Trying to figure out which Chase card will actually say “yes” can feel like a guessing game. You’ve seen the Sapphire Preferred ads and heard friends brag about their Freedom rewards, but your credit score sits somewhere in the middle, or maybe you’re just starting out. Applying for the wrong card means a hard pull for nothing, and that stings.

The easiest Chase credit card to get is the Chase Freedom Rise, built for people with limited or no credit history.

Here’s why this card is a smart first choice. We’ll also cover the sneaky 5/24 rule that can catch you off guard. Plus, we’ll share steps to increase your chances of approval before you apply.

Key Takeaways

This guide explains what is the easiest Chase credit card to get, identifying the Chase Freedom Rise as the top option for limited or no credit, plus the 5/24 rule and approval tips.

Core Facts:

- The Chase Freedom Rise is an unsecured card with no security deposit required, designed for people with limited or no credit history.

- The Freedom Rise offers 1.5% cash back on every purchase, no annual fee, and a $25 statement credit for setting up automatic payments within three months.

- Keeping at least $250 in a Chase checking or savings account is a documented factor that can improve Freedom Rise approval odds.

- The 5/24 rule means Chase generally denies applicants who opened five or more personal credit cards from any bank in the last 24 months.

- Mid-tier cards like Freedom Flex and Freedom Unlimited typically need scores around 700+, while Sapphire cards typically need 720+ to 740+.

- Chase evaluates income, debt load, recent hard inquiries, housing status, employment, and existing Chase banking relationships alongside credit score.

Best for:

- People with limited, thin, or no credit history looking for a first Chase credit card.

- Applicants who were previously denied by Chase and want to understand the 5/24 rule or other denial reasons.

- Readers comparing credit score requirements across the Chase card lineup before applying.

What Is the Easiest Chase Credit Card to Get?

If you want a quick answer: the Chase Freedom Rise is the most accessible Chase card on the market right now. It was designed for people with thin credit files or no credit at all. That means you don’t need a long borrowing history or a top-tier score to qualify. Most other Chase cards, like the Sapphire or Freedom Flex, want to see a strong credit profile. The Freedom Rise doesn’t ask for that.

Here’s the key thing to understand. “Easiest to get” is not the same as “best rewards.” The Freedom Rise gives you a flat 1.5% cash back on every purchase. That’s solid, but it won’t match the bonus categories or travel perks on Chase’s premium cards. Think of it as a doorway. You get in, you build your history with Chase, and later you can move up to a card with richer benefits.

For readers looking for a Chase starter credit card or a Chase card for fair credit, the Freedom Rise fills that exact gap. It’s the entry point Chase used to lack. Before this card existed, most beginners had to look at secured cards from other banks. Now Chase has its own answer, and it comes with no security deposit at all.

If your credit sits below the 650 mark, or if you’re new to credit and have no FICO score yet, this is the card to target first. Everything else in the Chase lineup gets harder from here.

Chase Freedom Rise: Chase’s Card for Limited or No Credit

The Chase Freedom Rise stands out because it’s an unsecured card that welcomes people who normally get turned away. Most beginner-friendly options force you to put down a cash deposit. This one doesn’t. That alone makes it worth a close look for anyone starting from zero.

Who actually qualifies? People with limited credit history, no credit history at all, or those rebuilding after a rough patch. You don’t need to hit the average U.S. FICO score of 715 that Experian reported for 2025 to get in. Chase doesn’t publish a hard minimum, but real-world approvals suggest scores in the low 600s, or even no score at all, can still work.

The features are simple and useful for a first card:

- 1.5% cash back on every purchase, with no categories to track

- No annual fee, so keeping the card open costs you nothing

- A $25 statement credit after you set up automatic payments in the first three months

- Free credit score tracking through Chase Credit Journey

- Access to Chase’s mobile app, alerts, and fraud protection

How is this different from a secured card? A secured card asks you to deposit cash (often $200 to $500) as collateral before you can spend a dime. If you close the account, you get that money back. The Freedom Rise skips this step. You get a real unsecured line of credit from day one. That’s rare for a credit-building card with no annual fee.

One more thing worth noting. Chase will review your account over time. If you use the card responsibly, pay on time, and keep balances low, you may be considered for an upgrade to a Freedom Flex or Freedom Unlimited later. That’s a real path forward, not just a marketing promise.

💡 Pro Tip: Set up autopay for at least the minimum payment the day your card arrives. You’ll never miss a due date, and you’ll grab the $25 statement credit without any extra effort.

Boost Your Odds With a Chase Checking or Savings Account

This is the single most useful lever most people miss. Chase confirmed in its official launch announcement that keeping at least $250 in a Chase checking or savings account helps improve your chances of approval for the Freedom Rise.

Here’s how to use it the right way:

- Open a Chase checking or savings account first. Basic checking has no monthly fee if you meet simple requirements like a direct deposit.

- Deposit at least $250 into the account.

- Apply for the Freedom Rise within a few days of that deposit hitting your account.

This is not a guarantee. Chase still checks your credit report, income, and other factors. But it is a documented, real advantage. Applicants who already bank with Chase give the system more data to work with. That reduces risk from Chase’s point of view, which lifts your approval odds.

If you can, open the account and fund it before you apply. Applying the same day you open the account can work, but giving it a few days to settle looks cleaner on Chase’s end.

⚠️ Mistake to Avoid: Don’t apply for the Freedom Rise the same hour you open your Chase checking account. Wait at least two to three days so the deposit fully posts and the banking relationship shows up on Chase’s internal profile.

Credit Score Requirements for Chase’s Other Popular Cards

Once you move past the Freedom Rise, the bar goes up fast. Chase’s other cards want to see real credit history and stronger scores. Knowing where each card sits helps you avoid a wasted application and a needless hard pull.

Here’s a realistic look at what each major Chase card typically wants:

| Chase Card | Typical Credit Needed | Best For |

|---|---|---|

| Chase Freedom Rise | Limited / No credit (roughly 600+) | First-time cardholders |

| Chase Freedom Flex | Good credit (~700+) | Rotating 5% cash back |

| Chase Freedom Unlimited | Good credit (~700+) | Flat 1.5%–3% cash back |

| Chase Sapphire Preferred | Good to excellent (~720+) | Travel rewards, mid-tier |

| Chase Sapphire Reserve | Excellent (~740+) | Premium travel, lounges |

| Ink Business Unlimited | Good credit (~680+) | Small business owners |

The Freedom Flex and Freedom Unlimited are the mid-tier cards. Most approvals happen with a FICO score range of 700 or higher, steady income, and a clean recent history. There is no annual fee on either card, which makes them popular targets after building some credit with the Freedom Rise.

The Sapphire Preferred and Sapphire Reserve sit in premium territory. You’ll generally need good-to-excellent credit, meaning a score in the 720s or above, a healthy income, and low existing debt. Chase looks harder at these applications because the rewards and travel perks are much richer.

A common myth is that Chase has a Chase card for bad credit below the 600 mark. That’s not really true. Chase doesn’t publish a subprime credit card. If your score is below 580, focus on rebuilding first through a secured card from another issuer, then work your way up to the Freedom Rise once your score recovers.

The average U.S. FICO score sits at 713, according to Experian’s 2025 credit trends report. If you’re around that average, the Freedom Flex or Unlimited become realistic targets. If you’re well below, the Freedom Rise is your smart first step.

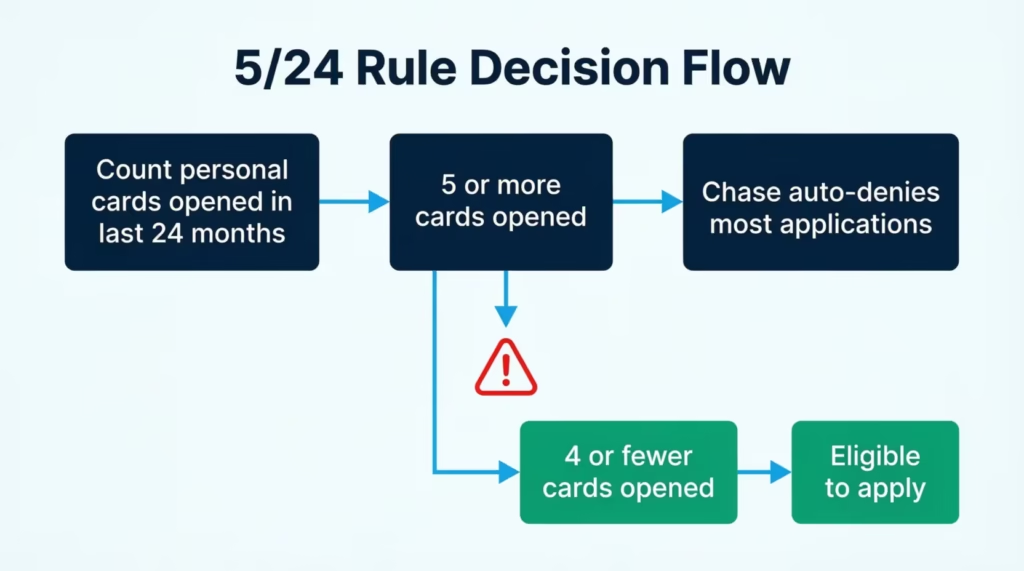

The Chase 5/24 Rule: A Hidden Reason You Might Get Denied

The 5/24 rule is one of the biggest reasons people with great credit still get denied by Chase. It’s an unwritten policy, meaning Chase never officially states it, but the pattern is very well documented across the industry.

Here’s the rule in plain English. If you’ve opened five or more personal credit cards from any bank in the last 24 months, Chase will almost always auto-deny your application for most of its cards. It doesn’t matter if your credit score is 800. It doesn’t matter if you make $200,000 a year. The system looks at the count and stops.

A few important details:

- The rule counts personal credit cards from any bank, not just Chase.

- Business credit cards from most issuers do not count toward your 5/24 total, because they usually don’t show up on your personal credit report.

- Authorized user accounts can count in some cases, though calling the reconsideration line to explain often removes them.

- Store cards, retail credit cards, and even short-lived cards you closed still count while they’re within the 24-month window.

Which cards does 5/24 hit? Most of the big names. That includes the Chase Sapphire Preferred, Sapphire Reserve, Freedom Flex, Freedom Unlimited, and the Ink business lineup. The Freedom Rise appears to be more lenient here, which is another reason it’s often the easiest path in.

The rule exists to stop churners, meaning people who open cards, grab the sign-up bonus, and move on. Chase doesn’t want that behavior on its books. So even if you’re not a churner, you can still get caught in the same net.

The Points Guy explains that Chase’s system considers you to fall below 5/24 on the first day of the 24th month after your fifth card was opened. So if your fifth card opened in June 2024, you’ll drop below 5/24 in June 2026.

The hard inquiry from a denied Chase application still hits your report. That’s why checking your 5/24 status matters so much before you apply.

📌 Did You Know: The 5/24 rule can trigger a denial even with an 800+ credit score and a six-figure income. Approval odds are shaped by account count, not just creditworthiness.

How to Check Your Own 5/24 Status

You don’t need any special tool to figure out where you stand. The process is simple and free.

- Pull a free credit report from AnnualCreditReport.com, the only site officially authorized by federal law.

- Look at the “Accounts” or “Open Accounts” section.

- Count every personal credit card with an “Opened” date within the last 24 months.

- Exclude business cards that don’t show on your personal report.

- Include cards you’ve since closed, since 5/24 counts open dates, not current status.

If your count is four or fewer, you’re under 5/24 and can apply for most Chase cards. If your count is five or higher, wait until the oldest card ages past 24 months before applying for a Chase card that follows the rule. Or, target the Freedom Rise, which appears to be far less strict.

Apps like Credit Karma also list your open accounts with dates, which makes counting quick. Just double-check the report itself for accuracy.

What Else Chase Looks at Beyond Your Credit Score

Your credit score is only one part of the picture. Chase runs a broader review before approving any card. Understanding these extra factors helps you spot weak areas and fix them before you apply.

Key items Chase reviews:

- Income: Chase wants to know you can pay back what you charge. Higher-tier cards like the Sapphire Reserve often want $75,000+ in income. Starter cards care less about a big number.

- Existing debt load: Your debt-to-income ratio matters. If half your income already goes to loan payments, Chase gets nervous, no matter how high your credit score is.

- Number of open credit accounts: Too many cards, even outside 5/24, can suggest you’re spread thin. Too few can suggest a very thin file.

- Recent hard inquiries: Every hard pull in the last six to twelve months signals credit seeking. Two or three is fine. Six or more looks risky.

- Housing status: Owning, renting, or living with family all get logged. Owning tends to look most stable, but renting is fine as long as your income and history are steady.

- Employment status: Steady, verifiable employment helps. Self-employed applicants can qualify but may need to explain their income.

- Chase banking relationship: Existing Chase checking, savings, mortgage, or auto-loan customers often see better approval odds. Chase already has your data, which reduces risk.

Your credit score requirement is the headline number, but these supporting factors decide close calls. A 690 score with strong income, low debt, and an existing Chase checking account will often beat a 720 score with high debt and no banking history.

If you want to stack the deck before you apply, pay down existing balances so your utilization drops below 30%, keep your job history stable, and open a Chase deposit account at least a month ahead. These small steps often make the difference between a borderline approval and a clean yes.

Easiest Chase Business Card to Get

Small business owners have a slightly different path. Chase’s Ink lineup is well-respected, but not every Ink card is equally easy to qualify for. The easiest Chase business card to get is generally the Ink Business Unlimited® Credit Card or the Ink Business Cash® Credit Card. Both have no annual fee and lower approval bars than the Ink Business Preferred or Ink Business Premier.

Typical qualifying criteria for Ink Business Unlimited:

- Personal credit score in the good range (roughly 680+), since Chase pulls your personal credit for business cards.

- Proof of business activity, even if that business is a side hustle or freelance work.

- A valid EIN or your SSN if you operate as a sole proprietor.

- Some level of business revenue, though there’s no strict minimum. Even a few hundred dollars a month can support an application.

- A clean recent inquiry and account history on your personal credit report.

The Ink Business Unlimited gives you a flat 1.5% cash back on all business purchases and often runs sign-up bonuses worth several hundred dollars. The Ink Business Cash gives 5% back on office supplies and telecom. This benefit suits online sellers, consultants, and small shops perfectly.

For freelancers, gig workers, Etsy sellers, Uber drivers, and consultants, this matters. You don’t need an LLC or a corporation to apply. Sole proprietors qualify all the time by using their SSN and reporting their real self-employment income.

How Business Card Approval Differs From Personal Cards

Business cards look similar on the outside, but the approval logic is different in a few important ways.

First, most business cards, including Chase’s Ink lineup, are still subject to the 5/24 rule for approval eligibility. So if you’ve opened five or more personal cards in the last 24 months, Chase will likely deny an Ink card too, even though it’s a business product.

Second, the Ink cards typically don’t add to your future 5/24 count. Chase business cards, like those from most major banks, report to business credit bureaus. They don’t show up on your personal credit report.

So opening an Ink card doesn’t push your personal card count up, which keeps you eligible for more Chase products later. This is a huge reason experienced applicants love the Ink lineup.

Third, business cards ask for revenue and business information. You’ll need to provide:

- Type of business (sole proprietor, LLC, corporation)

- Business start date

- Estimated annual revenue

- Estimated monthly spending on the card

- Business name (your legal name is fine for sole proprietors)

Even small numbers work. Reporting $5,000 in annual revenue is completely acceptable if that’s accurate. Chase isn’t looking for a Fortune 500 balance sheet. They’re looking for a real, honest business activity.

Fourth, your personal credit still carries most of the decision weight. Chase reviews your personal FICO score, income, and debt in the same way it would for a personal card. So the same score guidance applies, generally 680+ for a comfortable approval on Ink Business Unlimited.

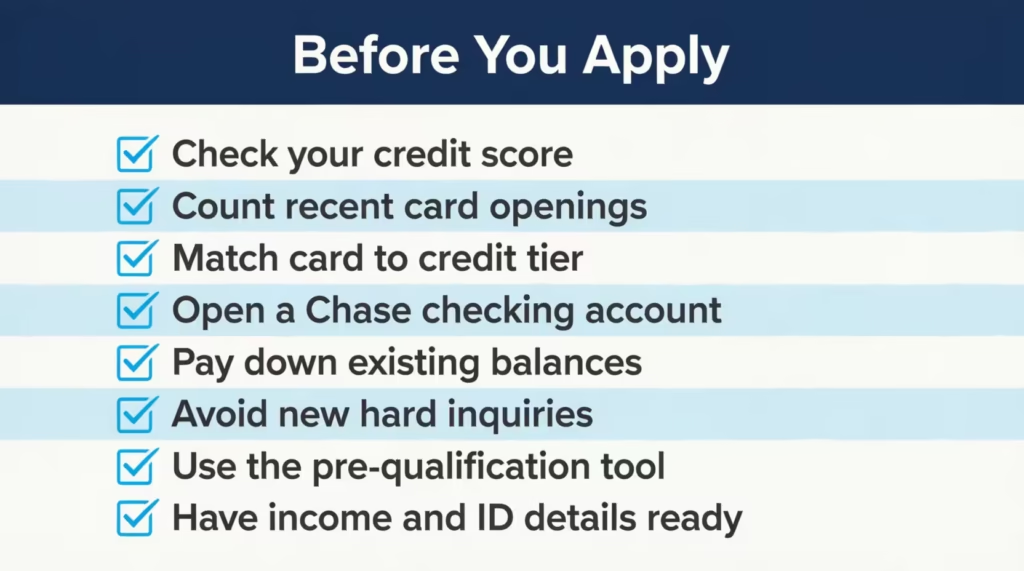

Steps to Take Before You Apply

Rushing to apply is the number one mistake. A little preparation can turn a borderline application into an approval. Follow this checklist in order.

- Check your credit score for free. Use Chase Credit Journey, Credit Karma, or your bank’s free FICO tool. Know your number before you pick a card.

- Count your recent card openings. Pull your credit report from AnnualCreditReport.com and check your 5/24 status. If you’re at five or more, target the Freedom Rise or wait for accounts to age off.

- Match the card to your credit tier. Score under 670? Aim for Freedom Rise. Score 700+? Freedom Flex or Unlimited works. Score 720+? Sapphire cards become realistic.

- Open a Chase checking or savings account if you’re targeting the Freedom Rise. Deposit at least $250 and let it sit for a few days. This directly improves your approval odds.

- Pay down existing balances. Lower credit utilization looks stronger to Chase. Aim for below 30% across all cards, and ideally below 10% on any single card.

- Avoid other hard inquiries. Don’t apply for other loans, cards, or lines of credit in the 30 days before your Chase application.

- Use Chase’s pre-qualification tool to test your odds without a hard pull. Details below.

- Have your details ready. Income, employment, housing payment, and Social Security number. Fumbling on the application form doesn’t help you.

Taking a week to prepare is often more valuable than any specific card strategy. Small fixes to your report and profile can shift you from borderline to approved.

Use Chase’s Pre-Qualification Tool

Chase’s pre-qualification tool lets you see which cards you may be matched for without any impact on your credit score. Here’s how it works and what to know:

- It uses a soft credit check, so there’s no hard inquiry and no score drop.

- You’ll enter basic info like name, address, and last four digits of your SSN.

- Chase then displays cards you’re pre-qualified for based on internal data and a soft pull.

- Results appear instantly on Chase’s site.

Being pre-qualified is not a guaranteed approval. When you actually apply, Chase runs a full hard pull and reviews your income, existing debt, and full credit file. But pre-qualification is a very strong signal. If a card shows up in your pre-qualified list, your approval odds are usually much higher than a cold application.

If nothing shows up, that’s important information too. It suggests your profile isn’t ready for Chase’s mid-tier or premium cards yet. Either target the Freedom Rise or spend a few more months building credit before applying.

The Chase Credit Journey tool is free and part of your Chase online banking. It provides a VantageScore and ongoing credit monitoring. Combine it with the pre-qualification tool for a complete picture before you commit to a hard inquiry.

What to Do If You’re Denied

A denial isn’t the end of the road. Chase sends every denial with a reason code, and knowing what to do next can turn a “no” into a “yes” within a few weeks or months.

Step 1: Read the denial letter carefully

Chase mails or emails a letter within 7 to 10 days that lists specific reasons. Common ones include “too many recent credit card accounts” (that’s 5/24), “insufficient credit history,” “high balances,” or “insufficient income.”

Step 2: Call the Chase reconsideration line

This is often the fastest fix. The number for personal cards is 1-888-270-2127, and the business card line is 1-800-453-9719. A real person reviews your application and hears your side. Be polite, be brief, and be ready to explain:

- Why you applied

- How you plan to use the card

- Any context Chase missed (like a recent income increase or a paid-off loan)

Many denials get flipped to approvals through reconsideration. It’s not a magic wand, but it’s a real second chance.

Step 3: Wait for accounts to age off 5/24

If 5/24 was the cause, no phone call will change that. Track when your fifth-most-recent card was opened and mark the 24-month anniversary on your calendar. Reapply the month after that date.

Step 4: Fall back to the Freedom Rise

If you were denied for a Sapphire or Freedom Flex due to thin credit, the Freedom Rise is your building path. Six to twelve months of on-time payments with a Freedom Rise can lift your profile enough to qualify for the card you originally wanted.

Step 5: Fix the root cause

If the denial reason was high balances, pay down debt. If it was low income, wait until you can document a raise or new job. If it was too many inquiries, hold off on new credit for six months.

Step 6: Don’t reapply too soon

Applying again within 30 days almost always leads to another denial and another hard inquiry on your report. Wait 90 days at minimum, and only after you’ve addressed the reason for the first denial.

A denied application isn’t a permanent mark against you. It just means the timing or the card choice was off. With the right adjustments, most people who get denied are approved on their next attempt.

Frequently Asked Questions (FAQs)

What is the easiest Chase credit card to get?

The Chase Freedom Rise is the easiest Chase card to get approved for. It’s built for people with limited or no credit history and requires no security deposit.

What is the best Chase credit card for beginners?

The Chase Freedom Rise is Chase’s best card for beginners, offering 1.5% cash back on every purchase with no annual fee. It also gives a $25 statement credit for setting up automatic payments within the first three months.

Can I get a Chase credit card with a 560 credit score?

A 560 score falls below what Chase typically approves, even for the Freedom Rise. Chase doesn’t publish a subprime card, so focus on rebuilding credit through a secured card from another issuer first.

Can I get a Chase card with a 650 credit score?

Yes, a 650 score puts you in range for the Chase Freedom Rise, which suggests approvals in the low 600s are realistic. Mid-tier cards like Freedom Flex typically need scores closer to 700.

What is the minimum credit score for a Chase card?

Chase doesn’t publish an official minimum score, but real-world approvals for the Freedom Rise suggest scores in the low 600s can work. Some applicants with no credit score at all have also been approved.

Why would I get denied for a Chase credit card?

Common denial reasons include the 5/24 rule, insufficient credit history, high existing balances, or insufficient income. Chase sends a denial letter within 7 to 10 days listing the specific reason.

Which Chase card is hardest to get?

The Chase Sapphire Reserve is the hardest Chase card to get approved for. It typically requires excellent credit around 740 or higher, plus high income and low existing debt.

Does Chase have a starter credit card?

Yes, the Chase Freedom Rise is Chase’s starter credit card. It’s unsecured, requires no deposit, and is designed for people with thin or no credit files.

Can you have a 700 credit score and still get denied?

Yes, a 700 score can still get denied under Chase’s 5/24 rule if you’ve opened five or more personal credit cards in the last 24 months. Income, debt load, and recent inquiries also factor into the decision.

Does Chase give instant approval?

Chase’s pre-qualification tool gives instant results using a soft credit check with no impact on your score. A full application still requires a hard pull, and final approval decisions can take longer to process.

Wrapping Up

Getting approved by Chase comes down to matching the card to your actual credit profile. The Freedom Rise stands out as the most accessible option for those with limited or no credit history, especially when paired with a Chase deposit account. Higher-tier cards need stronger scores and a clean 5/24 count.

The best way for most first-time applicants is to start with Freedom Rise. After building twelve months of clean payment history, they can then move to Freedom Flex or Sapphire Preferred.

If this guide helped, share it with a friend or family member who’s worried about their first credit card application. It might save them from a hard inquiry.