We’ve all had that moment. You want to book a trip, buy a new laptop, or just breathe a little easier when a bill hits your card. But your Chase credit limit feels too tight, and every swipe pushes your utilization higher. Many cardholders worry that asking for more credit will trigger a hard pull, lower their score, or lead to a flat denial. Learning the right way to handle a Chase credit limit increase removes that guesswork.

The fastest path is to request the raise through your Chase online account or the mobile app, prepare updated income details, and confirm whether Chase will use a soft or hard pull before you submit.

Below, we walk you through every request channel, the exact script to use on the phone, eligibility rules, and what to do if Chase says no. You’ll leave with a clear plan.

Key Takeaways

This guide explains how to request a Chase credit limit increase, including online, app, and phone request channels, eligibility factors, timing rules, target increase amounts, and how to protect your credit score during the process.

Core Facts:

- Chase offers three request channels: the online form at chase.com, the mobile app or secure message, and a phone call, each leading to the same review team.

- Most cardholders should wait at least 6 months after opening a Chase card before requesting a limit increase, since Chase needs sufficient spending history to review.

- A reasonable target increase is 25 to 50 percent above the current limit, and requesting a full doubling of the limit often triggers a hard pull or denial.

- Automatic Chase account reviews typically occur every 6 to 12 months and always use a soft inquiry, which does not affect a credit score.

- Online and app requests may use either a soft or hard pull, and cardholders can ask the representative or check the form wording to confirm which type applies before submitting.

- If denied, Chase sends an adverse action letter within 30 days listing the reason, and cardholders can call the reconsideration line to request another review.

Best for:

- Chase cardholders who want to lower their credit utilization ratio without increasing their spending.

- Cardholders whose income has increased since they opened their Chase card and want that change reflected in their credit line.

- Anyone who was previously denied a limit increase and wants to understand how to prepare a stronger follow-up request.

Ways to Request a Chase Credit Limit Increase

Chase gives you three main ways to ask for more credit on your card. You can use the website, the mobile app with a secure message, or a direct phone call. Each path leads to the same review team, but the speed, the paper trail, and the way you speak to Chase are different.

Picking the right channel matters. Some people get a fast yes online. Others do better on the phone, where they can talk through their income and spending. If you have a Chase Sapphire, Freedom, Slate, Ink Business, or co-branded card like United or Southwest, all three options are open to you.

Here is a quick view of how the three channels compare:

| Channel | Best For | Typical Decision Time | Paper Trail |

|---|---|---|---|

| Chase.com online form | Fast, simple requests | Instant to a few minutes | Yes, in your account |

| Chase mobile app / secure message | Written requests with notes | Same day to 2 business days | Yes, in message inbox |

| Phone call | Complex cases, reconsideration | Same call, often instant | You must take notes |

Pick the channel that fits your comfort level. If you know your numbers and want a fast answer, the site is great. If you want a written record with a short reason, use the secure message. If your case needs a real person, call.

Requesting Online Through Chase.com

The online form is the quickest way to ask for a credit line increase from Chase. You sign in at chase.com, open the card you want to change, and look for the “Request credit line increase” option under the account services menu.

Once you open the form, Chase asks for a few key details:

- Your current gross annual income

- Your monthly housing payment (rent or mortgage)

- Your total employment status

- The new credit limit amount you want

- A short reason for the request

Type these details carefully. Chase compares your new income to what they have on file. If your income has gone up since you opened the card, this is your chance to update it. Pick a target limit that feels reasonable, not double what you have now.

After you hit submit, Chase runs a quick review. Many users see a decision on screen within seconds. Others get a message that says the request is under review, and Chase will follow up in 7 to 10 business days by mail or secure message.

💡 Pro Tip: Update your income in your Chase profile a few days before you submit the request. That way, the number feels stable and not like a last-minute change.

Requesting Through the Chase Mobile App / Secure Message

If you prefer the app, open the Chase Mobile app, tap the card, and go to the “Things you can do” menu. Some card types show the same online form here. If not, use the secure message feature to write to a Chase rep.

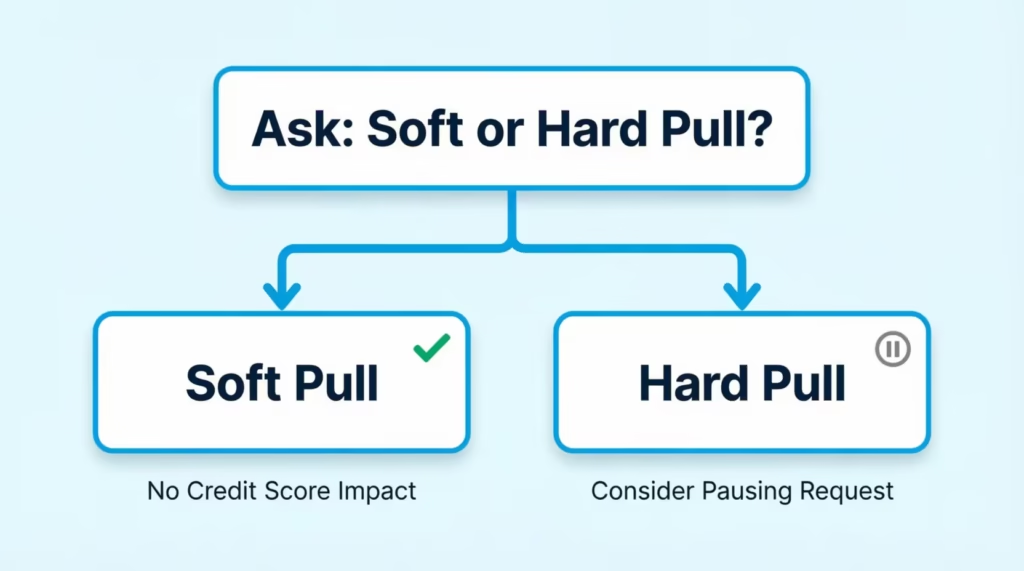

A secure message request should stay short and clear. State that you want a higher limit on your card. List your updated yearly income, your monthly rent or mortgage, and your target new limit. Ask the rep to confirm if the review will use a soft pull or a hard pull before they run it.

The app path is helpful when you want your words on record. You can look back at the message thread later if there is any confusion. Chase usually replies within one to two business days.

How to Request by Phone (With What to Say)

Some cardholders get better results by calling. A phone rep can pull up your account, walk you through the form, and answer questions on the spot.

The main Chase customer service number for personal cards is 1-800-432-3117. Business cardholders should use 1-800-CHASE38 (1-800-242-7338).

When you call, the rep will ask a few standard questions:

- Your full name and card details for identity checks

- Your current gross annual income

- Your monthly housing cost

- Your employment status

- The exact new limit you want

- The reason for the request

Prepare your answers before you dial. Have your pay stub or tax return close by. Keep your rent or mortgage number ready.

Use a script like this to keep the call clean and on point:

“Hi, I’d like to request a credit limit increase on my Chase card ending in [last four digits]. My current limit is [amount], and I’d like to raise it to [new amount]. My gross annual income is now [amount], up from [old amount] when I opened the card. My monthly housing payment is [amount]. Before we move forward, can you confirm whether this review will use a soft inquiry or a hard inquiry on my credit?”

That last line is key. Ask about the pull type first. If the rep says it will be a hard inquiry and you don’t want the score dip, you can pause the request. If it’s a soft pull, you can move ahead with less risk.

The rep may decide on the call. If not, they will note that a written reply will come within 7 to 10 business days.

Chase Automatic Credit Limit Increases

Chase also runs periodic account reviews on its own. If your account is in good shape, they may raise your limit without you asking. These reviews often happen every 6 to 12 months, though Chase does not publish a fixed schedule.

The good news about an automatic review is that it uses a soft inquiry. A soft pull does not show on your credit report to lenders and does not lower your FICO score. You may see the new limit appear in your account with a short note or a letter in the mail.

To boost your odds of an automatic bump, do these things:

- Use the card each month, but keep your balance well under the limit

- Pay your full statement balance on time, every time

- Avoid returned payments or late fees

- Keep your Chase profile up to date with your latest income

There is no way to force an auto-increase. But steady, healthy use of the card is the best signal you can send.

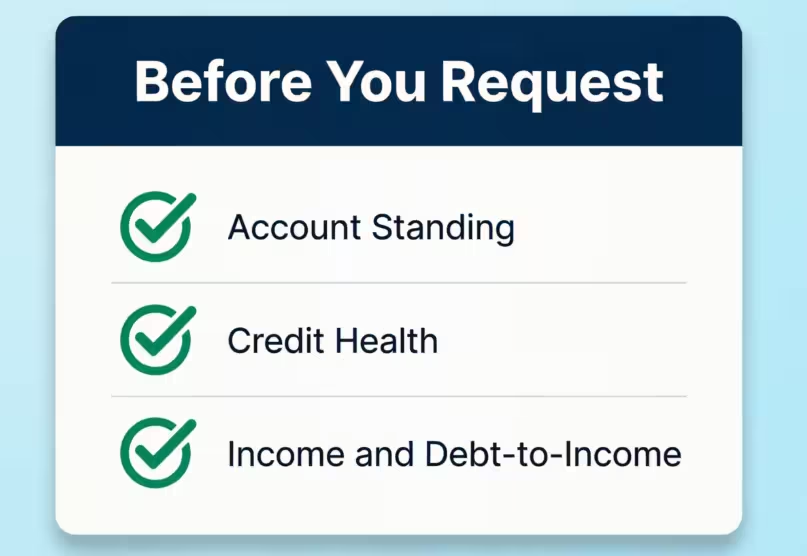

Eligibility Requirements Before You Request

Before you send in your request, check the basic rules that Chase looks at. Meeting these does not promise a yes. But missing them almost always leads to a no.

Chase looks at three main areas:

- Account standing. Your card must be in good shape. No missed payments in the last 6 to 12 months. No returned payments. No fraud flags or account holds.

- Credit health. Chase does not publish a strict cutoff, but most approved requests come from cardholders with a FICO score of 700 or higher. Experian data shows the average FICO Score in the U.S. was 717 in 2024, so a score in that range gives you a fair shot. Experian reports that the U.S. average credit score continues to trend upward year over year.

- Income and debt-to-income. Your debt-to-income ratio should be reasonable. Chase does not share an exact DTI limit, but most lenders prefer under 43 percent. The Consumer Financial Protection Bureau notes that 43 percent is the highest DTI for most qualified mortgages, and card issuers use similar thinking.

Also check that your income is up to date. If you got a raise or a new job, share the new number. This alone can move a maybe into a yes.

How Long to Wait After Opening a Chase Card

Chase does not publish a fixed wait time, but most reports from real cardholders point to a 6-month minimum after account opening. Some report success at 4 months, but that is rare.

If you ask too soon, Chase may deny the request because they don’t have enough spending history to review. Waiting also gives you time to build a strong pattern of on-time payments. That history is the biggest factor in a yes.

For a new card, mark 6 months on your calendar from the open date. Use the card in that window, pay in full, and then submit the request. If your first ask is denied, wait another 6 months before you try again. Requesting too often can look risky to Chase.

What Information Chase Will Ask For

Chase asks a small but focused set of questions. Have these numbers ready before you submit online or pick up the phone:

- Gross annual income. Use your pretax pay. Include a spouse or partner’s income only if you have reasonable access to it, per federal rules for card applicants over 21.

- Employment status. Full-time, part-time, self-employed, retired, student, or homemaker.

- Employer name and length of employment. For salaried workers.

- Monthly housing payment. Rent or mortgage total, not including utilities.

- Requested new credit limit. A clear number, not a range.

- Reason for the request. Keep it short and honest. Something like “planning a large purchase” or “want a lower utilization ratio” works fine.

Chase does not ask you to upload pay stubs or tax forms in most cases. They rely on the number you share. Still, give an accurate figure. Federal rules under the CARD Act require issuers to verify your ability to pay, and inflated numbers can trigger a denial or an account review.

Some self-employed cardholders should have their most recent tax return handy. If Chase needs proof, they may ask for it after the initial request.

How Much of an Increase to Request

Picking the right target amount is where many people slip up. Ask for too little, and you leave value on the table. Ask for too much, and Chase may say no or grant only a small part of what you wanted.

A good rule is to request a 25 to 50 percent bump over your current limit. If your limit is $5,000, a request for $6,500 to $7,500 is reasonable. If your limit is $10,000, a request in the $12,500 to $15,000 range is a solid ask.

Base your target on real needs, not big dreams. Think about:

- Your typical monthly spend on the card

- Any large purchases coming up in the next 6 months

- Your goal credit utilization ratio (many experts point to under 30 percent, and under 10 percent is even better)

For example, if you spend $2,000 a month on the card and want your utilization under 30 percent, you need a limit of at least $6,667. Aim a bit higher than the minimum so a spending spike does not push your ratio up.

⚠️ Mistake to Avoid: Asking Chase to double your limit in one shot. Large jumps often trigger a hard pull or a flat denial. Stepwise increases every 6 to 12 months work better.

Will Requesting a Credit Limit Increase Hurt Your Credit Score?

This is the top worry for most cardholders. The honest answer is: it depends.

Chase does not have a clear public rule about when it uses a soft inquiry versus a hard inquiry for a limit request. Real user reports and reconsideration data suggest a mixed pattern:

- Many online and app requests use a soft pull, especially for smaller increases.

- Some phone requests, or large increases, may trigger a hard pull.

- Automatic reviews always use a soft pull.

A soft inquiry does not affect your FICO score. A hard inquiry can drop your score by a few points (usually less than 5) and stays on your report for two years. Only one year of a hard pull affects your score in most scoring models.

To protect yourself, ask the rep or check the online form for pull-type wording before you submit. If the form or rep says “we may pull your credit,” that means it’s a hard inquiry. If they say “no impact to your credit,” that’s a soft pull.

The long-term score effect can actually be positive. A higher limit with the same spending lowers your utilization ratio. Since utilization makes up about 30 percent of your FICO Score, per myFICO’s breakdown of credit score factors, a lower ratio can lift your score by more than the small dip from a hard pull.

What Happens If Chase Denies Your Request

A denial stings, but it is not the end. Chase must send you an adverse action letter within 30 days that lists the exact reasons. Common ones include:

- Account too new

- Recent late payments

- Too many recent credit inquiries

- Income too low for the target limit

- High balances on other cards

- Not enough activity on the Chase card

Read the letter closely. It tells you what to fix. If you feel the denial was based on wrong info, or you have new details to share, you can call the Chase reconsideration line at 1-888-270-2127. This team can review your case again with fresh notes.

When you call reconsideration, be calm and direct. Explain any changes since your first request. Share updated income, a fresh pay stub, or proof that a late payment was a bank error. Ask the rep to note the account and re-review your case.

If reconsideration also says no, take these steps:

- Wait at least 6 months before you ask again.

- Focus on paying down other card balances to lower your total debt load.

- Check your credit reports at AnnualCreditReport.com for errors and dispute any that show up.

- Keep using the Chase card, pay in full each month, and update your income when it changes.

Time and clean habits are the best fix. A yes on your second try is common when you fix the reason from the first denial.

How a Higher Limit Affects Your Utilization and Spending

A higher limit is a tool. Used well, it can lift your credit score. Used poorly, it can pull you into debt. The math is simple, but the habits are what matter.

Your credit utilization ratio is the balance on your cards divided by your total limits. If you owe $3,000 on a $5,000 limit, your ratio is 60 percent. Raise the limit to $10,000 with the same $3,000 balance, and your ratio drops to 30 percent. That drop alone can raise your score by 10 to 30 points, based on how tight the old ratio was.

But there is a trap. Many cardholders see a higher limit as a green light to spend more. If your balance climbs to $6,000 on the new $10,000 limit, your ratio stays at 60 percent, and the score benefit is gone. Worse, you now owe twice as much.

To keep the win, follow these rules:

- Set a spending cap in your head based on what you can pay in full each month

- Track your balance mid-cycle, not just at the statement date

- Pay before the statement closes to lower the reported balance

- Treat the new limit as a safety net, not a spending budget

📌 Did You Know: Card issuers report your balance to the credit bureaus on the statement date, not the due date. Paying before the statement closes lowers the number lenders see, even if you plan to pay in full anyway.

Used with care, a Chase limit bump is one of the fastest ways to lower utilization, lift your score, and gain real breathing room in your budget.

Frequently Asked Questions

Why won’t Chase give me a credit limit increase?

Common reasons include a newer account with limited history, recent late payments, high balances on other cards, or income that doesn’t support the requested limit. Chase sends an adverse action letter within 30 days listing the exact reason for your denial.

Is a Chase credit limit increase request a hard pull?

It depends on the request type; automatic reviews always use a soft pull, while online, app, or phone requests may use either. Ask the representative or check the online form wording before submitting to confirm which type applies to you.

How often does Chase increase credit limits automatically?

Chase typically runs automatic account reviews every 6 to 12 months, though it doesn’t publish a fixed schedule. These reviews use a soft pull, so they don’t affect your credit score.

Why does Chase automatically increase my credit limit?

Chase rewards steady account behavior, including on-time payments, low balances relative to your limit, and no returned payments or fraud flags. Keeping your Chase profile updated with current income also improves your odds of an automatic bump.

Is a $30,000 credit card limit good?

A $30,000 limit works well if it keeps your usage low compared to your usual spending. Aim to use less than 30%. Staying under 10% is even better for your score. The limit itself matters less than how much of it you actually use each month.

What is the biggest killer of credit scores when it comes to credit limits?

High credit utilization is one of the biggest score drags, since it makes up about 30% of your FICO Score. A higher limit will only help if your balance doesn’t increase along with it, or else your utilization ratio will stay the same or even get worse.

How soon can I request a credit limit increase after opening a Chase card?

Most successful requests happen at least 6 months after account opening, since Chase needs enough spending history to review. Requesting too early can result in an automatic denial due to insufficient account history.

How much should I ask Chase to increase my credit limit by?

A 25 to 50 percent increase over your current limit is a reasonable target; for example, a $5,000 limit could reasonably become $6,500 to $7,500. Asking to double your limit in one request often triggers a hard pull or denial.

Wrapping Up

A Chase credit limit increase is one of the simplest tools for a stronger credit profile, but only when the timing and prep are right. Wait at least 6 months before you submit. Update your income first. Then, ask for a bump of 25 to 50 percent.

Also, confirm the pull type. This approach works best based on the request paths, eligibility rules, and score math discussed. If Chase says no, use the reconsideration line and fix the reason before you try again.

If you know a friend or family member stuck with a tight limit and rising utilization, share this guide with them. It could save them a hard pull, a denial, or months of higher interest costs.