I’ve been there too. You open your American Express statement, and a charge stares back at you that you didn’t recognize, didn’t approve, or never got the product for. It feels stressful, and you might worry the money is gone for good.

The good news? You can dispute a charge on Amex quickly, often online in under five minutes.

In this guide, we’ll walk through every step, the paperwork you need, and what to do if things don’t go your way.

Key Takeaways

This guide explains how to dispute a charge on an American Express credit card, covering the three dispute categories, how to file online in under five minutes, required documentation by dispute type, the 120-day filing window, how provisional credit works, and what to do if your case is denied.

Core Facts:

- Amex disputes fall into three distinct categories — fraud (unauthorized charges), billing errors (wrong amount, duplicate charge, canceled subscription), and goods or services problems — and each category follows a different resolution path with different rules.

- Filing online through the Amex Inquiry and Dispute Center is the fastest method, with most submissions completed in under five minutes by navigating to “Statements and Activity,” selecting the charge, and clicking “Dispute This Charge.”

- Amex typically applies a provisional credit within 1 to 2 business days of filing, removing the disputed amount from your statement balance while the investigation runs.

- The standard filing window is 120 days from the original charge date under Amex policy; federal law under the Fair Credit Billing Act provides a floor of 60 days from the statement date.

- The merchant has up to 20 days to respond after Amex notifies them; most disputes resolve within 30 to 60 days, with complex cases taking up to 90 days.

- If a dispute is denied, cardholders can submit a written appeal to Amex, file a complaint with the Consumer Financial Protection Bureau, pursue small claims court against the merchant, or request arbitration under the cardmember agreement.

Best for:

- Cardholders who see a charge they did not authorize, were billed the wrong amount, or paid for goods or a service that was never delivered or was significantly different from what was advertised.

- People who have already attempted to resolve the issue directly with the merchant and received no response or an unsatisfactory resolution within their stated deadline.

- Anyone who needs a clear explanation of what qualifies as a valid dispute reason versus what Amex will deny, including the distinction between buyer’s remorse and a legitimate goods or services complaint.

Is Your Amex Charge a Fraud Issue, a Billing Error, or a Goods and Services Problem?

Before you do anything else, you need to figure out which type of problem you have. American Express handles each one differently, and choosing the wrong path can slow down your refund or even close your case.

There are three main categories to know:

1. Fraud (unauthorized charge). Someone used your card or account without your permission. This includes stolen card numbers, account takeovers, or charges from a merchant you’ve never heard of. This is not a billing dispute. It’s a fraud case, and it goes straight to the Amex security team.

2. Billing error. The charge is yours, but something about it is wrong. Maybe you were charged twice, charged the wrong amount, billed after you canceled, or charged for a subscription you stopped. These are billing disputes and go through the American Express Dispute Center.

3. Goods and services problem. You made the purchase, but something went wrong after. The item never arrived, it was broken, the service was not what was promised, or the merchant refused to issue the refund you were owed. These also go through the billing dispute path.

Picking the right path matters because each one has different rules. Fraud cases trigger Amex fraud protection and a new card number. Billing disputes don’t. Filing a fraud claim for a real purchase you just regret can be flagged as misuse.

If you think your card has been stolen or has been used by someone else, call the Amex Security Team right away at 1-800-528-4800. Don’t file an online dispute first. The phone team can lock your card, send a replacement, and start a fraud investigation in one call.

For everything else, the dispute with the Amex credit card transaction process online is the fastest route.

💡 Pro Tip: Take a screenshot of the charge on your statement before you do anything. If the merchant later refunds it or the charge changes, having the original record protects your case.

Should You Contact the Merchant Before Disputing With Amex?

Yes, in most cases. Amex actually expects you to try the merchant first for goods and services issues. A quick call or email often solves the problem in a day, with no paperwork.

Reach out to the merchant if:

- The item was wrong, late, or damaged

- You were charged twice by mistake

- You canceled a subscription, but were still billed

- A refund was promised, but never showed up

Give the merchant a clear deadline, like 7 to 10 business days, to fix it. Keep every email, chat log, and receipt. If they refuse, ignore you, or the deadline passes, you’ve now got proof you tried. That proof makes your Amex case much stronger.

Skip the merchant step and go straight to Amex if:

- The charge is from a business you don’t recognize at all

- Your card was used without your permission

- The merchant is out of business or unreachable

- The merchant is hostile, threatening, or clearly dodging you

What Qualifies as a Valid Reason to Dispute an Amex Charge?

Not every charge you dislike is something you can dispute. Amex follows rules set by federal law and card network policy. Knowing what counts as a valid reason saves you time and keeps your case from being denied.

Valid reasons to dispute include:

- Unauthorized charge. You didn’t make it, and you didn’t let anyone use your card.

- Wrong amount. The merchant charged more than the agreed price.

- Duplicate charge. You were billed twice for the same purchase.

- Goods not received. You paid, but the item never arrived.

- Goods not as described. The product is broken, fake, or very different from what was advertised.

- Service not provided. A repair, booking, or service you paid for didn’t happen.

- Credit not processed. You returned the item or canceled, but the refund never posted.

- Subscription billed after cancellation. You stopped the service but kept getting charged.

- Recurring charge from a free trial you tried to cancel. Especially common with apps and streaming.

What doesn’t count as a valid reason to dispute:

- You changed your mind about the purchase.

- You forgot you signed up for a subscription.

- A family member used your card with your earlier permission.

- You think the product is overpriced now that you’ve used it.

- You’re unhappy with the service, but got what was described.

Buyer’s remorse is the most common reason disputes get denied. Amex will side with the merchant if you got what you paid for, even if you regret buying it.

For billing error cases, federal law gives you specific rights under the Fair Credit Billing Act. For goods or services not received or items not as described, you’ll need to show proof of what was promised versus what you got.

⚠️ Mistake to Avoid: Filing a fraud claim for a charge you actually made (because you think it’ll be faster) can trigger a fraud investigation against you, not just the merchant. Always pick the category that matches the truth.

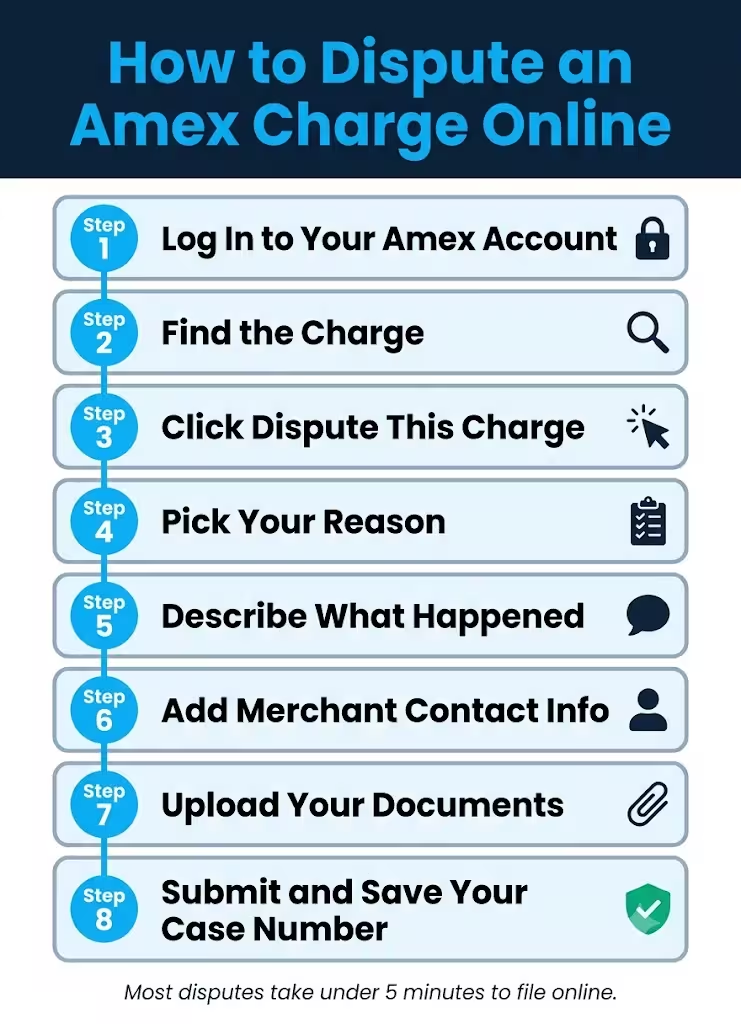

How to Dispute an Amex Charge Online (Step-by-Step)

The online method is the fastest way to file. Most people finish in under five minutes. Here’s exactly how to do it.

Step 1: Log in to your Amex account. Go to americanexpress.com and sign in with your username and password. If you have two-factor turned on, have your phone ready.

Step 2: Find the charge. Click on “Statements & Activity” in the top menu. You’ll see a list of recent transactions. Scroll or search for the charge you want to dispute. Click on it to open the details.

Step 3: Click “Dispute This Charge.” You’ll see this option under the transaction details. On mobile, you may need to tap the three dots or scroll down. This opens the Amex Inquiry and Dispute Center.

Step 4: Pick the reason. Amex gives you a list of dispute reasons. Pick the one that matches your situation. Common options include:

- “I do not recognize this charge”

- “I was charged more than once”

- “I did not receive the merchandise or service”

- “The merchandise was not as described”

- “I canceled this service”

- “I returned the item and have not received credit”

Step 5: Describe what happened. A text box appears for your story. Keep it short and clear. Stick to the facts: dates, amounts, and what went wrong. Don’t add emotion or extra details that aren’t useful.

Step 6: Add the merchant contact info you tried. If you reached out to the seller first, list who you spoke to, when, and what they said. This shows Amex you made a good-faith effort.

Step 7: Upload your documents. You’ll see an upload button for receipts, emails, screenshots, or photos. Add anything that supports your case.

Step 8: Submit and save the case number. Once you click submit, Amex gives you a case number. Write it down or screenshot it. You’ll use it to track progress and reference your dispute in any future calls.

After you submit, Amex usually applies a provisional credit within 1 to 2 business days. The disputed amount comes off your balance while they investigate.

How to Dispute an Amex Charge by Phone

Some people prefer to talk to a person. Call the number on the back of your card, or use 1-800-528-4800 for personal cards. Tell the rep you want to dispute a charge. They’ll ask the same questions the online form asks. Have your case details and any documents ready to email or fax in.

Phone disputes are good for:

- Confusing situations that need explaining

- Cases with lots of back-and-forth with the merchant

- People who aren’t comfortable with online forms

- Time-sensitive issues where you want instant confirmation

How to Dispute an Amex Charge by Mail

Mail is the slowest option, but it creates a paper trail that some people prefer. Send a written notice to:

American Express P.O. Box 981535 El Paso, TX 79998-1535

Include your name, account number (last four digits are safer than the full number), the charge date, the amount, the merchant name, and a clear explanation of the problem. Send it by certified mail with a return receipt so you have proof Amex got it.

Under the Fair Credit Billing Act, written disputes must be received within 60 days of the statement date for full federal protection.

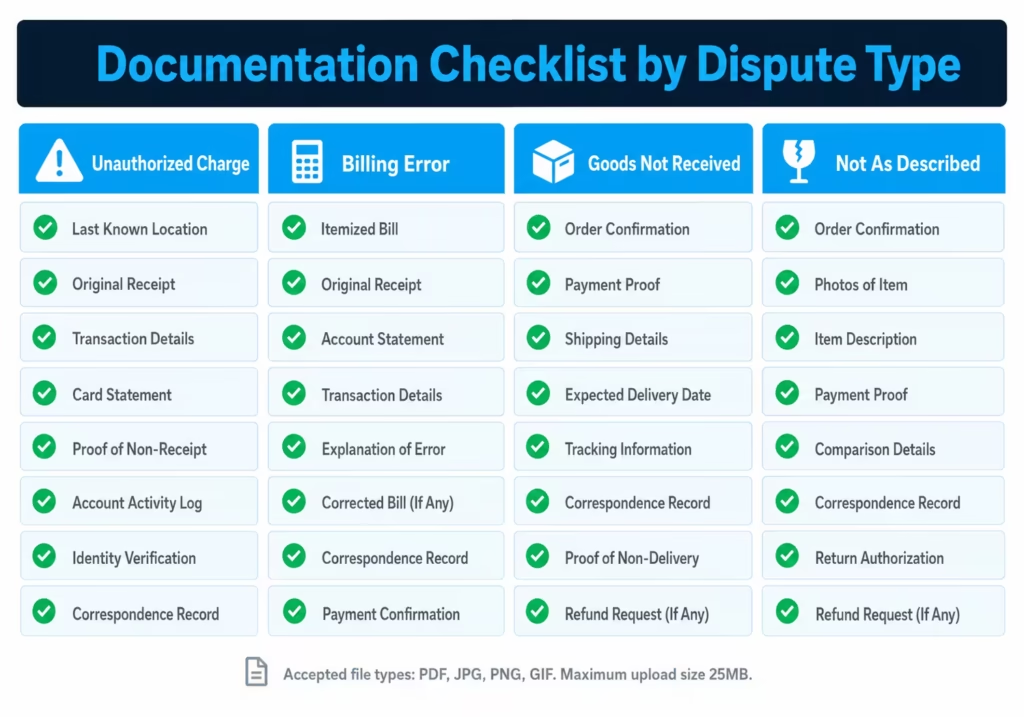

What Documentation to Gather Before You File

Strong supporting documentation is the single biggest factor in winning a dispute. Amex investigators look at the paper, not your feelings about the case.

What to gather depends on the type of dispute.

For unauthorized charges:

- Your last known location when the charge happened

- A police report (helpful but not always required)

- Any emails or texts from the merchant you don’t recognize

- Proof your card was in your possession (if it’s a physical card, use)

For billing errors (wrong amount or duplicate charge):

- The original receipt or order confirmation

- A screenshot of your statement showing both charges

- Any agreement showing the correct price

For goods not received:

- Order confirmation with the promised delivery date

- Shipping tracking that shows the item never arrived

- Emails to the merchant asking where it is

- The merchant’s response (or lack of one)

For goods not as described:

- Photos of what you received

- The original product listing or ad (screenshot it now if it’s still live)

- Emails or chats with the merchant about the problem

- Any return shipping receipt if you sent it back

For canceled subscriptions still being charged:

- A screenshot or email confirming cancellation

- The date you canceled

- Statements showing charges after that date

File requirements for uploads: Amex accepts PDF, JPG, PNG, and GIF files. The total upload size cap is 25MB. If your files are too big, compress images or split PDFs into smaller files.

Keep the originals safe. If Amex asks for more proof later, you’ll want quick access.

How Long Do You Have to Dispute an Amex Charge?

Time limits matter. Miss them, and you lose your right to a refund, no matter how strong your case is.

Amex gives you up to 120 days from the original charge date for most disputes. This is the 120-day dispute window, and it’s more generous than the federal floor.

Federal law, through the Fair Credit Billing Act, requires card issuers to honor billing disputes for at least 60 days from the date the statement with the charge was mailed to you.

The Consumer Financial Protection Bureau enforces this rule and provides official guidance for consumers on billing disputes.

So you have two clocks:

- Federal protection: 60 days from the statement date

- Amex policy: 120 days from the charge date (in most cases)

Always treat the 60-day window as a hard floor. If you file within 60 days of the statement, you get full federal protection on top of Amex’s own policy.

For goods not received or service not provided, the 120-day clock often starts on the date the item was supposed to arrive, not the date you paid. That gives you extra time for slow shipping or future-dated services like flights or events.

File as soon as you can. Waiting weakens your case. Memories fade, merchants close, and proof gets harder to find.

Can You Dispute a Pending Amex Charge?

Not yet. Pending charges aren’t final, so Amex can’t formally dispute them. You have to wait for the charge to post, which usually takes 1 to 5 business days.

In the meantime:

- Contact the merchant. Many pending charges drop off if the merchant cancels them.

- Watch the charge daily. If it posts, file your dispute right away.

- If you suspect fraud, don’t wait. Call 1-800-528-4800 so they can lock your card now, even before the charge posts.

What Happens to Your Account While the Dispute Is Open?

Once you file, Amex usually moves quickly to take the disputed amount off your balance. This is called provisional credit.

Here’s how the disputed amount removal process works:

- You file the dispute.

- Within 1 to 2 business days, Amex credits the disputed amount back to your account.

- The credit shows as a temporary adjustment, not a final refund.

- Your statement balance and minimum payment are recalculated without the disputed charge.

- If Amex sides with you, the credit becomes permanent.

- If Amex sides with the merchant, the credit is reversed, and the charge returns to your balance.

This is a big relief. You don’t have to pay for something you’re fighting while the case is open.

About your minimum payment: You still have to pay your minimum payment during the dispute for the rest of your balance. Skipping it can hurt your credit and trigger late fees. The disputed amount comes off the minimum, but the rest of what you owe is still due on time.

You also don’t earn interest on the disputed amount while it’s in review. If the dispute is denied later, Amex may add the interest back, so don’t assume you’re off the hook on the cost side until the case closes.

Does Disputing an Amex Charge Affect Your Credit Score?

Filing a dispute does not directly hurt your credit score. Amex does not report a dispute as a negative event to the credit bureaus. You won’t get a ding for using a right you legally have.

What can hurt your score:

- Missing the minimum payment on the rest of your balance

- Letting your account go past due during the dispute

- Closing the card while a dispute is open (do not do this)

A dispute also doesn’t help your score. It’s neutral. Just keep paying the non-disputed portion on time, and your credit stays clean.

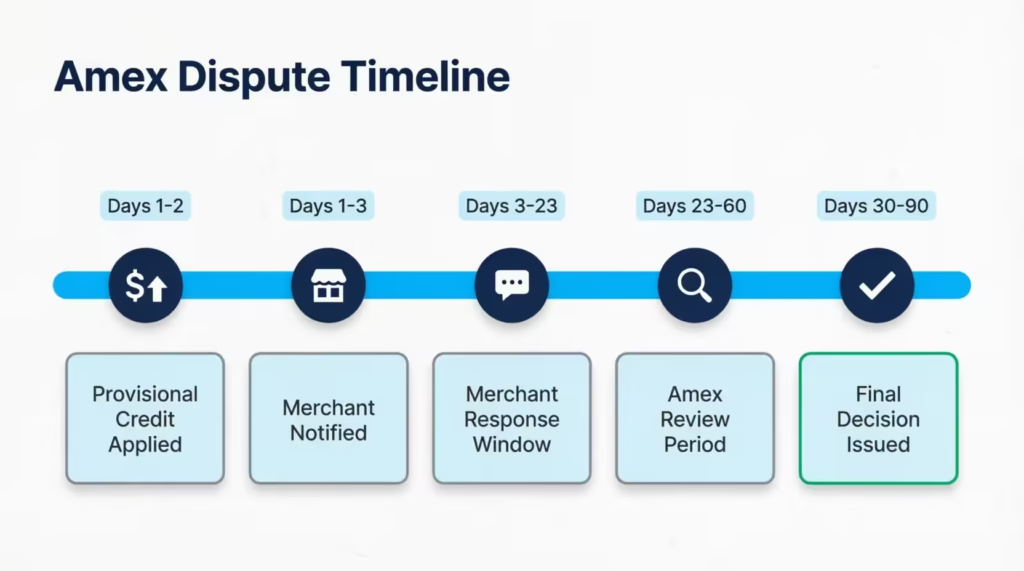

What Amex Does After You File a Dispute

Once your dispute lands, Amex starts the investigation. Here’s what’s happening behind the scenes.

Days 1-2: Provisional credit applied. Amex confirms your filing and removes the disputed amount.

Days 1-3: Merchant notified. Amex sends the dispute to the merchant with your reason and documents. This is the merchant response stage.

Days 3-23: Merchant response window. The merchant has up to 20 days to respond. They can:

- Accept the dispute and refund you.

- Push back with their own evidence (receipts, proof of delivery, signed contracts).

- Stay silent. If they don’t respond in time, you usually win by default.

Days 23-60: Amex review. If the merchant pushes back, Amex weighs both sides. They may ask you for more documents. Respond fast if they do. Slow replies often cost people their cases.

Days 30-90: Final decision. Most disputes wrap up within 30 to 60 days. Complex cases can take up to 90 days. Amex sends you the decision in writing through your online account or by mail.

If you win, the provisional credit becomes permanent. The case is closed.

If you lose, the provisional credit is reversed and lands back on your balance, and you’ll need to pay it like any other charge.

📌 Did You Know: Under the Fair Credit Billing Act, card issuers must resolve billing error disputes within two complete billing cycles, and no later than 90 days after getting your written notice. The CFPB outlines these protections in its consumer billing rights guidance.

How to Track Your Amex Dispute Status

You don’t have to wait blind. Amex lets you check on the case anytime.

To track your dispute:

- Log in to your Amex account online or in the app.

- Go to “Statements & Activity.”

- Find the disputed charge. It will be tagged with a dispute icon or note.

- Click on it to see the case status, timeline, and any messages from Amex.

Status updates usually include:

- Open / Under Review: Amex is still working on it.

- Awaiting Your Response: Amex needs more info from you. Act fast.

- Awaiting Merchant Response: The seller has the case.

- Resolved in Your Favor: You won.

- Resolved in Merchant’s Favor: You lost. The charge is back on your statement.

If you ever need to talk to a person, call the number on the back of your card and give them the case number you saved when you filed.

What to Do If Amex Denies Your Dispute

Losing a dispute is frustrating, but it’s not the end of the road. You have several ways to push back.

When Amex denies your case:

- The provisional credit is reversed.

- The original charge returns to your statement.

- You owe the amount by your next payment due date.

- Interest may be added back on the amount, dated from the original charge.

You’ll get a denial letter explaining why. Read it carefully. Most denials come from one of these reasons:

- The merchant gave proof that you got the goods or service.

- The dispute was filed past the deadline.

- The reason you picked doesn’t qualify under federal or Amex rules.

- Your documents were missing or unclear.

You’re not stuck. You have options.

Escalation Options After an Amex Dispute Denial

1. Submit a written appeal to Amex. You can ask Amex to reopen the case if you have new evidence. Send a written appeal to the dispute address with:

- Your case number

- A clear explanation of why the decision is wrong

- Any new documents that weren’t in the original filing

- A request for re-review

Amex usually responds to appeals within 30 days.

2. File a complaint with the CFPB. The Consumer Financial Protection Bureau handles complaints against card issuers. You can file online at consumerfinance.gov/complaint. Amex must respond to CFPB complaints within 15 days. Many disputes get reviewed again after a CFPB complaint, even ones that were denied twice.

3. Contact your state attorney general. If you think Amex broke a state consumer protection law, your state AG’s office can step in. This works best for clear rule violations, not just unhappy outcomes.

4. Small claims court. For amounts under your state’s small claims limit (usually $5,000 to $10,000), you can sue the merchant directly. Amex isn’t the defendant here. The merchant is. Bring all your documents, including the Amex denial.

5. Arbitration. Your Amex cardmember agreement likely has an arbitration clause. This lets you bring a formal complaint outside of court. It’s slower and more formal than small claims, but it’s an option for bigger amounts.

Most people win on appeal or after a CFPB complaint when their case has real merit and clean documents.

Tips to Strengthen Your Amex Dispute Before and After Filing

Winning a dispute often comes down to preparation. Small habits before you file, and quick action after, can flip a borderline case into a clear win.

Before you file:

- Try the merchant first for goods and services issues. Give them 7 to 10 business days, in writing.

- Save everything. Order confirmations, shipping notices, chat logs, emails, and photos. Screenshot product listings before they change.

- Pick the right reason. A dispute filed under the wrong category often gets denied even when the underlying case is strong.

- File fast. The closer to the charge date, the stronger your case. Aim for within 30 days when possible.

- Write a clear, short story. Skip the emotion. Stick to dates, amounts, and what went wrong.

After you file:

- Watch your email and Amex inbox daily. If Amex asks for more info, respond within 48 hours.

- Keep paying your minimum. The rest of your balance is still due.

- Don’t close the card. A closed account makes the dispute harder to track and resolve.

- Save the case number in a notes app or email folder you can find fast.

- Follow up if it goes quiet. If you hear nothing for 30 days, log in and check the status. Call if it’s stuck.

If the case is complex:

- Send a written summary to Amex with your timeline of events.

- Include only the documents that prove your point. Quality beats quantity.

- Reference the Fair Credit Billing Act by name if the case involves a billing error. It signals you know your rights.

A real example helps. Jennifer, a freelance designer in Austin, paid $1,275 for a custom desk from an online furniture store. The desk arrived cracked down the middle.

The seller offered a 20% partial refund. Jennifer refused, took photos from four angles, saved every email, and filed an Amex dispute for “not as described” with all 11 attachments uploaded at once. Amex sided with her in 22 days. The full $1,275 stayed credited. The difference was the paperwork.

Frequently Asked Questions (FAQs)

Will Amex refund me if I get scammed?

Yes, if someone used your card without permission, Amex treats it as a fraud case, not a billing dispute, and routes it to their security team. Call 1-800-528-4800 immediately so they can lock your card, issue a replacement, and launch a fraud investigation in one call.

Why is Amex so good at disputes?

Amex acts as both the card network and the card issuer, so it controls the entire dispute process without handing it off to a third-party bank. It also provides provisional credit within 1 to 2 business days, removing the disputed charge from your balance while the investigation runs.

What should I say in my credit card dispute?

Keep your description short and factual: state the charge date, the dollar amount, and exactly what went wrong. Skip emotion and stick to concrete details like “I was charged twice on March 4 for $89.99” or “the item arrived broken, and the merchant refused a return.”

What is the most successful reason for disputing a charge?

Unauthorized charges and undelivered goods have the highest success rates. This is because they are easy to prove with a police report, tracking record, or no merchant delivery confirmation. Buyer’s remorse and changed-mind disputes are the most commonly denied, regardless of how the case is framed.

Is there a downside to disputing a credit card charge?

You still need to make your minimum payment on the remaining balance during the dispute. If Amex decides in favour of the merchant, they may add any interest on the disputed amount back to your account. Filing a fraud claim for a charge you actually made can also trigger a fraud investigation against your own account.

Will I get my money back if I dispute a charge?

Amex applies a provisional credit within 1 to 2 business days, so the disputed amount comes off your balance while the case is open. If Amex sides with you, that credit becomes permanent; if the merchant wins, the charge returns to your statement.

Do merchants ever win chargebacks?

Yes, merchants benefit when they show proof that you got the goods or service, that the refund was issued, or that you approved the charge. Strong merchant documents can help with customer disputes. Examples include a signed delivery confirmation and a recorded cancellation policy.

Is it worth disputing a credit card charge?

Yes, especially since Amex gives you up to 120 days from the charge date to file and applies provisional credit almost immediately. The process takes under five minutes online, and most disputes with solid documentation resolve within 30 to 60 days.

Can you dispute a pending Amex charge?

No, Amex cannot formally open a dispute on a charge until it posts to your account, which usually takes 1 to 5 business days. If you suspect fraud on a pending charge, call 1-800-528-4800 right away so Amex can lock your card before the charge finalizes.

Does disputing an Amex charge hurt your credit score?

No, filing a dispute does not trigger any negative reporting to the credit bureaus. The only credit risk in an open dispute is missing your minimum payment on the rest of your balance. So, keep paying the non-disputed part on time.

Wrapping Up

Disputing a charge on your American Express card doesn’t have to feel overwhelming. Once you know your problem type, gather the right documents. Then, file within the 120-day window. This makes the process faster and fairer than many expect. We’ve covered every step, from the first click in the Amex Inquiry and Dispute Center to escalation if your case is denied.

This guide shows that the best approach is to act fast. Document everything carefully. Choose the right dispute reason from the start.

If you know a friend or family member who’s stuck staring at a charge they didn’t make or never got the product for, share this guide. It could put real money back in their pocket.