You’re scanning your Chase statement, and something doesn’t look right. Maybe there’s a charge from a merchant you don’t recognize. Maybe the amount is off, or a refund you expected never arrived.

Many cardholders hesitate because they’re unsure about deadlines, required steps, or what evidence to gather. Knowing how to dispute a Chase credit card charge the right way is the key to getting your money back. Disputing a qualifying charge is a clear, protected process.

This guide covers every step, from checking eligibility to knowing exactly what to do if Chase says no.

Key Takeaways

This guide explains how to dispute a Chase credit card charge, covering which charges qualify under the Fair Credit Billing Act, required documentation, the 60-day filing deadline, three submission methods, and what to do if Chase denies your claim.

Core Facts:

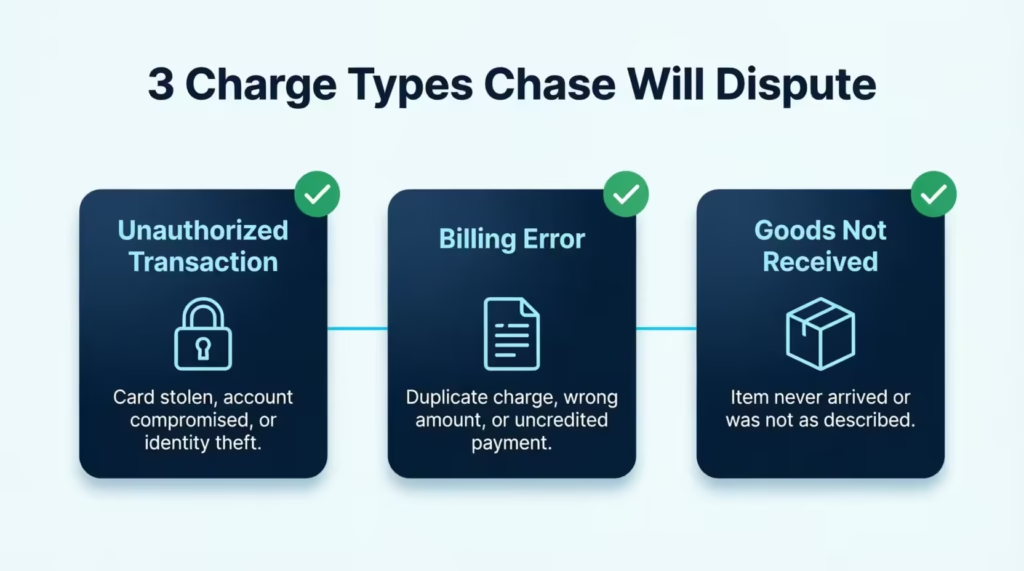

- Qualifying dispute reasons fall into three FCBA categories: unauthorized transactions, billing errors (duplicate charges, wrong amounts), and goods or services not received or materially misrepresented.

- Cardholders have 60 days from the statement date (not the date the charge was noticed) to file a Chase credit card dispute; missing this window forfeits all legal rights to contest the charge.

- For billing errors, contact the merchant by email first and allow 7 to 10 business days to respond before filing with Chase; fraud disputes skip this step entirely.

- Chase accepts disputes through three channels: online via the Chase app or website, by phone (number on the back of the card), or by certified mail to Chase Card Services, P.O. Box 15299, Wilmington, DE 19850-5299.

- Provisional credit for the disputed amount typically appears within 7 to 10 business days of filing; the full investigation can take up to 90 days for billing errors and 120 days for fraud.

- If Chase denies the dispute, cardholders can appeal in writing with new evidence, file a free complaint at consumerfinance.gov/complaint (CFPB), or escalate to the OCC at HelpWithMyBank.gov.

Best for:

- Cardholders who found an unrecognized, duplicate, or incorrect charge on their Chase statement and need a step-by-step process for disputing it before the 60-day deadline closes.

- People whose merchant refund was promised but never posted, or whose ordered goods were never delivered or arrived materially different from what was described.

- Anyone whose Chase dispute was already denied and who needs clear escalation options, including CFPB complaints and small claims court.

Which Chase Credit Card Charges Can You Dispute

Not every charge on your statement qualifies for a dispute. Chase only accepts disputes for specific, valid reasons. Knowing these upfront saves you time and helps you build the right case.

The Fair Credit Billing Act (FCBA), a federal consumer protection law, defines three main categories of charges that qualify:

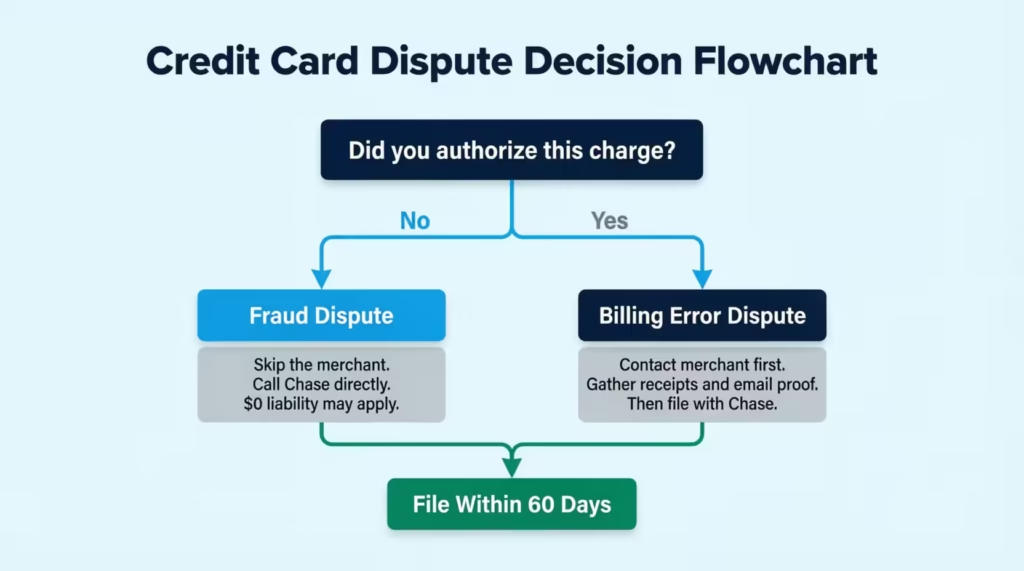

Unauthorized transactions. Someone used your card without your permission. This covers charges from a stolen card, a compromised account number, or identity theft. Chase’s $0 liability policy covers all confirmed fraudulent charges. You won’t owe anything once the unauthorized use is verified.

Billing errors. The amount charged was wrong. This includes duplicate charges, math errors, a payment that wasn’t credited to your account, and charges posted on the wrong date.

Goods or services not received or not as described. You paid for something but never got it. Or what arrived was clearly different from what the merchant promised.

These three categories cover most situations cardholders run into. Two common edge cases are worth knowing about.

The first is a merchant refund that hasn’t posted yet. If a merchant promised to refund you but the credit hasn’t appeared, give it 5 to 7 business days. If nothing posts after that, you have a solid dispute.

The second is a charge from a family member. If your spouse or partner used your card and you simply forgot about it, that’s not fraud. Filing an incorrect dispute can backfire if the merchant has evidence that the charge was authorized.

The dispute process is a formal legal tool. It works best when your reason clearly fits one of the three qualifying categories above.

Fraud Versus Billing Error: Why the Distinction Matters

There are two main types of credit card disputes: fraud and billing errors. They follow different rules, need different documents, and affect how you prepare your case.

A fraud dispute happens when someone uses your card without your knowledge. You never authorized the purchase. The card may have been physically stolen, the account number may have been compromised online, or someone opened a line of credit in your name.

A billing error dispute happens when a real merchant charged you incorrectly. They may have billed you twice for the same order. You may have returned an item and never received the refund. Or you paid for a service that was never delivered.

Here’s why the distinction matters in two key ways.

First, billing error disputes generally require you to try resolving the issue with the merchant before going to Chase. Fraud disputes don’t. There’s no point in contacting a fraudulent merchant.

Second, the documentation you need differs. Fraud disputes need confirmation that you didn’t authorize the transaction. Billing error disputes need records showing what you were promised versus what you were actually billed.

Getting your dispute type right before you file makes the entire process smoother and faster.

Charges That Do Not Qualify for a Dispute

Some charges look disputable but aren’t. Filing on a non-qualifying charge leads to a denial and wastes time.

The most common non-qualifying situations:

Buyer’s remorse. You authorized the purchase and have now changed your mind. That’s not a billing error. A return request goes directly to the merchant, not to Chase.

Dissatisfaction with a product you accepted and kept. If you used the item and held onto it, the dispute process doesn’t apply. Your recourse is a direct refund request to the merchant.

Filing after the deadline. If the 60-day window has passed, the charge is generally no longer disputable through Chase.

A forgotten subscription. Many cardholders see an unfamiliar charge and assume fraud, then realize it’s an annual renewal they signed up for a year ago. Check your active subscriptions before filing.

If your charge doesn’t fit a qualifying category, contact the merchant directly. That’s the right channel and often the faster one.

Contact the Merchant Before Disputing With Chase

For billing error disputes, the FCBA expects you to try resolving the issue with the merchant first. This isn’t just a formality. It’s a step that can directly affect whether Chase accepts your claim.

If you skip the merchant and go straight to Chase, one of two things can happen. Chase may reject the dispute outright. Or Chase may accept it, but ask whether you tried the merchant first, and your “no” weakens your case.

More importantly, contacting the merchant creates a paper trail. That paper trail becomes evidence in your dispute file.

Here’s how to do this step correctly.

Use email, not a phone call. A phone call leaves no record. An email creates a timestamped document showing when you reached out, what you asked for, and what the merchant said in return. That record goes directly into your dispute file.

Be specific and direct. State the charge amount. State the transaction date. Describe what went wrong. Request a specific resolution, such as a full refund, and give a clear deadline.

David, a freelance photographer, paid $189 for a hotel stay he cancelled 36 hours before check-in, well within the hotel’s free cancellation window. Despite the valid cancellation, his Chase Sapphire card was still charged. He emailed the hotel’s billing department with his reservation number, the cancellation timestamp from his confirmation email, and a direct quote from the hotel’s own refund policy. He asked for a full refund and gave them 7 business days to respond.

Set a response deadline. Give the merchant 7 to 10 business days to reply. If they don’t respond or they refuse, you’ve met the FCBA’s merchant-contact requirement. Save the email thread and move on to Chase.

Hold onto every reply. If the merchant agrees to refund you, wait 5 to 7 business days for the credit to post. If it doesn’t, that whole thread becomes extra documentation for your dispute. If they refuse or go silent, their response (or lack of one) is evidence Chase wants to see.

⚠️Mistake to Avoid: Don’t file a dispute with Chase while a merchant refund is still processing. If both credits post, you could end up with a double credit that Chase will reclaim later. Wait 5 to 7 business days for a promised refund before filing with Chase.

When You Can Skip the Merchant and Go Straight to Chase

For fraud disputes, skip the merchant contact step entirely. Call Chase directly.

If someone used your card number without your permission, reaching out to the merchant serves no purpose and could alert a fraudulent operator. Chase’s fraud team handles these cases and can act quickly to protect your account.

There are also a few billing error situations where going straight to Chase is acceptable:

- The merchant is unreachable. The business has closed, the website is down, or the contact information no longer works. Document your attempt to reach them and proceed.

- The merchant has gone out of business. There’s no one to contact. Note this when you submit your dispute.

- The merchant has already refused in writing. Once they’ve given a firm “no,” the merchant-contact requirement is satisfied. Save their written refusal and file it with Chase.

In all these cases, document your actions before filing. A screenshot of a closed website or an unanswered email shows you made a reasonable good-faith effort.

How Long You Have to Dispute a Chase Credit Card Charge

The single most important number in this entire process is 60 days.

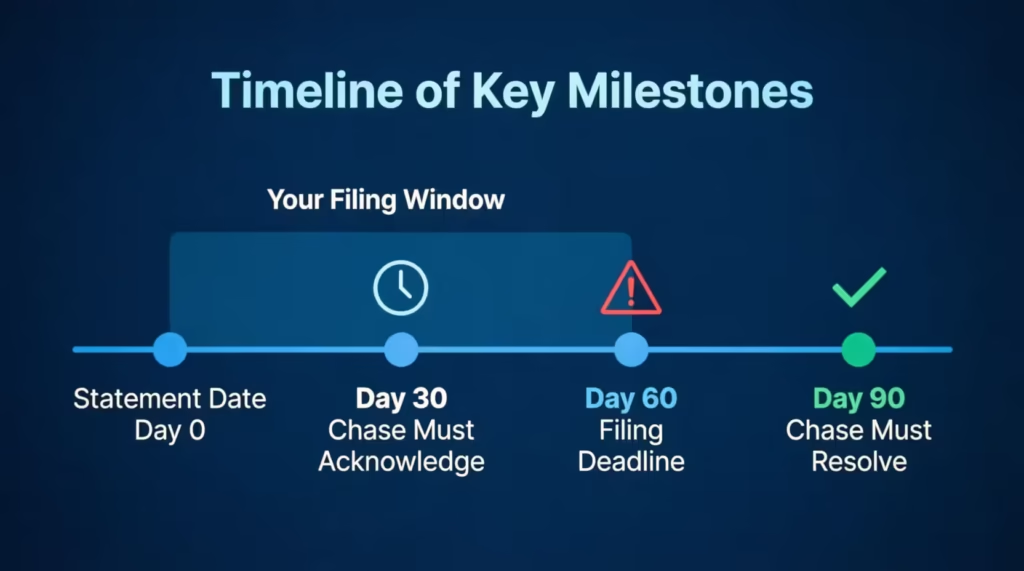

Under the Fair Credit Billing Act, cardholders have 60 days from the statement date on which the disputed charge first appeared to file with their card issuer. Miss this window, and you may permanently lose your legal right to contest the charge.

This rule applies specifically to billing errors. For fraud and unauthorized transactions, Chase may allow more flexibility under its own internal policies. But acting within 60 days is still the safest approach for every dispute type.

Once the deadline passes, Chase has no legal obligation to investigate. The charge becomes yours to pay.

📌Did You Know Under the FCBA, if Chase fails to acknowledge your dispute within 30 days or resolve it within 90 days (for billing disputes), Chase must forfeit the first $50 of the disputed amount regardless of the final outcome. Most cardholders never know about this protection.

The Clock Starts on the Statement Date, Not When You Noticed the Charge

This is where many cardholders lose their right to dispute without realizing it.

The 60-day window doesn’t start when you notice the charge. It starts on the date your statement was issued, meaning when it was mailed or made available online. If you open a statement three weeks late and find a suspicious charge, you could already be 40 to 50 days into your window.

Jennifer found a $275 unauthorized charge while reviewing her statement on April 25. Her statement had closed on April 1 and was available in the Chase app that same day. By the time she noticed the charge, she had roughly 36 days left to file. If she had waited until mid-May to pull everything together, her window might have closed entirely.

The fix is simple. Review your Chase statement the same day it becomes available in the app. Don’t save it for the end of the month. A quick 10-minute review each billing cycle protects your right to act.

What Documentation to Gather Before You File

Don’t open the dispute form or call Chase before your documents are ready. A complete, organized file leads to faster resolutions and better outcomes.

Every dispute needs these basics:

- The transaction date and the exact amount charged

- The merchant name as it appears on your statement

- Your account statement shows the charge as fully posted

- Confirmation that the charge is posted, not still pending

You’ll also need any communication you had with the merchant. Emails, chat transcripts, and written refusal notices all count. Even a screenshot of an unanswered email can help establish your case.

Get organized before you start. Create a folder on your device and name each file clearly. Labels like 2026-04-12-duplicate-charge-email.pdf make uploading fast and accurate when you reach the documentation step in the dispute form. Scrambling through your downloads folder mid-submission causes errors and delays.

Documentation by Dispute Type

The exact records you need depend on which type of dispute you’re filing.

Fraud or unauthorized charge:

- A written statement confirming you didn’t authorize the transaction

- For physical card theft, a police report (optional, but helpful for larger amounts)

- A note about any other suspicious transactions around the same time frame

Billing error (wrong amount or duplicate charge):

- Original receipt or order confirmation showing the correct amount

- Your Chase statement showing the incorrect or duplicate charge side by side

Goods not received:

- Order confirmation with the expected delivery date

- Shipping or tracking details confirming non-delivery

- Correspondence with the merchant about the missing item

Merchant-refused refund:

- Proof of the original purchase

- Proof of your return or cancellation (email confirmation, return tracking number)

- The merchant’s written refusal to issue a refund

The more specific your documentation, the less work Chase has to do to verify your claim. That typically means a faster resolution in your favor.

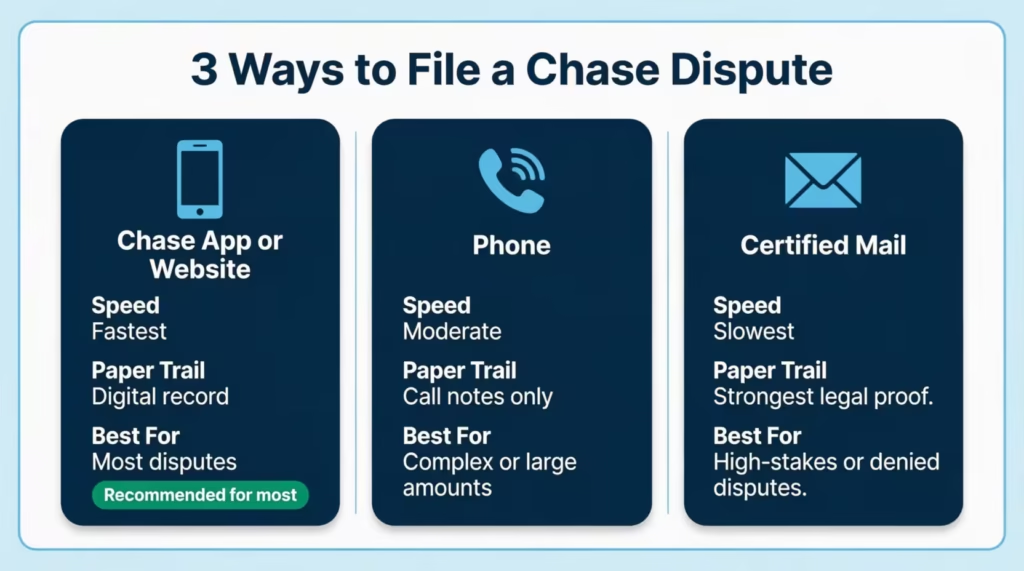

How to File a Chase Credit Card Dispute

Chase gives you three ways to file: online through the app or website, by phone, or by written mail. The right choice depends on your dispute type, the dollar amount involved, and how much documentation you need to submit.

One rule applies before you start: the charge must have fully posted to your account. If it still shows as “pending,” wait for it to post. Most credit card transactions post within 1 to 3 business days.

Filing Through the Chase App or Website (Step-by-Step)

For most cardholders, online filing is the fastest and most convenient option. It creates a digital record of your submission right away and gives you immediate access to the Chase Dispute Tracker.

- Sign in to your account at Chase.com or open the Chase mobile app.

- Navigate to your credit card account and find the transaction you want to dispute.

- Tap or click the arrow icon next to the charge to open the full transaction details.

- Scroll down and select “Dispute Transaction.”

- Choose the dispute reason from the dropdown menu that best fits your situation.

- Follow the prompts to add a description and upload your supporting documents.

- Review your submission and confirm.

After you submit, Chase displays a confirmation screen. You’ll also gain access to the Dispute Tracker, where you can monitor your case status at any time.

Both the website and the app work well for this. On a mobile device, the app is often easier because the camera integration lets you photograph and upload receipts directly without extra steps.

Filing a Dispute by Phone

Some cardholders prefer speaking with a representative, especially for larger amounts or more complex situations.

Call the number printed on the back of your Chase credit card. Follow the automated prompts to reach the disputes or billing inquiries department.

Before you call, have these ready:

- Your account number

- The transaction date and merchant name

- The disputed amount

- A summary of your supporting documentation

During the call, take notes. Write down the representative’s name, the time and date, and exactly what was confirmed. Always ask for a reference number for your dispute.

One important limitation: a phone call alone may not fully satisfy the FCBA’s written-notice requirement for billing errors. For amounts over a few hundred dollars, or in cases where you expect the merchant to push back, follow up your phone dispute with a written letter by certified mail as well.

Filing a Written Dispute by Mail

A mailed written notice provides the strongest legal protection under federal law. For larger amounts or disputes you expect to face resistance on, a certified letter creates a timestamped paper trail that a phone call or online form can’t fully replicate.

Your written notice must include:

- Your full name and account number

- The transaction date and exact dollar amount

- A clear statement that you’re disputing the charge

- A brief, factual explanation of what went wrong

Mail your letter to:

Chase Card Services P.O. Box 15299 Wilmington, DE 19850-5299

Send it by certified mail with a return receipt requested. That delivery confirmation shows exactly when Chase received your notice, which anchors your FCBA timeline.

The FCBA requires written notice within 60 days of the statement date. For billing errors, don’t rely solely on a phone call to meet this legal deadline. If you’ve already filed online, mailing a follow-up letter for high-stakes disputes adds a solid second layer of legal protection.

Pending Versus Posted Charges: When You Can File

If a suspicious charge still shows as “pending” in your account, you can’t file a dispute yet. Chase requires charges to be fully posted before they can be investigated.

Most transactions post within 1 to 3 business days. Hotel pre-authorizations and rental car holds can take a few extra days.

Here’s what to do while you wait. Take a screenshot of the pending charge with today’s date visible. Set a phone reminder for 3 to 5 business days. When the charge posts, file right away.

Don’t assume a pending charge will drop off on its own. Some authorizations do cancel without converting. But others post as full charges. Stay on top of it.

What Happens After You Submit a Chase Dispute

Once you file, Chase takes over the active investigation. Here’s exactly what that process looks like.

Chase contacts the merchant and requests documentation supporting the charge. The merchant typically has 7 to 21 days to respond, depending on the card network. Chase then reviews the merchant’s evidence against your claim. The final decision follows card network rules and weighs the documentation from both sides.

During this period, you’re not required to pay the disputed amount. But you are still responsible for paying the minimum monthly payment on your undisputed balance. Skipping that payment is the one action that can hurt your credit score while a dispute is active. Pay your minimum on time, every month, no matter what.

Provisional Credit: What It Is and When to Expect It

After you file a qualifying dispute, Chase will often apply a provisional credit to your account. This is a temporary credit for the disputed amount. It restores your available balance while the investigation runs.

Provisional credits typically appear within 7 to 10 business days of your filing date.

But here’s what most articles leave out: provisional credit is not a final decision. It’s conditional. If Chase’s investigation concludes in the merchant’s favor, the provisional credit will be reversed. The charge will reappear on your account.

Many cardholders stop monitoring after seeing the provisional credit. They assume the case is closed. It isn’t. Keep checking your account until Chase officially closes the case and confirms the credit is permanent.

💡Pro Tip: Set a calendar reminder for 45 days after you file. Log in to the Dispute Tracker and confirm a final decision is posted. If nothing’s changed, follow up through Chase’s secure message portal. Don’t let the case go quiet without a resolution.

How Long Does Chase Have to Resolve Your Dispute

Under the FCBA, Chase has up to two full billing cycles to resolve a billing error dispute. That period can’t exceed 90 days from the date Chase received your filing. Fraud disputes can run up to 120 days.

In practice, many disputes close faster. Clear unauthorized charge cases and obvious duplicate billing errors often resolve within 30 to 45 days. More complex cases, where the merchant provides competing documentation, may run closer to the 90-day limit.

If the 90-day window expires for a billing error dispute and Chase still hasn’t reached a decision, they violate the FCBA timeline. Document this breach in writing. Follow up through Chase’s secure message center and ask for a formal status update. Filing a CFPB complaint is also an option at that stage, which is covered in the next section.

How to Track Your Chase Dispute Status

Chase has a built-in Dispute Tracker inside your online account. It shows the real-time status of every open case.

Here’s how to access it:

- Sign in at Chase.com or through the Chase mobile app.

- Navigate to your credit card account.

- Find “Account Services” or the disputes section in the navigation menu.

- Open the Dispute Tracker to see all active and recent cases.

Common status labels and what they mean:

| Status | What It Means |

|---|---|

| Under Review | Chase is still investigating |

| Provisional Credit Issued | Temporary credit applied; case not yet closed |

| Resolved in Your Favor | Credit is permanent |

| Resolved Against You | Charge has been reinstated |

Check the tracker every 10 to 14 business days. If the status hasn’t changed in over 30 days, send a message through Chase’s secure portal to request an update.

What to Do If Chase Denies Your Dispute

A denial from Chase is not the final word. You have more steps available, and they carry real weight.

When Chase denies a dispute, they’re required to notify you in writing and explain the reason. Read that explanation carefully. It tells you exactly what evidence Chase relied on and why the merchant’s documentation was considered sufficient. That information is the foundation of your next move.

From here, you have two clear stages: an internal appeal directly to Chase, and, if that fails, escalation to federal regulators.

How to Appeal or Reopen a Denied Chase Dispute

Start by requesting the investigation file. Contact Chase in writing and ask them to provide all documents used in making their decision. This may include the merchant’s proof of authorization, a delivery confirmation, or a signed receipt.

Review the file carefully against your own documentation. Look for gaps, inaccuracies, or merchant claims you can directly address. For example:

- If the merchant submitted a signed receipt you don’t recognize, note any date or signature discrepancies in detail.

- If “proof of delivery” shows an address that isn’t yours, document that mismatch with your billing address records.

- If new evidence has come to light since your original filing, include it now.

Write a second written dispute and send it by certified mail to the Chase Card Services address listed above. Address the denial point by point. Attach all new or clarifying documentation. Keep copies of everything, including the certified mail tracking number.

A targeted, evidence-specific second letter is often more effective than the first. Vague general claims rarely succeed on appeal. Direct rebuttals with documentation do.

Escalation Options: CFPB, OCC, and Small Claims Court

If both internal attempts fail and you believe your claim has real merit, three external paths remain open.

Consumer Financial Protection Bureau (CFPB). Filing a complaint at consumerfinance.gov/complaint is free and takes about 15 minutes online. Banks respond to CFPB complaints with far more urgency than to internal escalations. The bureau acts as a mediator, and Chase must formally respond within a defined timeframe. For disputes in the $200 to $2,000 range, this is often the most effective next step available.

Office of the Comptroller of the Currency (OCC). The OCC regulates national banks, including Chase. If you believe Chase violated federal banking law during the dispute process, you can file a complaint at HelpWithMyBank.gov. Include your full dispute timeline, all supporting documentation, and copies of every denial letter Chase sent you.

Small claims court. If the disputed amount falls within your state’s limit (typically $5,000 to $10,000), you can file a case without an attorney. Most state courts have clear, accessible filing processes. Before pursuing this route, review your Chase cardholder agreement. It may contain an arbitration clause that affects your options for bringing a court claim.

How Disputing a Chase Charge Affects Your Credit Score

This concern stops more cardholders from filing than almost any other factor. Here’s the direct answer: disputing a charge with Chase does not affect your credit score.

The Fair Credit Reporting Act (FCRA) and Chase’s own policies protect the dispute process. No negative mark is added to your credit report simply because you questioned a charge.

Chase may add a notation to your report indicating the account is “in dispute.” This notation is removed once the investigation closes. It’s not a negative item. It carries no scoring penalty.

There’s one credit-related risk worth knowing. During the dispute, you don’t have to pay the disputed amount. But you must still pay the minimum due on your undisputed balance. If you stop making payments altogether, the unpaid undisputed portion can be reported as late. That does affect your score. The fix is straightforward: keep paying your minimum on the rest of your account while the case is open.

If the dispute resolves in your favor, there’s no credit impact. If it resolves against you and you accept the charge, there’s still no credit impact from the dispute process itself. The only real scoring risk comes from neglecting the rest of your account while you focus on the disputed charge.

One final note: if the dispute process somehow caused a late payment to be recorded on your credit report incorrectly, the FCRA gives you the right to fix it. You can file a separate dispute with each of the three credit bureaus (Equifax, Experian, and TransUnion) to have the error corrected.

Frequently Asked Questions (FAQs)

Can I dispute a Chase credit card charge that I already authorized?

Can I dispute a Chase credit card charge that I already authorized?

No. Charges you willingly approved do not qualify under the Fair Credit Billing Act. If you regret a purchase or are dissatisfied with a product you accepted and kept, you need to request a refund directly from the merchant.

Can I dispute a Chase charge from 2 years ago?

Almost certainly not. The Fair Credit Billing Act gives you 60 days from the statement date on which the charge first appeared. Once that window closes, Chase has no legal obligation to investigate the charge.

What are the common reasons Chase disputes get denied?

The most common reasons are missing documentation, filing after the 60-day deadline, or the merchant providing stronger evidence than the cardholder. Disputes filed for buyer’s remorse or for charges the cardholder authorized are also denied outright.

Why isn’t Chase letting me dispute a charge?

The two most common blockers are a charge that is still pending rather than fully posted, and a charge that falls outside the qualifying categories under the FCBA. Chase requires charges to post before they can be investigated, which typically takes 1 to 3 business days.

How long does it take to get money back after disputing a Chase charge?

A provisional credit often appears within 7 to 10 business days of filing. The full investigation can take up to 90 days for billing errors and up to 120 days for fraud, though straightforward cases often close in 30 to 45 days.

What is the best reason to dispute a Chase credit card charge?

The strongest disputes fall into one of three FCBA categories: an unauthorized transaction, a billing error such as a duplicate charge, or goods and services that were never delivered or were materially different from what was promised. Unauthorized fraud claims are the fastest to resolve because Chase’s $0 liability policy applies automatically.

How do you win a dispute with Chase?

File within the 60-day window, contact the merchant first for billing errors, and submit organized documentation that directly addresses your dispute reason. Specific evidence, such as a timestamped cancellation email or a side-by-side comparison of the billed amount versus the correct amount, consistently produces better outcomes than general claims.

Do I need a police report to dispute a fraudulent Chase charge?

No, a police report is not required to file a fraud dispute with Chase. It is optional, but it can strengthen your case for larger disputed amounts.

Can I dispute a Chase charge if I already paid my statement balance?

Yes. Paying your statement balance does not forfeit your right to dispute a charge. The 60-day window runs from the statement date the charge appeared, regardless of whether you paid the bill.

Bottom Line

Disputing a charge on your Chase card doesn’t have to be stressful. The process has clear steps and solid legal backing. Confirm your charge qualifies, contact the merchant for billing errors, and file within the 60-day window. Gather your documents before you submit, and track your case after you file. If Chase denies your claim, a written appeal and a CFPB complaint are both effective options.

Based on the protections in place, acting early with solid documentation gives you the best chance of getting your money back.

Know someone who just found an unexpected charge on their statement? Sharing this guide could help them act before their filing deadline closes.