I’ve spent hours in Chase’s help center looking for a “block merchant” button on my credit card account. It’s really frustrating when a subscription keeps charging you after you’ve canceled it.

You’re not missing a hidden setting. Chase credit cards simply don’t offer a self-service merchant blocking toggle, so the real fix lives in a different set of tools like stop payments, disputes, and card locks.

In the sections below, I’ll walk you through each working method, when to use it, and how to make it stick.

Key Takeaways

This guide explains how to block a merchant on a Chase credit card, covering why no self-service blocking feature exists, plus the four real tools: merchant cancellation, stop payments, formal disputes, and card locks.

Core Facts:

- Chase credit cards do not offer a self-service “block merchant” feature; the ACH debit block some sources reference only applies to business checking accounts, not personal credit cards.

- A stop payment request tells Chase to reject a specific upcoming preauthorized charge before it posts, and requires calling 1-800-432-3117 with the merchant name, amount, and expected date.

- Disputes under the Fair Credit Billing Act must be filed within 60 days of the statement showing the charge; Chase must acknowledge within 30 days and resolve most cases within 90 days, up to 120 for complex fraud.

- Locking a Chase card blocks new purchases, cash advances, and balance transfers, but some preauthorized recurring charges can still go through even when locked.

- Chase offers Zero Liability Protection for unauthorized charges reported promptly, which is stronger than the FCBA’s standard $50 liability cap.

- Stopping a payment or winning a dispute does not cancel the underlying contract with a merchant, so unpaid contract obligations can still go to collections and appear on a credit report for up to seven years.

Best for:

- Cardholders dealing with a subscription or merchant that continues billing after cancellation.

- Anyone deciding between a stop payment, a formal dispute, and a card lock for a specific unwanted or fraudulent charge.

- Readers who want to understand FCBA dispute deadlines and how blocking a payment affects their credit score and Chase relationship.

Does Chase Have a “Blocked Merchants” Feature?

Short answer: NO. Chase credit cards do not include a self-service option to block a specific merchant from charging your card. If you sign into your Chase account online or open the Chase Mobile app, you won’t find an “Edit Blocked Merchants” or “Manage Blocked Merchants” toggle anywhere under Account Services or Card Settings for your credit card.

Some third-party blog posts describe a Chase “blocked merchants feature,” but that information is inaccurate. It seems to mix up Chase credit cards with a product from another bank or with Chase’s ACH debit block, which is a service for business checking accounts.

That business tool blocks unauthorized ACH withdrawals from a business deposit account. It does not stop credit card charges, and consumer cardholders can’t enable it on a personal card.

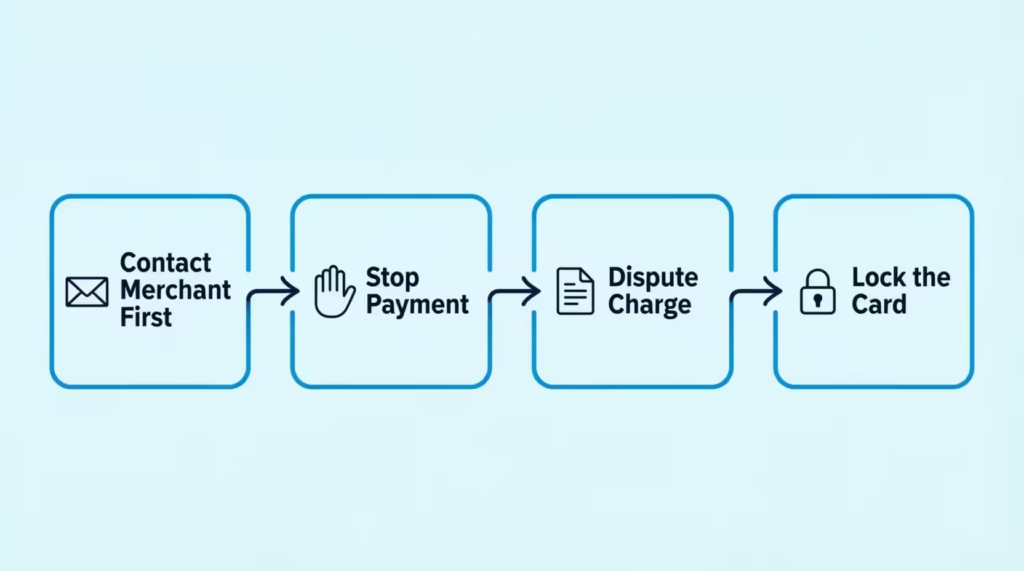

When someone asks how to block a company from charging their Chase card, the answer includes a few steps: cancel the charge with the merchant, request a stop payment, dispute the charge, or lock the card. Each method plays a different role, and the right one depends on why the charge keeps coming through.

What “Blocking a Merchant” Actually Means With a Credit Card

With a credit card, “blocking a merchant” is not a single button. It’s a workflow. In practice, it means one of four things:

- Telling the merchant to stop billing you (cancel the authorization at the source).

- Asking Chase to reject a specific upcoming charge (a stop payment request).

- Formally disputing a charge that already posted (a chargeback under the Fair Credit Billing Act).

- Preventing all card activity temporarily by locking or freezing the card.

Each step handles a different part of the problem. If you skip step one and jump to disputes, the merchant can often re-bill you legally. If you only lock the card, you also block groceries and gas. Knowing which tool matches your situation is the whole game, so the following sections break each one down.

Contact the Merchant First

Before Chase can help in most cases, the merchant has to be given a real chance to stop. This isn’t just a polite process; it’s how the chargeback system is designed. When you dispute a charge, Chase will often ask whether you already tried to cancel with the merchant.

If you skip this step, your dispute can get denied, and the merchant can legally keep billing because you still have an active authorization on file.

Start by finding the merchant’s cancellation channel. Look at the descriptor on your Chase statement, then search that name plus “cancel subscription” or “customer service.” Use the merchant’s official website or app.

Don’t trust phone numbers from random search results. Scam “cancellation lines” are real. Send your cancellation through a written channel whenever possible: email, in-app cancellation page, or web form. Written cancellation gives you a timestamp and a record.

Keep a short paper trail. Save the confirmation email, screenshot the cancellation page, and note the date, time, and the name of any agent you spoke with. That evidence is what makes a later stop payment or dispute stick. Chase support agents will ask for it, and so will the Consumer Financial Protection Bureau if you have to escalate.

If the merchant does not confirm the cancellation within a few business days, send a second written request. Say clearly that you are revoking authorization for any further charges to your Chase credit card ending in the last four digits of your card. That phrase, “revoking authorization,” is the legal language that matters if the case goes to a chargeback later.

How to Cancel a Subscription That Won’t Cancel

Some subscriptions are built to be sticky. Common traps include free trials that auto-renew, streaming services with hidden retention flows, and app store subscriptions. These subscriptions often exist within Apple or Google, not on the merchant’s site.

- App Store or Google Play subscriptions: Cancel inside your device, not on the merchant’s website. On iPhone, open Settings, tap your name, then Subscriptions. On Android, open the Google Play Store, tap your profile icon, then Payments & subscriptions.

- Gym and fitness memberships: Many require written notice by mail or a signed cancellation form. Read the original contract for the exact method and give yourself extra days for the notice window.

- Free trials converting to paid: Cancel at least 48 hours before the trial ends. Some merchants process renewal charges early.

- Merchants who won’t respond: After two written attempts with no reply, treat the authorization as revoked, save your evidence, and move to the stop payment or dispute steps below.

⚠️ Mistake to Avoid: Don’t just delete the app or close the browser tab. Uninstalling does not cancel billing. The subscription is stored on the merchant’s server, not on your phone. This means charges will keep hitting your card until you cancel it through the right way.

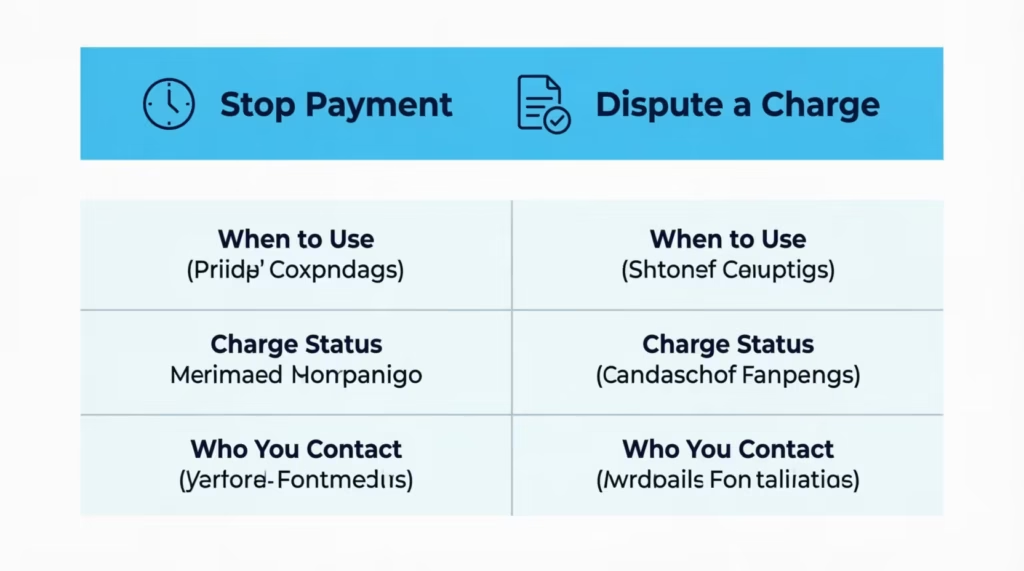

File a Stop Payment Request With Chase

A stop payment request tells Chase to reject a specific future charge before it posts. It’s different from a dispute, which deals with a charge that has already gone through. Think of it as pre-blocking a known upcoming payment rather than reversing one after the fact.

For credit cards, Chase generally handles stop-payment requests for preauthorized recurring charges.

To start one, call the Chase credit card customer service number on the back of your card, which for most cardholders is 1-800-432-3117. Explain that you canceled the service with the merchant, that the merchant is still scheduled to bill you, and that you want to stop the next preauthorized payment on your account.

Have three things ready before the call:

- The merchant’s exact billing name as it shows on your statement.

- The expected amount and approximate charge date.

- Proof you already asked the merchant to cancel (email, confirmation number, or screenshot).

A stop payment request has real limits. It usually applies only to specific upcoming or pending charges, not permanently to a merchant. If the merchant changes the amount, the descriptor, or the payment date by even a little, the block may not catch the new charge.

Chase may also charge a stop payment fee on some accounts, so ask about any fee before agreeing. If a preauthorized recurring subscription charge comes through unexpectedly, plan to file a formal dispute if it posts.

💡 Pro Tip: Request a written or in-app confirmation number for your stop payment. If the charge goes through, that confirmation is your quickest way to a full refund. It shows that Chase agreed to block the payment before it occurred.

Dispute the Charge With Chase

When a charge has already posted, disputing it is the strongest tool you have. This is where federal law does the heavy lifting. Under the Fair Credit Billing Act, you can dispute billing errors on a credit card, and the issuer has to investigate and respond within set deadlines.

You can file a Chase dispute for a range of reasons:

- Unauthorized charges you didn’t approve.

- Billing errors like duplicate charges or the wrong amount.

- Goods or services that were paid for but not delivered.

- Items that arrived damaged, defective, or not as described.

- Subscription charges that continued after you canceled in writing.

How to file a Chase dispute for an unauthorized charge online:

- Sign in at chase.com or open the Chase Mobile app.

- Scroll to Recent Activity and tap the charge you want to dispute.

- Choose “Dispute transaction” and follow the on-screen prompts. Chase will ask what happened and may request supporting documents.

- Submit and save the confirmation number.

You can also call Chase at 1-800-432-3117 to file by phone, or send a written dispute by mail. For written disputes, use Customer Service, PO Box 15299, Wilmington, DE 19850-5299, on its billing rights notice. Written disputes matter because they preserve your full FCBA billing rights in a way that a phone call alone doesn’t.

Timing rules to know:

- The FCBA gives you 60 days from the date Chase sent the first statement showing the disputed charge to file a written dispute, according to Chase’s own dispute guidance. Miss that window, and you lose the strongest legal protection.

- Chase must acknowledge your dispute in writing within 30 days of receiving it.

- Chase must fix most billing errors within 90 days, which is two billing cycles. For more complex cases, like fraud investigations, they can take up to 120 days. The FTC provides this information.

While the dispute is being investigated, Chase usually issues a provisional credit for the amount in question. That means the charge is temporarily removed from your balance so you don’t pay interest on it. If Chase sides with you, the credit becomes permanent. If Chase sides with the merchant, the amount goes back on your statement and you’ll have a chance to appeal.

What to Keep as Documentation

Your dispute is only as strong as your evidence. Chase’s investigators need enough proof to question the merchant’s records. The merchant will always get a chance to share their side. Save these items in one folder before you file:

- The dated cancellation email or in-app confirmation.

- Screenshots of the merchant’s cancellation page or subscription settings showing “canceled.”

- The original terms of service or receipt showing what you agreed to buy.

- Chat transcripts, call logs, or the name of any agent you spoke with, plus dates.

- Any tracking numbers, shipping confirmations, or delivery receipts if the dispute involves undelivered goods.

- Your written revocation of authorization if the charge is a recurring subscription.

Upload these directly through the Chase dispute form or fax them if you filed by phone. The more concrete the timeline, the more likely Chase resolves the case in your favor.

Report a Fraudulent or Unauthorized Charge

Fraud is a separate category from an unwanted charge, and it moves on a different track. If you see a charge you did not make, from a merchant you don’t recognize, on a card that hasn’t left your wallet, treat it as fraud and act fast.

Call the fraud number on the back of your Chase card the moment you spot it. You do not have to wait for the charge to post. Reporting a suspected fraudulent transaction immediately protects both your account and your dispute rights.

Chase offers Zero Liability Protection on its credit cards, which means cardholders are not held responsible for unauthorized charges when they are reported promptly. This is stronger than the baseline FCBA rule, which caps your liability at $50 for unauthorized credit card charges. Chase’s zero liability policy essentially waives even that $50.

When you report fraud, expect Chase to do three things:

- Freeze the card immediately to stop any further transactions.

- Reissue a new card with a new card number, expiration date, and security code, usually delivered within 3 to 7 business days.

- Open a fraud investigation with a provisional credit while the case is reviewed. Fraud cases can take up to 120 days to fully resolve.

Once you’re issued a new card, any auto-pay merchants tied to the old card number will fail on the next billing cycle. That’s what you want for a fraudster.

But you’ll need to update your card number for real subscriptions, like utilities, streaming services, and insurance. Card networks may automatically send the new number through account updater services. But don’t assume this will always happen. Log in to each real merchant and confirm the card on file.

Fraud protection is not the right tool for a subscription you signed up for and forgot to cancel. That’s a billing dispute, not fraud. Reporting a known merchant as fraudulent can backfire and delay the real fix.

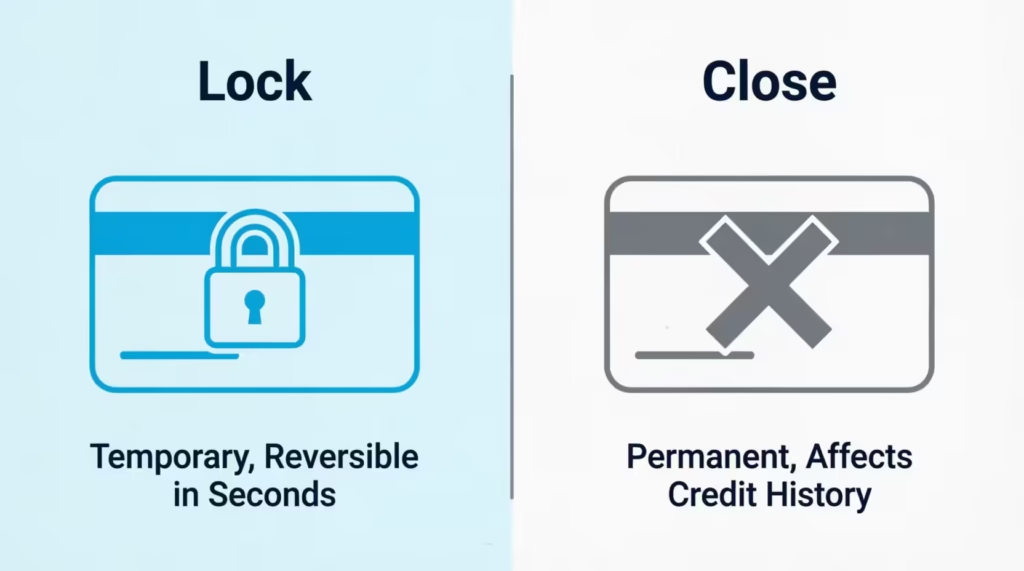

Freeze or Lock Your Chase Card

Locking your Chase card is the fastest emergency stop. When you lock the card, Chase blocks new purchases, cash advances, and balance transfers made with the card number, whether online, in-store, or over the phone. It’s a broad shutter, not a merchant-specific block.

To lock or unlock in the Chase Mobile app:

- Sign in and tap the credit card you want to lock.

- Swipe up to the Account services section and tap Lock & unlock card.

- Toggle the lock on. To unlock later, repeat the steps and toggle it off.

On desktop at chase.com, open the account, click the “more options” menu, and choose Lock & unlock card under Account services.

A card lock is best used as a short-term measure. Some situations where it makes sense:

- You misplaced your physical card and want to pause activity while you search.

- You spot a suspicious charge and need a few minutes to think before deciding fraud vs. dispute.

- You want to prevent your kids or an authorized user from purchasing a defined window.

What a lock will not do is stop a specific recurring subscription charge from a merchant you permitted to bill. Many card issuers, including Chase, let some recurring charges go through even when a card is locked.

This is because those charges are pre-authorized. So if the whole point is to freeze credit card access to one specific merchant, a lock alone is not enough. Combine it with the cancellation and dispute steps above.

Locking is also different from closing the card. A lock is temporary and reversible in seconds. Closing the account is permanent and can affect your credit utilization ratio and average age of accounts. Never close a Chase card just to stop one merchant unless you’ve already tried every other tool.

Which Method Should You Use? A Quick Decision Guide

Different problems need different tools. Use this quick guide to match your situation to the right first move:

| Your Situation | Best First Step | Backup If It Fails |

|---|---|---|

| Canceled subscription, merchant keeps billing | Contact merchant in writing to revoke authorization | File a dispute after the next unwanted charge posts |

| Charge you don’t recognize at all | Report as fraud, lock the card | Chase reissues new card number |

| Duplicate charge or wrong amount | File a Chase dispute for billing error | Written dispute within 60 days |

| Paid for goods that never arrived | Contact merchant, then dispute | CFPB complaint if unresolved |

| Card is missing but not confirmed stolen | Lock the card in the app | Report as lost and reissue if not found |

| One specific company charges you monthly and won’t stop | Cancel + written revocation + stop payment | Dispute each charge, then escalate |

The pattern to notice: for anything involving a known merchant, start with cancellation and documentation. For anything unknown, treat it as fraud and let Chase reissue the card. Card lock sits in the middle as a pause button, not a fix.

What Happens to Your Obligation to the Merchant

Blocking a payment is not the same as canceling a contract. This is one of the most misunderstood parts of the whole process, and it’s where cardholders sometimes get burned months later.

When you stop a payment or win a chargeback, Chase removes the charge from your credit card statement. That handles the money side. It does not, by itself, cancel any legal agreement you signed with the merchant.

If you’re under a 12-month gym contract, a wireless installment plan, or a service agreement with a cancellation clause, that contract still exists after the chargeback. The merchant can still send you a bill, add late fees, or hand the account over to collections.

If the merchant sends the debt to a collection agency, that account can end up on your credit report. A collection account can remain on your credit report for up to seven years. This starts from the original delinquency date.

It can significantly lower your credit score. So the safest path is to cancel the underlying agreement in writing first, then use Chase’s tools to block payment. That way, if the merchant tries to escalate, you have proof the service was legitimately canceled.

If the charge is a billing error under the Fair Credit Billing Act, or if the goods weren’t delivered, the FCBA protects you. It stops the disputed amount from being reported as delinquent while the investigation is ongoing.

Chase can’t ding your credit for the disputed dollars during that period. That protection only applies to disputes that are filed correctly. So, it’s important to file in writing and within the 60-day window.

Will This Affect Your Credit Score or Chase Relationship?

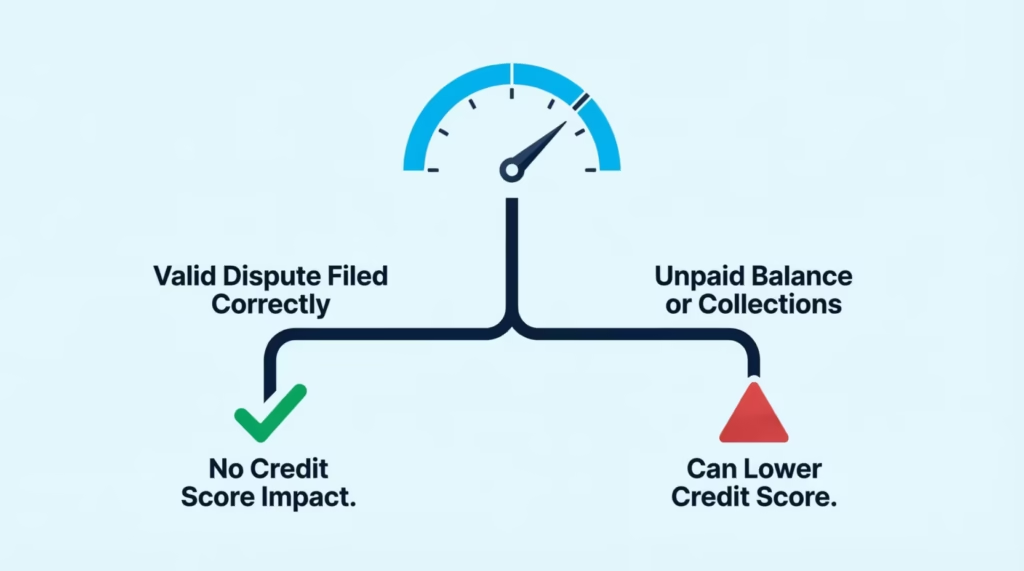

Filing a dispute, requesting a stop payment, or locking your card does not, on its own, affect your credit score. Chase won’t mark you late for the disputed amount in a valid FCBA dispute. So, none of these actions will appear as negative marks on your credit report.

Where credit impact can appear is in two indirect ways:

- Unpaid non-disputed balances. If you also stop paying the rest of your Chase bill because you’re upset about one charge, that missed payment can be reported and hurt your score. Always pay the undisputed portion on time.

- Collections from the underlying contract. If the merchant proves you still owe them, they can send you to collections. Then, that collection account can affect your credit file.

As for your Chase relationship, filing occasional disputes is normal. Chase, like every major issuer, sees disputes every day. A pattern of disputes can strain the relationship.

This happens when decisions always favor the merchant. It can also occur with disputes over services you clearly used and enjoyed. Use these tools when they’re warranted, not as a shortcut to avoid paying for something you agreed to.

What to Do if the Merchant Charges You Again

Sometimes the merchant charges you again the very next billing cycle. It’s frustrating, but it’s fixable, and each repeat charge actually strengthens your paper trail.

Start with the same playbook, then escalate:

- File a new dispute for each new charge. Chase treats each posted transaction as its own dispute. Reference your prior confirmation numbers so the investigator can see the pattern.

- Send a second written revocation of authorization to the merchant by email and, if possible, certified mail. Keep the receipt.

- Ask Chase to close and reissue your card with a new number. This is the most reliable way to stop a determined merchant. Once the old card number is dead, preauthorized charges to that number will fail. Update your legitimate merchants with the new number, but do not update the problem merchant.

- File a complaint with the Consumer Financial Protection Bureau. The CFPB complaint portal lets you file a formal complaint against Chase or the merchant. Companies typically respond within 15 days. In many cases, a CFPB complaint gets attention that regular customer service didn’t.

- Consider your state Attorney General or small claims court for persistent merchants who ignore both you and Chase. This is a last-resort option, but it works for clear breaches of contract or deceptive billing.

A determined merchant, a persistent Chase dispute, and a CFPB complaint usually end the charges. If it doesn’t, that pattern of unresolved disputes is exactly what a small claims judge or a state consumer protection office wants to see.

Frequently Asked Questions (FAQs)

Can I block a specific merchant on my Chase credit card?

No, Chase does not offer a self-service merchant blocking feature on credit cards. You need to combine merchant cancellation, stop payment requests, disputes, or card locks instead.

How do you legally stop a merchant from automatically charging your credit card?

Send written cancellation to the merchant stating you revoke authorization for further charges, keep proof of that request, then use a Chase stop payment for pending charges or a dispute for posted ones.

How do I block an automatic payment on Chase?

Call Chase customer service at 1-800-432-3117 and request a stop payment on the specific preauthorized charge, providing the merchant’s billing name, amount, and expected date.

Does locking a Chase card prevent transactions?

Locking blocks new purchases, cash advances, and balance transfers on the card, but some preauthorized recurring charges can still go through even when the card is locked.

Can you stop a transaction from going through?

Yes, if the charge hasn’t posted yet, a Chase stop payment request can reject that specific upcoming transaction before it clears.

Will Chase reverse a transaction?

Yes, Chase can reverse a posted charge through a formal dispute under the Fair Credit Billing Act, often issuing a provisional credit while investigating.

How long does a Chase dispute take to resolve?

Chase must acknowledge a dispute within 30 days and resolve most billing errors within 90 days, though complex fraud cases can take up to 120 days.

What’s the difference between disputing a charge and reporting fraud on Chase?

A dispute covers charges you authorized but have a problem with, like an unwanted subscription, while fraud covers charges you never approved at all and triggers an immediate card freeze and reissue.

Does blocking or disputing a charge cancel my contract with the merchant?

No, stopping payment only removes the charge from your statement. It doesn’t end a signed contract, so the merchant can still bill you or send the account to collections.

Can I dispute a credit card charge that is still pending?

No, Chase generally requires a charge to post before you can file a formal dispute. For a charge that hasn’t posted, request a stop payment instead.

Wrapping Up

Blocking a merchant on a Chase credit card isn’t just one step. It involves several actions:

- Direct cancellation

- Stop payment requests

- Formal disputes under the Fair Credit Billing Act

- A full card reissue, if necessary

The best way to start is by revoking authorization with the merchant in writing. Then, choose the right Chase tool for your issue. This could be a stop payment for pending charges, a dispute for posted charges, or a fraud report for any unauthorized transactions. Save every confirmation.

If this guide helped you cancel a stubborn subscription, share it with a friend facing the same charge. They shouldn’t have to deal with it alone.