I’ve been there too. You’re staring at your Amex account, wondering why your credit line feels too tight for the bills, travel, or business expenses you need to cover. Maybe a recent purchase pushed your utilization higher than you’d like, or you’re prepping for a big spend and don’t want it to ding your score.

That’s why so many cardholders search for a clear way to handle an Amex credit limit increase.

The quickest way: log in to your Amex app or online account. Then, open “Manage Your Credit Limit” and submit a request. This usually only leads to a soft credit check.

Here’s a quick guide on every channel and question Amex asks. I’ll cover the soft-pull vs. hard-pull rules, how to fix denials, and the best timing tips. This way, you can boost your spending power confidently.

Key Takeaways

This guide explains how to request an Amex credit limit increase through the app, website, or phone, including soft pull versus hard pull rules, eligibility timing, denial reasons, and alternative options like opening a new card.

Core Facts:

- Amex offers three request channels (mobile app, online account, phone), and most decisions appear instantly while some take 2 to 7 business days for review.

- Most standard requests trigger only a soft credit pull, which does not affect your credit score, while unusually large jumps may require a hard pull with your consent first.

- Eligibility typically opens once an account is 60 days old, with stronger approval odds after 6 months of on-time payments and utilization under 30 percent.

- Amex generally allows one credit limit increase request every 6 months per card, and each card has its own separate 6-month timer.

- Amex also runs automatic credit limit reviews starting around the 6-month mark and periodically afterward, and these increases are typically soft-pull only.

- Charge cards like the Platinum Card have no preset spending limit, so cardholders can use the Check Spending Power tool to confirm if a planned purchase is likely approved.

Best for:

- Cardholders with an Amex account at least 60 days old who want to raise their spending power before a large purchase or to lower their utilization ratio.

- Existing Amex customers comparing the soft-pull request process against opening a new card for additional spending power.

- Cardholders who were recently denied an increase and want to understand the most common reasons before reapplying.

How to Submit a Credit Limit Increase Request

American Express has three ways for cardholders to ask for more spending power. You can use the mobile app, the online account, or call customer care.

Each channel asks for the same core details, but the path you click through is different, and so is the experience when a decision comes back. Most requests get an instant answer on screen. Some go into a short review, usually 2 to 7 business days, and you’ll get an email or in-app message when the verdict is ready.

Before you begin, collect your annual income, monthly housing payment, job status, and the new credit line you want. Having these ready avoids guessing under pressure, which often leads to weaker numbers that hurt your odds.

Requesting an Increase Through the Amex App

The app is the quickest route for most people. Open the American Express app and sign in with your User ID and password (or Face ID/Touch ID if you’ve set that up).

Follow these steps inside the app:

- Tap the Account tab in the bottom menu.

- Scroll to the Card Management section.

- Tap Manage Your Credit Limit.

- Tap Start Request.

- Enter the new credit limit you’d like. Pick a realistic figure, usually 10% to 30% above your current line, for the strongest approval odds on a soft pull.

- Please share your job status. Also, tell us your total yearly income before taxes. Finally, include your monthly housing cost. This should cover rent or mortgage, plus any taxes and insurance.

- Review the summary screen, agree to the terms, and tap Submit Request.

In most cases, the decision shows up on the next screen within seconds. If it goes to review, you’ll see a confirmation message and get a follow-up notification.

Requesting an Increase Through Your Online Account

If you prefer a full-size screen, the desktop site offers the same options. Sign in at americanexpress.com using your usual login.

Once logged in, take this path:

- Click Account Services in the top menu.

- Open the Manage Accounts section.

- Click Payment and Credit Options.

- Select Change Credit Limit (or Request Credit Limit Increase, depending on your card).

- Choose the card you want to update if you have more than one.

- Enter your requested new credit line.

- Update your annual income, employment details, and housing cost.

- Submit the form.

The web flow shows a clear summary of your current limit, average monthly spend, and new limit. This helps you choose a smart target more easily. You’ll get an instant answer or a “we’re reviewing your request” message with a follow-up timeline.

Requesting an Increase by Phone

Some cardholders like speaking to a person. This is true for larger jumps or special situations, like a recent income boost or a big one-time purchase.

Call the customer service number on the back of your card. For most U.S. personal cards, that number is 1-800-528-4800. For business cards, use 1-800-492-8468. If you have a cobranded card like Delta SkyMiles, Hilton Honors, or Marriott Bonvoy, use the number on the back. It will link you to a special team for those cards.

When the agent picks up, say clearly: “I’d like to request a credit limit increase on my account.” They’ll verify your identity, ask the same income, housing, and employment questions, and confirm your target limit. The phone channel is helpful if you want to explain context, such as a recent raise or a planned wedding, that an online form can’t capture.

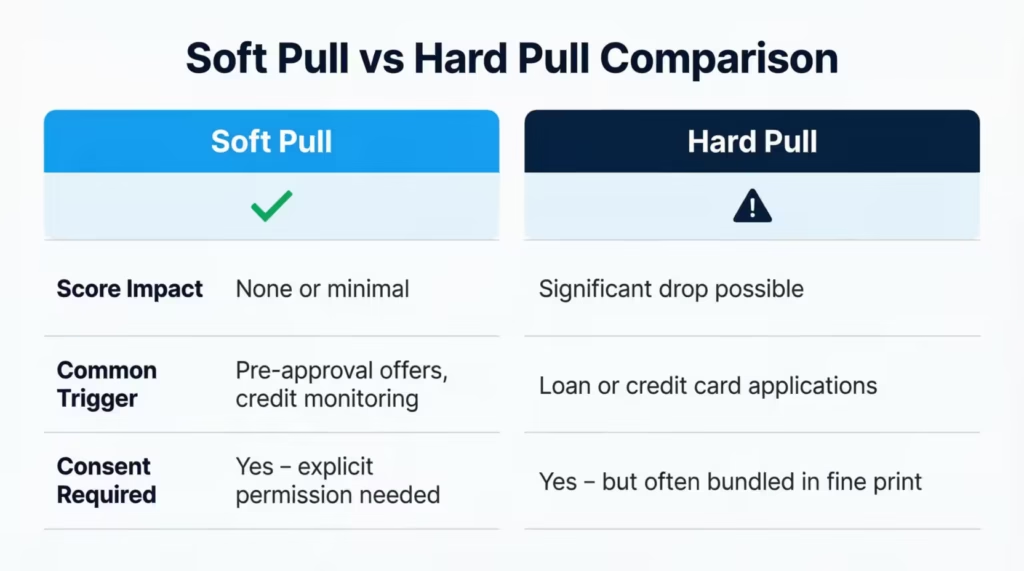

Will Requesting a Credit Limit Increase Hurt Your Credit Score

This is the question that stops most people from asking in the first place. The good news: in the vast majority of cases, an Amex request triggers a soft pull, which does not affect your credit score at all. A soft pull is a background check that Amex runs on your file, but credit bureaus don’t share it with lenders or factor it into your score.

That said, there are situations where Amex may run a hard inquiry instead. A hard pull does show up on your credit report and can ding your FICO score by a few points, usually 5 to 10, with the impact fading within a year. Knowing which scenario applies to your request makes a big difference, so here’s what triggers each one.

Soft Pull vs. Hard Pull on Amex Requests

For most standard requests, especially if the new limit is about three times your current one, Amex uses a soft pull and internal data. This includes your payment history and average spending pattern. No hard inquiry is added to your credit file.

A hard pull may happen when:

- You ask for an unusually large jump, such as doubling or tripling your current limit, or jumping past a high dollar threshold like $25,000.

- Your account is fairly new, and Amex doesn’t yet have enough internal data to decide.

- Your file shows recent credit issues that need a deeper review.

If a hard pull is needed, Amex must get your consent first. You’ll see a clear pop-up or on-screen notice telling you that continuing will result in a hard inquiry. You can decline at that point and either lower your requested amount or skip the request entirely.

According to Experian, a single hard inquiry typically drops a score by less than 5 points and falls off your report after two years, but the impact on scoring only lasts about 12 months.

💡 Pro Tip: If you’re worried about a hard pull, ask for a modest jump first, such as 25% above your current limit. Soft-pull approvals build internal trust with Amex, which makes future increases easier.

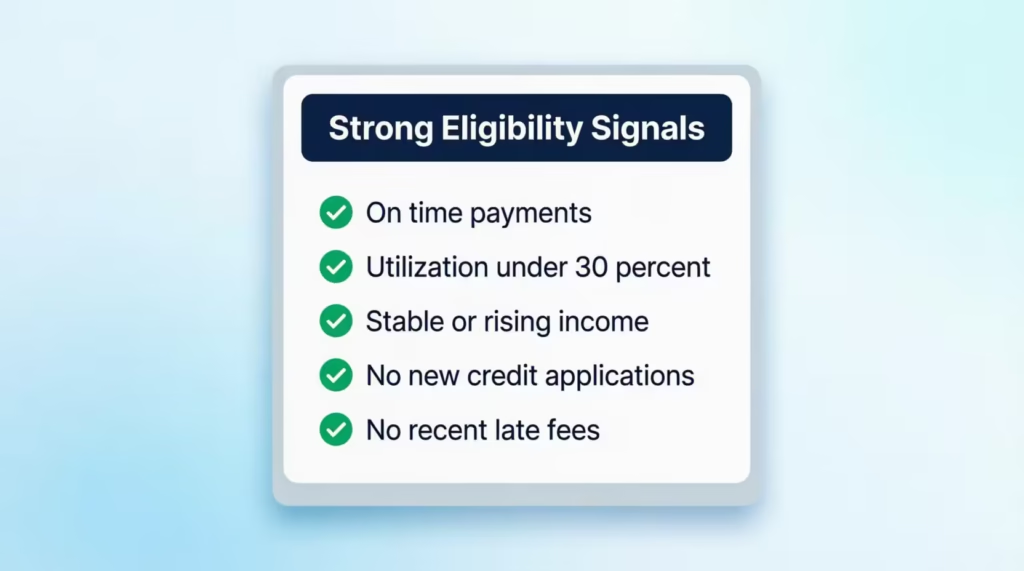

When You’re Eligible to Request an Increase

Amex doesn’t publish a strict eligibility chart, but the company follows clear internal patterns. Most cardholders can ask for a higher limit once their account is 60 days old. The chances get much better after six months. Before 60 days, the request button is usually hidden, or your request gets an automatic decline.

Strong eligibility signals include:

- On-time payments on the Amex card every month since opening.

- A current balance well under your limit (under 30% utilization is ideal, under 10% is even better).

- Stable or rising income compared to when you applied.

- No new credit applications in the last 3 to 6 months across all lenders.

- No returned payments, late fees, or over-limit issues in the past 12 months.

If you missed a payment recently or your utilization is sitting at 80% the day you ask, the request is far more likely to get denied. Fix those signals first, then try.

How Often You Can Request an Increase

American Express generally lets you submit a new request every 6 months per card. Some cardholders report success at the 90-day mark, but six months is the safe default. Asking too soon often results in a denial that cites “recent request on file,” which wastes the attempt without giving you new information.

If you have several Amex cards, the 6-month clock runs separately for each one. You can request an increase on your Gold card today and your Blue Cash card a few weeks later, as long as each card hasn’t been asked for within the last 6 months.

What Information Amex Will Ask You For

The request form is short, but every field matters. Amex uses these answers, plus your internal account history and a credit bureau check, to decide. Be ready to enter:

- Total annual income (gross, before taxes).

- Employment status (employed, self-employed, retired, student, homemaker, unemployed).

- Total monthly housing payment (rent or full mortgage payment with taxes and insurance).

- Your requested new credit limit is a specific dollar amount.

- Reason for the request (sometimes asked on the phone or in extended review).

Answer truthfully, because Amex can ask for proof, such as a recent pay stub or tax return, especially for big jumps.

How to Answer the Income and Reason Questions Strategically

Many cardholders shortchange themselves by reporting only their base salary. The Consumer Financial Protection Bureau allows credit card issuers to consider any income you have reasonable access to, which often includes more than your paycheck. Eligible sources can include:

- Base salary and wages (gross).

- Bonuses, commissions, and tips averaged over the past year.

- Self-employment or freelance income.

- Investment income (dividends, interest, rental income).

- Retirement income (Social Security, pensions, IRA/401(k) withdrawals).

- For applicants 21 and older, income from a spouse or partner you reasonably share access to, as confirmed by the CFPB rule.

For the reason field, keep it specific and positive. Examples that work well: “to support upcoming business travel expenses,” “to lower my utilization ratio,” or “to cover a planned home renovation.” Avoid vague reasons like “just in case” or red flags like “to consolidate other card debt,” which can hurt your odds.

⚠️ Mistake to Avoid: Don’t inflate your income. Amex may request documentation, and a mismatch can lead to account review or closure. Use your real, verifiable total.

Why Some Amex Cards Don’t Have a Traditional Limit to Increase

If you carry a Platinum Card, a traditional Gold Card, or a Business Platinum Card, you may have searched for the “increase limit” button and found nothing. That’s because these are charge cards, not credit cards. Charge cards have no preset spending limit, which means there’s no fixed ceiling to raise.

Instead of a hard cap, Amex evaluates each purchase based on your spending patterns, payment history, account age, credit profile, and current resources. A $4,000 purchase that gets approved one month might be paused another month if your patterns shift. Because there’s no set limit, the standard “request a credit limit increase” path doesn’t apply.

Using Check Spending Power Instead

For charge cards, Amex offers a tool called Check Spending Power. It lets you ask, before you swipe, whether a specific purchase amount is likely to be approved.

To use it:

- Sign in to the Amex app or website.

- Open the Account menu and look for Check Spending Power.

- Enter the exact dollar amount of the purchase you’re planning.

- Submit the check.

Amex returns a yes or no within seconds. A “yes” is not a guarantee, but it’s a strong signal that the charge will go through. If the answer is “no,” consider making a payment toward your current balance first, then re-check. Paying down a charge card balance boosts your spending power quickly, usually within 1 to 2 business days after the payment goes through.

Does Amex Increase Your Limit Automatically

Yes, Amex does run automatic account reviews, and these can lead to a higher credit line without you asking. The first automatic review usually happens around the 6-month mark, and then periodically after that, often every 6 to 12 months.

During an automatic review, Amex looks at:

- Your payment behavior on the card.

- Your spending patterns versus your current limit.

- Updates to your credit file at the bureaus.

- Any income data they already have on file.

If you qualify, you’ll get a notification in the app, by email, or through a letter showing the new, higher limit. No action is needed on your part. Unlike some issuers, Amex generally does not require you to opt in for an automatic increase, but you can decline if you don’t want a higher line. Automatic increases are almost always soft-pull only, which makes them a clean win for your credit profile.

📌 Did You Know: Heavy, consistent card use that you pay off in full each month is one of the strongest signals for an automatic Amex credit limit bump. Light, sporadic usage rarely triggers a review.

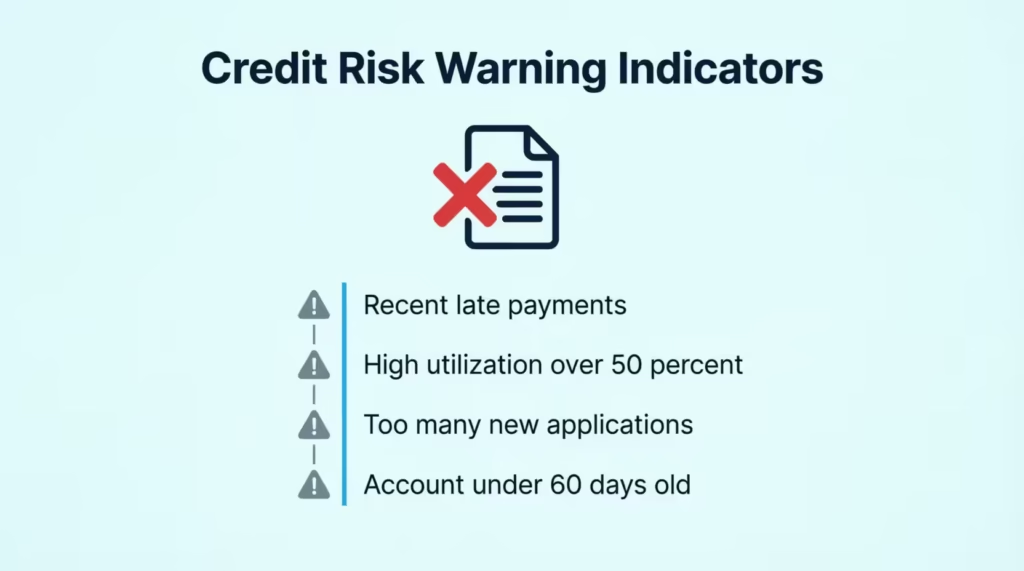

Why a Credit Limit Increase Request Gets Denied

A denial stings, but it’s almost always tied to specific signals Amex can see. The most common reasons include:

- Recent late or missed payments on the Amex card or another account.

- High utilization across your credit cards, typically over 50%.

- Too many new credit applications in the past 3 to 6 months.

- Account too new, often under 60 days old.

- Income that doesn’t support a higher line based on Amex’s internal models.

- A request submitted too soon after a prior request, usually within 6 months.

- Returned payments or recent over-limit activity.

- A drop in your credit score since your last review.

- An existing balance close to your current limit, which signals possible repayment stress.

When the denial comes, Amex sends a notice called an adverse action letter within about 7 to 10 days. It lists the main reasons for the decline and explains your right to a free copy of the credit report used in the decision. Reading that letter carefully is the fastest way to know exactly what to fix.

What to Do After a Denial

A denial is not the end of the road. Take these steps to bounce back stronger:

- Read the adverse action letter and note each reason listed.

- Get your free credit reports from all three bureaus at AnnualCreditReport.com. It’s the only federal source that offers them for free.

- Dispute any errors you find, such as accounts that don’t belong to you or paid balances showing as unpaid.

- Pay down balances to get every card under 30% utilization, and ideally under 10%.

- Pause new credit applications for at least 6 months.

- Set up autopay for at least the minimum on every card to prevent future late marks.

- Wait 6 months before submitting a new request, unless your situation has changed dramatically (such as a major raise) and you want to call in.

If you believe the denial was based on incorrect information, you can also call Amex and ask for a reconsideration. Be ready to share updated income or explain a one-time issue (like a hospital stay) that affected past payments.

Best Practices to Improve Your Approval Odds

Approvals come down to looking low-risk and high-value at the same time. Use this checklist before submitting your next request:

- Pay every Amex bill in full and on time for at least 6 months straight.

- Keep total credit utilization under 30%, with under 10% being ideal.

- Use the card regularly. Charges between 10% and 30% of your current limit each month show healthy activity.

- Update your income inside your Amex profile any time your earnings rise.

- Avoid opening new accounts or applying for other credit in the 90 days before your request.

- Ask for a realistic jump, usually 10% to 30% above your current line.

- Wait at least 6 months between requests on the same card.

- Make sure no recent returned payments or late fees sit on your file.

- Check that your credit score has held steady or improved since your last application.

Following this list won’t guarantee approval, but it stacks every controllable factor in your favor.

Opening a New Card as an Alternative Way to Increase Spending Power

If a limit raise isn’t possible, or if you want more total spending room, opening a second Amex card is a strong workaround. American Express allows most cardholders to hold up to 5 Amex credit cards at the same time (charge cards don’t count toward this cap). Each new credit card comes with its own limit, which adds to your total available credit across Amex.

A new card can also help you:

- Earn a fresh welcome bonus, often worth hundreds of dollars in points, miles, or statement credits.

- Diversify your rewards (for example, pairing a cash-back card with a travel card).

- Lower your overall utilization ratio, since a new limit increases your total available credit.

Keep these trade-offs in mind. A new card application triggers a hard inquiry, which can drop your score by a few points.

The new account also lowers your average age of accounts, another small scoring factor. For most cardholders with good credit, a higher total limit and the welcome bonus are worth any minor drawbacks in the short term.

If you’re choosing between a new card and a limit increase, think about this: if you have fewer than five cards and good credit, a new card usually gives you more value. If you’re at the cap or you don’t want a hard inquiry, stick with the increase request path.

Frequently Asked Questions (FAQs)

How do I raise my Amex credit limit?

Log in to the Amex app or website and open “Manage Your Credit Limit” to submit a request, or call 1-800-528-4800 for personal cards. Most requests get an instant decision and use only a soft credit check.

Does Amex increase the limit automatically?

Yes, Amex runs automatic reviews starting around the 6-month mark and then every 6 to 12 months after that. These reviews check your payment habits and spending patterns. If you qualify for an increase, it comes without a hard inquiry.

What is the Amex 2-90 rule?

The 2/90 rule is an unofficial Amex application guideline rather than a formally published American Express policy.

Can I spend $75,000 on an Amex Platinum?

The Platinum Card has no preset spending limit because it’s a charge card. Approval relies on your spending habits, payment history, and account status, not a set amount. Use the Check Spending Power tool in the app to see if a specific amount, like $75,000, is likely to go through before you charge it.

Is it hard to get a $10,000 credit limit?

It’s not inherently hard if your account is at least 6 months old, your utilization stays under 30%, and you’ve paid on time consistently. Requesting 10% to 30% above your current limit, rather than jumping straight to $10,000, gives you the best odds of a soft-pull approval.

What if I use 90% of my credit limit?

Using 90% of your limit signals repayment stress to Amex and is one of the most common reasons a credit limit increase request gets denied. It can also hurt your credit score, since utilization above 30% works against you even if you pay on time.

How often can I request a credit limit increase on Amex?

Amex generally allows one request every 6 months per card, and asking sooner often results in an automatic denial citing a recent request on file. If you have multiple Amex cards, each one has its own separate 6-month clock.

Will requesting a credit limit increase hurt my credit score?

In most cases, no, because Amex typically uses a soft pull that doesn’t affect your score at all. A hard pull only applies to unusually large increase requests, such as doubling your limit, and Amex will ask your permission first.

What happens if my Amex credit limit increase gets denied?

Amex sends an adverse action letter within 7 to 10 days listing the specific reasons for the denial. You can pull free credit reports from all three bureaus at AnnualCreditReport.com, fix any errors, and reapply after 6 months once your utilization and payment history improve.

How much income should I report when requesting an increase?

Report your total gross annual income. This includes salary, bonuses, self-employment earnings, investment income, and retirement income, as per CFPB rules. Applicants 21 and older can also include income from a spouse or partner they reasonably share access to.

Wrapping Up

Getting more spending power on your Amex card comes down to knowing the right channel, the right timing, and the right numbers to enter. The app, the website, and the phone line all work, but the app is fastest.

Most requests use a soft pull, so they won’t hurt your score. Eligibility opens around the 60-day mark. Also, a 6-month gap between requests helps keep your odds strong. Based on the patterns above, the most effective approach is to pay on time, keep utilization low, and ask for a realistic jump.

If you know a friend stretching their Amex limit too thin, share this guide so they can boost their credit line the smart way.