You’ve seen the Amex Platinum card everywhere. A friend pulled one out at dinner. A travel blog called it a “must-have.” Now you’re staring at the application page, wondering one thing: will my credit score actually be enough? The fear of getting denied, eating a hard inquiry, and watching your score dip for nothing is real. Most people don’t know the true Amex Platinum credit score requirement, and that guesswork creates a lot of anxiety.

Here’s the short answer: a FICO score of 700 or higher gives you a real shot, but 740+ is the sweet spot for approval.

I’ll walk you through every factor Amex looks at beyond the score, the prequal tools that protect your credit, and what to do if you get denied. Let’s get you ready to apply with confidence.

Key Takeaways

This guide explains the Amex Platinum credit score requirement, including FICO 8 score benchmarks, income and credit history factors, the 2/90 application rule, and prequalification tools to check approval odds risk-free.

Core Facts:

- A FICO Score 8 of at least 700 is the practical floor for Amex Platinum approval, with most approved applicants scoring 740 to 800 or higher.

- Amex pulls the FICO Score 8 from Experian for personal card applications, which can differ by 20 to 40 points from VantageScore models like Credit Karma.

- The soft income benchmark for Platinum approval is around $50,000 annually, though lower incomes can work with a 740+ score and clean credit file.

- Amex’s 2/90 rule limits applicants to no more than two American Express credit cards approved within any 90 day period.

- A minimum of two years of clean credit history, with no missed payments or collections, is the practical guideline for approval.

- CardMatch and Amex’s Apply With Confidence both use soft credit pulls to preview approval odds without affecting your credit score.

Best for:

- People with a FICO score between 670 and 740 who want to know their real approval odds before applying.

- Existing Amex cardholders considering an upgrade or additional card who want to understand income and history requirements.

- Anyone denied for Amex Platinum despite good credit who wants to know the reconsideration and reapplication process.

The Credit Score You Need for Amex Platinum Approval

Amex has never published an official minimum score. That’s the first thing to accept. But the data from approved applicants, denied ones, and Amex’s own credit education pages tell a clear story.

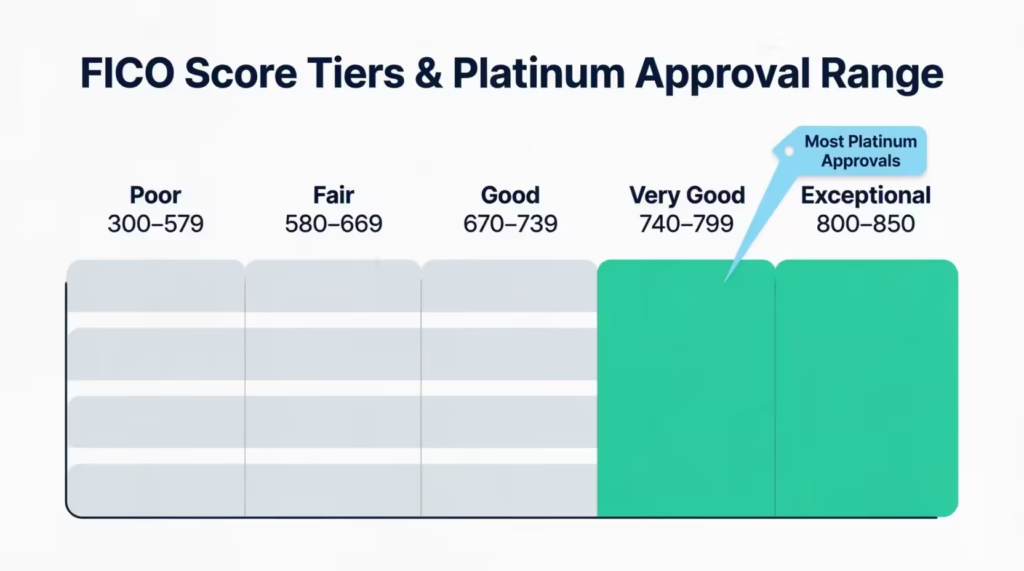

To get the Amex Platinum, you generally need a “good” to “excellent” credit score. In FICO terms, that means a score of at least 700, with most approved applicants landing in the 740 to 800+ range. The card sits in the premium travel tier, so Amex screens for low-risk borrowers who manage credit well.

American Express groups FICO Score 8 into five tiers in its own credit education content: Poor (300-579), Fair (580-669), Good (670-739), Very Good (740-799), and Exceptional (800-850). The Platinum card almost always goes to people in the top two tiers.

If your score sits in the high 600s (say, 670 to 699), approval is possible but risky. You’d need other strong factors, like solid income and a long credit history, to balance things out. Below 670, the odds drop sharply. You’re better off improving your score first than burning a hard pull.

💡 Pro Tip: Pull your FICO Score 8 from Experian before you apply. That’s the exact model and bureau Amex uses for personal cards, so it’s the truest preview of what they’ll see.

Why Different Sources Cite Different Numbers

Search around, and you’ll see scores quoted from 643 to 740+. That spread is confusing, but it makes sense once you understand what each number means.

Some blogs cite anecdotal reports from approved applicants who reported low scores on forums. A handful of people get approved with a 643 or 670. These are rare cases, often tied to long Amex history or high income. They are not typical.

Other sites cite the typical approval cluster, which sits at 740 and above. That’s where most new Platinum cardholders fall.

The gap exists because Amex has never released an official cutoff. So writers either share floor data (lowest approved) or cluster data (most common approval). Both are true. Neither tells the full story on its own.

For planning, treat 700 as your real floor and 740 as your comfort zone.

Which Credit Score Does Amex Actually Look At

Amex pulls your credit data from Experian for personal cards. The scoring model they rely on is FICO Score 8, the most widely used FICO version among lenders.

You can check this exact score for free through Amex’s own tool, MyCredit Guide, which provides your FICO Score 8 from Experian, updates weekly, and doesn’t hurt your credit. You don’t need to be an Amex cardholder to use it.

This matters because the score you see on Credit Karma (VantageScore from TransUnion and Equifax) is often 20 to 40 points different from your FICO 8 from Experian. Applying based on a Credit Karma score can lead to a nasty surprise. Check the right score first.

Does Amex Platinum Have an Income Requirement?

Amex does not publish a minimum income. But income plays a huge role in approval, and ignoring it is one of the most common mistakes applicants make.

Industry consensus places the soft benchmark around $50,000 in annual income. That’s not a hard cutoff. People with lower incomes do get approved, especially with strong credit and existing Amex accounts. But $50,000 is a reasonable signal that you can handle the card’s $695 annual fee and the kind of spending that makes the rewards worthwhile.

Why does income matter so much? The Platinum is a charge card at heart, meaning it uses a dynamic spending limit instead of a fixed credit line. Amex needs to feel confident you can pay off large balances each month. Your reported income helps them set that flexible limit.

When you report income, include all eligible sources: your salary, freelance income, investment income, and (if you’re 21 or older) accessible household income from a spouse or partner. Underreporting income to “play it safe” hurts you. Be accurate and complete.

If your income is closer to $35,000 or $40,000, you can still apply, but pair it with a 740+ score and a clean credit file. The lower the income, the more your other numbers need to shine.

How Your Credit History Length Affects Approval

A high score with a short history is a red flag for Amex. Think of two applicants: one has a 770 score built over six months with one credit card, and another has a 720 score built over five years across three cards. Amex will almost always favor the second applicant.

Length of credit shows a pattern. It tells Amex you’ve handled credit through different life events, not just a few perfect months. For the Platinum, a minimum of two years of clean credit history is the practical guideline. That means at least one account open for two-plus years, with no missed payments, no charge-offs, and no collections.

Newer credit users (under one year) face a tough road. The score alone, even a great one, isn’t enough proof. If you’re new to credit, build the file for 18 to 24 months on a no-annual-fee starter card before reaching for the Platinum. Use it, pay it in full, and let time do its work.

The length factor isn’t about being old. It’s about giving Amex enough data to predict your future behavior. The longer and cleaner your file, the easier the approval.

Behavior-Based Factors That Influence Your Approval Odds

A score is a snapshot. Behavior is the movie. Amex weighs both, and behavior often tips a borderline application either way.

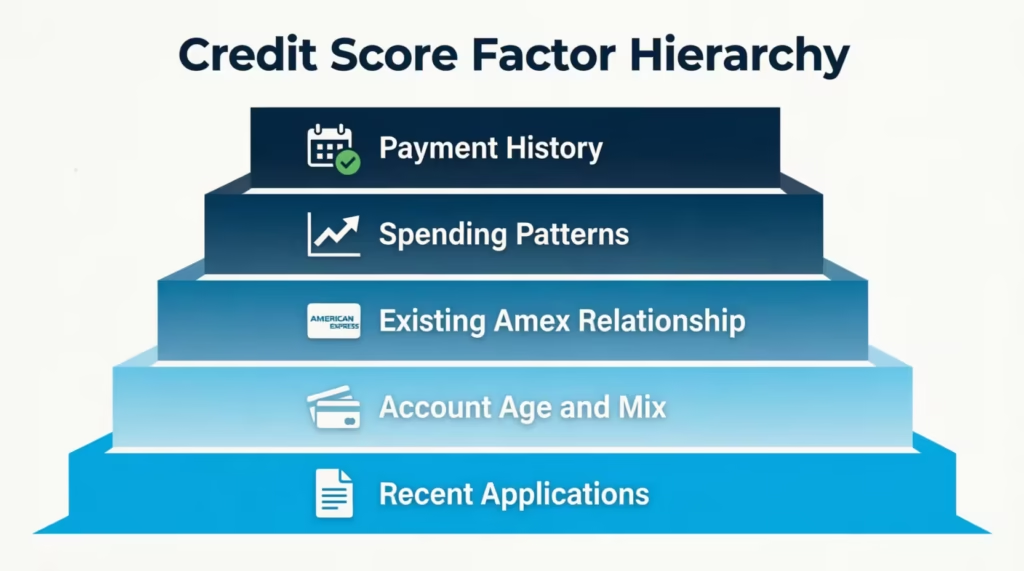

Here are the main behavior factors, ranked roughly by how much weight they carry:

- Payment history (highest weight): even one late payment in the last 12 months can sink a Platinum application.

- Spending patterns: consistent, reasonable card use over months beats sudden bursts of new activity.

- Existing Amex relationship: current cardholders in good standing get smoother approvals and targeted offers.

- Account age and mix: a healthy blend of revolving cards and installment loans helps.

- Recent applications: too many hard pulls in 12 months signals risk.

The first three matter most for Platinum specifically. Let’s break each one down.

How Your Spending Activity on Other Cards Is Evaluated

Amex looks at how you use your current credit cards. They want to see consistent monthly spending that you pay off responsibly. Dormant cards (open but rarely used) don’t help your case much because they show no spending pattern to study.

On the flip side, sudden heavy spending right before applying can backfire. If your utilization spikes above 30 percent, Amex sees higher risk, even if you plan to pay it off.

⚠️ Mistake to Avoid: Applying for multiple bonus offers across issuers in a short window (“churning”) can flag you as credit-seeking, which lowers your odds with Amex even if your score looks fine.

Steady, moderate use of your existing cards over the three months before applying gives the cleanest profile.

Why an Existing Amex Relationship Helps

If you already hold an Amex Gold, Green, Delta, or any other Amex card in good standing, your odds of Platinum approval go up. Amex sees your full account history with them, including how you handle the dynamic limits and whether you’ve ever paid late.

Existing cardholders often get targeted offers for the Platinum directly through their account login. These targeted offers usually carry a higher welcome bonus and signal that Amex has already pre-screened you.

Even a six-month relationship with a no-annual-fee card like the Amex EveryDay can soften the path to Platinum. It’s not a guarantee, but it’s a meaningful tailwind.

How a Single Late Payment Can Still Hurt You

A 30-day late payment in the past 12 to 24 months is a serious problem, even with a 760 score. Amex flags it during the manual review and often denies on that basis. The Platinum sits high on the risk ladder, so they screen tightly for recent slip-ups.

If you have one late payment within the past year, wait until at least 12 months have passed since that incident before applying. The further it sits in the rearview mirror, the less it weighs.

How Recent Credit Applications Can Hurt Your Approval Odds

Each credit card application creates a hard inquiry on your report. Hard inquiries shave a few points off your score and stay on file for two years. One or two won’t hurt much. Five or six in a year tells Amex you’re hunting for credit, which is a risk signal.

For Amex specifically, watch for the 2/90 rule. Data published by WalletHub shows that applicants can be approved for no more than two American Express credit cards within any 90 days. If you opened two Amex credit cards in the past 90 days, your Platinum application will likely be denied. This is true even if your credit profile looks strong.

Charge cards, like Green, Gold, and Platinum, may have separate counts. However, it’s best to space out all Amex applications by at least 90 days.

Across all issuers, aim for no more than two to three new credit applications in any 12-month window when planning a Platinum app. If you’ve just opened two cards in the last six months, hold off on Platinum for now. Let those accounts age, your score recover, and your file calm down.

📌 Did You Know: A hard inquiry usually lowers your FICO score by under five points. It impacts your score for one year, but stays on your report for two.

How to Check If You Prequalify Before You Apply

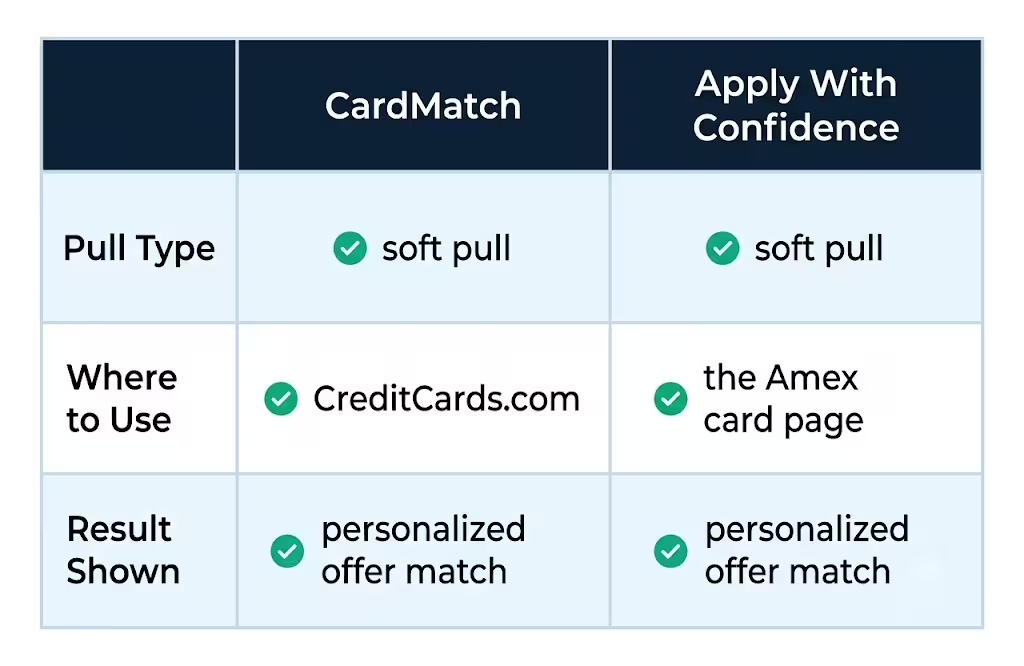

This is the most important step most applicants skip. You can preview your approval odds without any damage to your credit. Two main tools make this possible.

A prequalification check uses a soft credit pull. It does not appear on your credit report, does not lower your score, and does not commit you to anything. If you don’t qualify, you simply walk away.

The first tool to try is CardMatch from CreditCards.com. It scans your file via a soft pull and matches you with personalized credit card offers, including Amex Platinum if you qualify. Industry data shows that about 80 to 90 percent of preapproved applicants receive formal approval at the hard pull stage. Most late denials happen due to new information added between the soft and hard checks.

Important caveat: prequalification is not a guarantee. It means you’ve passed Amex’s initial soft-pull screen. The final hard-pull review checks income, identity, and full bureau data, any of which can shift the decision.

Steps to use CardMatch effectively:

- Visit CardMatch on CreditCards.com.

- Enter your name, address, and last four digits of your Social Security number.

- Review the offers shown for American Express cards.

- If you see Platinum, click to apply for the matched offer. This usually gives you the best welcome bonus.

Using Amex’s Apply With Confidence Tool

Amex runs its own version of prequalification called Apply With Confidence. It uses a soft credit check and tells you whether you’re approved for a specific card before you submit a real application.

How it works:

- Visit the Amex card page for the Platinum.

- Click the “Apply With Confidence” or “Check for Pre-Approved Offers” button.

- Enter your personal info for the soft pull.

- Review the result, which shows either a pre-approved offer or no current offer.

The catch: even if Apply With Confidence shows you’re approved, you still have to submit the formal application. That application triggers the hard pull and finalizes the decision. The soft-pull approval just tells you the hard pull is very likely to succeed.

Use both CardMatch and Apply With Confidence. They check different data, and a green light from either is a strong signal.

What to Do If You’re Denied Despite Good Credit

A denial with a 750 score feels unfair. It happens more often than people realize, and it’s almost always fixable.

First, read the denial letter carefully. Amex is legally required to mail you a notice of adverse action within 30 days. It lists the specific reasons your application was denied. Common reasons include: too many recent inquiries, too many Amex cards already open, insufficient income reported, or short credit history.

Second, call the Amex reconsideration line at 1-800-567-1085. This is a quiet but powerful tool. A real human reviewer will look at your file again. Be polite, explain any context (a recent job change, a credit report error, etc.), and ask if anything can be done. Many denials get reversed on the reconsideration call.

Tips for a successful reconsideration call:

- Have your application reference number ready.

- Know your income, employer, and credit details cold.

- If the denial cited “too many cards,” offer to move credit limits from other Amex accounts to the new card.

- Stay calm and professional. Pressure rarely works.

Third, address the cited reasons before reapplying. If the issue was recent inquiries, wait six months. If it were income, double-check that you reported all eligible household income. If your file showed an error, dispute it with Experian first.

One critical note on the welcome bonus: Amex enforces a “once per lifetime” rule, meaning each card’s welcome offer can typically be earned only one time per person. If you’ve had a Platinum bonus before, a new application usually won’t get you the bonus again. However, you can still apply for the card. Always read the offer’s terms to confirm your eligibility before applying.

How to Apply Once You’ve Confirmed You’re a Strong Candidate

You’ve checked your FICO 8 score (700+, ideally 740+). You’ve confirmed your income and credit history support the application. You’ve used Apply With Confidence and seen the green light. Now it’s time to apply for real.

Steps to apply for the Amex Platinum:

- Go directly to the Amex Platinum application page through your prequalified offer link (this locks in the highest welcome bonus available to you).

- Fill in your legal name exactly as it appears on your credit bureau file. Mismatches trigger manual review.

- Use your current home address (where your bills go) and the same phone number listed on your credit file.

- Report your total annual income honestly, including all eligible sources.

- List your housing payment (rent or mortgage) accurately.

- Review all info, then submit.

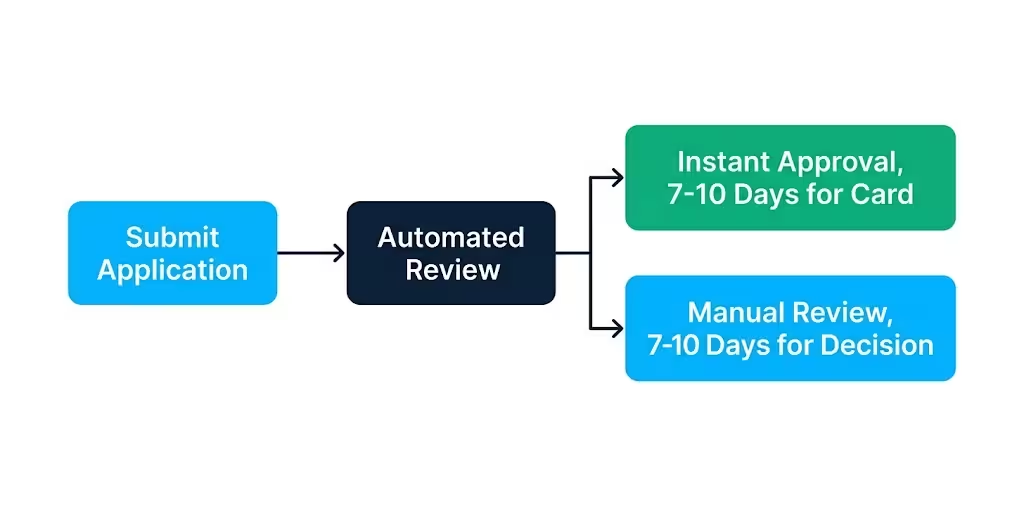

Two outcomes follow:

Instant approval: Amex’s automated system says yes on the spot. You’ll see an account number and welcome message within seconds. Your card arrives in 7 to 10 business days.

Manual review: The system needs a human to look at your file. This isn’t a denial. It usually means something needs verification (income, address, or one specific data point). Most manual reviews finish within 7 to 10 days. You’ll get an email when the decision is made. If a week passes with no update, call the application status line at 1-800-567-1085 to check in.

If you’re approved, set up online account access right away, link your payment account, and read the card benefits guide. The Platinum’s value comes from using its credits and perks (airline fee credit, hotel credits, lounge access). Plan how you’ll hit the welcome bonus spending requirement within the first 3 to 6 months, but only on purchases you would have made anyway.

Frequently Asked Questions (FAQs)

What credit score do you need for the Amex Platinum?

A FICO Score 8 of at least 700 gives you a real shot at approval, but most approved applicants fall in the 740 to 800+ range. Below 670, approval odds drop sharply.

Is it hard to get approved for the Amex Platinum?

Approval requires more than a good score. Amex also weighs income of at least $50,000, at least two years of clean credit history, and no late payments in the past 12 to 24 months.

What is the Amex 2/90 rule?

Amex generally approves no more than two American Express credit cards for one person within any 90 days. Opening two Amex cards in the past 90 days will likely get a Platinum application denied, even with strong credit.

Will Amex approve a 600 credit score?

A 600 score falls in the “fair” tier and sits well below the 700 floor most Platinum approvals need. Approval at that score is highly unlikely without exceptional offsetting factors like a very high income.

What salary do I need for an Amex Platinum?

There’s no published minimum, but the soft industry benchmark is around $50,000 in annual income. Lower incomes can still work if paired with a 740+ score and a clean credit file.

Is Amex Platinum harder to get than Gold?

The Platinum sits higher on Amex’s risk ladder than the Gold card, so it gets screened more tightly for income, credit history length, and recent late payments.

How rare is an 830 credit score?

An 830 falls in FICO’s top “Exceptional” tier, which spans 800 to 850. Scores in this range are uncommon and sit well above the 740+ that typically gets Platinum approval.

How can I check if I prequalify for the Amex Platinum before applying?

Use CardMatch from CreditCards.com or Amex’s own Apply With Confidence tool. Both use a soft credit pull, so checking your odds won’t lower your score or show up on your credit report.

What should I do if I’m denied for the Amex Platinum despite good credit?

Read your denial letter for the specific reason, then call the Amex reconsideration line at 1-800-567-1085 to ask for a second review. Fixing the cited issue, like reducing recent inquiries, before reapplying improves your odds.

Why is my Amex Platinum offer lower than expected?

Amex sets your dynamic spending limit based on factors like reported income, credit history, and existing account behavior rather than a fixed formula. A lower offer usually reflects one of those factors being weaker, not a fixed cap on the card itself.

Wrapping Up

To get approved for the Amex Platinum, focus on five key points:

- A FICO 8 score of at least 700 (740 is better).

- An income of around or above $50,000.

- At least two years of good credit history.

- No recent late payments or too many inquiries.

- A well-prepared application that aligns with your credit file.

Check your real FICO 8 score from Experian. Use CardMatch and Apply With Confidence to confirm your odds. Only apply when at least two strong factors support your decision.

If you know someone weighing the Platinum, share this guide. It could save them a wasted hard inquiry and weeks of credit recovery.