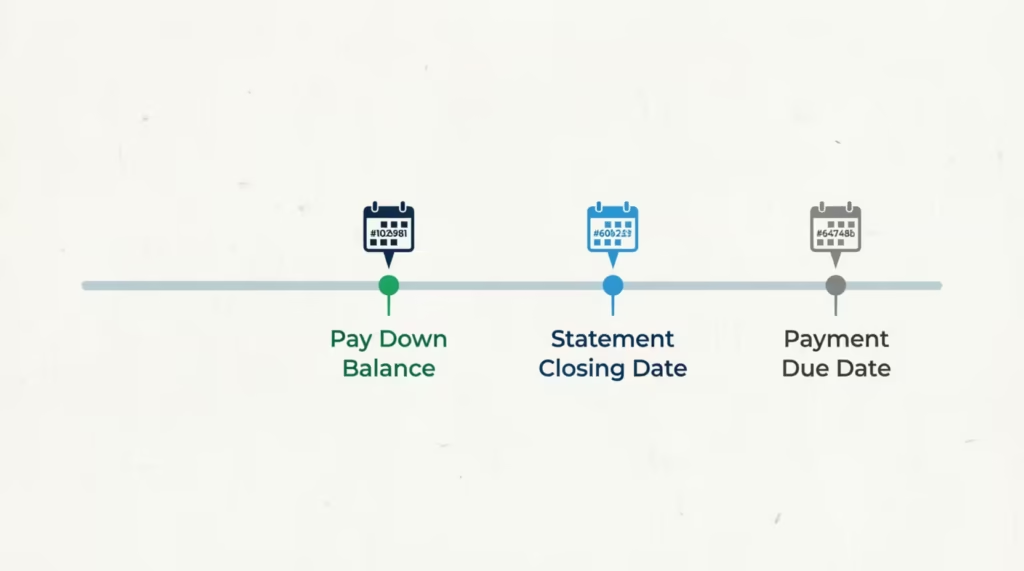

⚠️ Mistake to Avoid: Paying only by the due date isn’t enough to lower your reported balance. The due date is about 21-25 days after the closing date. By that point, the high balance has already been reported.

How to Time Payments to Lower Your Reported Balance

The timing trick is called “early payment” or “pre-statement payment.” Pay your balance down two to three days before the closing date. That way, when the cycle closes, the balance is low or even zero.

Say Michael, a freelance designer, runs $8,400 through his Amex Gold each month for business expenses. His closing date is the 12th. If he pays $8,000 on the 9th, only $400 hits his credit report. His utilization stays tiny, his score stays high, and he still earns the points on every dollar.

A few rules to keep in mind:

- Don’t pay so early that the payment posts to the prior cycle.

- Leave a tiny balance (a few dollars) rather than zero, since some scoring models prefer a small reported number over none.

- Watch your account in the Amex app to confirm the payment cleared before the cycle closes.

How Long Does It Take for a New Amex Card to First Appear on Your Credit Report

Brand-new Amex accounts usually show up on your credit report within 30 to 60 days. The exact timing depends on when in your billing cycle you opened the card. If you got approved a few days before your first statement closes, the account can appear within a couple of weeks. If you got approved right after a closing date, you might wait closer to 60 days.

Two extra points to know. First, Amex sometimes reports to one bureau before the others. So your Experian file might show the card a week before your TransUnion file does.

Second, your “account opened” date matters for the average age of accounts. Even if the card doesn’t appear on day one, the opened date will be backdated to your approval date once it shows up.

If you’re tracking the 5/24 rule or another card eligibility rule, watch all three bureau reports. Don’t rely on just one.

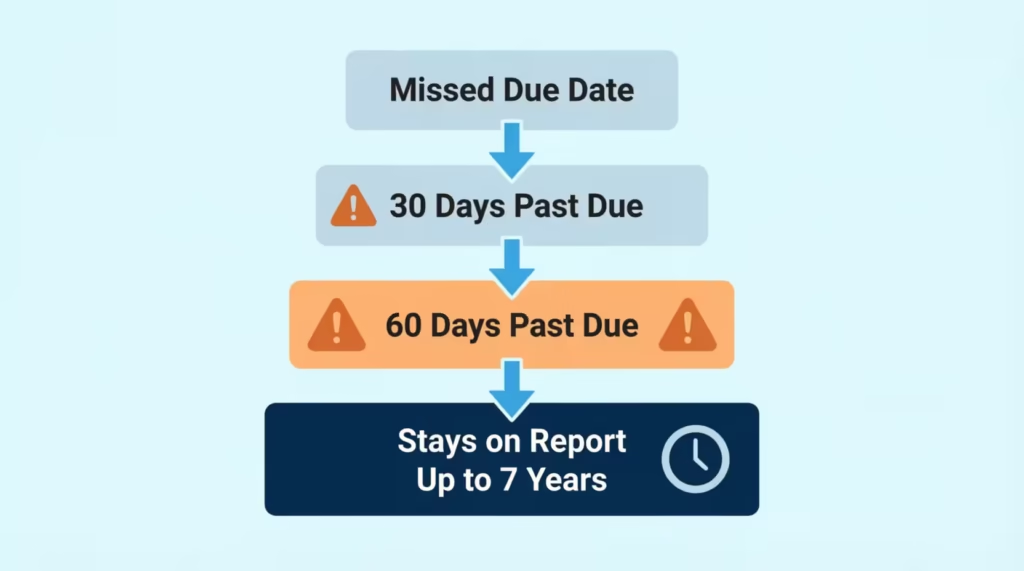

How Late Payments Get Reported to the Bureaus

A late payment doesn’t hit your credit report the day after you miss the due date. The credit bureaus only accept late marks for accounts that are 30 or more days past due. So if you miss your due date by a few days and then pay, you’ll get a late fee, but no bureau damage.

Once you pass 30 days, the next monthly report will include the “30 days past due” mark. If you stay unpaid, the next cycle adds a “60 days past due” mark. The damage grows the longer you wait. As myFICO notes, one 30-day late payment can drop a strong score by 60 to 110 points.

What Happens If You Pay a Past-Due Account Back to Current

Paying off the past-due amount stops the bleeding but doesn’t erase the history. If you were marked 30 days late once, that mark stays on your report for up to seven years. Paying brings the account status back to “current,” and that helps. But the old “30 days past due” notation will still show in your payment history grid.

You can ask Amex for a “goodwill adjustment” by phone or secure message. They sometimes remove a single late mark for a long-time customer with an otherwise clean record. There’s no guarantee, but it’s worth a polite ask.

How Account Closures Get Reported

When an Amex card closes, the next monthly report shows the new “closed” status. The report also notes who closed the account: you or Amex. If you closed it, the report says “closed by consumer.” If Amex closed it, the report often says “closed by credit grantor,” which can look worse to future lenders.

Closed accounts in good standing stay on your credit report for up to ten years. They keep helping the average age of accounts during that time.

Closed accounts that ended in default or charge-off stay for seven years from the first delinquency. So a clean closure isn’t a fast hit to your score, but it can reduce your total available credit and bump up your overall utilization ratio.

Managing Multiple Amex Cards With Different Closing Dates

Holding two or more Amex cards means tracking two or more closing dates. Each one is a separate reporting event.

Jennifer, a finance director with three Amex cards, ran into this when she planned a mortgage application. Her cards closed on the 5th, the 14th, and the 27th. She had to time payments around all three to get a clean utilization snapshot before her lender pulled credit.

A simple tracking method works best:

- List each card and its closing date in a notes app or spreadsheet.

- Set a phone reminder for three days before each closing date.

- Pay down each card the morning of that reminder.

- Check the Amex app the day after to make sure the payment posted on time.

You can also ask Amex to change a card’s closing date. Call the number on the back of the card and ask if your closing date can be shifted to a specific day of the month. Many cardholders move all their Amex closings to the same week to simplify cash-flow planning.

Why Your Credit Monitoring App Might Not Match Amex’s Reporting Date

Credit monitoring apps like Credit Karma, Experian, and the one inside the Amex app each refresh on their own schedule. Amex might send the data on the 18th, but your monitoring app might not show the update until the 21st or 25th. That lag isn’t a sign that Amex didn’t report. It’s just the app’s refresh cycle.

Free monitoring apps usually pull from one bureau or one type of credit report. Credit Karma uses TransUnion and Equifax. The free Experian app uses Experian.

So if Amex reports to Experian on Monday but your TransUnion-based app updates on Friday, you’ll see the change later. For the most accurate view, log in directly to AnnualCreditReport.com and pull all three bureau reports. That’s the official source, and it’s free once a week through the major bureaus.

📌 Did You Know: The score you see in a free credit app is often a VantageScore, not a FICO. Lenders mostly use FICO. So a 770 in your app might land as a 745 with a mortgage lender. Use the apps for trends, not for the exact number a bank will pull.

When Does the Amex Gold Card Report to Credit Bureaus?

The Amex Gold Card reports to all three bureaus once per month, tied to your statement closing date. The Gold is a charge card with no preset spending limit (NPSL), so the report shows your high balance rather than a fixed credit limit. Depending on the scoring model, that high balance may or may not be used in your utilization math.

If you upgraded from a Green card or downgraded from a Platinum to a Gold, your account number stays the same, and the reporting cycle stays the same. The card type on the report changes, but the open date, payment history, and reporting schedule stay the same. Gold cardholders should follow the same strategy: pay down balances before the closing date. This keeps reported balances neat.

When Does the Amex Platinum Card Report to Credit Bureaus?

The Amex Platinum Card also reports once per month to Equifax, Experian, and TransUnion, on your statement closing date. Like the Gold, the Platinum is a charge card with NPSL, so a high balance shows up in place of a fixed limit. Heavy spenders on the Platinum, usually $10,000 or more each cycle, should check if their FICO model sees that high balance as a usable limit.

David, a senior consultant, charges around $15,000 a month on his Platinum for client travel. By paying $14,000 of that down two days before his closing date of the 7th, only $1,000 shows up on his reports. His credit score stays high, even during heavy spending months.

If you upgrade from a Gold or another card to a Platinum, the account history transfers. The reporting cycle stays linked to your old billing cycle unless you ask Amex to change it. Platinum cardholders with high monthly spending might want to ask for a closing date change. This can help match their cash flow better.

Frequently Asked Questions (FAQs)

When does Amex report to credit bureaus?

Amex reports to Equifax, Experian, and TransUnion once a month, triggered by your statement closing date, not your due date. Most accounts update within two to seven business days after that closing date.

What is the 3-day rule for credit cards?

Paying your balance down two to three days before your statement closing date lowers the balance Amex reports to the bureaus that cycle. This can shrink your reported utilization even if you keep spending right after the payment posts.

Is it bad to go over 30% of the credit limit?

Yes, utilization above 30% typically hurts your credit score, since the bureaus only see your statement balance, not your real-time spending. Paying down your balance before the closing date keeps your reported utilization low regardless of how much you spend afterward.

What is the biggest killer of credit scores?

A late payment is one of the fastest ways to damage a credit score, with one 30-day late mark dropping a strong score by 60 to 110 points. The bureaus only record a late mark once you’re 30 or more days past due.

Do business Amex cards report to credit bureaus the same way as personal cards?

No, most Amex business cards skip personal credit reporting during normal use and only appear if the account becomes seriously past due. Personal cards like the Gold, Platinum, Green, and Blue Cash always report monthly to all three bureaus.

How long does it take for a new Amex card to show up on your credit report?

New Amex accounts typically appear within 30 to 60 days, depending on where your approval date falls in the billing cycle. Amex sometimes reports to one bureau before the others, so your Experian file may update before TransUnion.

What’s the difference between statement balance and current balance for Amex reporting?

Amex reports your statement balance, the amount owed when your billing cycle closed, not your current balance, which includes any new charges since then. This means spending right after your closing date won’t affect that month’s reported utilization.

How does an increase or decrease in an Amex credit limit affect your credit report?

A credit limit increase typically lowers your utilization ratio and can boost your score, while a limit cut raises your ratio even without new spending. The updated limit appears on your very next monthly report to the bureaus.

Wrapping Up

Your Amex reporting timeline is simple once you know the rules. Amex reports your statement balance to all three bureaus a few days after your closing date, not your due date. Pay before the closing date to keep your utilization low.

If you have more than one card, watch each card’s cycle. Also, remember that charge cards, like Gold and Platinum, follow the same monthly rhythm.

To sum up, the best way is to:

- Pay early.

- Track all closing dates.

- Pull reports from all three bureaus before any big application.

If this guide helped you, share it with a friend juggling cards before a mortgage; it could save their score at the exact moment they need it.