When you see those sleek Amex Gold and Platinum cards on social media, it’s easy to wonder if you could land one as your very first card. Many young adults with no credit history feel stuck, unsure if applying now will hurt their score or open a door they’ve been waiting for. The thought of asking, can I get Amex as my first credit card, often comes with confusion, fear, and zero clarity.

The short answer: YES, it’s possible, but only with specific entry-level Amex cards and a credit score of at least 670.

In this guide, we’ll walk you through which cards beginners can actually get, how to check your odds risk-free, and a step-by-step plan to qualify faster.

Key Takeaways

This guide explains whether you can get an American Express card as your first credit card, which entry-level cards are realistic for beginners, what credit score you need, and how to build your credit to qualify faster.

Core Facts:

- Getting an Amex card as a first credit card is possible, but requires a FICO score of at least 670 and at least a few months of existing credit history. Amex offers no secured cards in the United States.

- The most accessible entry-level options for beginners are the Blue Cash Everyday Card and the Delta SkyMiles Blue Card, both with no annual fee and a 670+ score requirement.

- Amex evaluates more than your credit score. Income, debt-to-income ratio, length of credit history, and recent late payments all factor into approval decisions.

- Amex uses a pre-approval tool called Apply with Confidence that runs a soft pull on your Experian file. It shows whether you are likely to be approved without triggering a hard inquiry or affecting your score.

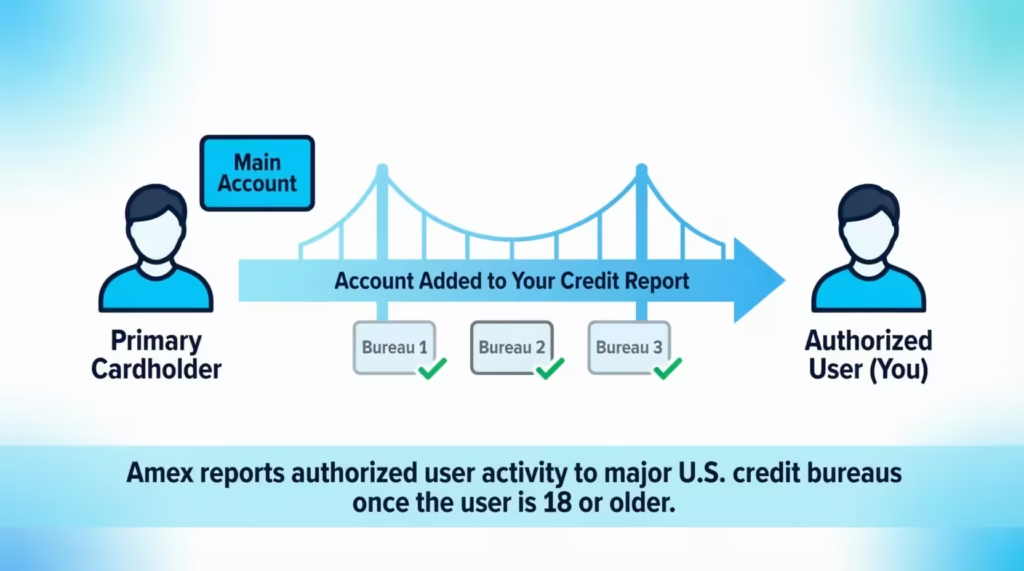

- Becoming an authorized user on an existing Amex account is a legitimate path to building credit. Amex reports authorized user activity to major U.S. credit bureaus once the user is 18 or older.

- Amex enforces a once-per-lifetime welcome bonus rule. Each card’s signup bonus can only be earned once, even if the card is closed and later reopened.

Best for:

- Young adults or first-time credit users who already have 6 or more months of credit history and a FICO score near 670 and want to make their first Amex card the right choice from the start.

- Beginners with no credit history who need a realistic step-by-step plan to build their score before applying for an entry-level Amex card.

- Anyone who has been denied an Amex card and wants to understand the reconsideration process or what to fix before reapplying.

Can You Get an American Express Card as Your First Credit Card?

Yes, you can get an American Express card as your first credit card, but only under the right conditions. The reality is that Amex does not offer secured cards or true “starter” cards in the United States. Every Amex card sold today expects you to already have some credit on file. So if you walk in with zero credit history, your odds are slim, even for the most beginner-friendly options.

Most approvals for an entry-level Amex happen when the applicant already has a FICO score of 670 or higher. That means a thin file or a clean slate usually won’t cut it. You will likely need at least a few months of healthy credit activity before Amex will say yes.

“First Amex Card” vs. “First Credit Card Ever”: Why It Matters

These two questions sound the same, but they lead to very different answers.

A “first Amex card” means you already have one or two credit cards from other banks. You’ve built a short but real credit history. In this case, applying for an entry-level Amex is a reasonable next step.

A “first credit card ever” means you have no open credit accounts and no credit history at all. In this situation, applying directly for an Amex is risky. Approval odds are low, and a denial can sit on your record. The smarter path is to start with a secured card or a student card, build six to twelve months of clean activity, then move on to Amex.

Knowing which group you fall into shapes every other decision in this guide.

What Credit Score Do You Need for an American Express Card?

There isn’t one fixed score that opens every Amex door. The number you need depends on which card you want. Each tier has its own unwritten benchmark, based on real applicant data.

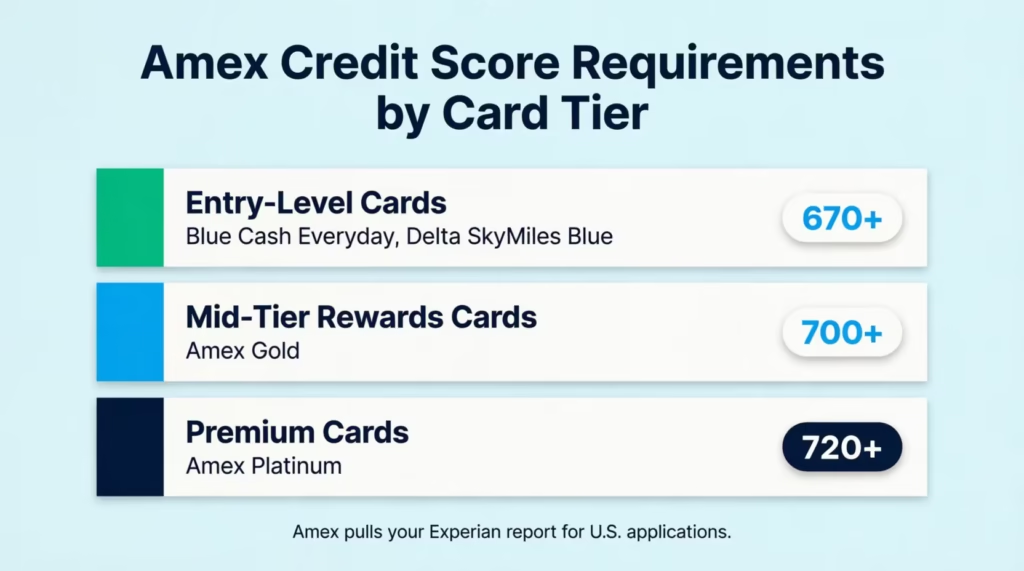

For entry-level cards like the Blue Cash Everyday or Delta SkyMiles Blue, a FICO score of 670 or higher gives you a fair shot at approval. This is the lowest realistic range for any Amex card in the U.S.

For mid-tier rewards cards like the Amex Gold, most approved applicants have a score of 700 or higher. Some go through with mid-680s, but those cases often involve high income or low debt.

For premium cards like the Platinum, approved applicants usually have scores of 720 or higher, plus a longer credit history.

Amex pulls your Experian report when reviewing applications in the U.S. So before you apply, check your Experian score, not just your Credit Karma or Chase score. You can pull a free Experian report through MyCredit Guide by Amex, which uses a soft pull and won’t ding your score.

Other Factors Amex Evaluates Beyond Your Credit Score

Your FICO number is only one piece of the puzzle. Amex looks at the full picture before approving anyone.

Income matters a lot. A higher income signals you can handle the credit line being offered. For students and young workers, even part-time income or stipends count, as long as you report it honestly.

Your debt-to-income ratio also plays a role. If you already carry high balances on other cards, Amex may pass even with a decent score. A ratio under 36% is generally seen as healthy.

Length of credit history is another factor. Six months is the bare minimum for most approvals. A year or more gives you a stronger case.

Amex also checks for any recent late payments, collections, or bankruptcies. Even one late payment in the past 12 months can sink your application.

💡 Pro Tip: Pay down balances before your statement closes, not after. Amex sees the reported balance on your Experian file, so a lower reported amount makes your debt-to-income ratio look cleaner on application day.

The Easiest American Express Cards to Get as a Beginner

Not every Amex card is built the same way. Some are far more accessible for new applicants. Here are the three best entry points for beginners in the U.S.

The Blue Cash Everyday® Card is the most popular first Amex. It has a $0 annual fee, asks for a FICO score of about 670 or higher, and offers solid cash back at U.S. supermarkets, gas stations, and online retail. For a first Amex, this card hits the sweet spot of low cost and useful rewards.

The Delta SkyMiles® Blue American Express Card is another beginner-friendly pick. It also has a $0 annual fee and gives you flat-rate miles on dining and Delta purchases. It’s a strong choice if you fly Delta even a few times a year.

The American Express® Green Card is a step up. It carries a $150 annual fee but offers stronger travel and dining rewards. It typically needs a score of 700 or higher, so it’s best for applicants who already have a few months of clean credit activity.

| Card | Annual Fee | Score Needed | Best For |

|---|---|---|---|

| Blue Cash Everyday | $0 | 670+ | Cash back on groceries and gas |

| Delta SkyMiles Blue | $0 | 670+ | Occasional Delta flyers |

| Amex Green | $150 | 700+ | Travel and dining rewards |

Can I Get the Amex Gold Card as My First Credit Card?

It’s possible, but it’s not the smart move for most first-time applicants. The Amex Gold Card is a mid-premium card with a $325 annual fee and powerful dining and grocery rewards. Approved applicants usually have a FICO score of 700 or higher, plus at least one year of credit history.

If your first card ever is the Gold, you’re paying a steep annual fee while you’re still learning how credit works. A better path is to start with the Blue Cash Everyday for 12 months, build your score and habits, then upgrade or apply for the Gold.

Can I Get the Amex Platinum Card as My First Credit Card?

In almost every case, no. The Platinum Card has a $695 annual fee and is built for travelers who already spend heavily on flights, hotels, and dining. Most approved applicants have FICO scores of 720 or higher, multi-year credit histories, and high incomes.

Even if Amex did approve a first-time applicant for Platinum, the perks would likely go unused. The card pays back its fee through lounge access, hotel credits, and travel benefits, not through everyday spending. For a beginner, the math just doesn’t work.

Can I Get the Amex Cobalt Card as My First Credit Card? (Canada)

For Canadian readers, the picture looks a little different. The American Express Cobalt® Card is issued by Amex Bank of Canada and is one of the most popular cards in the country.

The good news: Amex doesn’t list a minimum personal income for the Cobalt. The official eligibility rules from American Express Canada only require that you are a Canadian resident, have a Canadian credit file, and are of the age of majority in your province or territory.

That said, approval isn’t automatic. Most approved Cobalt applicants have a credit score of 660 or higher, with 700+ giving you a much better shot. The card uses a monthly fee structure of $15.99 per month, which works out to about $192 per year. That’s not pocket change for a first credit card.

If you have at least six months of clean credit activity in Canada, a 660+ score, and steady income, the Cobalt is realistically within reach as a first card. But if your credit file is brand new, start with a no-fee card from a Canadian bank for six to twelve months first. Then apply for the Cobalt with stronger numbers behind you.

⚠️ Mistake to Avoid: Don’t apply for the Cobalt the same week you open your first bank account or arrive in Canada. Without a Canadian credit file, the application will be denied no matter how high your income is.

How to Check if You’ll Be Approved for Amex Without Hurting Your Credit Score

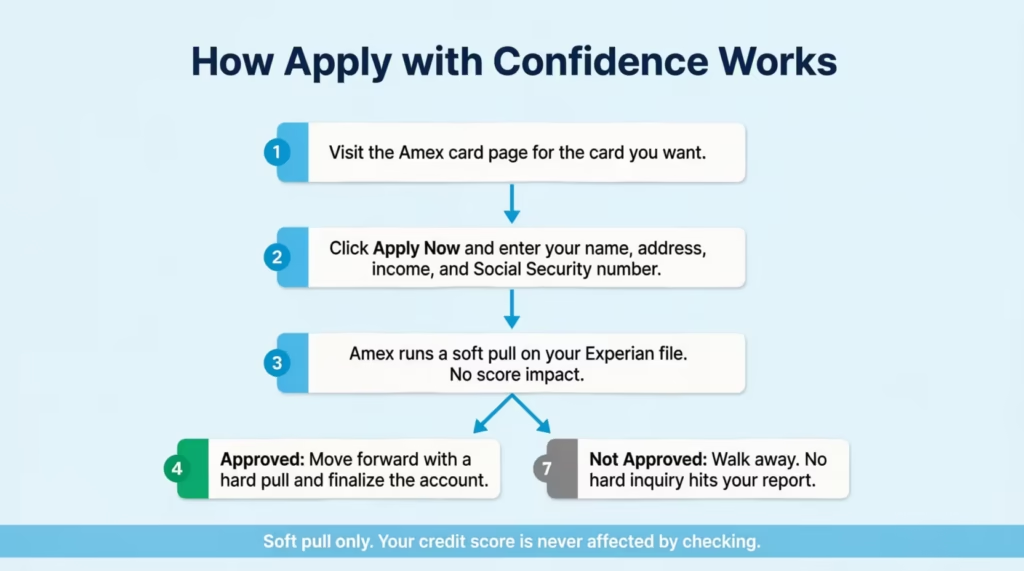

Before you submit a full application, you can check your approval odds for free, with zero score impact. Amex offers a tool called Apply with Confidence, which uses a soft credit pull to tell you if you’ll likely be approved.

Here’s how it works in plain steps:

Step 1: Visit the Amex card page for the card you want, such as the Blue Cash Everyday.

Step 2: Click “Apply Now” and start filling out the application form with your name, address, income, and Social Security number.

Step 3: Amex runs a soft pull on your Experian file. This soft inquiry does not affect your credit score in any way.

Step 4: Within a few seconds, you’ll see one of two messages. Either Amex confirms you’re approved and gives you the card terms, or it tells you that you don’t qualify right now.

Step 5: If the result is positive, you can move forward with a hard pull and finalize the account. If it’s negative, you simply walk away. No hard inquiry hits your report.

This tool is gold for nervous first-time applicants. It lets you test the waters before any real risk. Bankrate confirms that the Apply with Confidence tool uses a soft credit check that does not show up on your credit report or lower your score.

One thing to know: not every Amex card supports this tool every day. Availability can shift. If you don’t see the option on the card you want, try checking back in a few days.

How to Use Authorized User Status to Work Toward Your Own Amex Card

If you can’t get approved on your own yet, becoming an authorized user is one of the fastest ways to build a credit file. Amex calls authorized users “Additional Card Members.” When a parent, partner, or family member adds you to their Amex card, you get your own card with your name on it, but the main account stays in their name.

The big win here is credit reporting. Amex reports authorized user activity to the major U.S. credit bureaus once the user is 18 years or older. That means the primary cardholder’s payment history, account age, and credit limit can all start to show up on your credit report. Over time, this builds your file even though you didn’t open the account yourself.

A few rules to know before you sign up. The primary cardholder must trust you completely, since they remain fully responsible for paying the balance. If they miss payments or run up huge balances, your credit will take the hit too, not just theirs. So pick the right person, ideally someone with a long, clean Amex history.

The cost is also worth checking. Some Amex cards charge a fee for additional card members, while others are free. For example, the Amex Gold lets you add up to five additional cards with no fee.

After six to twelve months as an authorized user, you’ll often have enough credit history to apply for your own Amex card under your name.

📌 Did You Know: An authorized user on a 10-year-old Amex account can sometimes inherit that full account age on their own credit report. That single move can push your average account age from zero to a decade overnight.

How to Build Your Credit Score to Qualify for Amex

If you’re starting from scratch, you’ll need a real plan to reach the 670+ score range that opens up Amex approvals. Here’s a practical 6 to 18 month roadmap that works for most beginners.

Month 1 to 3: Open a secured credit card or a student credit card. Secured cards from issuers like Discover or Capital One require a small refundable deposit, usually $200 to $500. Student cards work if you’re enrolled in college. Either path gets your credit file started.

Month 1 to 6: Use the card for one or two small purchases each month. Think groceries, gas, or a streaming service. Pay the full balance before the statement closes. Never carry a balance month to month. Carrying balances builds interest charges, not credit.

Month 3 to 12: Keep your credit utilization below 30% of your limit at all times. Lower is better. If your limit is $500, try to keep balances under $150 at any moment. Many credit experts now suggest keeping utilization under 10% for the fastest score growth.

Month 6 to 12: Check your FICO score monthly. Free tools like Experian or MyCredit Guide let you watch your score climb. Once you cross 670, you’re in entry-level Amex territory.

Month 12 to 18: Use the Apply with Confidence tool on the Blue Cash Everyday or another beginner Amex card. If you get a green light, move forward. If not, give it another three months and try again.

Consider Jasmine, a 22-year-old graphic design student. She started with a $300 secured card from her credit union. After 14 months of using it for her $42 monthly subscription bill and paying in full, her FICO score hit 698. She used Apply with Confidence on the Blue Cash Everyday and was approved that same day.

What Happens if American Express Denies Your Application

A denial isn’t the end of the road, but it does need a careful response. If Amex turns down your application, the first thing that happens is a written notice. By federal law, Amex must send you an adverse action letter within 60 days. This letter spells out the exact reasons for the denial, often things like a thin credit file, low score, or too many recent inquiries.

Read this letter carefully. The reasons listed are your roadmap for fixing the issue.

Your next move is the Amex reconsideration line. You can call 1-800-567-1083 within roughly 30 days of the denial to ask for a second look. A real person reviews your case and may overturn the decision if you can explain your situation. Common winning arguments include offering to lower the credit limit on another Amex card, updating your income, or clarifying a temporary debt.

If reconsideration doesn’t work, do not apply again right away. Wait at least 90 days before reapplying. Reapplying too soon triggers more hard inquiries, which makes the next denial more likely.

Use the waiting period wisely. Pay down balances, clean up any late payments, and let your credit file age. Then apply with stronger numbers behind you.

Amex Application Rules First-Time Applicants Need to Know

Amex has a few unique rules that catch many first-time applicants off guard. Knowing them ahead of time saves real money and credit damage.

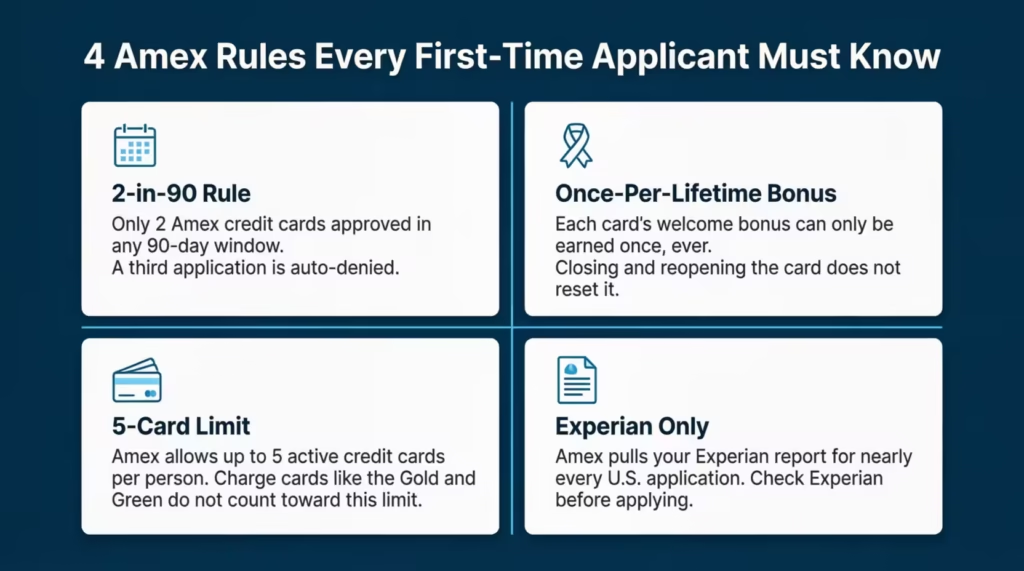

The 2-in-90 Rule. You can only be approved for two Amex credit cards within any 90-day window. If you apply for a third, you’ll be auto-denied, no matter how strong your score is. For a first-time applicant, this rarely matters, but it’s worth knowing if you plan to add an Amex business card soon after.

The Once-Per-Lifetime Welcome Bonus Rule. This is the big one. Amex gives you the welcome bonus on each card only once in your entire life. If you earn a bonus on the Blue Cash Everyday today and close the card next year, you can never earn that same card’s bonus again. Even if you reopen it ten years later. As Bankrate notes, Amex enforces this rule strictly and tracks bonuses by your name and Social Security number.

The 5-Credit-Card Limit. Amex usually allows a maximum of five active credit cards per person at one time. Charge cards like the Green and Gold don’t count against this number, but credit cards like the Blue Cash Everyday do.

Experian Credit Pulls. Amex pulls your Experian report for almost every U.S. application. So before you apply, make sure your Experian file is clean and up to date. Other bureaus matter less for Amex specifically.

For a first-time applicant, the practical takeaway is simple. Pick your first Amex card carefully. The welcome bonus rule means the card you pick today affects bonus eligibility for life. Choose a card you actually want long-term, not just the one with the flashiest sign-up offer.

Frequently Asked Questions (FAQs)

Can I get an Amex as my first credit card?

Yes, but only if you already have a FICO score of 670 or higher and at least a few months of credit history. Amex offers no secured or starter cards, so a completely blank credit file will almost always result in a denial.

Should I get an Amex as my first credit card?

Only if you already have a 670+ FICO score and six or more months of clean credit activity. If you are starting from zero, build your credit with a secured card for 6 to 12 months first, then apply for an entry-level Amex like the Blue Cash Everyday.

What Amex should I get as my first ever credit card?

The Blue Cash Everyday Card is the strongest starting point because it has a $0 annual fee and requires a FICO score of roughly 670. The Delta SkyMiles Blue is another $0 fee option if you occasionally fly Delta.

Is Amex beginner friendly?

Less so than other issuers. Amex does not offer secured cards in the U.S., which means you need an existing credit file and a FICO score of at least 670 before any application has a realistic chance of approval.

Is Amex the hardest credit card to get?

Amex is harder to break into than most issuers because it offers no secured cards and requires a minimum FICO score around 670 even for its entry-level products. Premium cards like the Platinum typically require 720 or higher plus a multi-year credit history.

What salary do I need for an Amex card?

Amex does not publish a minimum salary requirement, but income is a real factor in approval decisions. Part-time income and stipends count as long as you report them honestly, and keeping your debt-to-income ratio under 36% strengthens your application regardless of the exact dollar amount.

Is Amex Platinum for wealthy people?

It is designed for high-income, heavy travelers. Most approved applicants carry FICO scores of 720 or higher, have multi-year credit histories, and earn enough income to justify a $695 annual fee through perks like lounge access, hotel credits, and travel benefits.

What happens if Amex denies my application?

Amex must mail you an adverse action letter within 60 days explaining the exact denial reasons. You can then call the Amex reconsideration line at 1-800-567-1083 within about 30 days to request a manual review and potentially reverse the decision.

Can I become an Amex authorized user with no credit history?

Yes. A parent, partner, or family member can add you to their Amex account as an authorized user, and Amex reports that activity to the major credit bureaus once you are 18 or older. After 6 to 12 months, that history can be enough to qualify for your own Amex card.

Wrapping Up

Getting an Amex card as your first credit card is possible, but only if you approach it strategically. Most beginners need a FICO score of 670 or higher, six months of clean history, and the right entry-level card like the Blue Cash Everyday.

Tools like Apply with Confidence let you test approval risk-free, while authorized user status and a steady credit-building plan close any remaining gaps. For most readers, the most effective approach is to build six to twelve months of credit first, then apply with confidence.

If you know a student or young professional dreaming about their first Amex, share this guide. It could save them a denial and a hit to their score.