We get it. You’re ready to apply for an Amex card. Maybe it’s the Platinum, the Gold, or a business card you’ve been eyeing. But you have a credit freeze on one bureau. Or maybe you just don’t want a hard inquiry showing up on the wrong file. The big question on your mind is simple: which credit bureau does American Express actually pull?

The short answer: American Express pulls Experian first for most personal card applications in the U.S.

Below, we’ll walk you through the full picture. You’ll find out when Amex checks other bureaus. You’ll see what happens with business cards. You’ll learn how to verify the pull later and how to manage a credit freeze before applying.

Key Takeaways

This guide explains which credit bureau American Express pulls for personal and business card applications, including fallback bureau behavior, the difference between soft and hard inquiries, freeze management steps, and monthly reporting practices across all three bureaus.

Core Facts:

- American Express pulls Experian first for most personal card applications, based on consistent patterns reported by cardholders rather than official published policy.

- Amex may pull Equifax or TransUnion instead when the Experian file is frozen or has too little data to score the applicant.

- For small business card applications, Amex typically runs a personal hard inquiry on Experian and separately checks business bureau activity, including Dun and Bradstreet and Experian Business.

- Many Amex applications use a soft credit check first through the Apply With Confidence feature, with the hard inquiry occurring only after the applicant accepts an approved offer.

- A hard inquiry typically lowers a FICO score by fewer than 5 points and remains on a credit report for 24 months.

- After approval, Amex reports account data, including payment history, balance, credit limit, account status, and account age, to all three bureaus every month regardless of which bureau was used for the original approval decision.

Best for:

- Applicants who have a credit freeze in place and want to know which bureau to unfreeze before applying.

- Small business card applicants who want to understand why both a personal and business bureau check may occur.

- Anyone who wants to confirm which bureau Amex pulled after submitting an application.

Which Credit Bureau Does American Express Pull for Most Applications

If you’re applying for a personal Amex card, Experian is almost always the bureau pulled. This pattern shows up again and again in reports from cardholders, credit forums, and data trackers like the CreditBoards database.

Amex doesn’t publish an official list saying “we use Experian.” So this is not a written policy you can quote back to a customer service agent. It is, however, the most consistent real-world pattern over many years and thousands of applications.

This means one thing for you: if you only manage one credit file before applying, make it your Experian file. That’s the one Amex is most likely to look at when deciding whether to approve your application.

Why Experian Is Amex’s Default Bureau

American Express and Experian appear to have a long-standing data relationship. Amex also offers a free credit tool called MyCredit Guide, which pulls your Experian credit report and a VantageScore. That’s another sign of how closely the two companies work together.

The default bureau pull also lines up with where Amex feels most confident scoring you. Experian carries the bulk of consumer data that Amex uses to judge risk and approval odds for premium products.

Does the Card Type Change Which Bureau Is Pulled

For most personal cards, the answer is no. Whether you apply for a Delta SkyMiles card, the Amex Gold, or the Platinum, the pattern is the same. Experian is usually first in line.

Card type may shift other things, like the minimum credit profile Amex wants. But the bureau itself tends to stay the same across the consumer lineup.

💡 Pro Tip: If you’ve been declined by Amex in the past and you’re not sure why, pull your free Experian report first. The story behind your denial is most likely sitting on that one file, not on your Equifax or TransUnion report.

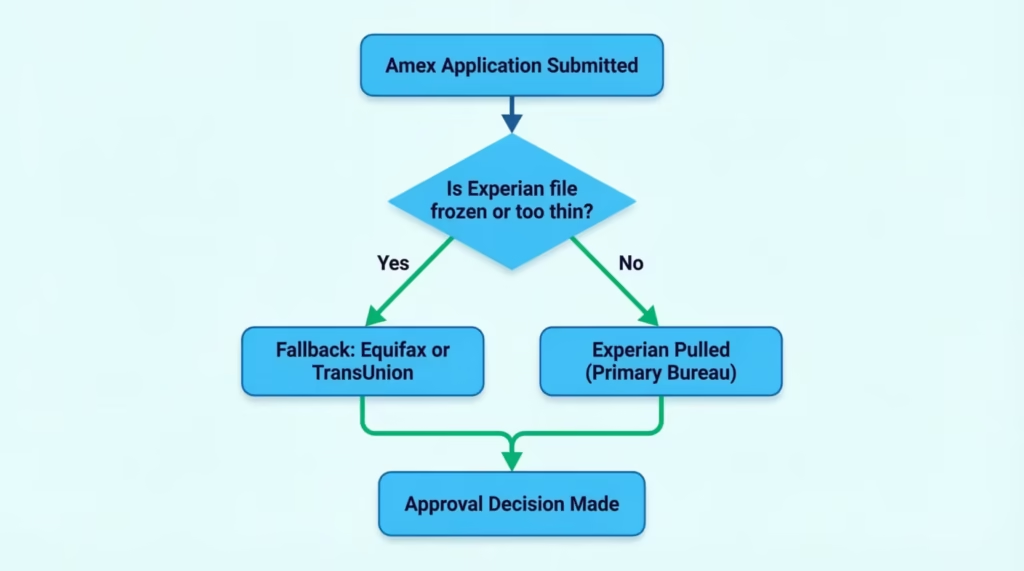

When American Express Uses Equifax or TransUnion Instead

Sometimes, Amex doesn’t pull Experian. This usually happens for one of two reasons. Either your Experian file is frozen, or your file is too thin for Amex to score with confidence. In both cases, Amex may fall back on Equifax or TransUnion to make a decision.

This fallback behavior is not posted on the Amex website. It’s a pattern that cardholders have noticed and reported over the years. Treat it as a likely scenario, not a guaranteed rule.

A fallback bureau pull is not a bad thing. Your approval odds don’t drop just because Amex looks at a different file. The credit data is similar across the three bureaus, even if the exact score number is not. So if your Equifax or TransUnion file is healthy, a fallback pull can still lead to an easy approval.

What Happens If Your Primary Bureau Is Frozen or Has a Thin File

A credit freeze on Experian usually blocks Amex from pulling that file at all. When that happens, Amex has two choices: pause the application and ask you to lift the freeze, or run a fallback check on another bureau.

A thin file works in a similar way. If Experian doesn’t have enough data on you, Amex may peek at Equifax or TransUnion to find a fuller picture. This is more common for new credit users, recent immigrants, or anyone who has frozen and never refreshed their Experian file.

⚠️ Mistake to Avoid: Don’t assume Amex will silently switch bureaus if Experian is frozen. Many applicants get an instant pending status or a denial instead. Lift the freeze before you click apply, not after.

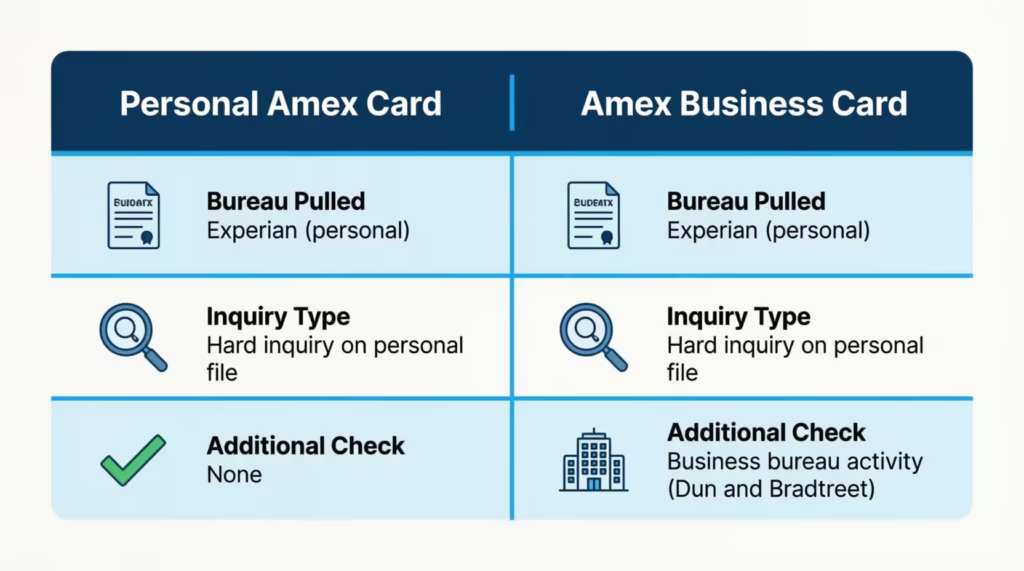

What Bureau Does American Express Use for Business Cards

Business card applicants often get caught off guard. They expect Amex to look only at business credit. The reality is different. Amex usually checks your personal credit for small-business card applications. They also look at business bureaus.

The personal pull is almost always Experian, just like a consumer card. This is because Amex requires a personal guarantee for most small-business cards. You’re personally on the hook for the debt, so Amex wants to see your personal credit profile before approving.

On the business side, Amex reports and may check data from the major business bureaus: Dun & Bradstreet, Experian Business, and Equifax Business. Amex conducts a hard inquiry on personal credit for most small-business card applications, alongside business bureau activity.

So you should expect two things:

- A hard inquiry on your personal Experian report after approval

- Activity tied to your business profile at one or more business credit bureaus

For example, Michael, a marketing consultant who runs a small LLC, applied for the Amex Business Platinum.

He was surprised to see a hard inquiry hit his personal Experian file two days later, on top of a new tradeline being set up under his Dun & Bradstreet number. Both are normal. That dual track is just how Amex Business cards work.

Hard Inquiry vs. Soft Inquiry: When Each Happens With American Express

This is where many readers feel real anxiety. You don’t want to risk a hard pull until you know your odds are strong. Amex actually makes this easier than most issuers because of how the application flow is built.

For many personal Amex cards, the first step is a soft inquiry. A soft pull doesn’t hurt your credit score and doesn’t show up to other lenders. Only after you’re approved and you accept the card does Amex run a hard inquiry. That hard pull then shows up on your Experian report (or whichever bureau Amex used).

Compare this to some other issuers, where the hard pull hits the second you submit the application, whether you’re approved or not. The Amex flow gives you a safer first look at your odds.

Experian explains that pre-qualification uses a soft credit check, so your score is not affected at this stage. Amex follows the same model for cards covered by its check-in-advance feature.

How Amex’s Apply With Confidence Feature Works

Amex calls this process Apply With Confidence. You start the application like normal. Before any hard pull happens, Amex runs a soft check to see if you’d be approved. If the answer is yes, you can choose to move forward, and that’s when the hard inquiry occurs. If the answer is no, you walk away with no hard pull on your record.

You can access Apply With Confidence directly through the Amex website. Look for the message during the application process that confirms a soft check is being used.

A few details to keep in mind:

- Not every Amex card is part of the feature, so always read the fine print on the application page.

- Even with Apply With Confidence, you’ll still get the hard inquiry once you accept the offer.

- The soft pull uses the same primary bureau most of the time, so a frozen Experian file can still block the check.

📌 Did You Know: A hard inquiry typically lowers your FICO score by fewer than 5 points and falls off your report after 24 months. That’s a small price for a card you’ll keep for years.

Should You Unfreeze Experian Before Applying for an American Express Card

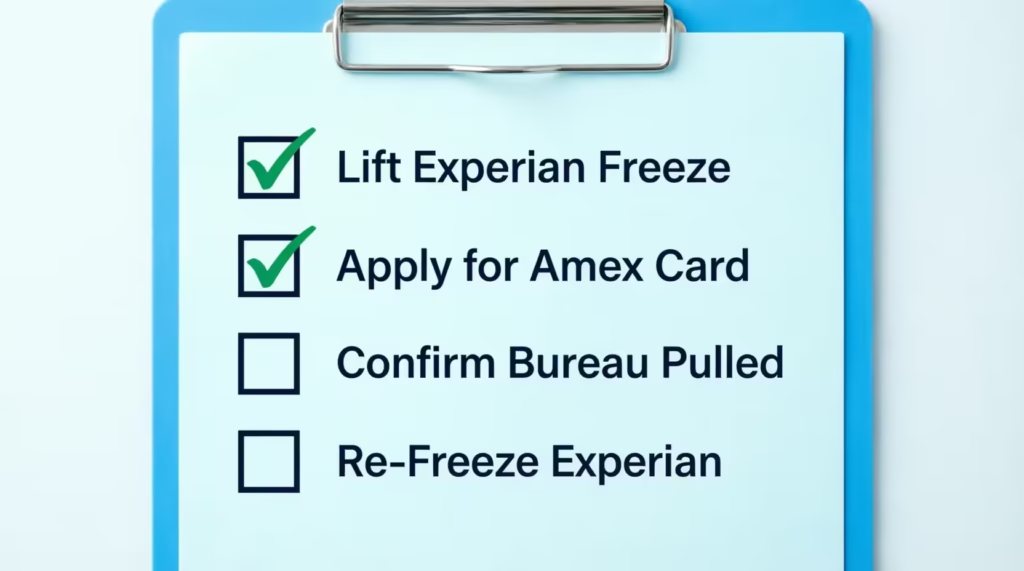

Yes. If you have a freeze on Experian, lift it before you apply for an Amex card. Since Experian is the default bureau, a freeze there is the single biggest blocker between you and a clean approval.

You don’t need to unfreeze all three bureaus. Equifax and TransUnion can stay frozen for most personal Amex applications. Lifting just Experian is usually enough.

Here’s a clean sequence to follow:

- Lift your Experian freeze. Go to the Experian Freeze Center and choose a temporary thaw. You can pick a date range, so the freeze comes back on automatically.

- Apply for your Amex card. Do this within the thaw window. Most approvals happen within minutes.

- Confirm the bureau Amex pulled. Check your Experian report a few days later to make sure the inquiry landed.

- Re-freeze Experian. If your temporary thaw didn’t auto-end, log back in and refreeze your file.

This approach gives Amex the clean read it needs without leaving your credit file open longer than necessary.

For people with thin files or past identity theft, the freeze management piece really matters. Sarah, a freelance graphic designer in Austin, had frozen all three of her bureaus after a data breach. When she applied for an Amex Gold, the application stalled in pending status. A two-minute thaw of her Experian file moved her from pending to approved the same day.

How to Find Out Which Bureau American Express Actually Pulled

After you apply, you have a simple way to confirm which bureau Amex used. The pull will show up as a hard inquiry on that bureau’s credit report, listed under American Express or AMEX as the creditor name.

The best free source is AnnualCreditReport.com, the official site backed by all three bureaus. You can pull free weekly reports from Equifax, Experian, and TransUnion. That’s plenty for confirming which file Amex hit.

Follow these steps:

- Visit AnnualCreditReport.com.

- Request a report from Experian first, since it’s the most likely bureau.

- Scroll to the Inquiries section of the report.

- Look for an entry tagged American Express with a recent date.

- If you don’t see it on Experian, repeat the steps with Equifax and TransUnion.

You can also log in to your Amex account once the card is open. The account portal may show details from the application process. If you call, customer service can confirm which bureau was used. But the credit report itself is the most reliable proof.

This step matters for two reasons. First, it gives you peace of mind. Second, if you ever need to dispute an unauthorized inquiry, you’ll know exactly which bureau to contact.

Which Bureaus Does American Express Reports to After Approval

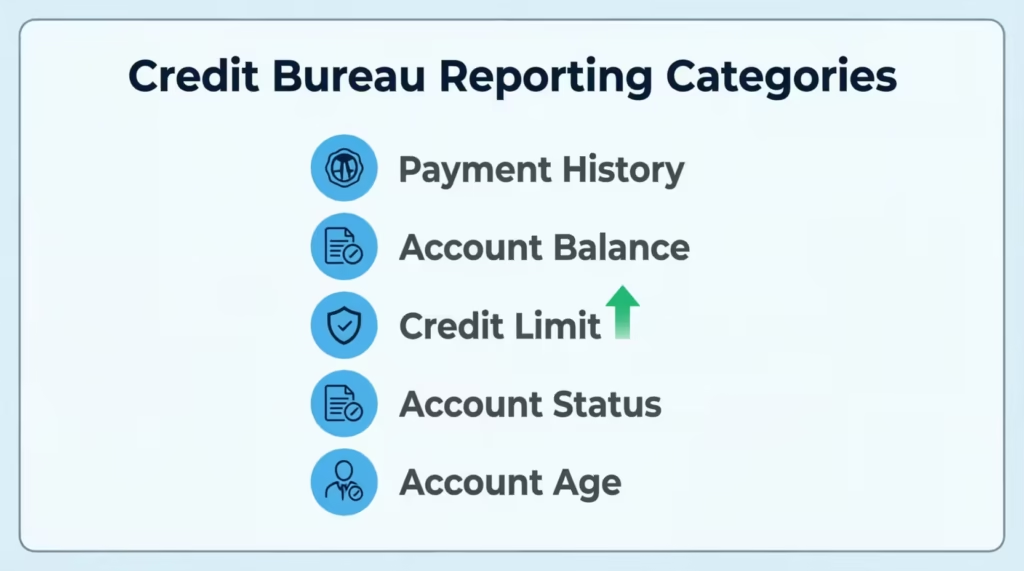

Pulling a bureau and reporting to a bureau are two different things. Once your Amex account is open, the reporting picture changes a lot. Amex reports to all three major bureaus: Equifax, Experian, and TransUnion. This happens every single month.

So even if Amex pulls only your Experian file for approval, your account activity will show up on all three reports going forward. That’s good news for your overall credit profile, since on-time payments help raise your score at every bureau, not just one.

According to American Express, the three major bureaus collect and organize the credit data lenders use to make decisions, and Amex feeds them updates each cycle.

Here’s what Amex sends in those monthly updates:

| Reported Data | What It Shows |

|---|---|

| Payment history | On-time, late, or missed payments |

| Account balance | Your statement balance at the close of the cycle |

| Credit limit | For most cards (charge cards may show differently) |

| Account status | Open, closed, or in collections |

| Account age | Months since the account was opened |

For business cards, the reporting flow shifts to business bureaus. Amex sends data primarily to Equifax Business, Experian Business, and Dun & Bradstreet. Personal credit reporting for business cards varies by product and structure. Always check your card’s terms.

Does It Matter Which Bureau Was Pulled for Approval

Not really, once you’re approved. The application pull is a one-time event. The monthly reporting is what shapes your credit profile over time.

In other words, the Amex bureau looked at matters on day one for getting in the door. After that, all three bureaus get the same updates from Amex. So if your goal is building credit with your new Amex account, every bureau benefits equally.

Frequently Asked Questions (FAQs)

What credit bureau does American Express use?

American Express pulls Experian first for most personal card applications. This is the most consistent pattern reported by cardholders and credit trackers over the years, even though Amex has never confirmed it as official policy.

Which credit bureau does American Express pull?

Experian is the default bureau for nearly all personal Amex cards, including the Platinum, Gold, and Delta SkyMiles cards. Amex may fall back on Equifax or TransUnion only if your Experian file is frozen or too thin to score.

Is Amex TransUnion or Equifax?

Amex is neither by default. Experian is the primary bureau, and Equifax or TransUnion only come into play as fallback options when Experian is frozen or lacks enough data.

Does a hard inquiry from Amex hurt my credit score?

A hard inquiry typically lowers your FICO score by fewer than 5 points and falls off your report after 24 months. Amex also runs a soft check first through its Apply With Confidence feature, so you only get a hard pull after you’re approved and accept the card.

Do I need to unfreeze all three credit bureaus before applying for an Amex card?

No, you only need to lift the freeze on Experian since that’s the bureau Amex checks first. Equifax and TransUnion can stay frozen for most personal Amex applications.

Does Amex report to all three bureaus even though it only pulls one?

Yes, Amex reports your account activity to Equifax, Experian, and TransUnion every month after approval, regardless of which bureau was pulled during the application. This means on-time payments help your score across all three files, not just the one Amex originally checked.

What happens if Amex can’t verify my identity with a soft credit check?

If your Experian file is frozen or has a thin history, Amex may pause your application in pending status rather than silently switching bureaus. Lifting your Experian freeze before applying prevents this stall in most cases.

Does applying for an Amex business card hurt my personal credit?

Yes, most small-business Amex cards require a personal guarantee, so Amex runs a hard inquiry on your personal Experian report after approval. Amex also tracks activity under your business profile at bureaus like Dun & Bradstreet and Experian Business.

How can I check which bureau Amex pulled for my application?

Pull a free report from AnnualCreditReport.com, starting with Experian, since it’s the most likely match. Look in the Inquiries section for an entry listed under American Express with a recent date; if it’s not there, check Equifax and TransUnion next.

Does it matter which bureau Amex pulled once I’m approved?

Not really. The bureau pull only affects your approval decision on day one, but Amex reports your monthly payment history to all three bureaus afterward, so your credit builds evenly across Equifax, Experian, and TransUnion regardless of which one was checked.

Wrapping Up

To wrap it up: American Express pulls Experian first for most personal card applications, with Equifax and TransUnion serving as fallback options when needed. Business cards cause a personal Experian pull and report to business bureaus, such as Dun & Bradstreet. Apply With Confidence keeps the first check soft, and your hard inquiry only lands after approval.

To get the best results, lift your Experian freeze, use Apply With Confidence, and check the inquiry later.

If you know someone planning a big Amex application, this guide could save them a frozen-file headache and protect their score. Share it with them today.