We’ve all been there. You slide your debit card into the ATM, ask for a big cash withdrawal, and the screen throws back “transaction denied.” Maybe you’re closing on a used car, paying a moving crew, or leaving for a trip in the morning. Suddenly the daily cap on your account feels like a wall. Many people don’t even know if the Chase ATM withdrawal limit can be raised, which channel to use, or how long it takes.

The good news: YES, Chase will usually let you raise your cash withdrawal limit, either for one day or on an ongoing basis.

In this guide, you’ll get the exact steps, the info Chase will ask for, what boosts your approval odds, and same-day cash options if you can’t wait.

Key Takeaways

This guide explains how to increase your Chase ATM withdrawal limit, including current limits by account tier and ATM type, request steps through the app, phone, or a branch, and same-day cash alternatives.

Core Facts:

- Chase ATM cash limits vary by ATM type, ranging from roughly $500 to $1,000 at non-Chase ATMs up to $3,000 at in-branch lobby ATMs for many accounts.

- Account tier sets the baseline limit, from $500 to $1,000 for Chase Total Checking up to $3,000 for Chase Private Client Checking.

- Temporary limit increases can be requested through the Chase Mobile app, chase.com online banking, or by phone at 1-800-935-9935, and often apply within minutes.

- Permanent limit increases typically require a branch visit with government-issued photo ID or an upgrade to a higher account tier.

- Approval depends on factors including account tenure, clean account standing, a clear reason for the request, and giving advance notice before the cash is needed.

- Same-day cash options that bypass the ATM limit include cash back at checkout (up to $300 at some stores) and in-branch teller withdrawals limited only by account balance.

Best for:

- Chase customers who need a one-time higher cash withdrawal for a specific event like a car purchase or contractor payment.

- Chase customers with ongoing higher cash needs, such as landlords or tradespeople, who want a permanent limit change or account upgrade.

- Anyone whose limit request was denied and needs same-day cash through checkout cash back or a branch teller instead.

Chase ATM Withdrawal Limits by Account Type and ATM Location

Before you request an increase, it helps to know the number you’re actually working with. Chase does not publish one flat cap for every customer. Your daily cash limit depends on two things: the account you hold and the type of ATM you use.

Limits vary by ATM location

Chase treats different ATMs differently. Withdrawals from a Chase ATM inside a branch lobby usually allow the highest daily amount. Chase ATMs on the outside of a branch or in stand-alone kiosks often cap you at a lower figure.

And when you use a non-Chase ATM, both Chase and the ATM owner can enforce their own limits, which stack. Chase confirms that daily fund transfer limits apply at its ATMs and that “withdrawals made with any of your ATM or debit cards count toward every card’s Chase In-Branch ATM Limit,” per its official Clear & Simple Guide for Total Checking.

Reported ranges from Chase users and industry trackers look roughly like this:

| ATM Type | Typical Daily Cash Limit |

|---|---|

| Chase in-branch (lobby) ATM | Up to $3,000 for many accounts |

| Chase exterior / 24-hour ATM | Often $1,000 to $2,000 |

| Non-Chase ATM (Allpoint, MoneyPass, other networks) | Often $500 to $1,000, plus network cap |

These are ballpark figures. Your real number can be higher or lower.

Account tier changes the baseline

Your account type is the other big factor. A basic Chase Total Checking customer usually starts with a lower daily cash cap than a Sapphire Checking or Private Client customer. Data from MyBankTracker’s Chase ATM Withdrawal Limit guide shows that debit card spending limits at Chase can range from around $300 up to $7,500 based on the account tier and history. Premium accounts also tend to unlock higher daily withdrawal limit amounts at Chase ATMs.

Here is a general picture by tier:

| Chase Account Tier | Typical ATM Daily Cash Limit |

|---|---|

| Chase Total Checking | $500 to $1,000 |

| Chase Premier Plus Checking | $1,000 to $2,000 |

| Chase Sapphire Checking | Around $2,000 |

| Chase Private Client Checking | Up to $3,000 |

How to check your exact personal limit

Instead of guessing, check the number tied to your own card. Three places show it:

- The Chase Mobile app: Sign in, open the account, and look under transaction limits or debit card settings.

- Chase online banking at chase.com: Under “Payment preferences,” pick “Manage transaction limits,” as Chase explains on its Manage Transactions help page.

- Your cardholder agreement: The booklet or PDF you got when you opened the account.

If the limit still isn’t clear, call the number on the back of your debit card. A rep can quote the exact figure.

📌 Did You Know: A single limit applies across all cards on the same account. If you and a spouse both have debit cards on one Chase Total Checking account, together you share the daily cash cap. It’s not one cap per card.

Can Chase ATM Withdrawal Limits Actually Be Increased?

YES. Chase clearly states on its own site that “some banks may allow you to request a temporary or permanent increase in your ATM withdrawal limit,” per its ATM Withdrawal Limit education page. Chase does allow both types of changes.

Here is what to expect at a high level:

- A temporary limit increase covers a short window, often just one day or a few days. You use it for a one-time need like a car down payment or a wedding vendor. After the window ends, your limit snaps back to normal.

- A permanent limit increase stays on your card. You use it when your cash needs are ongoing, like a landlord who collects rent in cash or a contractor.

- The size of the raise is usually a few hundred to a few thousand dollars above your default, not unlimited. So don’t expect to jump from $500 to $10,000 in one call. Chase reviews your account first.

To sum it up: an increase is very possible, but it’s a request, not a right. What you ask for, why you ask, and how your account looks all matter. The next sections walk you through both paths, step by step.

How to Request a Temporary Withdrawal Limit Increase

A temporary bump is the fastest and easiest kind of change. Ask for it when you need extra cash for a single event, and then you’re fine with going back to your normal cap. Think one-time large purchases, a short vacation, or a family emergency.

Chase gives you three channels for a temporary Chase ATM limit increase. The mobile app is usually quickest, but not every account shows the option. If it doesn’t, phone or online banking works too.

Requesting via the Chase Mobile App

The app is the top pick for most readers because it’s fast and self-service. Download the free Chase Mobile app from the App Store or Chase Mobile on Google Play if you don’t already have it.

Steps to request a higher ATM limit at Chase inside the app:

- Sign in to the Chase Mobile app.

- Tap the checking account tied to your debit card.

- Scroll to “Account services” or your card settings.

- Look for “Manage transaction limits” or “Change debit card limits.”

- Tap the ATM withdrawal line and adjust the amount for today or the coming days.

- Confirm the change and save the confirmation screen.

If the option is present, the change often goes live right away. If you don’t see the “manage limits” option, that means your account type or debit card doesn’t allow self-service changes. In that case, use one of the two channels below.

Requesting via Chase.com Online Banking

The desktop path mirrors the app. Sign in at chase.com, then follow the steps Chase lists on its own Manage Transactions page:

- Sign in to your account at chase.com.

- Open the checking account linked to your debit card.

- Click “Account services,” then “Payment preferences.”

- Choose “Manage transaction limits.”

- Pick the ATM withdrawal line and enter your new amount.

- Confirm. You’ll see a success message and a confirmation email.

Online banking is helpful when you want a larger screen to review terms. The confirmation email is also handy proof if you have to argue with a machine later.

Requesting by Phone

If your app and online options don’t show a self-service increase, call Chase. Two numbers work:

- The number on the back of your Chase debit card.

- Chase’s main customer service line: 1-800-935-9935 (personal banking).

What to say to the rep:

- “I’d like a temporary ATM cash withdrawal limit increase.”

- Give the date or dates you need the higher amount.

- State the reason clearly (car purchase, contractor payment, medical bill).

- Give the exact new daily amount you want.

Have your account number, debit card, and ID handy. The rep will run a quick review of your account standing and, in most cases, apply the change within minutes.

💡 Pro Tip: Ask the rep to confirm both the new limit and the exact date the higher cap will end. Some readers hit a wall on day two because the temp increase was set for only 24 hours.

How to Request a Permanent Withdrawal Limit Increase

A permanent change makes sense when your cash needs are ongoing, not just a one-off event. Landlords, tradespeople, small business owners, and folks who prefer cash budgeting are good fits. A permanent limit increase takes more review than a temporary one, and Chase often wants a live human to verify who you are and why you need the change.

Two paths lead to a lasting raise: a branch visit or an account tier upgrade.

Requesting In Person at a Branch

The branch route is the most reliable for a permanent Chase debit card withdrawal limit increase. A banker can pull your file, check your history, and set a new cap on the spot in many cases.

Bring these items:

- A government-issued photo ID (driver’s license, passport, state ID).

- Your Chase debit card.

- Your account number if you have it.

- Any paperwork that shows why you need the higher limit, like a rental lease or contractor invoice, if it helps your case.

At the branch, ask to speak with a personal banker. Tell them you want a permanent ATM cash withdrawal limit increase and share the amount plus the reason. The banker will confirm your ID, review your account, and either approve it, submit it for review, or suggest an account tier upgrade.

Use the Chase branch locator to find the nearest office and its hours.

Upgrading Your Account Tier for a Higher Baseline Limit

Sometimes the best fix isn’t a limit request; it’s a different account. Higher-tier accounts come with higher default caps and more perks. If you keep asking for the same increase every month, an upgrade often makes more sense.

Here’s how tiers tend to compare on ATM defaults:

- Chase Total Checking: entry-level, lowest ATM default.

- Chase Premier Plus Checking: mid-tier, higher default.

- Chase Sapphire Checking: premium, higher default plus ATM fee rebates.

- Chase Private Client Checking: top-tier, up to $3,000 daily ATM withdrawal reported by Johnny Jet’s Chase Private Client comparison, plus a dedicated banker.

When to upgrade instead of asking for repeated increases:

- You need higher cash access at least twice a month.

- You keep a balance that meets the next tier’s minimum.

- You’d also use the extra perks: ATM fee refunds, priority service, wire fee waivers.

A banker can move you to a new tier in about 20 minutes. Once the new tier is live, your default limit goes up without you needing to file another request.

What Information Chase Will Ask for When You Request an Increase

Chase treats a limit request like a small verification check. The rep or banker will confirm you are who you say you are, look at your account standing, and then decide. Come prepared and the whole thing wraps up in one call or one visit.

Expect these questions:

- Reason for the increase. Be direct. “I’m buying a used car from a private seller on Saturday and need $2,500 in cash” works better than “I just need more money.” A clear, real reason helps the rep push it through.

- Account/ID verification details. They’ll ask for your name, date of birth, the last four digits of your Social Security number, your address, or a security question. In branch, they’ll scan your ID. On the phone, they may text a one-time code to the number on file.

- One-time or ongoing need. Chase wants to know if you’re asking for a single-day change or a permanent raise. Say it clearly up front. This shapes which review path they use.

- Exact new amount. Have a specific number. “I’d like a one-day increase to $2,500” is far better than “I need more.”

- Timing window. For a temporary bump, state the date. Say “Saturday, October 12” instead of “this weekend.”

Some agents will also glance at your cardholder agreement terms to check that the increase is allowed for your card type. Not every debit card supports the same maximum, so if they push back, ask them to quote what the agreement allows.

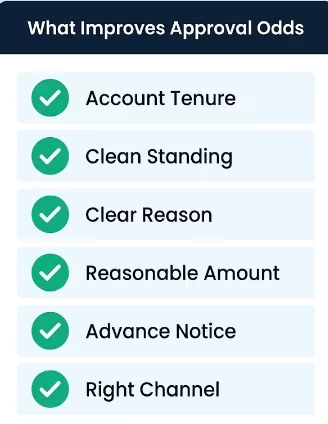

What Improves Your Approval Odds

Approval isn’t automatic. Chase looks at a few signals before saying yes. The reader who preps for these has a much smoother call.

Account tenure. Longer relationships get more benefit of the doubt. If you’ve been a Chase customer for five years, a rep is more likely to push through a bump than for a customer who opened the account last month.

Clean account standing. No recent overdrafts, no fraud flags, and a positive balance history all help. A quick check in the Chase Mobile app for any red flags before your call is smart.

A clear, believable reason. “I’m paying a moving company on Friday” is specific. “I might need some extra cash” is not. Reps hear vague reasons every day. A concrete story about a real event moves you up the trust ladder.

A requested amount that fits your account activity. If your account usually holds $3,000 and you ask for a $9,500 one-day cash pull, that’s a stretch. Ask for what your history supports.

Advance notice. A customer service request made three days before the cash need almost always goes better than one made 20 minutes before you hit the ATM. If you can, plan the call earlier in the week.

Correct channel. Some readers get told no by the app, but yes by a banker. If self-service fails, don’t stop there. Move to phone or branch.

⚠️ Mistake to Avoid: Don’t ask for the highest number you can think of “just in case.” Reps see the reach and often deny the whole request. Ask for the actual amount you need, plus a small cushion.

What to Do if Your Request Is Denied

A denial is not the end of the road. Chase agents work off scripts and account rules, and a different agent, channel, or angle can still get you to yes.

Try these steps in order:

- Switch channels. If the app said no, try the phone. If the phone rep said no, walk into a branch. Bankers in a branch often have more discretion than a call center rep, and they can pull the full picture of your account. A quick trip beats losing a deal.

- Escalate inside Chase. On a call, ask politely, “Can you please connect me to a supervisor or a relationship banker?” Supervisors sometimes have higher approval ceilings. In a branch, ask for the branch manager if the personal banker says no.

- Sharpen your reason. A vague ask often gets denied. A clear, documented reason often flips it. If you’re paying a contractor, bring the invoice. If you’re closing on a private car sale, bring the bill of sale draft.

- Ask for the specific reason for denial. Chase won’t always spell it out, but sometimes they will. If the block is “account too new,” you know to wait. If it’s “recent overdraft,” you know to clean up first.

- Consider a tier upgrade. If your account keeps hitting the ceiling, moving to a premium account tier solves the problem for good. See the “Upgrading Your Account Tier for a Higher Baseline Limit” section above for the details.

- Try again after a short cool-down. If you were denied today, try again in a week with a cleaner account or a different reason. A hard “no” is rarely permanent.

If none of that works and you still need cash, jump to the next section for same-day options.

Getting Cash Today if You Can’t Wait for an Increase

Sometimes the deal is tonight, and the request review is next week. You’ve got two solid same-day options that don’t depend on any limit change: cash back at checkout and an in-branch teller withdrawal. Both work while your permanent fix is still processing.

Cash Back at Checkout

Grocery stores, drug stores, and big-box stores let you tack cash onto a debit card purchase. This is a cash advance alternative for smaller amounts, and it doesn’t touch your ATM daily cap.

How to use it:

- Bring a small item to the register, like a pack of gum.

- Pay with your Chase debit card and pick “Debit” (not credit).

- Enter your PIN when asked.

- The screen or cashier asks, “Cash back?” Say yes and pick the amount.

- The cashier hands you the cash with your receipt.

Common store caps:

| Store | Typical Cash Back Cap |

|---|---|

| Walmart | Up to $100 |

| Target | Up to $40 |

| CVS | Up to $35 |

| Kroger | Up to $300 |

| Publix | Up to $100 |

You can chain a few stores together in one afternoon if you need more than one store’s cap. Just note this pulls from your daily debit purchase limit, not your ATM cap, so it stays clear of that ceiling.

In-Branch Teller Withdrawal

For bigger same-day needs, the branch teller is your friend. A teller isn’t held to the ATM daily cap. Instead, they’re limited by your account balance and Chase’s internal cash-handling rules.

What to bring:

- Your government-issued photo ID.

- Your Chase debit card or account number.

- Any paperwork that supports the purpose, though it’s rarely required.

A few tips:

- For very large amounts, call ahead. Branches don’t always keep $10,000 or more in the drawer. A quick call to your local branch, or a chat with a customer service representative, gives them time to order the cash from the vault.

- Go earlier in the day. Late-afternoon branches often run low on high bills.

- Try a Chase ATM outside a branch only for smaller amounts. Even a non-Chase ATM won’t help here because those tend to have lower caps than Chase’s own.

Between cash back and the teller, most readers can cover any same-day need up to their full account balance without a formal limit change.

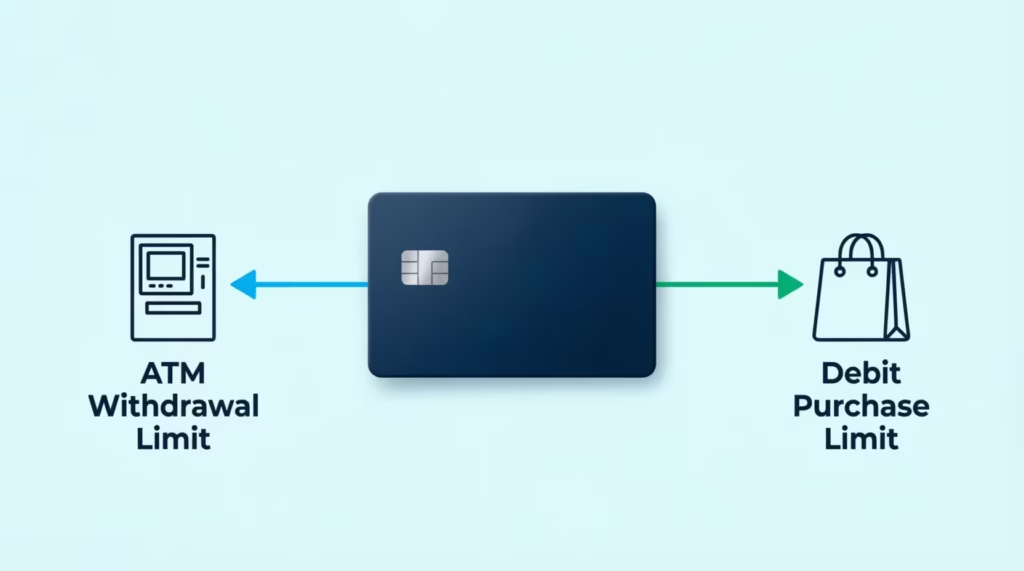

Debit Card Purchase Limits vs. ATM Withdrawal Limits

Two limits share your debit card, and confusing them causes a lot of wasted phone calls. Here’s the short version so you don’t misapply this article.

- ATM withdrawal limit: The most cash you can pull from an ATM in one day. This is the focus of this guide.

- Debit card purchase limit: The most you can spend on the same card at stores, restaurants, and online in one day. Chase confirms these are separate on its own ATM withdrawal limit page, which notes “there may also be daily purchase limits on your debit cards separate from the ATM withdrawal limit.”

They’re managed separately. Raising one does not raise the other. If you’re paying a large bill with your card at a store, and the card is declined, that’s a debit card purchase limit issue, not an ATM problem. Ask Chase to review that limit on its own.

The good news: both live in the same “Manage transaction limits” screen in the app and on chase.com. So if you’re already in there raising one, you can adjust the other in the same session.

Frequently Asked Questions (FAQs)

What is Chase’s daily ATM withdrawal limit?

Your limit depends on your account tier and which ATM you use, ranging from around $500 to $3,000 daily. Chase Total Checking customers typically see $500 to $1,000, while Private Client accounts can reach up to $3,000.

Can I withdraw $1,000 from a Chase ATM?

In most cases, yes, especially at a Chase in-branch ATM where limits often reach $3,000. Exterior or non-Chase ATMs may cap you lower, often between $500 and $2,000, so check your specific limit in the Chase app first.

Can I withdraw $3,000 from a Chase ATM?

Withdrawing $3,000 in one day is possible mainly through a Chase in-branch lobby ATM, which allows up to $3,000 for many accounts. Private Client Checking customers have this as their typical daily ATM cap.

Can I withdraw $10,000 from Chase in one day?

An ATM won’t allow this since daily caps top out around $3,000 even for premium accounts. For $10,000, visit a branch and use an in-branch teller withdrawal, which isn’t held to the ATM daily cap.

How do I withdraw a large amount of cash from Chase?

For same-day large withdrawals, an in-branch teller withdrawal works best since it’s limited by your account balance, not the ATM cap. Bring photo ID and call ahead for amounts over $10,000 so the branch can prepare the cash.

Are there ways to get cash beyond my ATM withdrawal limit?

Yes, cash back at checkout when using your Chase debit card as a purchase doesn’t count against your ATM cap. Stores like Kroger allow up to $300 in cash back, and this pulls from your debit purchase limit instead.

How do I increase my Chase debit card ATM limit?

Request a change through the Chase Mobile app under “Manage transaction limits,” by phone at 1-800-935-9935, or in person at a branch. Temporary increases can go live within minutes, while permanent changes usually need a branch visit.

What is the daily spending limit for Chase separate from ATM withdrawals?

Chase debit cards have a separate purchase limit for spending at stores and online, distinct from the ATM cash withdrawal limit. Raising one does not raise the other, though both can be adjusted in the same “Manage transaction limits” screen.

Can I withdraw $5,000 from an ATM in one day?

This exceeds typical Chase ATM caps, which max out around $3,000 even for top-tier accounts. To access $5,000 same-day, use an in-branch teller withdrawal instead, since it draws from your account balance rather than the ATM limit.

How long does it take for a Chase ATM limit increase to take effect?

A temporary increase through the app or phone often applies within minutes of approval. A permanent increase or account tier upgrade at a branch typically takes about 20 minutes to process.

Wrapping Up

Raising your daily cash cap at Chase comes down to three things: know your current limit, pick the right channel, and give a clear reason. A temporary bump is quick and often works through the app or phone. A permanent change usually needs a branch visit or an account upgrade. If today’s cash need can’t wait, cash back at checkout and teller withdrawals bridge the gap.

To get the best results from Chase, it’s smart to call or visit a few days in advance. Be clear about the dollar amount you need and give a real reason for your request.

Bookmark this guide, and if you know someone about to buy a car, pay a contractor, or move cross-country, share it. It could save them a wasted trip and a lot of stress.