If you’re eyeing an American Express card, you’ve probably asked yourself: Do I have the right credit score to get approved? It’s a fair question. Nobody wants to apply, take a hard inquiry hit, and then get denied. Many people assume any decent score will do, but Amex has specific thresholds that vary by card type.

Most Amex cards require at least a 670 FICO score, but premium cards like the Gold and Platinum have a higher bar.

In this guide, we break down the exact score ranges by card tier, the other factors Amex checks, and how to know your odds before you apply.

Key Takeaways

This guide explains what credit score you need for an American Express card, covering score thresholds by card tier, the four factors Amex evaluates beyond your score, how to check approval odds without a hard inquiry, and steps to take if your application is denied.

Core Facts:

- Most Amex cards require a minimum 670 FICO score; entry-level cards may approve mid-600s, while premium cards like the Gold and Platinum require 700 to 740 or higher.

- Amex evaluates four factors beyond your credit score: income and debt-to-income ratio (preferred below 30%), credit history length, recent hard inquiries, and existing Amex account relationships.

- Amex primarily pulls your Experian credit report when reviewing applications, making Experian the file to monitor and clean up before applying.

- The Apply with Confidence feature lets applicants see approval decisions via soft pull before a hard inquiry is performed, eliminating score risk on a denied application.

- Amex enforces internal rules that can cause denial regardless of creditworthiness: no more than one card approval within five days, no more than two approvals within 90 days, and a five-card credit card limit per cardholder.

- Denied applicants can call the Amex reconsideration line (877-399-3083 for new applicants) to correct income errors, address credit report inaccuracies, or reallocate an existing credit limit to the new card.

Best for:

- First-time Amex applicants with scores in the 650 to 720 range who need to know which card tier matches their current credit profile before applying.

- Applicants targeting the Amex Gold or Platinum Card who want to understand the full approval criteria beyond the credit score requirement.

- Anyone who has been denied an Amex card and wants a clear explanation of reconsideration options and a timeline for reapplying.

The Credit Score Amex Generally Requires

The number most commonly tied to Amex approval is 670. That’s the FICO threshold where “good credit” begins, and it’s also the floor most American Express cards use when evaluating new applicants.

FICO defines good credit as any score between 670 and 739. Very good credit runs from 740 to 799. Excellent credit is 800 and above. Amex generally expects applicants to land in at least the good range before they’ll approve a new account.

What makes Amex different from issuers like Discover or Capital One is that it doesn’t offer cards for people with fair credit or those rebuilding from past problems. There’s no subprime Amex card. There’s no secured Amex option for U.S. residents. If your score sits below 670, your approval odds are low regardless of which card you’re looking at.

That said, the 670 floor is a starting point, not a finish line. Entry-level Amex cards may approve scores in the mid-600s in some cases. Premium cards like the Platinum push that floor up to 700 or higher.

Why Amex Doesn’t Publish an Official Minimum

American Express doesn’t post a specific minimum credit score anywhere in its terms or application materials. This isn’t unusual. Most major card issuers operate the same way.

The reason is simple: Amex doesn’t approve or deny applications based on score alone. It looks at the full picture. Your income, your debt load, how long your credit history runs, and whether you’re already an Amex customer all factor into the decision. A 680 score with strong income and a clean payment history can outperform a 720 score attached to a thin file and high balances.

The 670 figure comes from aggregated approval data reported by cardholders, not from anything Amex officially states. It’s the best available benchmark, but it’s not a guarantee. A perfect 850 score won’t guarantee approval if your income is too low or your debt-to-income ratio is too high. Likewise, a score a few points under 670 isn’t an automatic denial if everything else on your application looks solid.

This is important to understand before you apply. The score matters a lot. But it’s one input in a broader evaluation.

Amex Credit Score Requirements by Card Tier

Amex offers cards across a wide range, from no-annual-fee cash back products to premium travel cards with annual fees over $695. The credit score threshold isn’t the same across all of them. Higher-tier cards expect higher scores, and the gap between tiers is real enough to affect which card makes sense for you to apply for right now.

The clearest way to think about this is in three tiers: entry-level, mid-tier, and premium. Each tier covers specific cards, and each has a realistic score range where approvals tend to happen.

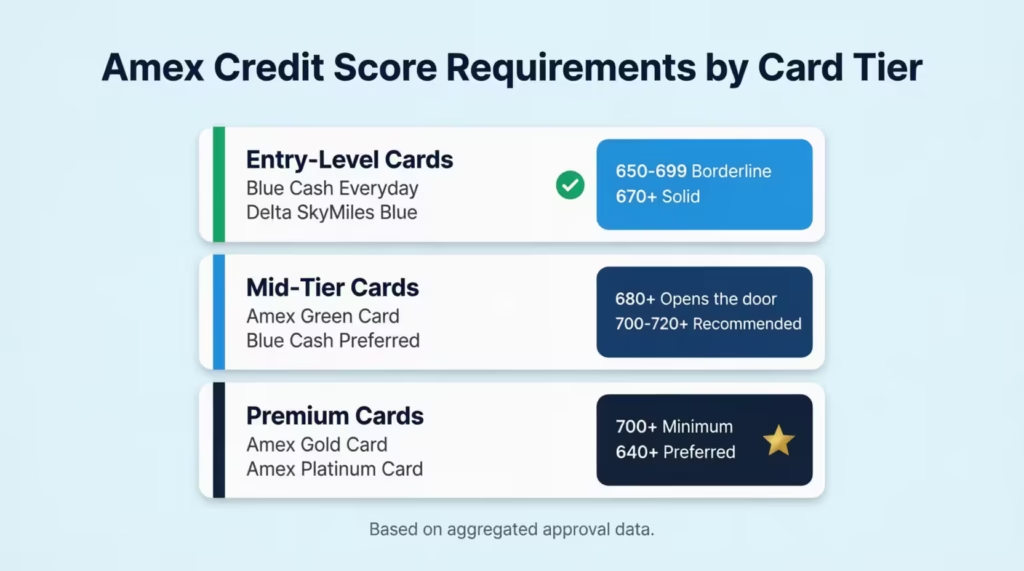

Entry-Level Amex Cards (Score Range: 650-699 Borderline, 670+ Solid)

The easiest Amex cards to get approved for are the ones with no annual fee or a low annual fee and a straightforward rewards structure. The two most commonly referenced in this category are the Blue Cash Everyday Card from American Express and the Delta SkyMiles Blue American Express Card.

Both cards require good credit, but they’re where Amex draws the line between “you have a real shot” and “you need more time.” Applicants with scores in the high 600s are in reasonable shape. There are reported approvals in the mid-600s, though those tend to come from applicants with strong income or longer credit histories that compensate for the lower score.

If your score is between 650 and 669, these entry-level cards are the only Amex products worth applying for. Don’t apply for the Gold or Platinum at this range. Start with the entry level. Use the card wisely, and your score will improve as you build a payment history with Amex.

One strategic reason to start here: existing Amex customers get a meaningful edge when applying for additional cards later. Getting your first Amex account open, even at the entry level, sets you up for easier approvals on premium products down the road.

Mid-Tier Amex Cards (Score Range: 680-720+ Recommended)

The American Express Green Card and the Blue Cash Preferred Card from American Express fall into the middle tier. These cards have annual fees and offer better rewards than basic options. They expect applicants to have a stronger credit profile.

A score of 680 is roughly where the door opens for these cards. But “opening the door” and “walking through comfortably” are different things. At 680, your approval odds depend heavily on the other factors in your application. If your income is high, your balances are low, and your history runs at least a few years, 680 can work. If you have a thin file or high balances, 700 or above gives you meaningfully better odds.

Mid-tier Amex cards suit applicants who have had one or two cards for a few years. They should pay on time and keep their usage low. If that’s where you are, and your score lands between 680 and 720, this tier is worth targeting.

Premium Amex Cards (Score Range: 700+ Minimum, 740+ Preferred)

The American Express Gold Card and the Platinum Card from American Express are the products most people are searching for when they research Amex credit score requirements. These are also the cards with the strictest approval standards.

For the Gold Card, a score of 680 to 700 is where applications start to succeed. The more honest benchmark is 720 or higher, which is where approval odds improve substantially. Anecdotal approvals are often in the high 600s. However, these cases usually involve higher incomes or existing Amex relationships.

For the Platinum Card, the floor moves up a notch. Most approved applicants have scores of 700 or above, and the cluster of successful applications sits at 720 to 740 and higher. The Platinum comes with a $695 annual fee and a benefits package designed around frequent travelers with significant incomes. Amex’s underwriting reflects that expectation.

⚠️ Mistake to Avoid: Applying for the Amex Platinum or Gold when your score is in the mid-600s. Even if your score is close to the floor, a thin file or high debt will push the outcome toward denial. That hard inquiry stays on your report for two years. Target the right tier for your current profile, not the card you eventually want.

At the premium tier, your credit score matters, but it shares the stage equally with income and credit history length. A 740 score with a thin, two-year file is a weaker application than a 710 score with six years of clean payment history and a $90,000 income. More on those factors in the next section.

Other Factors Amex Evaluates Beyond Your Credit Score

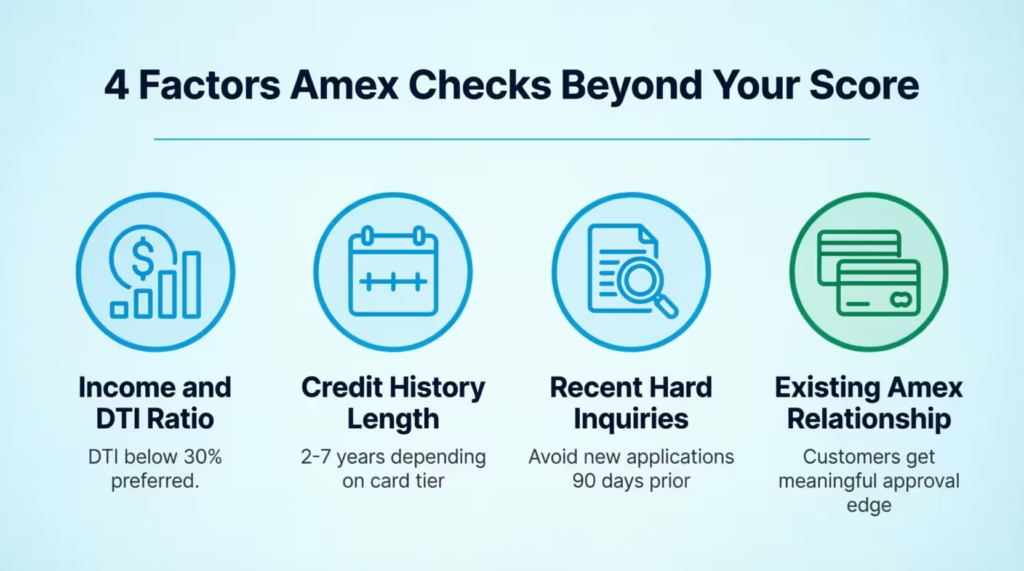

Many people are surprised when Amex denies them despite a qualifying credit score. The reason is almost always one of four things: income and debt load, credit history length, too many recent hard inquiries, or a lack of an existing Amex relationship. Understanding each of these gives you a complete picture of how the approval decision actually gets made.

Income and Debt-to-Income Ratio

Amex doesn’t publish a specific income requirement for most of its cards. But income is a significant factor, and it carries more weight on premium products with high annual fees.

The key metric isn’t your raw income. It’s how your income compares to your existing debt obligations. This is called the debt-to-income ratio (DTI), and Amex prefers applicants with a DTI in the low 30s or below. To find yours, add your monthly debt payments. This includes rent or mortgage, car payment, minimum credit card payments, student loans, and any other regular bills. Then, divide that total by your gross monthly income. Multiply by 100 to get your percentage.

For example, if your monthly debts total $1,200 and your gross monthly income is $5,000, your DTI is 24%. That’s a comfortable range for most Amex applications. If your monthly debts push your DTI above 40%, that’s a flag, even if your credit score is solid.

For the Amex Platinum specifically, reported approvals tend to cluster among applicants earning $50,000 or more annually. That’s not a published rule, but it reflects the card’s design. A $695 annual fee paired with a benefits package built around frequent spending and travel assumes a certain income tier.

One thing worth knowing: when Amex asks for income, it allows you to include all eligible income. That includes wages, salaries, self-employment income, rental income, investment income, and in some cases, household income if you have access to it. Don’t underreport.

Length of Credit History

A credit score of 720 built over 18 months tells a different story than a 720 score built over 7 years. Amex reads both scores, but it weighs them very differently.

A short credit history means Amex has limited data to evaluate. There’s less proof of how you act under financial stress. It’s unclear how you handle multiple accounts over time or if your good behaviour stays consistent. Amex calls this a “thin file,” and it increases the perceived risk of approving a new card, especially a premium one.

For entry-level cards, a credit history of one to two years can be enough if the score is solid. For mid-tier cards, two to three years is a reasonable baseline. For premium cards like the Gold and Platinum, applicants with thin files, even those with good scores, face a harder path. A longer, cleaner history is one of the strongest signals you can send to Amex’s underwriting system.

This is also why starting with an entry-level Amex card, if you’re earlier in your credit journey, is more than just a fallback option. It’s a strategic move. Your Amex account becomes part of your history, and Amex can evaluate your behavior directly when you apply for a premium card later.

Recent Hard Inquiries

Every time you apply for a credit product, the lender performs a hard inquiry on your credit report. Hard inquiries stay on your report for two years. Each one causes a small, temporary dip in your score, typically 5 to 10 points, and signals to lenders that you’re actively seeking new credit.

A handful of hard inquiries over two or three years isn’t a problem. But multiple inquiries in a short window, say three or four in 90 days, raise a flag. It looks like you’re in a hurry for credit, which is a risk signal.

Before applying for any Amex card, especially a premium one, avoid new credit applications for at least 90 days. That includes car loans, mortgage pre-approvals, and other credit cards. Give your profile time to look stable, not frantic.

This factor is separate from Amex’s own application timing rules (covered later). We’re discussing the inquiries from other lenders on your report, not how Amex handles many applications internally.

Your Existing Relationship with Amex

If you already have an Amex card in good standing, your next application starts from a stronger position. Amex can see your actual payment behavior. It knows your spending patterns. It has direct evidence of how you manage credit with them.

Existing customers often get approved with slightly lower scores than new applicants. Their income and history requirements can also be easier to meet since Amex has a track record to reference. This isn’t a guarantee, but it’s a consistent pattern in approval data.

This dynamic is part of why the “start with an entry-level card first” strategy works. You’re not just building your credit score. You’re building a relationship with the specific issuer whose premium cards you want.

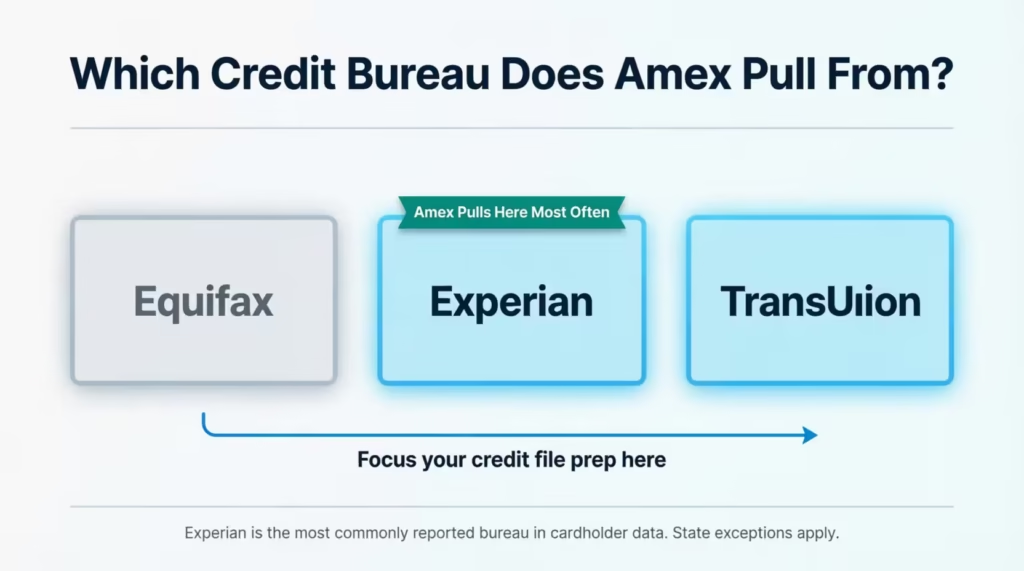

Which Credit Bureau Does Amex Pull From?

When Amex reviews your application, it pulls your credit report from one of the three major bureaus: Experian, Equifax, or TransUnion. In most cases, Amex pulls primarily from Experian.

This isn’t universal. In certain states, Amex may pull from Equifax or TransUnion instead. But Experian is the most commonly reported bureau in cardholder data, which means it’s the file you should focus on when preparing to apply.

Why does this matter? Your credit score isn’t always identical across all three bureaus. If your Experian score is 708 and your TransUnion score is 694, and Amex pulls from Experian, that 14-point difference could be meaningful. You want to know what your Experian score looks like specifically, not just your average score or whichever one a free app happens to show you.

Before applying, pull your free Experian credit report at AnnualCreditReport.com. Look for any inaccuracies: incorrect late payments, accounts you didn’t open, or debts that have aged past the seven-year reporting window. Dispute any errors directly with Experian before you apply. Cleaning up your Experian file can improve the score Amex actually evaluates, which is the only one that matters at the moment of application.

📌 Did You Know: Amex offers its own free credit score monitoring tool called MyCredit Guide. It shows your TransUnion score, not Experian, so it’s useful for tracking trends, but it won’t show you the exact score Amex is most likely to pull when you apply.

How to Check Your Amex Approval Odds Without a Hard Inquiry

One of the biggest concerns people have before applying is the hard inquiry. Applying for a credit card triggers a hard pull on your credit report, which temporarily lowers your score. If you get denied, you’ve taken the score hit for nothing.

Amex has a way around this problem. It’s called Apply with Confidence.

Apply with Confidence lets you submit a full application and see whether you’re approved before Amex performs a hard inquiry. The initial review uses a soft pull, which has no impact on your credit score. If you’re approved and choose to accept the card, Amex then performs the hard inquiry. If you’re not approved, your score is untouched.

This is a meaningful feature. It lets you find out where you stand without any downside risk to your credit. To use it, simply go through the standard application process on Amex’s website. The soft-pull review happens automatically. You don’t need to take any extra steps to trigger it.

Before using Apply with Confidence, there are two other tools worth knowing:

The CardMatch tool (available at NerdWallet, Bankrate, and other finance sites) uses a soft pull to show you which Amex cards you’re pre-matched with based on your credit profile. Pre-match results mean Amex has already signaled that you meet preliminary criteria for those cards. It’s not a guarantee of approval, but it’s a strong indicator.

Amex MyCredit Guide is Amex’s own free credit monitoring tool. You don’t need to be a cardholder to use it. It shows your TransUnion score and helps you track score trends over time. Use it to watch your general trajectory, but remember that it shows TransUnion data, not Experian.

The key distinction to understand about all three tools is that pre-qualification is not approval. A positive pre-match or soft-pull result means you’ve cleared the first screening. The final decision still depends on the full review, including income verification and a complete hard-pull report. But a strong pre-qualification result is a solid signal that your application is worth submitting.

Amex Application Rules That Can Cause Denial Regardless of Your Score

Even applicants with excellent credit and high income can get denied if they run into Amex’s internal application frequency rules. These rules are separate from credit score requirements. They’re policies that govern how often Amex will approve you for new cards, regardless of your creditworthiness.

The 1-in-5 Rule

Amex generally won’t approve more than one credit card application within a five-day window. If you apply for two Amex credit cards on the same day (or within five days), the second application is likely to be denied automatically. This rule applies to credit cards. Charge cards, like the Platinum and Gold, which are technically “no preset spending limit” products, may be handled differently under this rule in some cases.

The 2-in-90 Rule

Within any 90 days, Amex will typically approve no more than two credit cards. Even if you space your applications more than five days apart, a third approval inside that 90-day window is unlikely. Once you’ve been approved for two cards in 90 days, wait until the window resets before applying again.

The Five Credit Card Limits

Amex limits cardholders to five credit cards at one time. Personal and business credit cards both count toward this cap. If you’re already holding five Amex credit cards and you apply for a sixth, the application will be denied. To open a new one, you’d need to close an existing account first.

Note that “no preset spending limit” products (the Platinum, Gold, Green, and charge cards) are counted separately and don’t fall under the five-card cap.

The Once-Per-Lifetime Welcome Bonus Restriction

This isn’t a denial trigger, but it affects whether applying again makes sense. Amex restricts welcome bonuses to one per card, per lifetime. If you’ve held the Amex Gold before and earned the welcome bonus, you won’t be eligible to earn it again on a new Gold application. Amex often shows a pop-up notification during the application process if you’re ineligible for the bonus before you submit.

💡 Pro Tip: If you plan to apply for multiple Amex cards in the same period, space them at least six days apart and stay under two approvals per 90-day window. Timing your applications correctly can mean the difference between two approvals and an automatic denial on the second card.

How to Improve Your Credit Score Before Applying for Amex

If your score isn’t where it needs to be yet, the good news is that some improvements happen faster than others. The steps below are organized by what you can do in the next 30 days versus what requires more time.

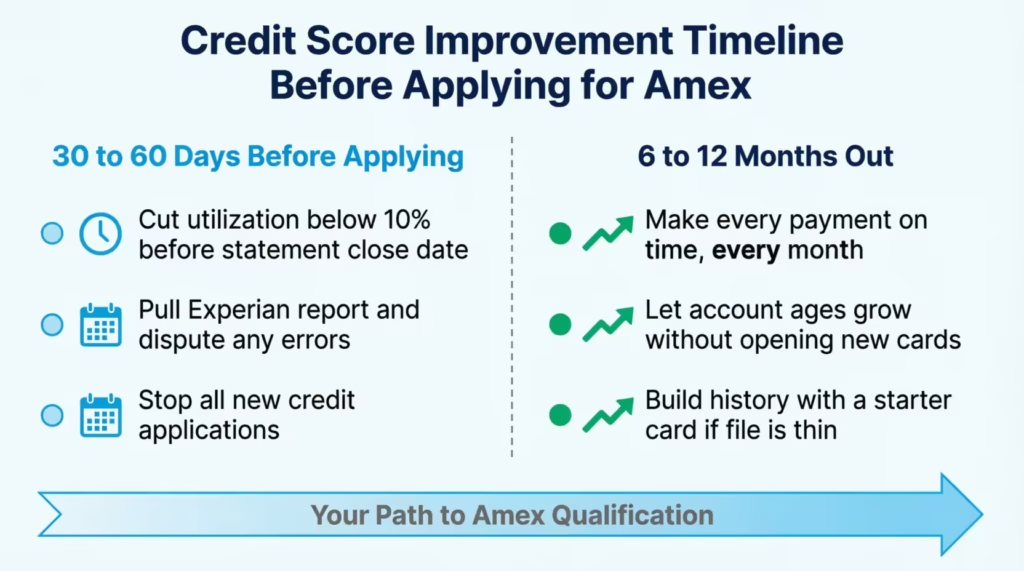

In the 30 to 60 Days Before You Apply

Reduce your credit utilization below 10%

Utilization is the percentage of your available revolving credit you’re currently using. It’s one of the heaviest-weighted inputs in your FICO score. Many people know to stay below 30%, but for the biggest score impact, especially before a major application, getting it below 10% is the target. Pay down balances before your statement closing date, not just before your payment due date. The balance that posts to the bureaus is the statement balance, not your current balance.

Pull your Experian report and dispute any errors.

Go to AnnualCreditReport.com and request your Experian report specifically. Look for late payments marked incorrectly, accounts you didn’t open, balances that don’t match, or accounts that should have aged off (most negative items disappear after seven years). File disputes directly with Experian. Corrected errors can produce score improvements within 30 to 45 days.

Stop applying for other credit.

Each new application generates a hard inquiry. Avoid applying for car loans, mortgages, store cards, or other credit cards in the 90 days before you apply for Amex. Every hard inquiry is a signal that you’re actively seeking credit, which increases perceived risk.

Use Amex’s pre-qualification tools.

Before submitting a full application, run through Apply with Confidence or CardMatch to get a soft-pull read on your odds. If those tools show you’re not pre-matched for the card you’re targeting, that’s useful information. It means either your score or another factor isn’t quite there yet.

If You Need More Time (6 to 12 Months)

Make on-time payments your absolute priority.

Payment history accounts for 35% of your FICO score. A single missed payment can knock 50 to 100 points off your score and stay on your report for seven years. Set up autopay for at least the minimum on every account so you never miss a due date accidentally.

Let your account ages grow.

The length of your credit history is partly determined by the age of your oldest account and partly by the average age of all your accounts. Opening new credit cards lowers your average account age temporarily. If you’re aiming for a premium Amex card, don’t open new accounts. Instead, let your current history develop.

Consider a starter card if your file is thin.

If your credit history is less than two years and your score is below 670, an entry-level Amex card, or even a different issuer’s card, can serve as a foundation. Use it for regular purchases, pay it off monthly, and give it 12 to 18 months. A thin file with clean payment behavior is a meaningfully stronger application than the same thin file without one.

The Experian focus matters here: you’re ultimately preparing the specific file Amex is most likely to pull. Boosting your score on TransUnion or Equifax helps your credit health. But in the weeks before applying for Amex, focus on Experian first.

What to Do If Amex Denies Your Application

A denial isn’t the end of the road. Amex is required by federal law to send you an adverse action notice explaining the reasons for the denial. Read it carefully. The reasons in that letter show what you need to fix. This could be your score, your utilization, your income, or too many recent inquiries.

Before anything else, check whether the denial reason points to something correctable right now or something that needs time to fix. If the letter says your score was too low, or your credit history is too short, those aren’t quick fixes. If it says your income couldn’t be verified or there’s an error on your credit report, you can address those issues right away through reconsideration.

How to Use the Amex Reconsideration Line

The Amex reconsideration line connects you with a representative who can manually review your application. It’s worth calling if your denial was triggered by a correctable issue.

Phone numbers:

- New applicants: 877-399-3083

- Existing Amex customers: 866-314-0237

Hours are Monday through Friday, 8 a.m. to midnight Eastern, and Saturday, 10 a.m. to 6:30 p.m. Eastern.

Before you call, have your application ID ready, your denial letter in front of you, and a clear sense of what you want to address. Amex reconsideration reps are primarily empowered to verify information, correct errors, and move credit limits around for existing customers. They’re not in a position to override a denial based on emotion or persistence alone.

Here’s what works on a reconsideration call:

- Income correction. If you entered your income incorrectly or left out eligible income sources, this is your chance to clarify.

- Credit report error. If the denial was triggered by a negative item you believe is inaccurate, reference it specifically and explain what you’re disputing.

- Credit limit reallocation. If you’re an existing Amex customer with another card, you can ask the rep to move a part of your existing credit limit to the new card. This is one of the most effective options available in a reconsideration call because it removes the risk of Amex extending new credit.

Approach the call matter-of-factly. State your purpose, reference the specific denial reason, and make your request directly. Politeness matters. Rambling doesn’t help.

When to Wait and Reapply Instead

If the denial reason takes time to fix, such as a low score, a thin file, or too many inquiries, the reconsideration call likely won’t change the outcome. Amex’s reps can’t override the underwriting system’s score-based decisions.

In that case, Amex asks applicants to wait at least 30 days before reapplying. But 30 days is a minimum, not a recommendation. If your score was the issue, 30 days is not enough time to meaningfully move it. Give yourself 90 to 180 days, implement the credit improvement steps from the previous section, and come back with a stronger application.

Also consider whether the same card is still the right target. If you were applying for the Amex Gold and your score sits at 670, the Blue Cash Everyday might be the better first step. Getting that approval and using it wisely for 12 months helps you a lot. Then, when you apply for Gold as an existing cardholder, you’re in a better spot than if you reapply for Gold at the same score two months later.

Frequently Asked Questions (FAQs)

Will Amex approve a 600 credit score?

A 600 credit score falls below the 670 floor that most Amex cards require, and Amex doesn’t offer any subprime or secured card options, so approval at 600 is very unlikely. Focusing on improving your score to at least 670 before applying gives you a realistic shot at an entry-level card like the Blue Cash Everyday.

Will Amex approve a 650 credit score?

A score of 650 is below Amex’s general 670 floor, though a small number of entry-level cards have approved applicants in the mid-600s when income and credit history are strong. At 650, your odds improve significantly if you bring your utilization below 10% and have at least two years of clean payment history.

Is Amex hard to get approved for?

Amex is stricter than many card issuers because it requires at least good credit (670 or higher) for every card it offers and has no products designed for fair credit or credit rebuilding. Beyond the score, Amex also evaluates your income, debt-to-income ratio, and credit history length, which means a qualifying score alone doesn’t guarantee approval.

What credit score do I need for the Amex Gold Card?

Most successful Amex Gold Card applications come from applicants with scores of 700 or higher, with 720 or above giving you substantially better odds. A score in the high 600s can occasionally result in approval, but it typically requires above-average income or an existing Amex account in good standing to compensate.

What is the easiest Amex card to get?

The easiest American Express cards to qualify for are generally the Blue Cash Everyday® Card and the Delta SkyMiles® Blue American Express Card. These entry-level cards often approve applicants with good credit, including some with credit scores in the mid-600s and otherwise strong applications.

How do you get a 700 credit score in 30 days?

The fastest lever available in 30 days is paying down revolving balances to below 10% of your credit limits before your statement closing date, since that’s the balance that posts to the bureaus. Disputing any inaccurate negative items on your Experian credit report can also produce score improvements within 30 to 45 days if errors are corrected.

What is the biggest killer of credit scores?

Missing a payment is the single most damaging thing you can do to your credit score, since payment history makes up 35% of your FICO score and a single missed payment can knock 50 to 100 points off your score instantly. Setting up autopay for at least the minimum payment on every account eliminates this risk entirely.

How fast can you build credit from a 500 to a 700?

Building your credit score from 500 to 700 typically takes 12 to 24 months of consistent positive credit habits. Making every payment on time, keeping credit utilization below 10%, and avoiding new negative marks can help you reach that goal faster.

Can you call Amex to reverse a denial?

Yes. You can contact American Express’s reconsideration line to request a review of your application, especially if the denial was caused by a correctable issue, such as an income error or inaccurate credit report information.

Bottom Line

Getting approved for an Amex card comes down to matching your current credit profile to the right card tier. Most cards require a 670 FICO score or above, while premium cards like the Gold and Platinum expect scores closer to 700 to 740 or higher. But the score is just one piece. Income, debt-to-income ratio, credit history length, and your existing relationship with Amex all shape the final decision.

For most applicants, the best way to start is by using Apply with Confidence. Check your odds first. Then, choose the card tier that matches your score. Finally, fix any issues on your Experian file before you apply. If you’re not quite ready, the improvement steps in this guide give you a clear path forward.

If this helped you figure out where you stand, share it with someone who’s also weighing an Amex application. Knowing the full picture before applying can save them from a hard inquiry denial they didn’t see coming.