You need cash today. Maybe rent is due in cash, a vendor only takes bills, or you’re stuck somewhere your card won’t swipe. You already know your Chase card has credit available, but pulling actual cash from it feels like a black box. The fees, the PIN, the limits, the interest all of it sits behind language most cardholders never bother to read. I’ve walked through this process with my own Chase card, and I know how stressful that “I need cash now” moment can be.

Here’s the short answer: you can get a cash advance from your Chase credit card at an ATM with your PIN, at any Chase branch with a teller, or by writing a convenience check Chase mailed you.

Below, you’ll get the exact steps for each method, current fees and APR figures, how to check your cash advance limit, and how this move can affect your credit score.

Key Takeaways

This guide explains how to get a cash advance from a Chase credit card, covering ATM, branch, and convenience check methods, current fees and APR, cash advance limits, and the impact on credit utilization.

Core Facts:

- Chase offers three cash advance methods: ATM withdrawal with a PIN, branch teller withdrawal with photo ID, or a mailed convenience check.

- Most Chase consumer cards charge a cash advance fee of either $10 or 5% of the amount, whichever is greater.

- Cash advance APR has no grace period and accrues interest from the transaction date, typically landing around 28% to 30% on most personal Chase cards.

- ATM cash advances are usually capped at $1,000 per day, while the cash access line is typically 20% to 30% of the total credit limit.

- A $1,000 cash advance held for 30 days costs about $74.66 total, while holding it for 90 days raises the total cost to about $123.97.

- Cash advances raise credit utilization since the balance counts against the credit limit, which can lower a credit score even without missed payments.

Best for:

- Cardholders who need cash quickly and have no cheaper short-term borrowing option available.

- People comparing ATM, branch, and convenience check methods to find the fastest or lowest-cost option for their situation.

- Cardholders evaluating how a cash advance will affect their credit utilization and overall card costs before borrowing.

Ways to Get a Cash Advance from a Chase Credit Card

A Chase cash advance lets you tap a portion of your credit line as actual cash. That portion is called your cash access line, and it sits inside your total credit limit, not on top of it.

Three doors lead to that money: an ATM withdrawal, a teller cash withdrawal at a Chase branch, or a convenience check you write to yourself or a payee. Every Chase consumer card, including Freedom, Sapphire, Ink, Southwest, and the Amazon co-brand, uses the same three channels. The difference is mostly in your card’s specific cash access line, fee minimum, and APR, not in the mechanics.

The reason this matters: each door has a different speed, a different cost ceiling, and a different ID or PIN requirement. Picking the wrong one can mean a wasted trip to the ATM, a declined transaction, or a higher fee than you needed to pay.

Which Method Fits Your Situation

Use this quick decision frame before you leave the house.

If you already have your cash advance PIN and need the money in the next hour, an ATM is fastest. You can use any Chase ATM or any Visa or Mastercard ATM that accepts cash advances. Daily ATM caps will still apply.

If you don’t have a PIN or you need more cash than the ATM will dispense in a day, go to a Chase branch. A teller can give you a cash advance with a valid government ID. The branch limit is usually higher than the ATM limit, often reaching your full cash access line.

If you don’t need the cash immediately and want to pay a person, landlord, or small vendor directly, a Chase convenience check is the cleanest option. You write the check like a personal check, the recipient deposits it, and the amount posts to your card as a cash advance.

💡 Pro Tip: If your need is under $500 and the recipient takes Zelle, ask if you can pay through your Chase checking account instead. A cash advance to fund a small payment often costs more in fees and interest than the convenience is worth.

Can You Get a Chase Cash Advance Online?

Chase does not offer a purely online cash advance. You can’t log into chase.com or the Chase Mobile app and click a button that sends cash from your credit card to your checking account. Federal Reserve and card network rules treat that as a cash advance, but Chase doesn’t currently process them through the app.

What you can do online:

- Check your available cash access line.

- Request or reset your cash advance PIN.

- Order convenience checks if your card is eligible.

Once those steps are done, the actual cash pickup still happens at an ATM, a branch, or by check.

How to Get a Cash Advance from a Chase Sapphire Credit Card

Sapphire Preferred and Sapphire Reserve both support cash advances. The process is identical to other Chase consumer cards, but two details are worth flagging.

First, the cash advance fee on most Sapphire cards is either $10 or 5% of the amount, whichever is greater, per the current Chase cardmember agreement. Second, Sapphire cards do not earn Ultimate Rewards points on cash advances, so don’t expect any points on a $1,000 withdrawal.

Steps:

- Log in to the Chase Mobile app or chase.com and confirm your cash access line.

- Make sure your cash advance PIN is set. Request one in the app if it isn’t.

- Insert your Sapphire card at a Chase ATM, enter your PIN, choose Cash Advance, enter the amount, and accept the fee disclosure on screen.

- Or, walk into any Chase branch with your card and a government ID and ask the teller for a cash advance.

How to Get a Cash Advance from a Chase Freedom Credit Card

Freedom, Freedom Unlimited, and Freedom Flex all work the same way. The cash advance fee is either $10 or 5% of the transaction, whichever is greater, and the cash access line is typically a small slice of your total credit limit, often around 20% to 30% depending on your account history.

Steps:

- Open the Chase Mobile app and tap your Freedom card.

- Tap Account Services, then Cash Advance PIN to set or retrieve your PIN if you haven’t already.

- At any Visa-network ATM, insert the card, enter the PIN, select Credit or Cash Advance, then choose the amount.

- Confirm the fee on the ATM screen before you accept.

How to Get a Cash Advance from a Chase Business Credit Card

Ink Business Cash, Ink Business Unlimited, and Ink Business Preferred all offer cash advances. Business cardholders manage them through the Chase for Business portal rather than the personal app.

The process is the same as a personal card: set up a PIN, then use an ATM, visit a branch, or use a convenience check tied to the business account. Most Ink cards have a fee structure of either $15 or 5% of the transaction, whichever is greater. This means the minimum fee is a bit higher than that of personal Chase cards.

A key point: cash advances on a business card show up on the business credit profile. They may also impact the personal credit of the authorized owner, based on how the account is set up. Confirm with your Chase business banker before pulling a large advance.

How to Get a Cash Advance from a Chase Southwest Credit Card

The Southwest Rapid Rewards Plus, Premier, and Priority cards all allow cash advances through the same three channels: ATM, branch, or convenience check. The fee is either $10 or 5% of the amount, whichever is greater.

The catch: you don’t earn Rapid Rewards points on cash advances. A $2,000 cash advance does not earn 2,000 points, even on the Priority card. Treat the Southwest cash advance like an emergency liquidity tool, not a points-earning move.

How to Get a Cash Advance from an Amazon Chase Credit Card

The Amazon Prime Visa and Amazon Visa, both issued by Chase, support cash advances using the same Chase process. You’ll need a PIN, you’ll pay the standard cash advance fee, and the APR will be higher than your purchase APR.

Like the Southwest cards, Amazon co-brand cards do not earn rewards on cash advances. The 5% back on Amazon.com purchases doesn’t apply when you pull cash from an ATM. Use this only if it’s your only Chase card, and you need cash quickly.

Getting a Cash Advance at a Chase ATM

A Chase ATM cash advance is the fastest path to actual cash, often done in under two minutes if your PIN is already set.

Step-by-step at a Chase ATM:

- Insert your Chase credit card into the ATM card slot. Do not use a Chase debit card by mistake, since that pulls from checking, not your credit line.

- Enter your cash advance PIN. If you don’t have one, the ATM will simply reject the transaction. There is no override at the machine itself.

- Select Credit Card or Cash Advance from the on-screen menu. The wording varies slightly by ATM.

- Enter the amount. Stay within your daily ATM withdrawal cap, which is typically $1,000 per day on most Chase consumer cards but can be lower on newer accounts.

- Review the fee disclosure. The screen will show the cash advance fee Chase will charge, and any ATM surcharge if you’re using a non-Chase machine. You must accept to continue.

- Take your cash, card, and receipt. The receipt is your proof of the transaction date, which matters because interest starts accruing immediately.

If you don’t have a Chase ATM nearby, any Visa-branded ATM in the U.S. or abroad will process the cash advance. Outside the Chase network, you usually pay an extra $2.50 to $5 in ATM surcharges. This is added to the Chase cash advance fee. If you’re overseas, there’s also a foreign transaction fee.

How Long It Takes for Funds to Be Available

The cash itself is immediate. The bills come out of the ATM the moment the transaction approves, just like a debit withdrawal.

The transaction posting is slightly different. The advance shows as pending on your account within a few minutes and usually posts as a finalized cash advance within one to two business days. Interest starts accruing from the transaction date, not the posting date, so the one-to-two-day posting gap does not give you a free interest window.

Setting Up or Retrieving Your Chase Credit Card PIN

A cash advance PIN is separate from any debit card PIN you have. Chase doesn’t automatically give you one with your credit card. So, many cardholders find out when they try to use an ATM and get rejected.

You have three ways to set or reset the PIN:

- Chase Mobile app or chase.com. Log in, open your card account, tap or click Account Services, then choose Cash Advance PIN. You can usually set a new PIN instantly or have it mailed within five to seven business days, depending on your card.

- By phone. Call Chase customer service at the number on the back of your card. Tell the agent you need to set or reset your cash advance PIN. They’ll verify your identity and either set the PIN on the call or send it by mail.

- At a branch. Walk into any Chase branch with your card and a government ID. A banker can initiate the PIN request, though most branches still mail the PIN rather than print it on the spot.

Mailed PINs typically arrive in five to seven business days, in a plain envelope. If you need cash sooner than that, skip the PIN route and use a branch teller cash advance, which doesn’t require a PIN, just a valid ID and your card.

⚠️ Mistake to Avoid: Don’t keep retrying ATM withdrawals if your PIN doesn’t work. After three failed attempts, Chase locks the PIN, and you’ll have to call to unlock it before any further attempt.

Getting a Cash Advance at a Chase Branch

The branch teller route is the right choice when you need more cash than an ATM will dispense in a day, or when you don’t have a working PIN.

What you need to bring:

- Your physical Chase credit card. A digital wallet image won’t work at the teller window.

- A valid government-issued photo ID, usually a driver’s license, state ID, or passport. The name must match the name on the card.

- A rough idea of your cash access line, so you don’t ask for more than the system will approve.

The teller swipes your card, runs the advance against your cash access line, and counts out the cash. The whole interaction takes about five minutes once you reach the window.

Branch advances often allow larger withdrawals than ATM caps, sometimes up to your full available cash access line. If you need $3,000 in one transaction, the teller can often process that in a single advance, where an ATM would force you to split it across multiple days.

You’ll still pay the same cash advance fee structure (either $10 or 5% of the amount, whichever is greater on most consumer cards) and the same cash advance APR. The branch doesn’t add a separate fee on top, which is a small advantage over non-Chase ATMs that charge their own surcharge.

Using a Chase Convenience Check

Chase periodically mails convenience checks to eligible cardholders. These look like personal checks, but they draw against your credit card’s cash access line instead of a checking account.

How to use one:

- Fill it out like a regular check. Write the date, the payee’s name, the amount in numbers and words, and sign it.

- Decide who to pay. You can write the check to yourself, then deposit it in your own checking account to get cash that way. Or write it directly to a landlord, contractor, or small vendor who doesn’t accept cards.

- Track the transaction. The check posts to your credit card account as a cash advance within a few business days of being deposited.

To check availability, log into chase.com or the app and look at your card’s offers section. If checks are available, you can either request a new batch by phone or download a printable version, depending on your account.

Writing the check to yourself is the most common use. It’s cleaner than an ATM because there’s no daily withdrawal cap and no machine fee, though the cash advance fee and APR still apply.

📌 Did You Know: Some Chase convenience check offers come with a promotional APR, sometimes 0% for a limited window. If you use one, read the offer terms closely. The promo rate often ends on a set date. After that, any balance will switch to the standard cash advance APR.

Checking Your Chase Cash Advance Limit

Your cash advance limit, also called your cash access line, is a slice of your total credit limit set aside for cash transactions. Per Chase’s own explainer, this line is a part of your overall credit limit, not an additional pool of money.

Two reliable places to check it:

- The Chase Mobile app or chase.com. Open your card, tap or click See details under your available credit, and the cash access line will appear as a separate figure. It updates in real time as you make purchases and payments.

- Your monthly statement. The cash advance limit and the amount of that limit currently available are printed near the top of your statement, alongside your purchase credit limit.

For most Chase consumer cards, the cash access line is roughly 20% to 30% of your total credit limit, though it varies by card type and your account history. If your total credit limit is $10,000, expect a cash access line somewhere between $2,000 and $3,000.

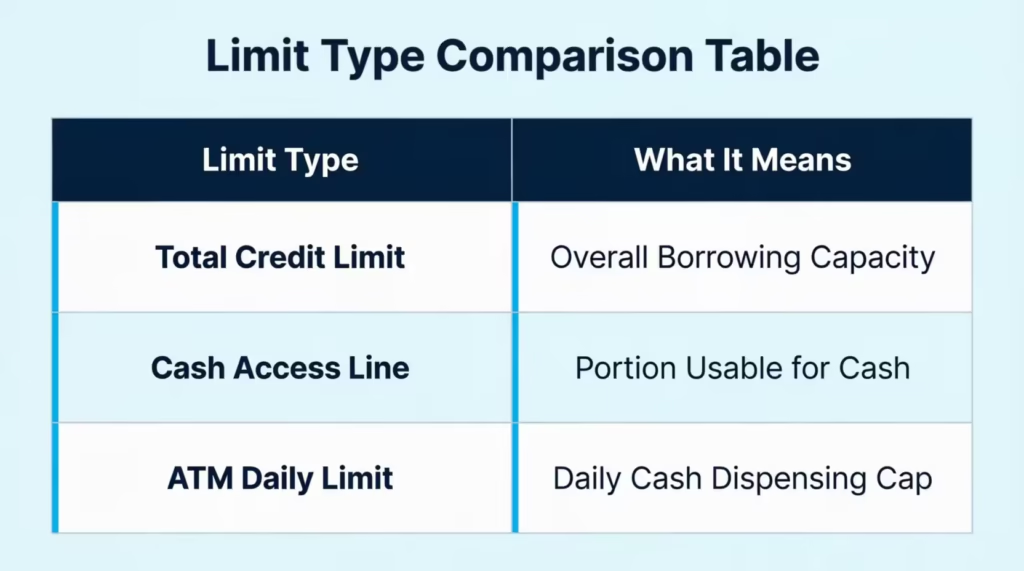

Cash Advance Limit vs. Credit Limit vs. ATM Daily Limit

These three numbers get blurred together, and the confusion can cost you a wasted trip to the ATM. Here’s the clean breakdown.

| Limit type | What it represents | Typical range on a Chase card |

|---|---|---|

| Total credit limit | Maximum balance you can carry on the card across all transaction types | Set when account opens, often $5,000 to $25,000+ |

| Cash access line (cash advance limit) | Portion of total credit limit you can use for cash advances | About 20% to 30% of total credit limit |

| ATM daily withdrawal limit | Maximum cash an ATM will dispense to you in a 24-hour period | Often $1,000 per day, set by Chase or by the ATM operator |

The total credit limit is your overall borrowing capacity. The cash access line is the cap on how much of that capacity can come out as cash. The ATM daily limit is a dispensing cap, not a borrowing cap, and it resets every 24 hours.

Example: your credit limit is $12,000, your cash access line is $3,000, and the ATM daily limit is $1,000. You can borrow up to $3,000 in cash advances total, but you’d need three days of ATM trips to pull it all out at a machine. A branch teller could give you the full $3,000 in one visit.

Chase Cash Advance Fees Explained

The cash advance fee is a one-time charge added the moment your advance posts. On most Chase consumer cards, the fee is either $10 or 5% of the cash advance amount, whichever is greater, based on the current sample cardmember agreement from Chase. On most Chase business cards, the minimum is $15 or 5%, whichever is greater.

Quick fee math:

- $100 advance: 5% would be $5, but the $10 minimum applies, so the fee is $10.

- $300 advance: 5% would be $15, which beats the $10 minimum, so the fee is $15.

- $1,000 advance: 5% is $50, charged on top of the $1,000 you receive.

Three other fees can stack on top of the Chase fee:

- Non-Chase ATM surcharge. If you use a non-Chase ATM, the ATM operator typically charges $2.50 to $5 for the use of the machine. Chase doesn’t refund this on credit card cash advances.

- Foreign transaction fee. Many Chase cards charge 3% on transactions made outside the U.S., including foreign-ATM cash advances. Some travel cards (Sapphire Preferred, Sapphire Reserve, most Ink Business cards) waive this. Check your specific card terms.

- Returned convenience check fee. If your account lacks enough credit to cover a check, Chase may charge a returned check fee. This means the payment will bounce too.

A 2024 Chase cardmember rates and fees table confirms the “either $10 or 5%, whichever is greater” structure on most personal cards in the current lineup.

Chase Cash Advance APR and How Interest Accrues

The cash advance APR on Chase cards is higher than the purchase APR, and there is no grace period. Interest starts accruing from the day of the transaction, not from your statement date.

Most current Chase consumer cards set the cash advance APR by adding 21.74% to the Prime Rate, per the latest Chase cardmember agreement rates table. With the Prime Rate at recent levels, that puts the cash advance APR in roughly the 28% to 30% range on most personal cards, well above typical purchase APRs.

Two specific points to internalize:

- No grace period. Chase confirms in its own cash advance APR explainer that cash advance APRs do not have a grace period. The Consumer Financial Protection Bureau’s Regulation Z commentary also confirms that a card issuer’s grace period does not apply to cash advances. This means a $1,000 cash advance starts costing you interest the same day, even if you pay your full statement balance on the due date.

- Variable rates. The cash advance APR moves with the Prime Rate. When the Federal Reserve raises rates, your cash advance APR goes up at the start of the next billing cycle.

Payments to your card go toward the highest-APR balance first for any amount you pay above the minimum. That’s a federal CARD Act rule. So if you pay extra, that extra wipes out the cash advance balance before it touches purchases.

Real Cost Example of a Chase Cash Advance

Let’s put numbers to it.

Scenario: Sarah, a freelance graphic designer, takes a $1,000 cash advance from her Chase Freedom Unlimited on June 1, with a cash advance APR of 29.99%. She pays it back in full on July 1, exactly 30 days later. She makes no other purchases on the card.

- Cash advance fee (5% of $1,000, since $50 beats the $10 minimum): $50

- Daily periodic rate: 29.99% ÷ 365 ≈ 0.0822% per day

- Daily interest on $1,000: $1,000 × 0.000822 ≈ $0.82 per day

- Interest over 30 days: $0.82 × 30 ≈ $24.66

- Total cost of the $1,000 cash advance: $50 + $24.66 = $74.66

If Sarah instead lets the balance ride for 90 days before paying it off:

- Interest over 90 days: $0.82 × 90 ≈ $73.97

- Total cost: $50 + $73.97 = $123.97

That’s nearly 12.4% of the borrowed amount in just three months. The lesson is simple: cash advances are short-term liquidity tools. The longer the balance sits, the worse the math gets.

How a Chase Cash Advance Affects Your Credit Score

A cash advance itself doesn’t show up on your credit report as a separate line item. What changes on your report is your credit utilization ratio, the percentage of your available credit you’re currently using. That ratio is a major input into your FICO and VantageScore credit scores.

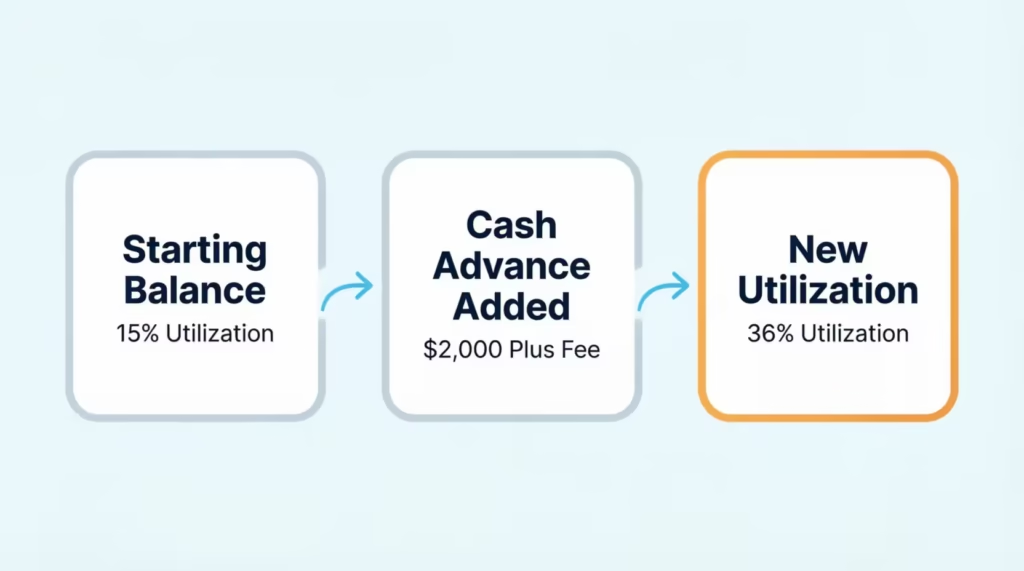

How it plays out:

- You have a $10,000 credit limit on your Chase Sapphire.

- Your balance before the advance is $1,500, so utilization is 15%.

- You take a $2,000 cash advance, plus a $100 fee, bringing your balance to $3,600.

- New utilization: 36%.

Credit scoring models generally prefer utilization under 30%, with under 10% being ideal for the highest scores. Jumping from 15% to 36% in one transaction can cause a noticeable score drop in your next reporting cycle. This is especially true if this is your only credit card.

Three specific impacts to expect:

- Higher utilization shows up within 30 days. Chase reports your balance to the credit bureaus around your statement date. Whatever your balance is on that date is what gets reported, even if you pay it down a few days later.

- The cash advance APR can compound the problem. Since interest accrues daily with no grace period, the balance grows even if you don’t spend more, pushing utilization higher over time.

- Lenders may view repeated cash advances as a warning sign. A single cash advance usually goes unnoticed in line-item details. However, if there are multiple advances, they can reveal patterns in account behavior. Lenders often look at this data when deciding on new credit.

The fix is straightforward: pay the cash advance balance down as quickly as possible. A payment made a few days before your statement closes can lower the balance. This helps protect your credit utilization ratio, as reported by Chase.

If you can’t pay it off in full, prioritize paying more than the minimum, since payment above the minimum gets applied to the highest-APR balance first under the CARD Act, which means your cash advance.

Frequently Asked Questions (FAQs)

How much is a cash advance fee for $1,000?

The fee is 5% of the amount, which equals $50 since that beats the $10 minimum. You’ll receive $1,000 in cash, but the advance actually costs $1,050 before any interest accrues.

Do cash advances hurt your credit?

A cash advance itself isn’t reported as a separate item, but it raises your credit utilization ratio since the balance counts against your limit. A jump from 15% to 36% utilization can cause a noticeable score drop in the next reporting cycle.

How much is 26.99% APR on $3,000?

At a 26.99% cash advance APR, the daily rate is about 0.074%, or roughly $2.22 per day on a $3,000 balance. Over 30 days, that’s about $66.60 in interest, separate from the upfront cash advance fee.

Is it a good idea to get a cash advance on a credit card?

It works best as a short-term liquidity tool you repay within 30 days, since interest starts accruing immediately with no grace period. At nearly 30% APR plus a 5% fee, letting the balance sit for 90 days can cost over 12% of the amount borrowed.

Can I withdraw $5,000 from my credit card?

It depends on your cash access line, which is typically only 20% to 30% of your total credit limit. A branch teller can usually process up to your full cash access line in one visit, while ATMs cap withdrawals around $1,000 per day.

Can I use a credit card cash advance at an ATM?

Yes, any Chase ATM or Visa/Mastercard-network ATM that accepts cash advances will work with your PIN. You’ll need a cash advance PIN set up first, since the ATM has no way to override a missing PIN.

How do I get my Chase cash advance PIN?

Set or retrieve it through the Chase Mobile app or chase.com under Account Services, by calling the number on the back of your card, or in person at a branch. Mailed PINs typically take five to seven business days to arrive.

What is Chase’s daily ATM withdrawal limit for cash advances?

Most Chase consumer cards cap ATM cash advances at $1,000 per day, though newer accounts can have a lower limit. This is a dispensing cap separate from your overall cash access line, and it resets every 24 hours.

Can a Chase cash advance hurt my score?

Yes, indirectly, since the advance raises your balance and credit utilization ratio, a major scoring factor. Paying the balance down before your statement closing date can limit the impact reported to the bureaus.

Do you pay interest on a cash advance if you pay it off early?

Yes, interest accrues daily from the transaction date with no grace period, so even paying it off in a few days means some interest is owed. Paying it off quickly still minimizes the total cost compared to letting the balance ride for weeks or months.

Wrapping Up

Pulling cash from a Chase credit card is straightforward once you know the three channels: ATM with a PIN, branch with an ID, or convenience check by mail. The mechanical steps are easy. The math is the hard part, with a 5% fee, a cash advance APR near 30%, no grace period, and a credit utilization hit that can ding your score.

To save money, treat a cash advance like a short-term loan. Pay it off within 30 days or before your next statement. Use it only when there are no cheaper options available.

If you know someone weighing a cash advance to cover an unexpected bill, share this guide with them. Five minutes of reading could save them a hundred dollars in fees and interest they didn’t see coming.